Download to read offline

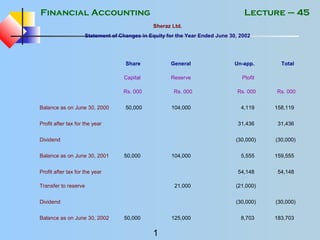

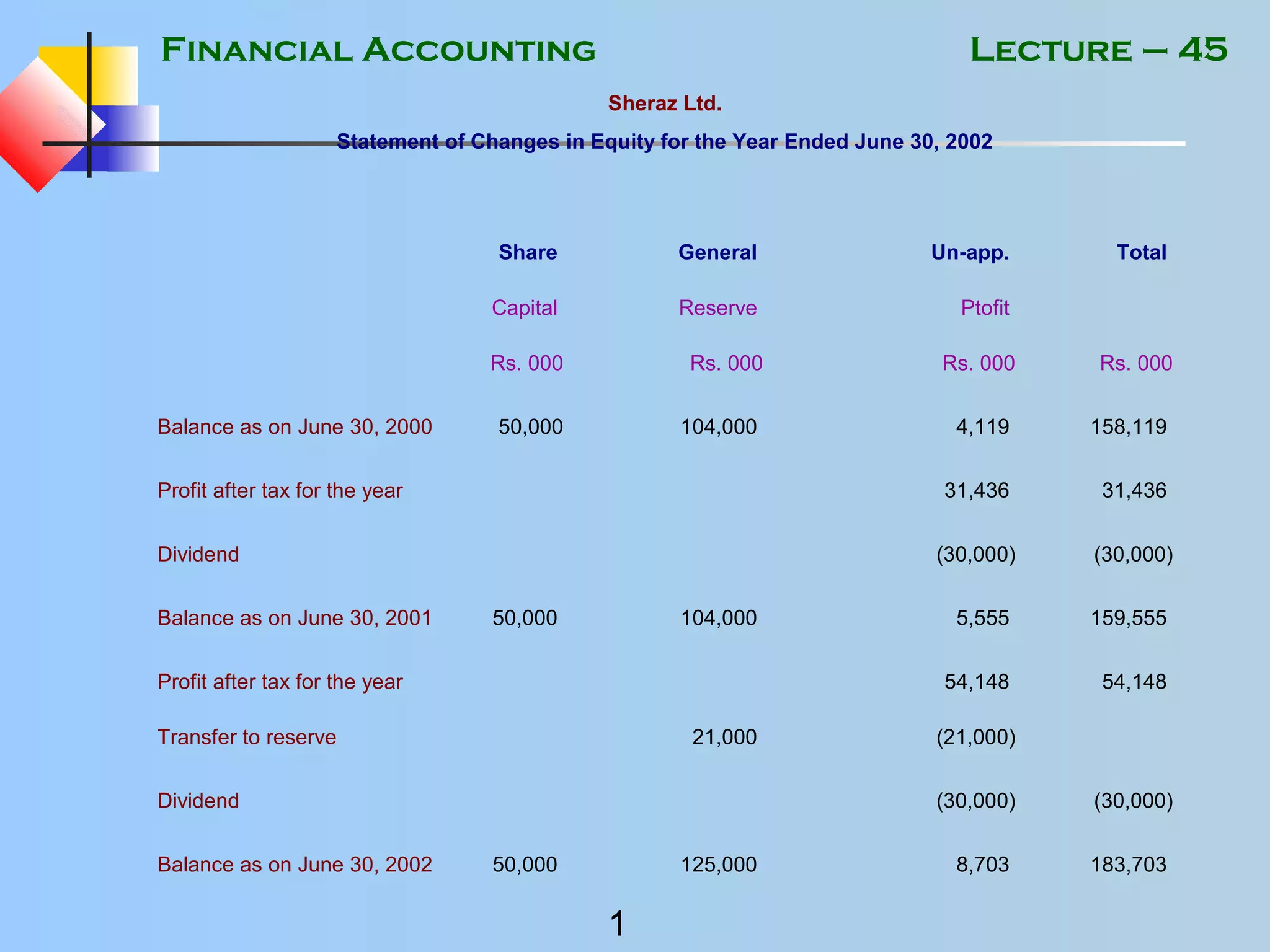

The document outlines the financial statement of Sheraz Ltd. for the year ended June 30, 2002, including details on changes in equity and significant accounting policies. It describes the company’s operations and adherence to the Companies Ordinance 1984 and international accounting standards, including historical costs and revenue recognition principles. Additionally, various financial ratios for analysis, such as profitability and turnover ratios, are presented.