Download to read offline

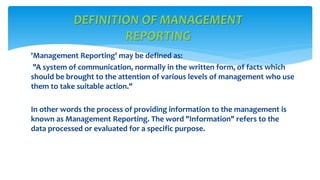

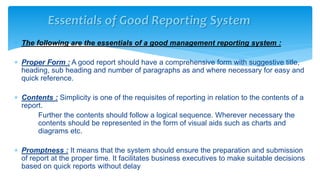

Management reporting is defined as a written system of communication that provides facts and information to various levels of management to assist them in decision making. An effective management reporting system has several essential characteristics, including using a proper reporting form with a clear structure, containing logical and simple content presented visually when needed, providing reports promptly, enabling comparability of actual and budgeted performance, maintaining consistency in accounting principles over time, keeping the style and presentation simple, and allowing flexibility to adjust to users' needs.