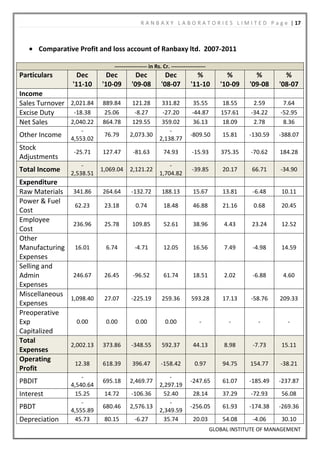

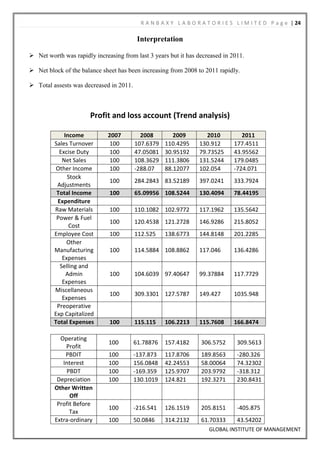

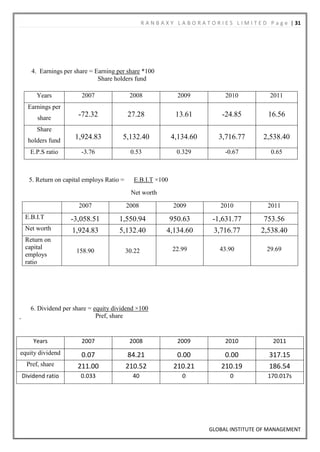

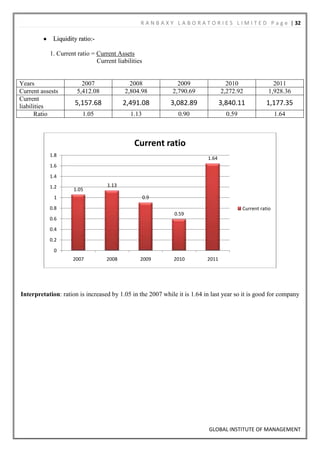

Downloaded 33 times

This document provides an overview of Ranbaxy Laboratories Limited, an Indian pharmaceutical company. It discusses the company's history, products, and financial reports from 2007-2012. Ranbaxy was founded in 1961 and went public in 1973. It manufactures generic drugs, branded generics, active pharmaceutical ingredients, and intermediates. The top selling products include Valacyclovir, Simvastatin, and various statins, antibiotics, and vitamins. Financial reports from the last 5 years are analyzed regarding the company's balance sheet, profit and loss, cash flows, ratios and other accounting details.