Indian markets reverse gains on global risk aversion

•

1 like•111 views

- The Indian stock markets reversed gains from the previous day and closed lower due to risk aversion in global markets and fears about the impact of an earthquake in Indonesia. - Key indices like the Sensex and Nifty fell around 0.3% while mid-cap stocks declined more. Selling pressure was seen in metal, consumer durable, oil & gas and capital goods stocks. - Market volatility is expected to continue ahead of important domestic economic data releases and the RBI's monetary policy meeting next week.

Recommended

Recommended

More Related Content

What's hot

What's hot (19)

Viewers also liked

Viewers also liked (16)

Similar to Indian markets reverse gains on global risk aversion

Similar to Indian markets reverse gains on global risk aversion (20)

More from Keynote Capitals Ltd.

More from Keynote Capitals Ltd. (20)

Recently uploaded

Recently uploaded (20)

Indian markets reverse gains on global risk aversion

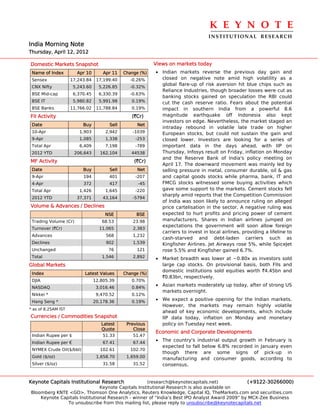

- 1. K E Y N O T E INSTITUTIONAL RESEARCH India Morning Note Thursday, April 12, 2012 Domestic Markets Snapshot Views on markets today Name of Index Apr 10 Apr 11 Change (%) • Indian markets reverse the previous day gain and Sensex 17,243.84 17,199.40 -0.26% closed on negative note amid high volatility as a global flare-up of risk aversion hit blue chips such as CNX Nifty 5,243.60 5,226.85 -0.32% Reliance Industries, though broader losses were cut as BSE Mid-cap 6,370.45 6,330.39 -0.63% banking stocks gained on speculation the RBI could BSE IT 5,980.82 5,991.98 0.19% cut the cash reserve ratio. Fears about the potential BSE Banks 11,766.02 11,788.84 0.19% impact in southern India from a powerful 8.6 FII Activity (`Cr) magnitude earthquake off Indonesia also kept investors on edge. Nevertheless, the market staged an Date Buy Sell Net intraday rebound in volatile late trade on higher 10-Apr 1,903 2,942 -1039 European stocks, but could not sustain the gain and 9-Apr 1,085 1,338 -253 closed lower. Investors are looking for a series of Total Apr 6,409 7,198 -789 important data in the days ahead, with IIP on 2012 YTD 206,643 162,104 44538 Thursday, Infosys result on Friday, inflation on Monday and the Reserve Bank of India's policy meeting on MF Activity (`Cr) April 17. The downward movement was mainly led by Date Buy Sell Net selling pressure in metal, consumer durable, oil & gas 9-Apr 194 401 -207 and capital goods stocks while pharma, bank, IT and 4-Apr 372 417 -45 FMCG stocks witnessed some buying activities which Total Apr 1,426 1,645 -220 gave some support to the markets. Cement stocks fell sharply amid reports that the Competition Commission 2012 YTD 37,371 43,164 -5794 of India was soon likely to announce ruling on alleged Volume & Advances / Declines price cartelisation in the sector. A negative ruling was NSE BSE expected to hurt profits and pricing power of cement Trading Volume (Cr) 68.53 23.98 manufacturers. Shares in Indian airlines jumped on expectations the government will soon allow foreign Turnover (`Cr) 11,065 2,383 carriers to invest in local airlines, providing a lifeline to Advances 568 1,232 cash-starved and debt-laden carriers such as Declines 902 1,539 Kingfisher Airlines. Jet Airways rose 5%, while SpiceJet Unchanged 76 121 rose 5.5% and Kingfisher gained 6.7%. Total 1,546 2,892 • Market breadth was lower at ~0.80x as investors sold Global Markets large cap stocks. On provisional basis, both FIIs and domestic institutions sold equities worth `4.45bn and Index Latest Values Change (%) `0.83bn, respectively. DJIA 12,805.39 0.70% NASDAQ 3,016.46 0.84% • Asian markets moderately up today, after of strong US markets overnight. Nikkei * 9,470.52 0.12% Hang Seng * 20,178.36 0.19% • We expect a positive opening for the Indian markets. However, the markets may remain highly volatile * as of 8.25AM IST ahead of key economic developments, which include Currencies / Commodities Snapshot IIP data today, inflation on Monday and monetary Latest Previous policy on Tuesday next week. Quote Close Economic and Corporate Developments Indian Rupee per $ 51.33 51.47 • The country's industrial output growth in February is Indian Rupee per € 67.41 67.44 expected to fall below 6.8% recorded in January even NYMEX Crude Oil($/bbl) 102.61 102.70 though there are some signs of pick-up in Gold ($/oz) 1,658.70 1,659.00 manufacturing and consumer goods, according to Silver ($/oz) 31.58 31.52 consensus. Keynote Capitals Institutional Research (research@keynotecapitals.net) (+9122-30266000) Keynote Capitals Institutional Research is also available on Bloomberg KNTE <GO>, Thomson One Analytics, Reuters Knowledge, Capital IQ, TheMarkets.com and securities.com Keynote Capitals Institutional Research - winner of “India’s Best IPO Analyst Award 2009” by MCX-Zee Business To unsubscribe from this mailing list, please reply to unsubscribe@keynotecapitals.net

