This document summarizes the key financial responsibilities of a leasehold property purchase. It outlines costs associated with the purchase, including notice fees and deed of covenant fees. It also details regular payments during ownership, such as ground rent and service charges. Additionally, it notes potential additional payments in the future, like excess service charges, planned maintenance contributions, and future fees when selling or subletting. More information on leaseholder responsibilities can be found online at www.lease-advice.org.

CBDT releases draft rules prescribing method of valuation of unquoted equity shares for the purpose of Sections 56(2)(x) and 50CA; CBDT invites comments and suggestions from stakeholders by May 19. Copy of Notification and draft rules are attached. Valuation of unquoted equity shares are to be calculated as per draft rules by taking into account the FMV of jewellery, artistic work, shares & securities and stamp duty value in case of immovable property and book value for the rest of the assets . As per existing 11UA rule the book value (and not the FMV / stamp duty value) is taken into consideration for determining the value of such shares.

Home loan borrowers enjoy dual tax benefits under the Income Tax Act. One, on the Principal Amount repaid and the second, on the Interest paid. These benefits are also available for loans taken for additions and altercations of the house and Commercial property.

Tax Rebate IT Act Sections

The tax rules relating to home loan rebates are governed under the Income Tax Act, 1961 and its amendments under the following Sections:-

(a) Section 80 C

Applicable to Principal Amount Repayment.

(b) Section 24

Applicable to Interest Payment.

(c) Section 80 EE

Additional Amount of Rs 50,000 Interest Payment (effective from 01 April 2016 onwards ).

First Time House Buyers and the House is Self Occupied

(a) Under Section 80 C

The Principal amount repaid towards home loans, enjoys tax rebate under Section 80 C. But this amount is limited to the maximum of Rs.1.5 lakhs (Rs 2 lakhs for Senior Citizens) clubbed with all other investments like PPF, Insurance etc.

Therefore, this benefit gives relief to the loan seekers to subscribe lesser amount towards investments being made to reach the limit of Rs 1.5 lakhs thereby leaving more money in their hands to repay the Equated Monthly Installments (EMIs).

Stamp Duty and Registration Charges

The Amount paid as Stamp Duty & Registration Charges are also allowed as tax deduction under Section 80C. But these can be claimed only in the year in which they were paid.

(b) Under Section 24

The Interest amount paid to the banks/NBFCs enjoy tax rebate Under Section 24. The maximum limit of this exemption is up to Rs 2 lakhs (Rs 2.5 lakhs for Senior Citizens). If the property is not completed or acquired within 05 years from the end of the Financial Year in which the loan was taken, then the amount of interest qualifying for rebate will be Rs 30,000 only.

This PDF document details all the taxes housing societies in India has to pay along with their rates, dates of submissions and filing returns. It also discusses the common problems faced by apartments to calculate their taxes and how to overcome it.

CBDT releases draft rules prescribing method of valuation of unquoted equity shares for the purpose of Sections 56(2)(x) and 50CA; CBDT invites comments and suggestions from stakeholders by May 19. Copy of Notification and draft rules are attached. Valuation of unquoted equity shares are to be calculated as per draft rules by taking into account the FMV of jewellery, artistic work, shares & securities and stamp duty value in case of immovable property and book value for the rest of the assets . As per existing 11UA rule the book value (and not the FMV / stamp duty value) is taken into consideration for determining the value of such shares.

Home loan borrowers enjoy dual tax benefits under the Income Tax Act. One, on the Principal Amount repaid and the second, on the Interest paid. These benefits are also available for loans taken for additions and altercations of the house and Commercial property.

Tax Rebate IT Act Sections

The tax rules relating to home loan rebates are governed under the Income Tax Act, 1961 and its amendments under the following Sections:-

(a) Section 80 C

Applicable to Principal Amount Repayment.

(b) Section 24

Applicable to Interest Payment.

(c) Section 80 EE

Additional Amount of Rs 50,000 Interest Payment (effective from 01 April 2016 onwards ).

First Time House Buyers and the House is Self Occupied

(a) Under Section 80 C

The Principal amount repaid towards home loans, enjoys tax rebate under Section 80 C. But this amount is limited to the maximum of Rs.1.5 lakhs (Rs 2 lakhs for Senior Citizens) clubbed with all other investments like PPF, Insurance etc.

Therefore, this benefit gives relief to the loan seekers to subscribe lesser amount towards investments being made to reach the limit of Rs 1.5 lakhs thereby leaving more money in their hands to repay the Equated Monthly Installments (EMIs).

Stamp Duty and Registration Charges

The Amount paid as Stamp Duty & Registration Charges are also allowed as tax deduction under Section 80C. But these can be claimed only in the year in which they were paid.

