Downloaded 12 times

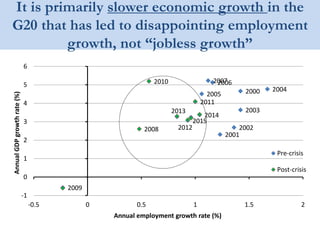

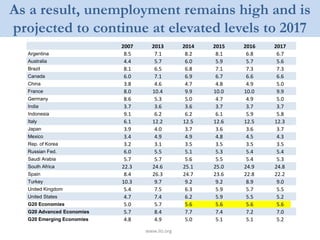

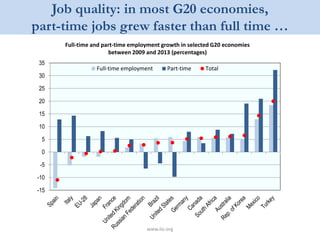

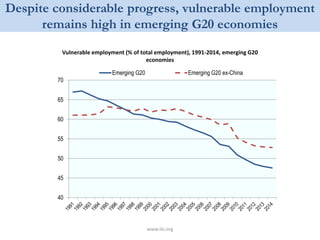

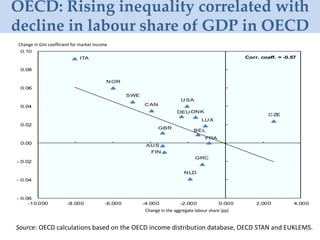

The G20 Labour Markets report from 2015 discusses the weakened link between employment and growth, noting that slow economic growth rather than 'jobless growth' is primarily responsible for disappointing employment rates. Unemployment levels remain high across G20 countries, with a projection of continued elevated levels until 2017, and a notable increase in part-time jobs compared to full-time positions. The document suggests that to strengthen the connection between growth and employment, G20 nations should adopt employment-friendly policies, enhance labor market participation, and address rising inequality, which negatively impacts growth.