Recommended

More Related Content

What's hot

Similar to LL 478

More from Anand Mehta & Co., Chartered Accountants

More from Anand Mehta & Co., Chartered Accountants (18)

Recently uploaded

Recently uploaded (20)

LL 478

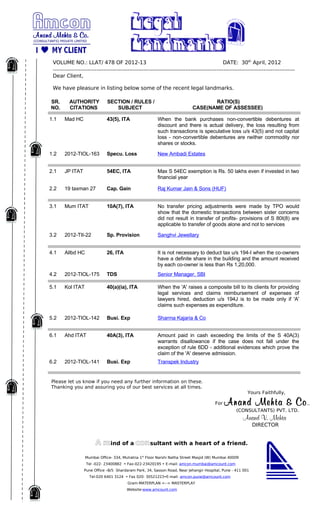

- 1. VOLUME NO.: LLAT/ 478 OF 2012-13 DATE: 30th April, 2012 Dear Client, We have pleasure in listing below some of the recent legal landmarks. SR. AUTHORITY SECTION / RULES / RATIO(S) NO. CITATIONS SUBJECT CASE(NAME OF ASSESSEE) 1.1 Mad HC 43(5), ITA When the bank purchases non-convertible debentures at discount and there is actual delivery, the loss resulting from such transactions is speculative loss u/s 43(5) and not capital loss - non-convertible debentures are neither commodity nor shares or stocks. 1.2 2012-TIOL-163 Specu. Loss New Ambadi Estates 2.1 JP ITAT 54EC, ITA Max S 54EC exemption is Rs. 50 lakhs even if invested in two financial year 2.2 19 taxman 27 Cap. Gain Raj Kumar Jain & Sons (HUF) 3.1 Mum ITAT 10A(7), ITA No transfer pricing adjustments were made by TPO would show that the domestic transactions between sister concerns did not result in transfer of profits- provisions of S 80I(8) are applicable to transfer of goods alone and not to services 3.2 2012-TII-22 Sp. Provision Sanghvi Jewellary 4.1 Allbd HC 26, ITA It is not necessary to deduct tax u/s 194-I when the co-owners have a definite share in the building and the amount received by each co-owner is less than Rs 1,20,000. 4.2 2012-TIOL-175 TDS Senior Manager, SBI 5.1 Kol ITAT 40(a)(ia), ITA When the 'A' raises a composite bill to its clients for providing legal services and claims reimbursement of expenses of lawyers hired, deduction u/s 194J is to be made only if 'A' claims such expenses as expenditure. 5.2 2012-TIOL-142 Busi. Exp Sharma Kajaria & Co 6.1 Ahd ITAT 40A(3), ITA Amount paid in cash exceeding the limits of the S 40A(3) warrants disallowance if the case does not fall under the exception of rule 6DD - additional evidences which prove the claim of the 'A' deserve admission. 6.2 2012-TIOL-141 Busi. Exp Transpek Industry Please let us know if you need any further information on these. Thanking you and assuring you of our best services at all times. Yours Faithfully, For Anand Mehta & Co ., (CONSULTANTS) PVT. LTD. Anand V. Mehta DIRECTOR A mind of a consultant with a heart of a friend. Mumbai Office- 334, Mulratna 1st Floor Narshi Natha Street Masjid (W) Mumbai 40009 Tel -022- 23400882 • Fax-022-23420195 • E-mail: amcon.mumbai@amcount.com Pune Office –B/5 Shardaram Park, 34, Sasson Road, Near Jehangir Hospital, Pune - 411 001 Tel-020 6401 3124 • Fax 020- 30521223•E-mail: amcon.pune@amcount.com Gram-MATERPLAN <--> MASTERPLAY Website:www.amcount.com