This document provides a summary of recent legal landmarks in India. It lists 6 key legal cases or rulings with details including the authority, sections of law, key ratios or outcomes. The cases cover topics around taxation of the construction industry, deductions, definition of business vs profession, exemptions for charitable trusts, capital gains taxation, and tax deducted at source requirements. The document was sent by Anand Mehta & Co consultants to a client to update them on new legal precedents.

Marel Q1 2024 Investor Presentation from May 8, 2024

LL 489

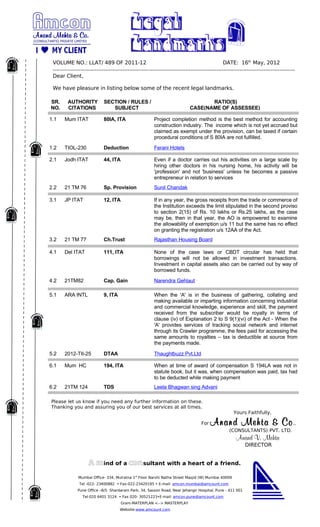

1. VOLUME NO.: LLAT/ 489 OF 2011-12 DATE: 16th May, 2012

Dear Client,

We have pleasure in listing below some of the recent legal landmarks.

SR. AUTHORITY SECTION / RULES / RATIO(S)

NO. CITATIONS SUBJECT CASE(NAME OF ASSESSEE)

1.1 Mum ITAT 80IA, ITA Project completion method is the best method for accounting

construction industry. The income which is not yet accrued but

claimed as exempt under the provision, can be taxed if certain

procedural conditions of S 80IA are not fulfilled.

1.2 TIOL-230 Deduction Ferani Hotels

2.1 Jodh ITAT 44, ITA Even if a doctor carries out his activities on a large scale by

hiring other doctors in his nursing home, his activity will be

'profession' and not 'business' unless he becomes a passive

entrepreneur in relation to services

2.2 21 TM 76 Sp. Provision Sunil Chandak

3.1 JP ITAT 12, ITA If in any year, the gross receipts from the trade or commerce of

the Institution exceeds the limit stipulated in the second proviso

to section 2(15) of Rs. 10 lakhs or Rs.25 lakhs, as the case

may be, then in that year, the AO is empowered to examine

the allowability of exemption u/s 11 but the same has no effect

on granting the registration u/s 12AA of the Act.

3.2 21 TM 77 Ch.Trust Rajasthan Housing Board

4.1 Del ITAT 111, ITA None of the case laws or CBDT circular has held that

borrowings will not be allowed in investment transactions.

Investment in capital assets also can be carried out by way of

borrowed funds.

4.2 21TM82 Cap. Gain Narendra Gehlaut

5.1 ARA INTL 9, ITA When the 'A' is in the business of gathering, collating and

making available or imparting information concerning industrial

and commercial knowledge, experience and skill, the payment

received from the subscriber would be royalty in terms of

clause (iv) of Explanation 2 to S 9(1)(vi) of the Act - When the

'A' provides services of tracking social network and internet

through its Crawler programme, the fees paid for accessing the

same amounts to royalties – tax is deductible at source from

the payments made.

5.2 2012-TII-25 DTAA Thaughtbuzz Pvt.Ltd

6.1 Mum HC 194, ITA When at time of award of compensation S 194LA was not in

statute book, but it was, when compensation was paid, tax had

to be deducted while making payment

6.2 21TM 124 TDS Leela Bhagwan sing Advani

Please let us know if you need any further information on these.

Thanking you and assuring you of our best services at all times.

Yours Faithfully,

For Anand Mehta & Co .,

(CONSULTANTS) PVT. LTD.

Anand V. Mehta

DIRECTOR

A mind of a consultant with a heart of a friend.

Mumbai Office- 334, Mulratna 1st Floor Narshi Natha Street Masjid (W) Mumbai 40009

Tel -022- 23400882 • Fax-022-23420195 • E-mail: amcon.mumbai@amcount.com

Pune Office –B/5 Shardaram Park, 34, Sasson Road, Near Jehangir Hospital, Pune - 411 001

Tel-020 6401 3124 • Fax 020- 30521223•E-mail: amcon.pune@amcount.com

Gram-MATERPLAN <--> MASTERPLAY

Website:www.amcount.com