Lsi 09.2

The document advertises the 2nd Life Settlements & Longevity Summit conference. It provides details on: - Speakers including industry leaders, investors, medical experts and insurance commissioners who will discuss topics like regulatory developments, investment trends, medical advancements and more. - Sessions that will explore issues like the global investment picture, restoring confidence in life expectancies, an economist's response to regulatory proposals, and perspectives from pension funds. - Interactive elements including a think tank limited to pension/endowment funds, and roundtable discussions on pressing issues in the industry. - The goal of helping investors navigate opportunities and challenges to achieve superior returns through investments in life settlements and longevity-linked assets.

Recommended

More Related Content

What's hot

What's hot (20)

Viewers also liked

Similar to Lsi 09.2

Similar to Lsi 09.2 (20)

More from Dhaval Thakur

More from Dhaval Thakur (13)

Recently uploaded

Recently uploaded (20)

Lsi 09.2

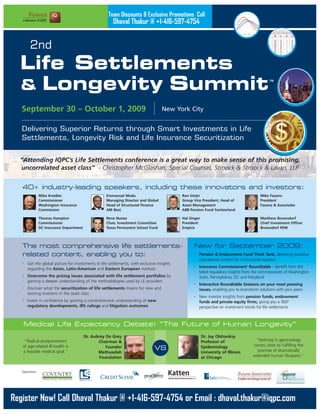

- 1. Register Now! Call Dhaval Thakur @ +1-416-597-4754 or Email : dhaval.thakur@iqpc.com • Get the global picture for investments in life settlements, with exclusive insights regarding the Asian, Latin-American and Eastern European markets • Overcome the pricing issues associated with life settlement portfolios by gaining a deeper understanding of the methodologies used by LE providers • Discover what the securitization of life settlements means for new and existing investors in the asset class • Invest in confidence by gaining a comprehensive understanding of new regulatory developments, IRS rulings and litigation outcomes Dr. Aubrey De Grey Chairman & Founder Methuselah Foundation "Radical postponement of age-related ill-health is a feasible medical goal." Sponsors: Dr. Jay Olshanksy Professor of Epidemiology University of Illinois at Chicago “Nothing in gerontology comes close to fulfilling the promise of dramatically extended human lifespans.” Mike Kreidler Commissioner Washington Insurance Commission Thomas Hampton Commissioner DC Insurance Department Emmanuel Modu Managing Director and Global Head of Structured Finance AM Best Rene Nunez Chair, Investment Committee Texas Permanent School Fund Ron Steijn Group Vice President, Head of Asset Management ABB Pension Fund Switzerland Hal Singer President Empiris The most comprehensive life settlements- related content, enabling you to: • Pension & Endowment Fund Think Tank, delivering exclusive educational content for institutional investors • Insurance Commissioners’ Roundtable – benefit from the latest regulatory insights from the commissioners of Washington State, Pennsylvania, DC and Maryland • Interactive Roundtable Sessions on your most pressing issues, enabling you to brainstorm solutions with your peers • New investor insights from pension funds, endowment funds and private equity firms, giving you a 360º perspective on investment trends for life settlements New for September 2009: 40+ industry-leading speakers, including these innovators and investors: Mike Fasano President Fasano & Associates Matthew Browndorf Chief Investment Officer Browndorf PEM VS 2nd Life Settlements & Longevity SummitTM Team Discounts & Exclusive Promotions Call Dhaval Thakur @ +1-416-597-4754 September 30 – October 1, 2009 New York City Delivering Superior Returns through Smart Investments in Life Settlements, Longevity Risk and Life Insurance Securitization Medical Life Expectancy Debate! “The Future of Human Longevity” “Attending IQPC’s Life Settlements conference is a great way to make sense of this promising, uncorrelated asset class” - Christopher McGlashan, Special Counsel, Stroock & Stroock & Lavan, LLP

