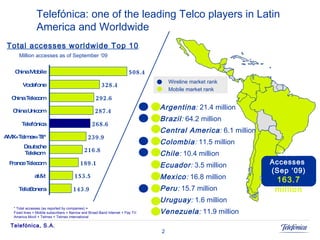

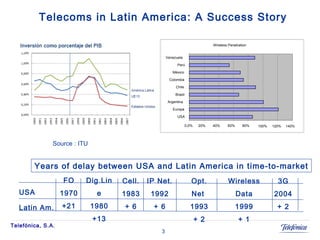

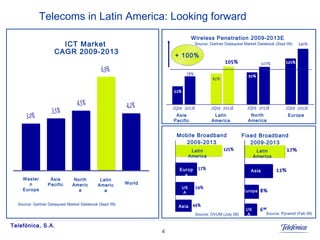

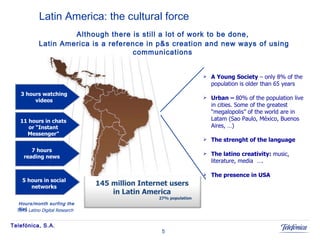

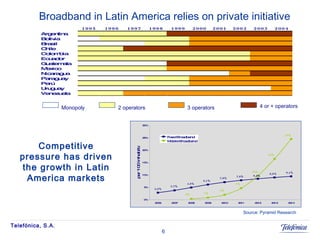

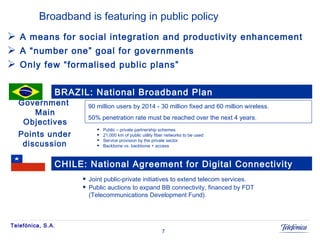

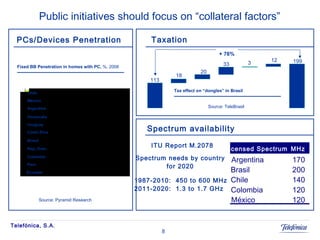

The document discusses the state of the telecommunications market in Latin America, highlighting the significant growth in total accesses and the competitive pressures that have driven this expansion. It emphasizes the importance of public-private partnerships and regulatory stability for future developments, as well as the necessity for targeted investments to extend broadband access, especially in underserved areas. Additionally, it touches on cultural factors, national broadband plans, and the role of government initiatives in improving connectivity across the region.

![Getting Started with Apache Spark: Big Data Made Simple [Free Meetup]](https://cdn.slidesharecdn.com/ss_thumbnails/apachesparkgettingstarted-260203175547-8361bcc3-thumbnail.jpg?width=640&height=640&fit=bounds)