Download to read offline

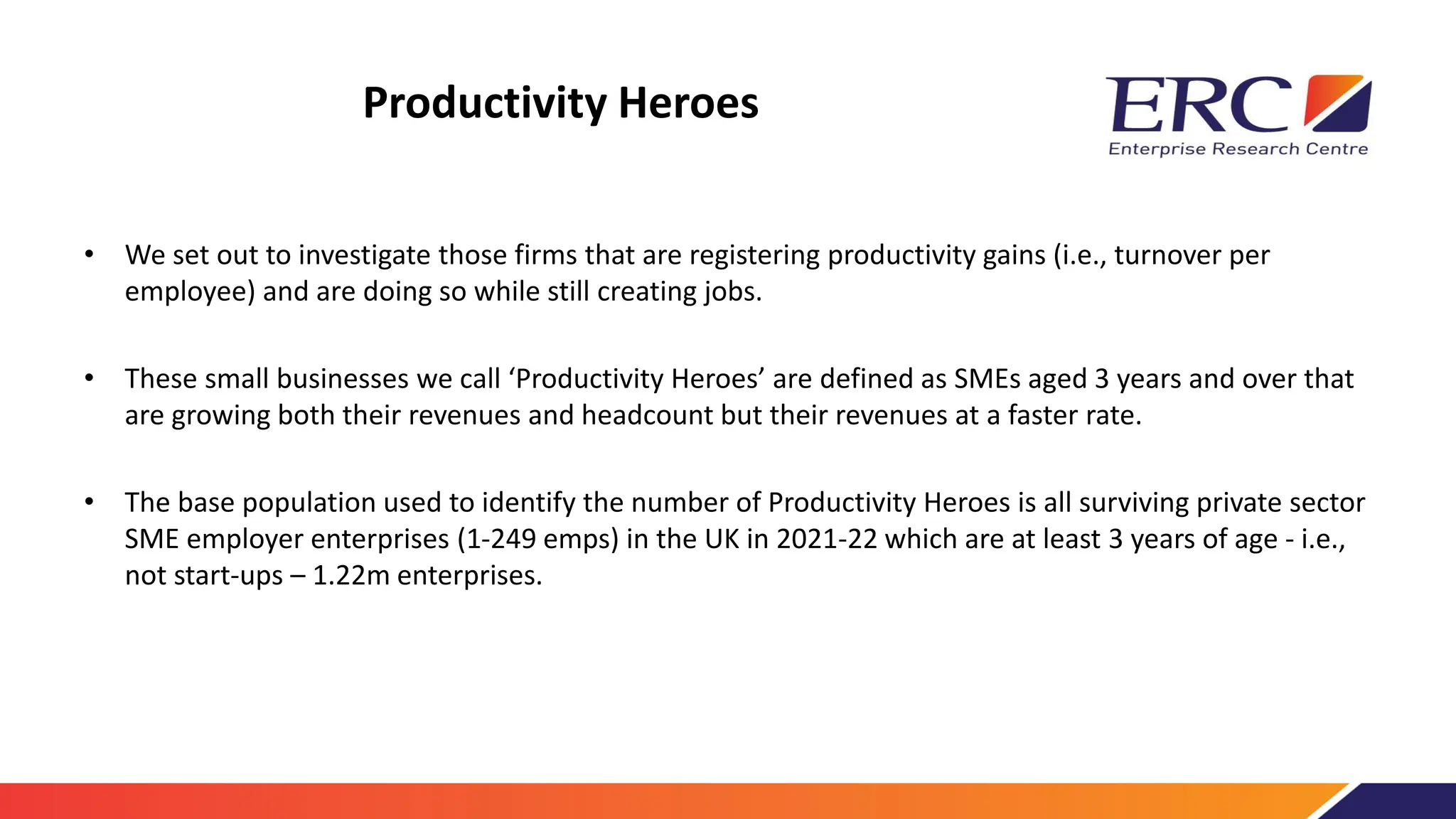

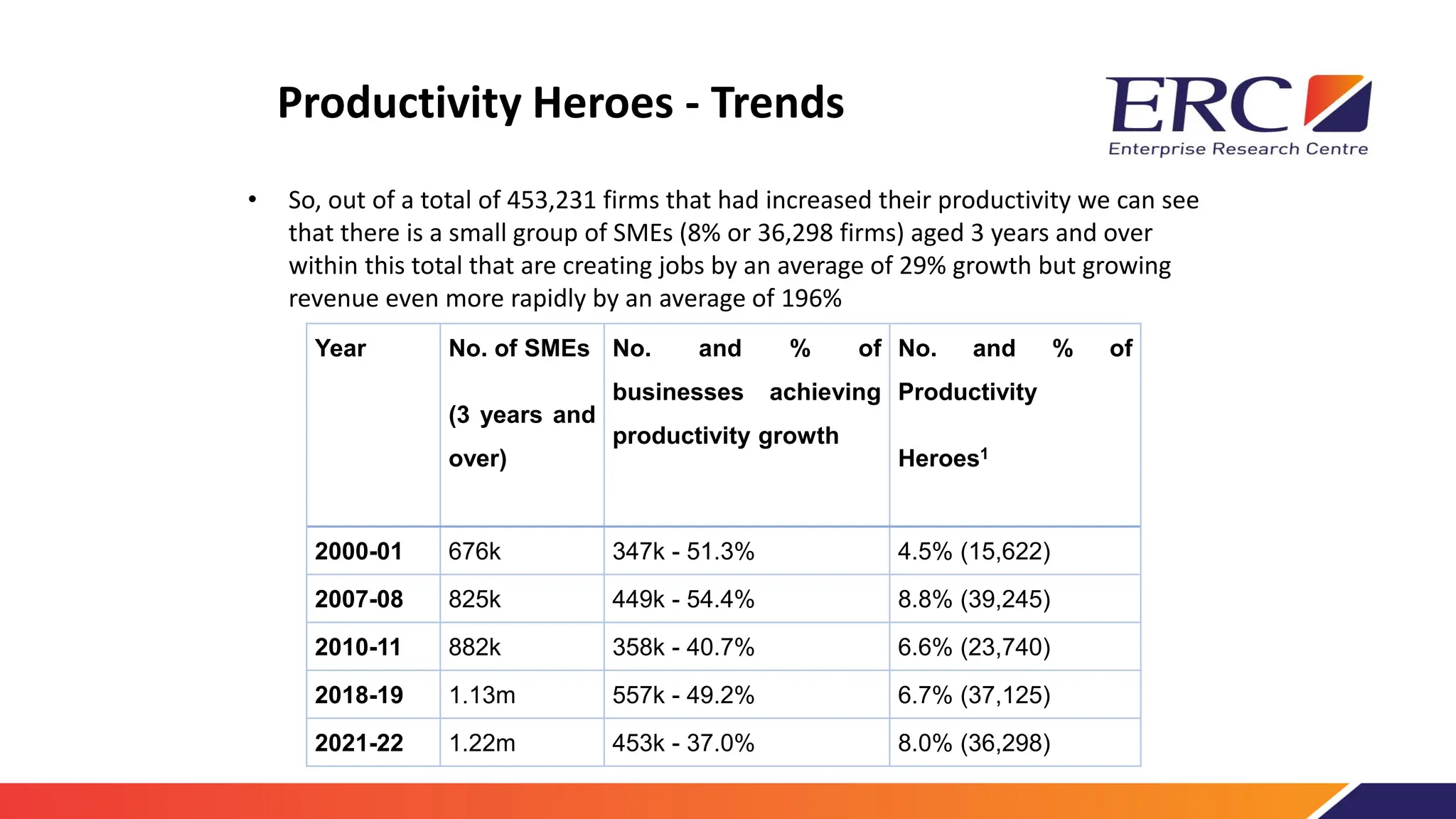

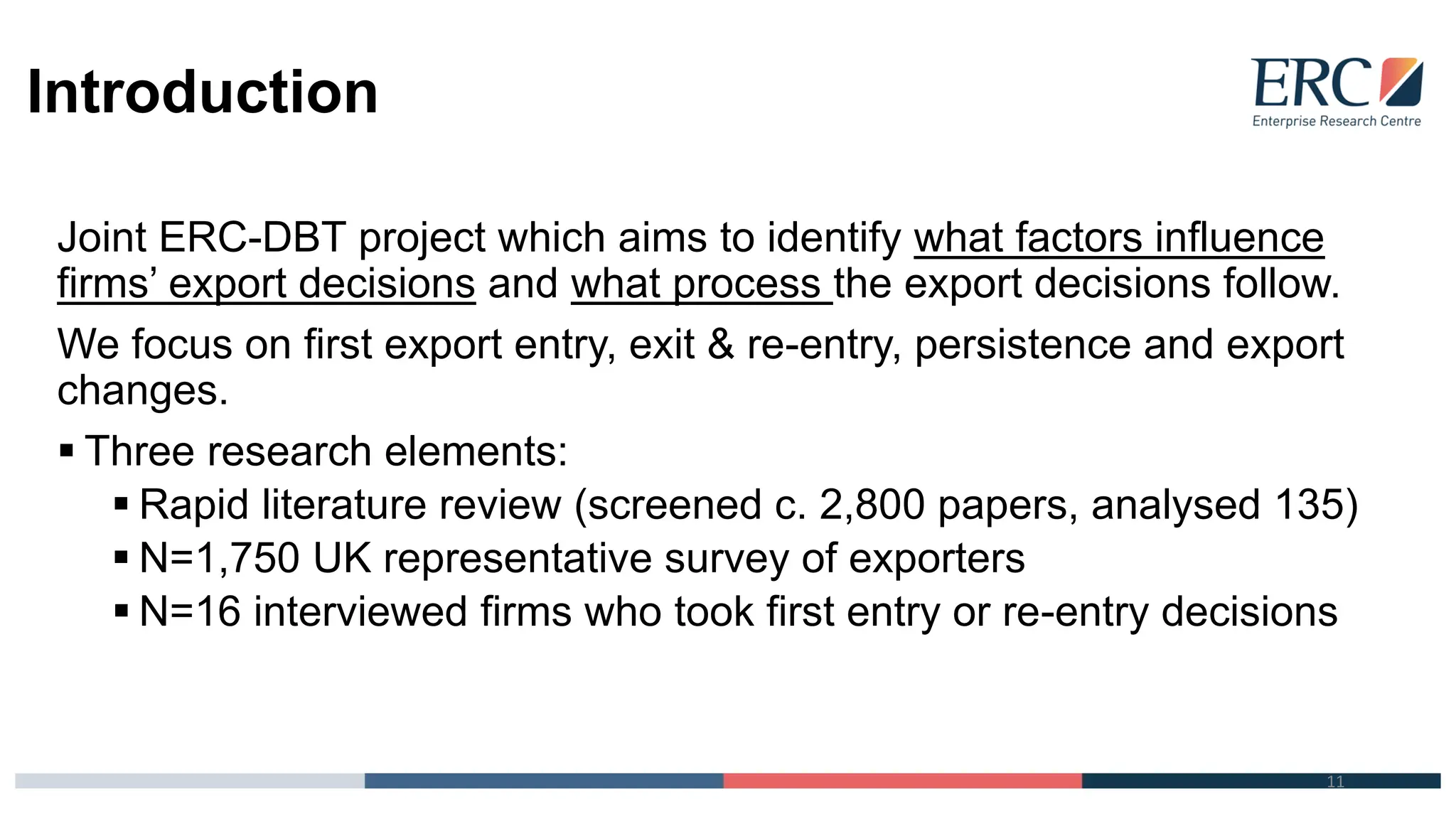