- 2. Rene Nunez, Chair, Investment Committee, Texas Permanent School Fund Ron Steijn, Group Vice President, Head of Asset Management, ABB Pension Fund Switzerland Matthew Browndorf, Chief Investment Officer, Browndorf PEM Joel Ario, Commissioner, Pennsylvania Insurance Department Thomas Hampton, Commissioner, DC Insurance Department Ralph Tyler, Commissioner, Maryland Insurance Department Mike Kreidler, Commissioner, Washington Insurance Commission Steven Bloom, Senior Portfolio Analyst, APG Investments Heinz Kubli, Managing Partner, Fundabilis Emmanuel Modu, Managing Director and Global Head of Structured Finance, AM Best Antony Mott, Managing Director, Structured Insurance Products, ICAP Jonas Mårtenson, Founder & CEO, Ress Capital Jose Garcia, CEO, Carlisle Fund Management Andrew Terrell, CEO, Bristlecone Capital Isaac Efrat, Senior Managing Director, Aladdin Capital James Wang, Managing Director, Greater Asia Asset Management HK Victor DeLaet, CEO, Focused Money Solutions Franz-Philippe Pryzbyl, CEO, Berlin Atlantic Capital Ed Lay, Chairman & CEO, Emeritus Capital Kt Huang, Managing Director, Emeritus Capital Brian Smith, CEO, Life Equity LLC Michael Crane, Managing Director, Coventry Dr Jay Olshanksy, Professor of Epidemiology, University of Illinois at Chicago Dr Aubrey De Grey, Chairman & Founder, Methuselah Foundation Dr Hal Singer, President, Empiris Brian Tijan, Director, Life Finance Group, Credit Suisse Caleb Pitters, Director, Credit Suisse Robin Willi, Principal, BlueCrest Capital Management Mike Fasano, President, Fasano & Associates Register Now! Call Dhaval Thakur @ +1-416-597-4754 or Email : dhaval.thakur@iqpc.com2 An outstanding line-up of investors, fund managers and industry experts: Who Will Attend: Dear Colleague, Clearly, 2009 is a year of tremendous opportunity for investors in life settlements and longevity.More seniors are turning to the life settlement option than ever before, increasing the amount ofproduct on the market and creating a strong negotiating position for investors. At the same time,global stock volatility is intensifying the need to diversify with an uncorrelated asset. Lifesettlements, it seems, have never been such a great investment. It isn’t all roses, however. Following the life expectancy revision in 2008, many investors lost moneyon their portfolios and there remains widespread uncertainty regarding LEs currently in place. Canthe new LEs be trusted? Will they too be revised upwards in the next few years? What caninvestors do to guard against that extension risk? Furthermore, the environment for investing in lifesettlements grows increasingly more complicated with new tax rulings, regulatory changes and alack of nationwide consensus on the definition of “insurable interest”. The opportunities are real,but the complexity is real too. Taking place in New York City from September 30th – October 1st, IQPC’s 2nd Life Settlements &Longevity Summit has been specifically designed to help you – the investor – make sense of theopportunities and pitfalls of this exciting investment class. Whether you’re an experienced investor– keen to maximize your existing investment – or new to the market and still evaluating thesuitability of the asset class, this conference delivers invaluable insights from investors, fundmanagers and industry experts, ensuring you make the best possible decisions for superior returns. • Confused about the regulatory environment for life settlements?Then don’t miss our Insurance Commissioners’ Roundtable, bringing together Mike Kreidler ofWashington State, Thomas Hampton of Washington DC, Joel Ario of Pennsylvania andRalph Tyler of Maryland, in an extended panel discussion on the development of regulatoryattitudes towards investments in the secondary market. See page 3 for further details. • Want to know how institutional investors are evaluating the asset class?Don’t miss out on your chance to meet with Steven Bloom of APG, Ron Steijn of ABB PensionFund and Rene Nunez of Texas Permanent School Fund – among many others – in a closed-door Pension & Endowment Fund Think Tank that’s dedicated to the concerns of institutionalinvestors. See page 3 for further details. • Interested in a fresh perspective on the life expectancy discussion?IQPC is excited and honored to announce a special medical guest debate, featuring world-renowned gerontologist Dr. Aubrey de Grey in an explosive showdown with Dr. S. JayOlshansky, Professor of Epidemiology at the University of Illinois at Chicago, on the future ofhuman longevity and the prospects for radical lifespan enhancement. See page 4 for furtherdetails. Just three highlights from an agenda that is literally jam-packed with exciting new speakers, paneldiscussions, and critical insights into the dynamics of the asset class. I look forward to meeting you in NYC this September! Kind regards, Toby Donovan Program Director Finance IQ, a division of IQPC P.S. Don’t miss key academic insights from Dr. Hal Singer, one of the leading economists in the space – see page 3. 2nd Life Settlements & Longevity SummitTM ■ 12% Pension Funds & Institutional Investors ■ 18% Hedge Funds ■ 15% Asset Management Firms & Other Buyside ■ 15% Banks ■ 15% Life Settlement Companies ■ 10% Law Firms ■ 10% LE Provers & Underwriters ■ 5% Other “For investors interested in life settlements, there are exciting opportunities but a number of pitfalls too that can catch the unwary. Attending IQPC’s Life Settlements conference is a great way to make sense of this promising, uncorrelated, yet challenging asset class.” - Christopher McGlashan, Special Counsel, Stroock & Stroock & Lavan, LLP

