Downloaded 13 times

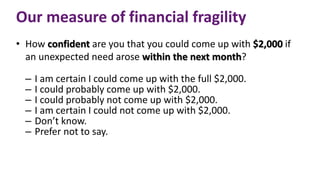

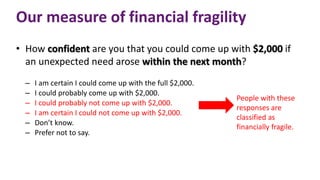

The document discusses financial fragility in American households, illustrating how many individuals continue to struggle with financial security years after the recession. It highlights a measure of financial fragility based on people's confidence in handling unexpected expenses and shows that women, low-income individuals, and those without bank accounts are particularly affected. The findings emphasize the need for improved financial education, targeted interventions, and policy changes to bolster short-term savings and overall financial capability.

![[18] Sept 2009 [E Pres] Judicial Review](https://cdn.slidesharecdn.com/ss_thumbnails/18sept2009epresjudicialreview-090918034235-phpapp01-thumbnail.jpg?width=640&height=640&fit=bounds)