(b) Under Section 24

The Interest amount paid to the banks/NBFCs enjoy tax rebate Under Section 24. The maximum limit of this exemption is up to Rs 2 lakhs (Rs 2.5 lakhs for Senior Citizens). If the property is not completed or acquired within 05 years from the end of the Financial Year in which the loan was taken, then the amount of interest qualifying for rebate will be Rs 30,000 only.

This PDF document details all the taxes housing societies in India has to pay along with their rates, dates of submissions and filing returns. It also discusses the common problems faced by apartments to calculate their taxes and how to overcome it.

This was presented to attorneys and CPAs for CLE/CPE credit. The class focused on learning about IRS Audit Representation and Collection Defense and what can be done for their clients. The topics included audit representation and other liability cases, audit defense techniques, and collection defense issues and strategy.

These slides describe the law relating to the payment of stamp duty and when such payment should be made in respect of various instruments. This is from a lecture in Conveyancing conducted for the final year students of the Sri Lanka Law College in 2007

This was presented to attorneys and CPAs for CLE/CPE credit. The class focused on learning about IRS Audit Representation and Collection Defense and what can be done for their clients. The topics included audit representation and other liability cases, audit defense techniques, and collection defense issues and strategy.

These slides describe the law relating to the payment of stamp duty and when such payment should be made in respect of various instruments. This is from a lecture in Conveyancing conducted for the final year students of the Sri Lanka Law College in 2007

This is a presentation highlighting the intricacies involoved in work contract. A work contract is though a single contract for material and labour but invites the levy of service tax, sales tax, tds and above that reverse charge mechanism. Though a bit complicated yet intresting

This ppt is a comprehensive presentation on various aspects for the entities working in the construction domain. Starting from Tendering to Budgeting and going on to indirect tax aspects like VAT and service Tax.

Applying the New Lease Guidance for ASC 842RKLeSolutions

In this webinar Lease Query reviews a comprehensive example of how to apply the new lease accounting standard, ASC 842. The presentation reviews key lease dates and terms under the new standard and identify contract financial components and their applicability towards the lease liability calculation and determination of the appropriate discount rate. The presentation also covers journal entries under ASC 842.

Sample Project Proforma. The property is a City of Commerce, CA industrial property currently active for sale as of 07/13.

The property meets our buying criteria guidelines.

Current property key characteristics:

90,000 sq ft

50% coverage

16' ceiling clearance

20+ dock high loading

Urban infill location

Market rent analysis compliant

Europeana Generic Services Projects Meeting, 29-30 October 2018, The Hague, E...

LPE2 with form fields

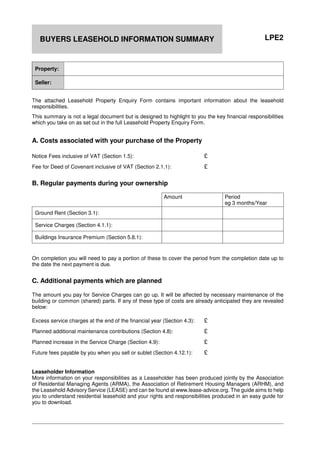

1. LPE2BUYERS LEASEHOLD INFORMATION SUMMARY

Property:

Seller:

The attached Leasehold Property Enquiry Form contains important information about the leasehold

responsibilities.

This summary is not a legal document but is designed to highlight to you the key financial responsibilities

which you take on as set out in the full Leasehold Property Enquiry Form.

A. Costs associated with your purchase of the Property

Notice Fees inclusive of VAT (Section 1.5): £

Fee for Deed of Covenant inclusive of VAT (Section 2.1.1): £

B. Regular payments during your ownership

Amount Period

eg 3 months/Year

Ground Rent (Section 3.1):

Service Charges (Section 4.1.1):

Buildings Insurance Premium (Section 5.8.1):

On completion you will need to pay a portion of these to cover the period from the completion date up to

the date the next payment is due.

C. Additional payments which are planned

The amount you pay for Service Charges can go up. It will be affected by necessary maintenance of the

building or common (shared) parts. If any of these type of costs are already anticipated they are revealed

below:

Excess service charges at the end of the financial year (Section 4.3): £

Planned additional maintenance contributions (Section 4.8): £

Planned increase in the Service Charge (Section 4.9): £

Future fees payable by you when you sell or sublet (Section 4.12.1): £

Leaseholder Information

More information on your responsibilities as a Leaseholder has been produced jointly by the Association

of Residential Managing Agents (ARMA), the Association of Retirement Housing Managers (ARHM), and

the Leasehold Advisory Service (LEASE) and can be found at www.lease-advice.org. The guide aims to help

you to understand residential leasehold and your rights and responsibilities produced in an easy guide for

you to download.