- 3. legislative scrutiny. What are the implications for investors, fund managers and life settlement providers? Do market participants need to change their business practices? How will regulation shape the marketplace going forward? IQPC is honored to convene a panel discussion of insurance commissioners from Pennsylvania, DC, Washington State, and Maryland, to debate the latest changes to life settlements regulation and answer your burning questions. Specific focus points are set to include: • Regulatory attitudes towards STOLI, and the emerging consensus on “insurable interest” • An overview of changes to state and federal life settlement regulations, and their implications on existing and prospective investors • Understanding how the new administration will regard the intersection between insurance and the capital markets in general, and life settlements in particular Joel Ario Commissioner Pennsylvania Insurance Department Thomas Hampton Commissioner DC Insurance Department Ralph Tyler Commissioner Maryland Insurance Department Mike Kreidler Commissioner Washington Insurance Department 1:00 Networking Lunch 2:00 Fund Managers’ Perspectives on the Future of the Life Settlements Space: Creating an Effective Vehicle to Navigate Uncertain Investment Waters • Identifying the fund structures most likely to succeed in the current life settlements environment • Issues relating to the fund manager’s choice of medical underwriter • Fund managers’ perspectives on the attitudes of institutional investors to the asset class • Innovative capital formation approaches and fund-raising strategies • Fund construction and tax liability • Successful trading strategies for life settlement portfolios Jonas Mårtenson Founder & CEO Ress Capital Jose Garcia CEO Carlisle Fund Management Andrew Terrell CEO Bristlecone Capital Luke Rahbari CIO Peachtree Asset Management Michael Krasnerman CEO AllFinancial Group 2:45 Expanding the Investor Base in Longevity-Linked Products • What is the involvement of hedge funds and "real money" players in the longevity market? • What is the attraction of longevity to a traditionally non-actuarial investor? • In what format do nontraditional life investors typically enter the life space? Brian Tijan, Director Life Finance Group Credit Suisse Caleb Pitters Director Credit Suisse 7:45 Registration & Coffee 8:45 Welcome & Chairman’s Opening Remarks • New investment structures and the implications of recent tax law changes • Business as usual? The impact of new regulatory changes on the future health and vitality of the life settlements market 9:00 The Future of Investments in Life Settlements: Towards a Deeper Understanding of the Dynamics of the Asset Class • Examining the relationship between global equities and investment levels in the life settlements space • Exploring the possibility of a “correlation of mood”: How investment decisions are made and why the uncertainty around equities is affecting the secondary market in life insurance • The effect of the downturn on pension funds and the solvency of seniors: Understanding the implications of an “inverse liquidity correlation” • Alternative investments and the flight from equities: Examining the role that life settlements can play in future asset allocation strategies Matthew Browndorf Chief Investment Officer Browndorf PEM Michael Crane Managing Director Coventry Heinz Kubli Managing Partner Fundabilis Brian Smith CEO Life Equity LLC 9:45 Restoring Investor Confidence in Life Expectancies: Accuracy, Transparency, and the Future of Medical Underwriting • Gaining a deeper understanding of the methodologies used to create life expectancies • Examining the 2008 VBT tables and other data upon which LEs are based • Addressing common underwriting concerns, including bias, morbidity and impairment issues • Evaluating the allowance made by LE providers for continuing extensions in human longevity • Enhancing the transparency of the underwriting process Mike Fasano President Fasano & Associates 10:30 Networking Break in the Solutions Zone 11:15 An Economist’s Response to the ACLI: Using “Real Options Analysis” to Quantify the Economic Impact of the ACLI’s Proposed Changes to Life Settlements Regulation • Understanding the ACLI’s proposal • The real options analysis framework • Valuing the individual option to resell one’s insurance • Valuing the option to resell before the holding period expires as a series of European puts • Valuing the option to resell after the holding period expires as an American put • The decline in the option value of a representative policy caused by a mandatory five-year holding period • The decline in the option value summed across all eligible policies caused by a mandatory five-year holding period Hal Singer President Empiris 12:00 The Insurance Commissioners’ Roundtable: Surveying the Regulatory Landscape for Life Settlements The regulatory environment for life settlements is confusing, complex, and rapidly evolving thanks to the change in administration and new 3 Main Conference Day 1 Wednesday, September 30, 2009