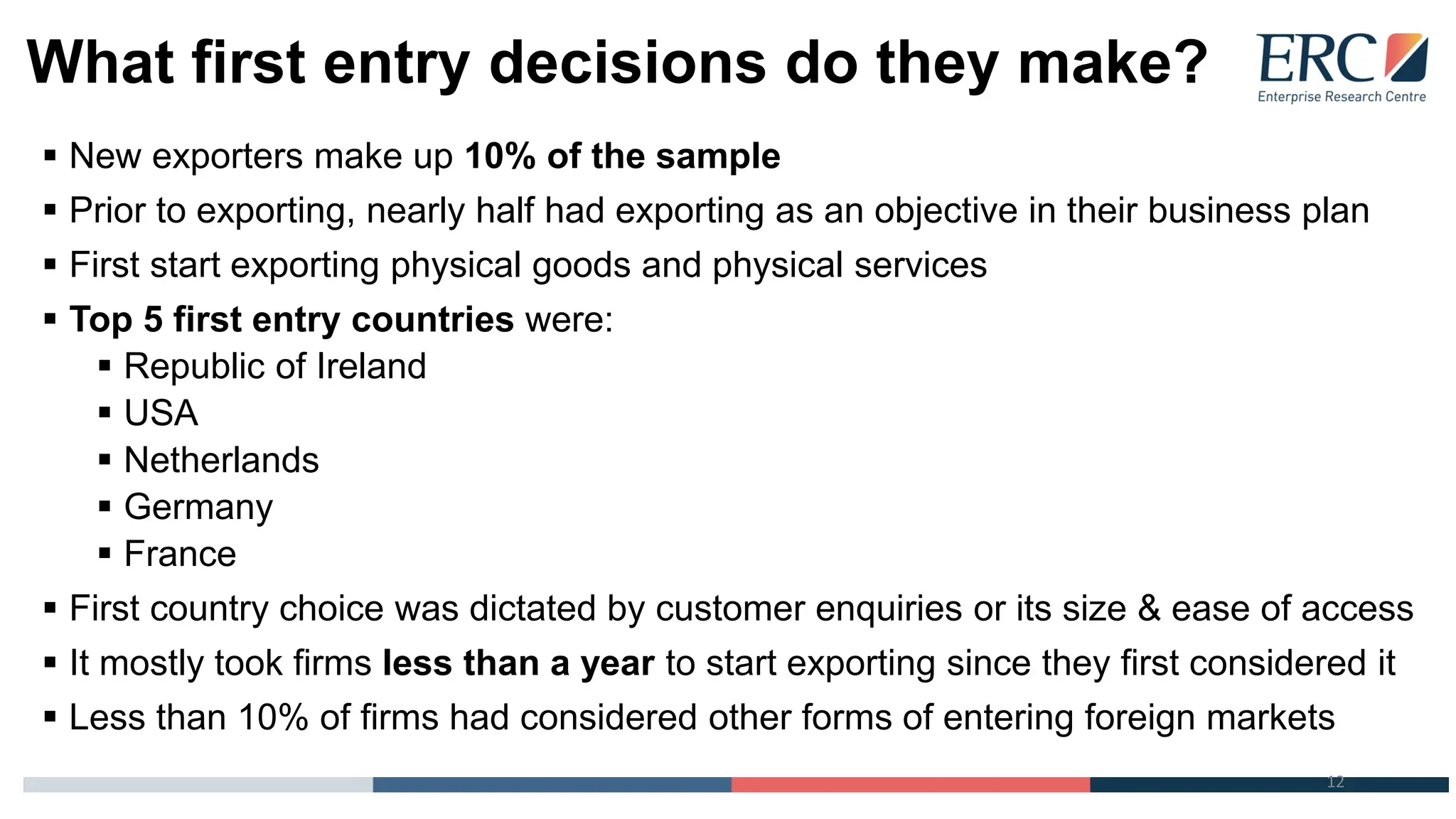

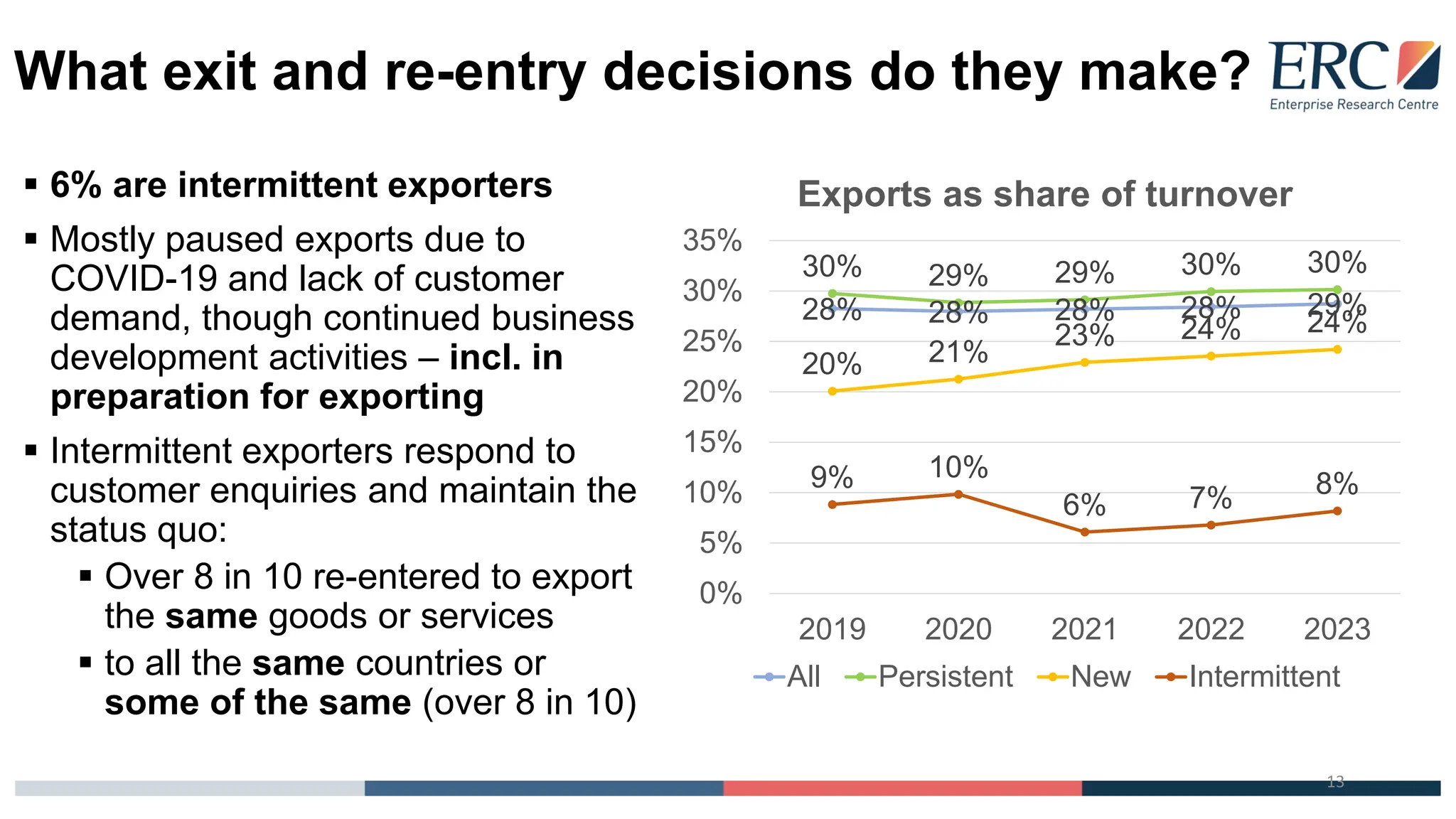

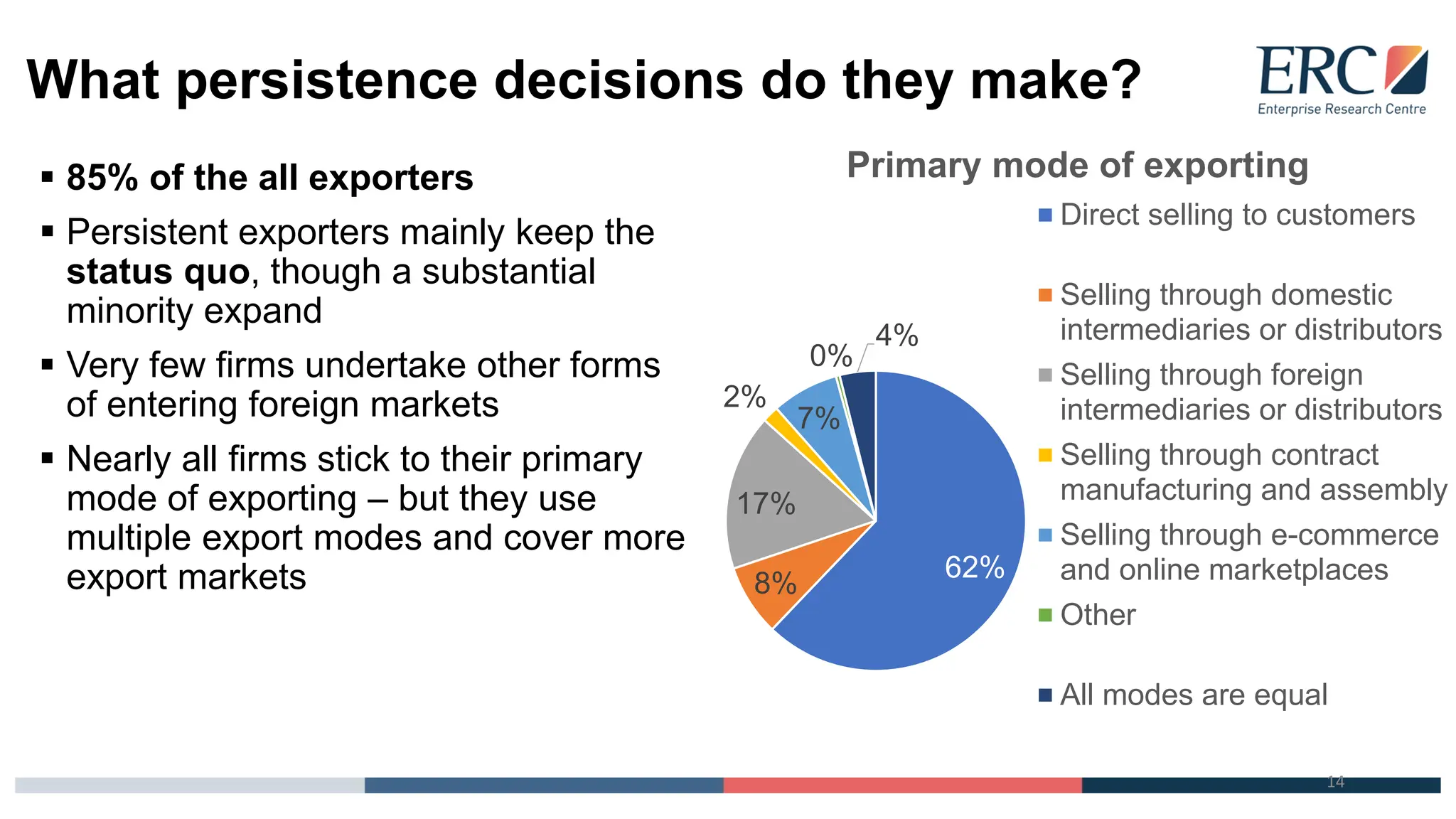

