Download as PDF, PPTX

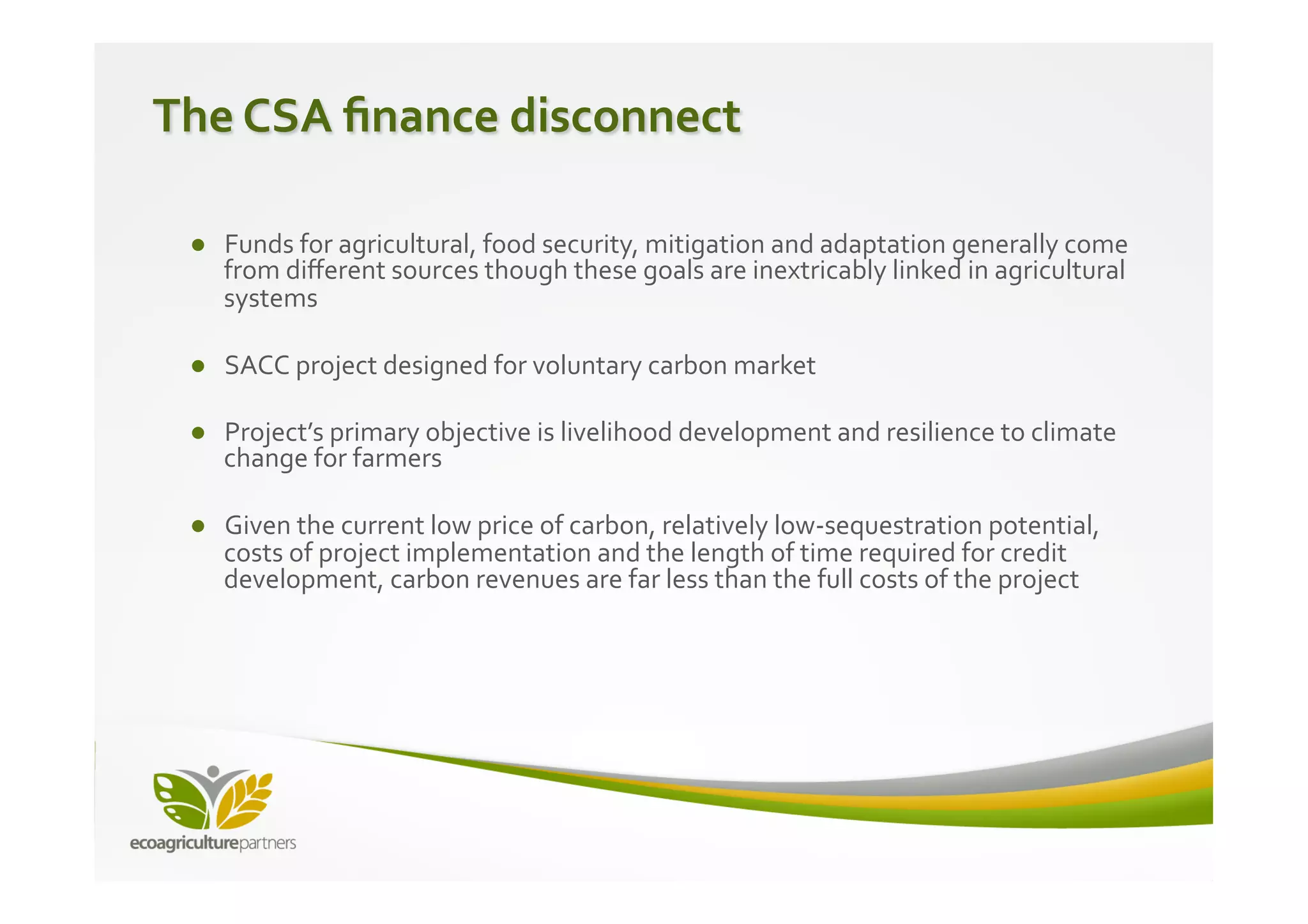

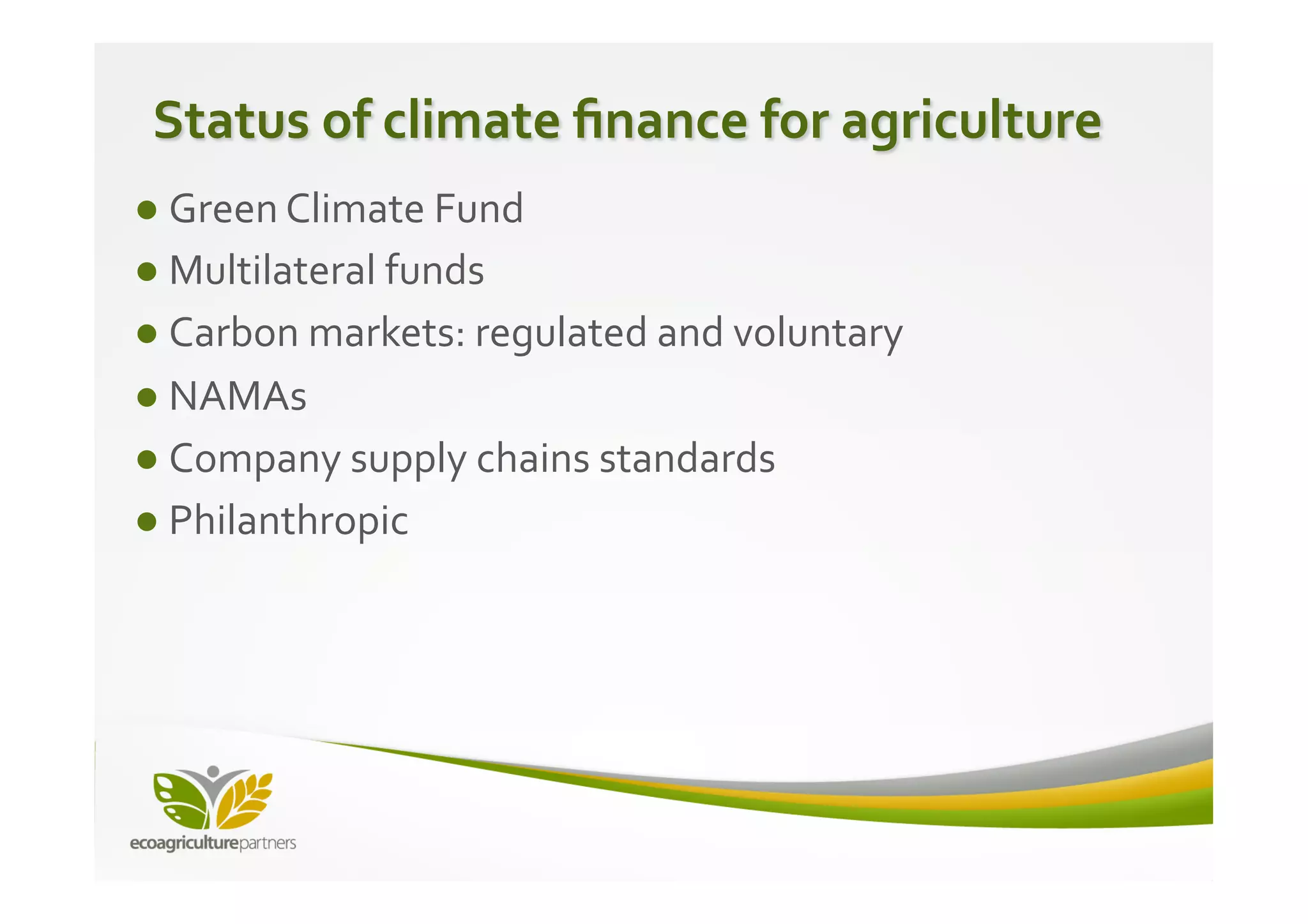

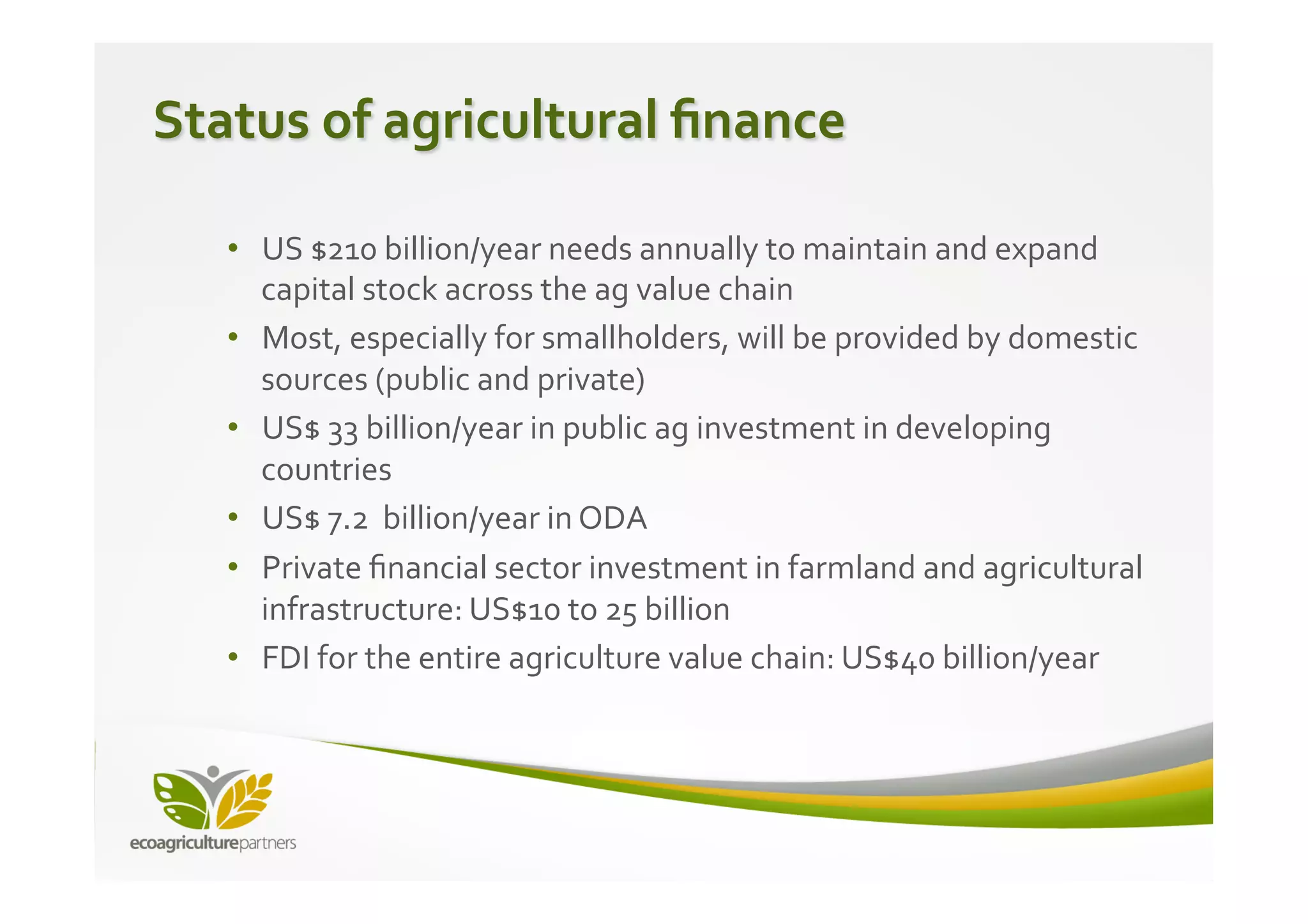

The document discusses financing possibilities for climate-smart agriculture (CSA) in Africa, highlighting a disconnect between climate and agricultural finance sources. It outlines the constraints of current financial structures, such as modest climate finance scale and limited carbon market benefits for farmers, and presents options for integration of climate and agricultural finance. The SACC project in Western Kenya serves as a case study for potential financing pathways that can enhance agricultural resilience and adaptation to climate change.