- 4. 4 Register Now! Call Dhaval Thakur @ +1-416-597-4754 or Email : dhaval.thakur@iqpc.com 3:30 The Global Investment Picture for Life Settlements & Life ILS: Emerging Trends from Asia, Latin America and Eastern Europe • A survey of key investor issues and influences in Europe, Asia and Latin America • Special Focus: Asia - A new and growing frontier for alternative investments • Examining new strategies for producing risk-managed yields for institutional investors • The role of insurance linked securities in new applications to realize specific investor goals Ed Lay Chairman & CEO Emeritus Capital Kt Huang Managing Director Emeritus Capital Franz-Philippe Pryzbyl CEO Berlin Atlantic Capital Evaluating the Investment Opportunities in Longevity-Based Assets The Pension & Endowment Fund Think Tank is an hour long discussion session limited to 15 participants from pension and endowment funds. There are two levels of participation: you can be among a select group of leaders who will bring to the forefront one topic of interest or challenge you are facing right now. Or you can be a featured participant and take advantage of an exclusive networking and learning opportunity that is focused on your specific needs. Attendance is strictly limited to pension and endowment fund participants, and all discussions are off-line and off the record. Participants Include: Rene Nunez Chair, Investment Committee Texas Permanent School Fund Steven Bloom Senior Portfolio Analyst APG Investments Ron Steijn Group Vice President, Head of Asset Management ABB Pension Fund Switzerland Want to nominate yourself or a colleague? E-mail: dhaval.thakur@iqpc.com 4:15 Networking Break in the Solutions Zone 4:45 Interactive Roundtable Discussions – New! After a jam-packed day of big picture keynotes, panel discussions, case studies, and presentations, the 2nd Life Settlements & Longevity Summit gives you the chance to meet and brainstorm with small groups of your peers during our interactive roundtable discussions. This is a great opportunity to make valuable contacts from your area of interest, and to deep-dive into the tricky details that you may have missed in the course of the day’s sessions. Discussion topics at the conference include: A. Reducing the Costs of Carry: Driving Investment Returns by Enhancing Efficiency within your Administrative, Tracking & Portfolio Servicing Activities B. Understanding the Factors Involved in Portfolio Valuation: Should Investors have Confidence in the Prices of Life Settlement Pools? C. Liquidity Solutions for Distressed Life Settlement Portfolios: Evaluating Options to Bridge Liquidity Gaps and Unlock Future Value D. Pure Longevity vs. Life Settlement Pools: Comparing Synthetic Structures with Traditional Cash Investments in the Asset Class E. Bespoke Medical Underwriting vs. Off-The-Shelf: Enhancing the Transparency of your Portfolio Valuations through a More Granular Analysis of Policies F. Combating STOLI Without Violating Consumer Rights: Is there a Future in Premium Finance? 5:45 Cocktail Reception & End of Main Conference Day One Sponsored by Pension & Endowment Think Tank – New!General Session The following sessions will run concurrently Main Conference Day 1 ...continued “I was impressed by the quality of the attendees – we made important new contacts.” - Ward Bondurant, Partner, Morris Manning & Martin, LLP