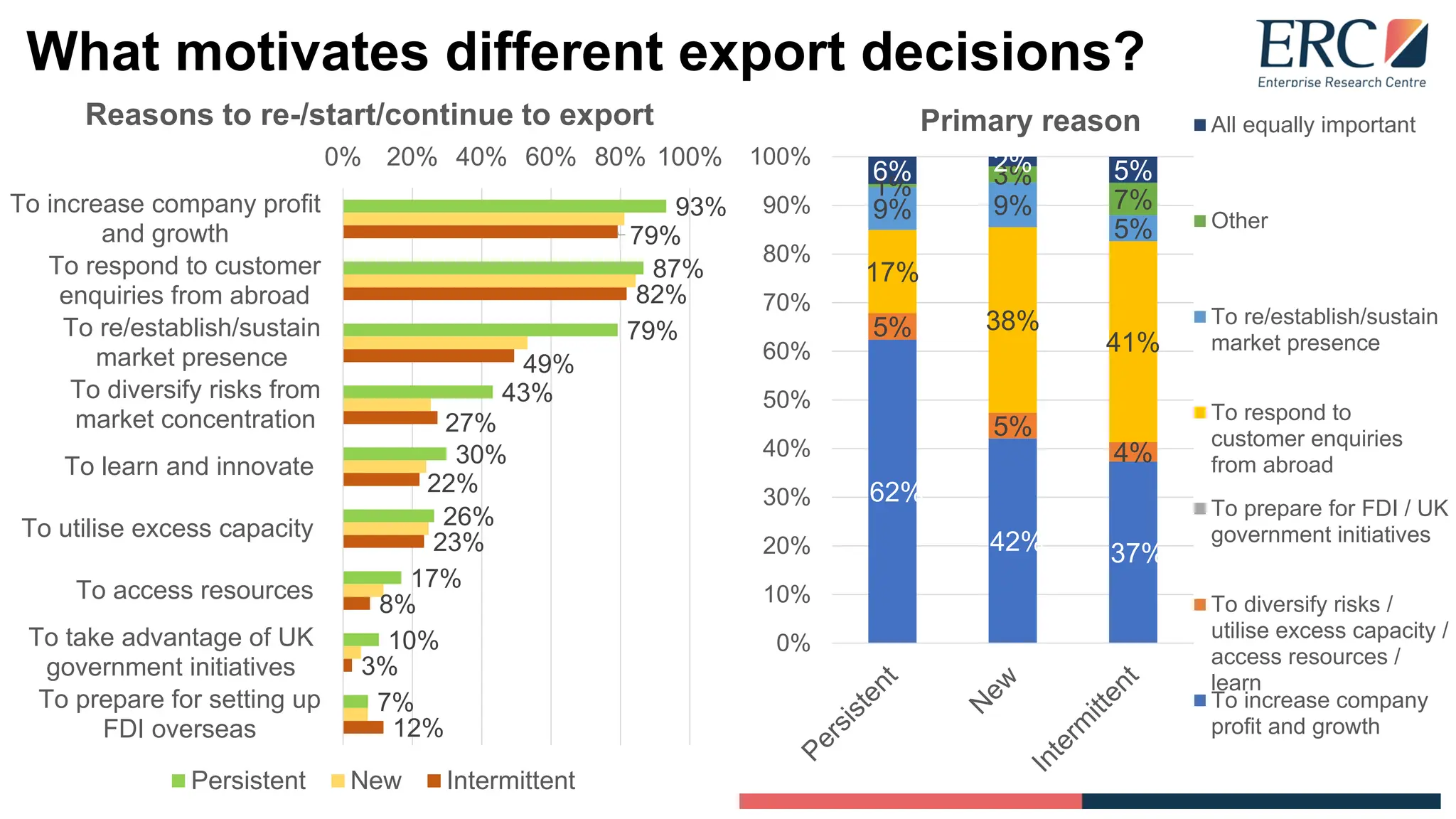

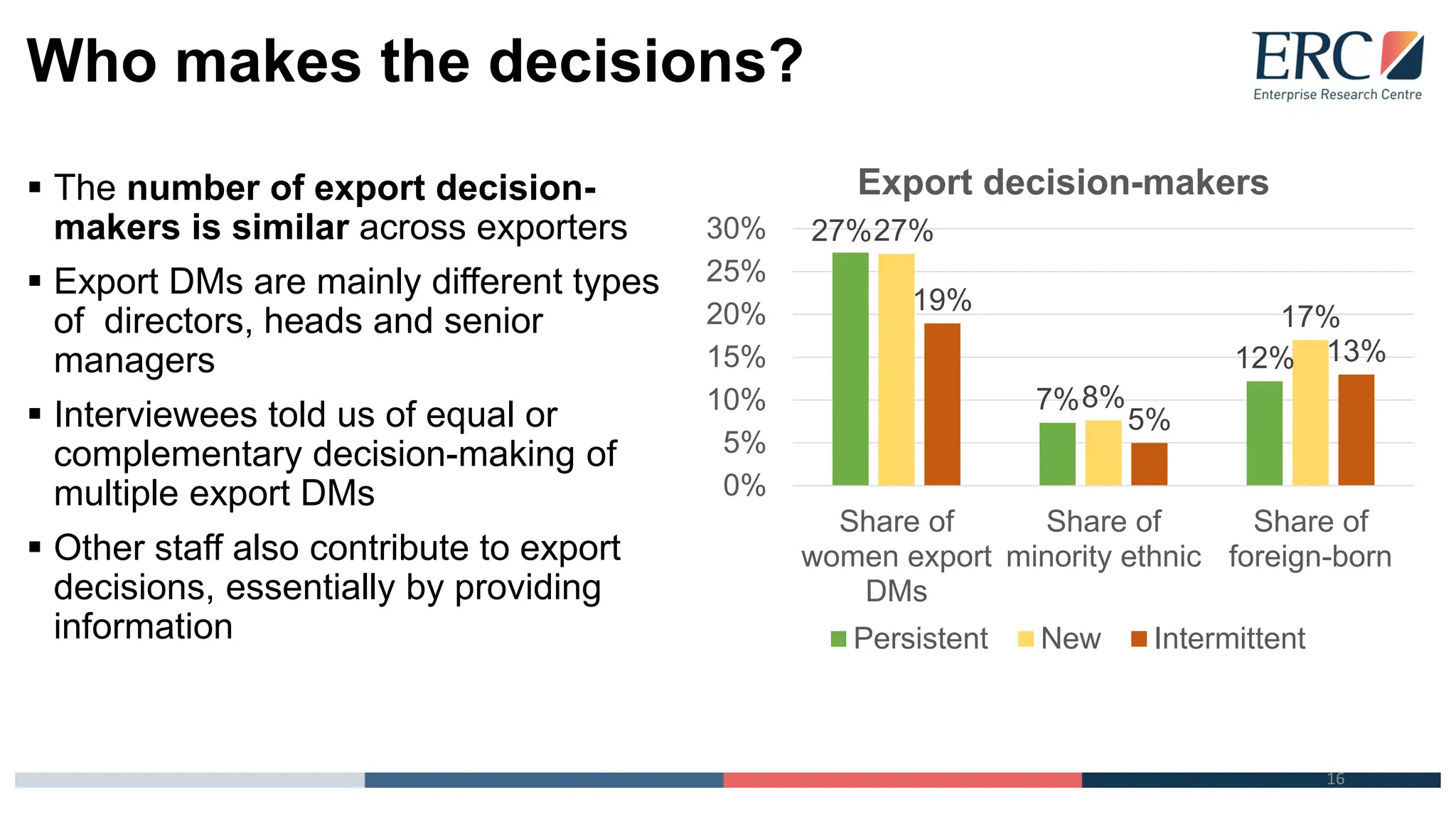

This document summarizes several presentations from the ERC Research Showcase on February 22nd 2024. The first presentation identified a small group of UK SMEs called "Productivity Heroes" that have significantly increased turnover, jobs, and productivity at the same time between 2021-2022. The next steps are to track their long-term performance and understand the drivers of their productivity gains through qualitative research. The second presentation discussed research on UK firms' export decisions. It found customer demand is important at all stages of exporting. Exporting firms make multiple decisions over time to first enter markets, exit and re-enter, and persist in exporting. Support should target firms at different points in their export journey.