New 2024 Cannabis Edibles Investor Pitch Deck Template

Llat482

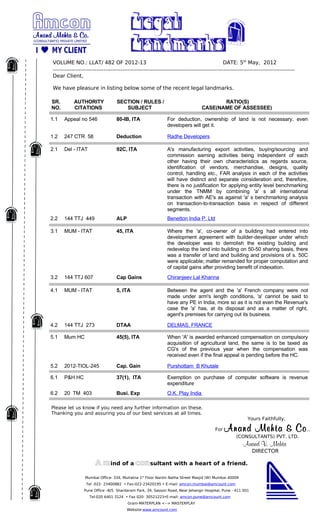

1. VOLUME NO.: LLAT/ 482 OF 2012-13 DATE: 5th May, 2012

Dear Client,

We have pleasure in listing below some of the recent legal landmarks.

SR. AUTHORITY SECTION / RULES / RATIO(S)

NO. CITATIONS SUBJECT CASE(NAME OF ASSESSEE)

1.1 Appeal no 546 80-IB, ITA For deduction, ownership of land is not necessary, even

developers will get it.

1.2 247 CTR 58 Deduction Radhe Developers

2.1 Del - ITAT 92C, ITA A's manufacturing export activities, buying/sourcing and

commission earning activities being independent of each

other having their own characteristics as regards source,

identification of vendors, merchandise, designs, quality

control, handling etc., FAR analysis in each of the activities

will have distinct and separate consideration and, therefore,

there is no justification for applying entity level benchmarking

under the TNMM by combining 'a' s all international

transaction with AE's as against 'a' s benchmarking analysis

on transaction-to-transaction basis in respect of different

segments.

2.2 144 TTJ 449 ALP Benetton India P. Ltd

3.1 MUM - ITAT 45, ITA Where the 'a', co-owner of a building had entered into

development agreement with builder-developer under which

the developer was to demolish the existing building and

redevelop the land into building on 50-50 sharing basis, there

was a transfer of land and building and provisions of s. 50C

were applicable; matter remanded for proper computation and

of capital gains after providing benefit of indexation.

3.2 144 TTJ 607 Cap Gains Chiranjeev Lal Khanna

4.1 MUM - ITAT 5, ITA Between the agent and the 'a' French company were not

made under arm's length conditions, 'a' cannot be said to

have any PE in India, more so as it is not even the Revenue's

case the 'a' has, at its disposal and as a matter of right,

agent's premises for carrying out its business.

4.2 144 TTJ 273 DTAA DELMAS, FRANCE

5.1 Mum HC 45(5), ITA When 'A' is awarded enhanced compensation on compulsory

acquisition of agricultural land, the same is to be taxed as

CG's of the previous year when the compensation was

received even if the final appeal is pending before the HC.

5.2 2012-TIOL-245 Cap. Gain Purshottam B Khutale

6.1 P&H HC 37(1), ITA Exemption on purchase of computer software is revenue

expenditure

6.2 20 TM 403 Busi. Exp O.K. Play India

Please let us know if you need any further information on these.

Thanking you and assuring you of our best services at all times.

Yours Faithfully,

For Anand Mehta & Co .,

(CONSULTANTS) PVT. LTD.

Anand V. Mehta

DIRECTOR

A mind of a consultant with a heart of a friend.

Mumbai Office- 334, Mulratna 1st Floor Narshi Natha Street Masjid (W) Mumbai 40009

Tel -022- 23400882 • Fax-022-23420195 • E-mail: amcon.mumbai@amcount.com

Pune Office –B/5 Shardaram Park, 34, Sasson Road, Near Jehangir Hospital, Pune - 411 001

Tel-020 6401 3124 • Fax 020- 30521223•E-mail: amcon.pune@amcount.com

Gram-MATERPLAN <--> MASTERPLAY

Website:www.amcount.com