- 5. 7:45 Registration & Coffee 8:30 Chairman’s Opening Remarks 8:45 What Pension & Endowment Funds are Looking For in Life Settlements: Transparency, Institutionalization, and the Future of the Asset Class • Evaluating the benefits of life settlements for pension funds seeking a non- stock market correlated asset class with low volatility levels • Identifying the common obstacles to investments in life settlements by pension funds and other institutional investors • Assessing the suitability of longevity-based investments for an LDI-style strategy • Comparing life settlement investments with synthetic longevity products • Examining the progress made towards “institutionalizing” the asset class • Mapping out the timelines for full asset class maturity: When will life settlements come of age and what value will they deliver within a pension fund allocation plan? Antony Mott Managing Director, Structured Insurance Products ICAP Rene Nunez Chair, Investment Committee Texas Permanent School Fund Additional Pension Funds & Endowment Funds to be announced - Call Dhaval Thakur @ +1-416-597-4754 or Email : dhaval.thakur@iqpc.com 9:30 Life Settlements & Taxation: Understanding What the New Rulings Mean for your Investments Roger Lorence Tax Group, Partner Sadis & Goldberg LLP Steven Huttler Financial Services Group, Of Counsel Sadis & Goldberg LLP 10:15 Networking Break in Solutions Zone 10:45 Examining the Role of Rating Agencies Within a Life Settlement Securitization • Examining the methodology used in rating a life settlements securitization: -Performing due diligence on policy origination -Creating boundaries for mortality degradations -Stress-testing life settlements based on policy size -Applying lags to the collection of death benefits, to better simulate actual collection patterns -Applying credit stress tests and default stress tests • What does the rating signify, and can it be trusted? Emmanuel Modu Managing Director and Global Head of Structured Finance AM Best 11:10 Securitization of a Life Settlements Pool: Uncovering New Opportunities for New Kinds of Investors • Understanding what securitization means for the long term future of the life settlements space • A closer look at the AIG embedded value securitization and its implications for the life settlements market • Examining the investment characteristics of securitized life settlements: What new types of investors stand to benefit from these securities? • Does securitization bring any dangers? Avoiding mistakes made in the mortgage-backed securities space Emmanuel Modu Managing Director and Global Head of Structured Finance AM Best Wai-Keung Tang Managing Partner Kappa-Life Isaac Efrat Senior Managing Director Aladdin Capital Michael Crane Managing Director Coventry Rachel B. Coan Partner Katten Muchin Rosenman LLP 5 Register Now! Call Dhaval Thakur @ +1-416-597-4754 or Email : dhaval.thakur@iqpc.com Main Conference Day 2 Thursday, October 1, 2009 11:50 Medical Life Expectancy Debate - The Future of Human Longevity Is Radical Human Lifespan Extension Within Our Grasp? Dr. Aubrey De Grey Chairman & Founder Methuselah Foundation Dr. Jay Olshanksy Professor of Epidemiology University of Illinois at Chicago VS YES “Aging is the lifelong accumulation of bodily damage. Its immense complexity focuses gerontologists on modest medical goals: essentially, optimizing our natural anti-aging defenses. Skeptics like Jay neglect the burgeoning field of regenerative medicine, which promises repair of bodily damage, and which could therefore postpone aging indefinitely. In fact, experts in all relevant strands of regenerative medicine now aim to treat aging - despite what Jay says! I thus estimate a 50% chance of radical life extension arriving in 25-30 years. Moreover, corresponding results in mice could occur within ten years, which will alter public expectations and force dramatic changes in policy.” NO Radical life extension is not going to happen (if it ever happens) in time to influence any of the investment decisions made by those involved with life settlements or insurance linked securities. Nothing in gerontology even comes close to fulfilling the promise of dramatically extended human lifespans – despite what Aubrey says! However, anyone interested in investing in life settlements should develop a sound understanding of the biological and demographic dynamics that drive mortality trends at older ages. Attending this debate will deepen your understanding of the factors that affect longevity, and may make you a smarter investor. 1:00 Networking Lunch & End of Main Conference

