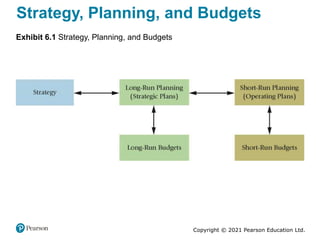

The document discusses budgets and the budgeting process. It defines a budget as a quantitative plan for a future period that includes both financial and non-financial aspects. Budgets help managers communicate goals, measure performance, and motivate employees. The budgeting process involves strategic planning, developing operating and financial budgets, and comparing actual results to the budget. The master budget is the core document and includes an operating budget with schedules for revenues, production, costs, and an income statement, as well as a financial budget.