- 6. Register Now! Call Dhaval Thakur @ +1-416-597-4754 or Email : dhaval.thakur@iqpc.com6 Post Conference Workshops Thursday, October 1, 2009 2:00 pm - 4:00 pm (Registration at 1:45 pm) In spite of the significant opportunities in the life settlements space, investments in the asset class remain complicated and there are significant pitfalls for investors who don’t conduct the right due diligence, actuarial, and economic analyses before purchasing. If you’re evaluating the marketplace, but have yet to allocate capital, this extended workshop is for you. You’ll walk away with practical strategies for safeguarding your life settlements portfolio and significantly enhancing the security of your investment. What You Will Learn: • Understand the importance of achieving financial and legal protection for your investment • Utilize water-tight due diligence processes to ensure pristine policy origination and eliminate the possibility of future contestability issues • Stochastically simulate portfolio performance to determine best and worst case scenarios • Understand how to make use of both primary and secondary LE analysis How You Will Benefit: • Achieve confidence in portfolio pricing by making a more thorough analysis • Negotiate more effectively with third parties, and achieve more favorable pricing arrangements • Reduce contestability issues by sourcing clean, uncompromised policies Workshop Leader to be announced – Call Dhaval Thakur @ +1-416-597-4754 or Email : dhaval.thakur@iqpc.com “Immunizing” the Secondary Market Buyer: The 5 Things You MUST Do Before Buying a Life Settlements Portfolio A 4:00 pm – 6:00 pm (Registration at 3:45 pm) The normal strategy for investing in the secondary market is to purchase a ready-made portfolio of life settlements. While purchasing an existing pool of insurance policies may appear to be a quick way for fund managers to enter the market, there is also an alternative view: namely that the time and energy needed to perform the proper due diligence on an existing portfolio of policies is better allocated to building a new portfolio from scratch. What You Will Learn: • Weigh up due diligence activity on an existing life settlements portfolio with the time needed to create a customized portfolio: Where is your time better spent? • Define the parameters of your portfolio: Align risk, price and volatility factors with your overall investment strategy • Select between LE market segments: 2-4 year LEs vs. 12 years+ • Examining the mechanics of life settlement aggregation: Painless strategies for producing a transparent, optimized portfolio How You Will Benefit: • Invest in life settlements without due diligence headaches • Determine the characteristics of your portfolio in advance • Design a life settlements portfolio that better suits your overall investment strategy Workshop Leader to be announced – Call Dhaval Thakur @ +1-416-597-4754 or Email : dhaval.thakur@iqpc.com Custom-Building a Life Settlements Portfolio: Leveraging the Latest Policy Aggregation Techniques to Construct a Bespoke Portfolio with Pre-Determined Size, Risk, and Performance Attributes B "Investors are attracted to life settlements because insurance is seen as a noncorrelated alternative asset. Life settlements provide noncorrelated diversification because insurance policies are independent of the factors contributing to economic downturns, such as interest rate fluctuations and increasing fuel cost. As a result, life settlements are one way to reduce a portfolio's exposure to sudden downturns in the stock and bond markets," – Conning Research & Consulting “Experts predict explosive growth in life settlements over the next decade as a result of increasing amounts of institutional capital being pumped into the system as well as a growing demographic of elderly, well-off individuals to ensure a generous supply of life insurance policies.” – Nuwire Investor Magazine

- 7. Register Now! Call Dhaval Thakur @ +1-416-597-4754 or Email : dhaval.thakur@iqpc.com7 About Our Sponsors Sponsorship And Exhibition Opportunities Sponsorships and exhibits are excellent opportunities for your company to showcase its products and services to high-level, targeted decision-makers attending the 2nd Life Settlements & Longevity Summit. IQPC and Finance IQ help companies like yours achieve important sales, marketing and branding objectives by setting aside a limited number of event sponsorships and exhibit spaces – all of which are tailored to assist your organization in creating a platform to maximize its exposure at the event. For more information on sponsoring or exhibiting at the Life Settlements & Longevity Summit, please contact Dhaval Thakur at (416) 597-4754 or dhaval.thakur@iqpc.com. About the Organizer Finance IQ, the financial division of IQPC, produces the world’s most cutting-edge and strategic financial conferences across the US, Europe, Asia and the Middle East every year, educating almost 5,000 high-level executives annually. Our comprehensive events provide an unbiased, specialized forum where you can discuss the issues most important to you and network with industry leaders. For over 25 years, Coventry has been redefining insurance. Founded in 1982, Coventry began as an insurance marketing, product development and policy administration firm. Known as a leading innovator in the industry, Coventry assisted insurance carriers in the development of product, software and distribution. It established itself as one of the top corporate life insurance companies in America during the 1990s, servicing over 70,000 policies for its corporate clients. In 1998, Coventry created the secondary market for life insurance in the United States and coined the term “life settlement”. As the market leader, Coventry has structured and financed transactions representing more than $25 billion of death benefit and has been a key driver behind the market’s rapid growth. Today, Coventry is the largest purchaser and servicer in the longevity and mortality market, employing more than 200 people. Based in Pennsylvania, Coventry was the first secondary market firm to earn Standard and Poor’s highest servicer ranking (2004 and reaffirmed in 2006). In 2005, Coventry was first in revenue in the insurance category of the annual Inc. 500 listing of the fastest growing private companies in America. Website: www.coventry.com At LIFE EQUITY, our pricing philosophy is governed by the standard that two policies with the same criteria will receive the same offer. We believe this approach results in consistent and higher payments to owners of life insurance policies who wish to integrate a life settlement into their financial planning. Our funding comes from top-rated financial institutions and not from private investors. LIFE EQUITY makes direct contact with policy owners or their intermediaries regarding offers made. This practice assures a more efficient and expeditious process. Website: www.lifeequity.net As one of the world’s leading banks, Credit Suisse provides its clients with investment banking, private banking and asset management services worldwide. Credit Suisse offers advisory services, comprehensive solutions and innovative products to companies, institutional clients and high- net-worth private clients globally, as well as retail clients in Switzerland. Credit Suisse is active in over 50 countries and employs approximately 48,000 people. Credit Suisse’s parent company, Credit Suisse Group, is a leading global financial services company headquartered in Zurich. Credit Suisse Group’s registered shares (CSGN) are listed in Switzerland and, in the form of American Depository Shares (CS), in New York. The Life Finance Group at Credit Suisse is a dedicated group of over 90 professionals with backgrounds in various industries which include insurance, banking, structuring, sales and risk management based in New York, London and Hong Kong. Website: www.credit-suisse.com Established in 2008, Peachtree Asset Management, Ltd. (“PAM”) is a UK based investment manager focused on providing global institutional investors direct access to non-correlated alternative assets acquired directly from premier originators in the U.S. PAM focuses on assets that represent high quality, illiquid deferred payment obligations including life settlements, structured legal settlements, lottery winnings and selected insurance and annuity products. Website: www.lumpsum.com Founded in 1912, Rosenman & Colin LLP was a distinguished New York firm with a nearly century-long reputation for providing the highest quality legal work and client service. After merging in 2002 with Katten Muchin Zavis to become Katten Muchin Zavis Rosenman, the firm was renamed Katten Muchin Rosenman LLP on May 2, 2005. Katten is a full-service law firm with more than 600 attorneys in locations across the United States and an affiliate in London. The firm’s business-savvy professionals provide clients in numerous industries with sophisticated, high- value legal services, with a focus on corporate, litigation, financial services, insurance capital markets, real estate, tax planning, commercial finance, intellectual property and trusts and estates. Among our clients are a wide range of public and private companies, including a third of the Fortune 100, as well as a number of government and nonprofit organizations and individuals. Website: www.kattenlaw.com Sadis & Goldberg LLP is nationally recognized for its formidable financial services practice that consists of representing hundreds of investment advisers and related investment entities (including hedge funds, private equity funds and venture capital funds). Similarly, the firm provides regulatory and compliance advice and representation in connection with SEC enforcement proceedings. Notwithstanding the emphasis on the financial services industry, the firm also provides a full range of litigation, real estate, intellectual property and corporate services to our clients. Website: www.sglawyers.com Fasano Associates is a leading underwriting firm, serving the life, annuity and life settlement markets, with particular expertise in over-65 and impaired life mortality. Fasano’s estimates of life expectancy are considered the most accurate in life settlement market, with an Actual to Expected accuracy ratio of 96% estimated in two successive independent actuarial evaluations. Contact Fasano at www.fasanoassociates.com. Website: www.fasanoassociates.com AllFinancial Group Inc. and affiliates are a major participant and principal investor in life settlements. AFG has developed an integrated business model that spans the life settlement and premium finance markets. AFG's operations include 1) a life settlement provider, 2) a life settlement servicing operation, 3) portfolio origination and trading platform, 4) a licensed premium finance lender, and 5) an asset management platform that manages several investment vehicles that invest in life settlement and premium finance portfolios, including a 50/50 joint venture ("JV") with an international financial services firm. AllFinancial Group LLC ("AFG") will co-invest with investors to ensure alignment of interests. AFG posses an exceptional track record of originating and actively managing life settlement assets. Founded in 1997, AFG has originated over $4 billion in life settlement face value for sale to the market has purchases over $1 billion in face value for its own account. Over the past four years, AFG has invested over $170 million in combined institutional and proprietary capital, achieving exceptional average annual returns (available upon request). Website: www.allfinancialgroupllc.com

- 8. Team Discounts & Exclusive Promotions Call Dhaval Thakur @ +1-416-597-4754 Register Now! Call Dhaval Thakur @ +1-416-597-4754 or Email : dhaval.thakur@iqpc.com Registration Information Please note multiple discounts cannot be combined. A $99 processing charge will be assessed to all registrations not accompanied by credit card payment at the time of registration. MAKE CHECKS PAYABLE IN U.S. DOLLARS TO: IQPC * CT residents or people employed in the state of CT must add 6% sales tax. TEAM DISCOUNTS For information on team discounts, please contact IQPC Customer Service at 1-800-882-8684. Only one discount may be applied per registrant. Special Discounts Available: A limited number of discounts are available for the non-profit sector, government organizations and academia. For more information, please contact Dhaval Thakur @ 416-597-4754 Details for making payment via EFT or wire transfer: JPMorgan Chase - Penton Learning Systems LLC dba IQPC: 957-097239 ABA/Routing #: 021000021 Reference: Please include the name of the attendee(s) and the event number: 17092.002 Payment Policy: Payment is due in full at the time of registration and includes lunches, refreshment and detailed conference materials. Your registration will not be confirmed until payment is received and may be subject to cancellation. Special Dietary Needs: If you have a dietary restriction, please contact Customer Service at 1-800-398-1966 to discuss your specific needs. ©2009 IQPC. All Rights Reserved. The format, design, content and arrangement of this brochure constitute a trademark of IQPC. Unauthorized reproduction will be actionable under the Lanham Act and common law principles. Please see the website at www.lifesettlementsummit.com for an explanation of Hedge Funds, Pension Funds, Endowment Funds & Asset Managers and All Others. Qualified Investors (Pension Funds, Endowment Funds, Hedge Funds and Asset Management Firms) June 19, 2009 July 3, 2009 July 17, 2009 July 31, 2009 August 28, 2009 Standard Price Conference Only (Save $900) (Save $800) (Save $600) (Save $400) (Save $200) $599 $699 $899 $1,099 $1,299 $1,499 All-Access Pass (Save $1,198) (Save $1,098) (Save $898) (Save $698) (Save $498) (Save $298) (Main Conference $1,399 $1,499 $1,699 $1,899 $2,099 $2,299 + 2 Workshops) Workshop(s) $549 each $549 each $549 each $549 each $549 each $549 each All Others (banks, life settlement providers, law firms, consultants, LE providers, medical underwriters, life settlement exchanges, software providers, rating agencies, and all other companies) July 31, 2009 August 28, 2009 Standard Price Conference Only (save $600) (save $300) $1,899 $2,199 $2,499 All-Access Pass (Save $998) (Save $698) (Save $398) (Main Conference + 2 Workshops) $2,599 $2,899 $3,199 Workshop(s) $549 each $549 each $549 each YES! Please register me for Name ____________________________________________________________ Job Title _________________________________________________ Organization______________________________________________________ Approving Manager________________________________________ Address _____________________________________________ City___________________________________State__________Zip__________ Phone________________________________________________E-mail_________________________________________________________________ ❑ Please keep me informed via email about this and other related events. ❑ Check enclosed for $_________ (Payable to IQPC) ❑ Charge my ❑ Amex ❑ Visa ❑Mastercard ❑ Diners Club Card #_______________________________Exp. Date___/___ ❑ I cannot attend, but please keep me informed of all future events. 4 EASY WAYS TO REGISTER: 2 1 3 4 Call: 1-800-398-1966 or 1-416-597-4754 Email: Dhaval.thakur@iqpc.com Fax: 1-416-598-7934 Mail: IQPC 60 St. Calir Ave, E. Suite 304 Toronto, ON M4T 1N5 2nd Life Settlements & Longevity SummitTM ❑ Conference Only ❑ All Access Pass ❑ Workshop A ❑ Workshop B Sponsors: TLS/DPT