- 2. K E Y N O T E INSTITUTIONAL RESEARCH TOP GAINERS Buzzing Stocks (BSE A-Group) • A SAIL-led consortium will bid for copper and gold Previous Current Change reserves in the mineral-rich country, steel minister Company Name Close(`) Price(`) (%) Beni Prasad Verma said on Wednesday. Verma met Strides Arco 596.00 631.90 6.02 Afghanistan President Hamid Karzai on Tuesday Financial Tech 706.45 747.10 5.75 during his visit there and discussed various aspects Max India 181.65 188.25 3.63 of bilateral cooperation and mutual development. Kotak Mah Bank 545.05 560.00 2.74 SAIL-led consortium and Afghanistan government Hexaware Tech 116.95 120.00 2.61 are likely to ink a final pact in May to develop Hajigak iron ore mines and set up steel and power (BSE Mid-Cap) plants there. Previous Current Change • Jet Airways has said there has been some delays in Company Name Close(`) Price(`) (%) its payments to airports due to rising fuel costs and Godfrey Phil 3333.50 3542.95 6.28 a depreciating rupee. Strides Arco 596.00 631.90 6.02 Financial Tech 706.45 747.10 5.75 • National Thermal Power Corporation Limited (NTPC) Jet Air India 340.60 358.50 5.26 has expressed confidence to cross its power Fresenius Kabi 153.40 159.70 4.11 generation target during the 12th five year plan. • Piramal Healthcare on Wednesday announced it has TOP LOSERS received European regulatory nod to sell BST-CarGel, a bio-orthopaedic product. The approval will enable (BSE A-Group) Piramal to commercialise BST-CarGel in all of the Previous Current Change countries in the European Union. It will also serve as Company Name Close(`) Price(`) (%) the basis to obtain commercial authorisation for the Gujarat Gas 341.95 316.85 -7.34 product in areas such as West Asia. Century Tex 368.05 345.35 -6.17 Reliance Cap 381.45 360.55 -5.48 • Ashok Leyland is to enter Britain’s mid-range truck market through a tie-up by its Prague-based ACC 1300.80 1236.65 -4.93 subsidiary, Avia Ashok Leyland. United Brew 538.75 513.45 -4.70 US markets (BSE Mid-Cap) U.S. stocks rose overnight, after Spanish and Italian Previous Current Change bond yields fell and aluminum maker Alcoa Inc. Company Name Close(`) Price(`) (%) reported a surprising profit. COX KINGS 155.95 143.70 -7.86 India Cements 104.85 96.75 -7.73 The Dow Jones Industrial Average rose 89.46 points, or Gujarat Gas 341.95 316.85 -7.34 0.7%, to 12,805.3. The S&P 500 Index gained 10.12 Century Tex 368.05 345.35 -6.17 points, or 0.7%, to 1,368.71. The Nasdaq Composite added 12.24 points, or 0.8%, to 3,016.46. Edelweiss Capital 31.55 30.25 -4.12 Keynote Capitals Institutional Research (research@keynotecapitals.net) (+9122-30266000)

- 3. K E Y N O T E INSTIT UT IONAL R ES EAR C H India and Global Economic Calendar Countries / Thursday Friday Monday Tuesday Regions 12/Apr 13/Apr 16/Apr 17/Apr India IIP Data Forex Reserves Data Monthly Inflation RBI's Monetary Policy Weekly Supplement of RBI US Initial Jobless claims Consumer Price Retail Sales Housing Starts Index & Consumer (MoM) Price Index Ex Food & Energy (YoY & MoM) Producer price Index Retail Sales & Retail Empire State Index Capacity Utilization Sales Ex Autos and Home builders' (MoM), index Trade balance Reuters/ Michigan Business Inventories Building Permits Consumer (MoM) Sentiment Index Global UK trade balance UK Producer Price UK's Building data Index - Input (YoY & Permits (MoM) and MoM) n.s.a (YoY) Germany WPI Data UK Producer Price Japan's Industrial Index - Output (YoY Production (MoM) & MoM) n.s.a and (YoY) European central China Industrial bank (ECB) monthly Production (YoY), report GDP (YoY), Retail Sales (YoY) KEYNOTE CAPITALS LTD. 4th Floor, Balmer Lawrie Building, 5, J. N. Heredia Marg, Ballard Estate, Mumbai 400 001. INDIA Tel. : 9122-2269 4322 / 24 / 25 • www.keynotecapitals.com Disclaimer: This report is purely for information purpose and is based on public information. News content is attributable to various media, unless specified otherwise. All market related statistical data pertains to the immediately preceding trading day, unless stated otherwise. Neither the information nor any opinion expressed in this report constitutes an offer, or an invitation to make an offer, to buy or sell the securities mentioned herein. We or any of our directors, officers or employees shall not in any way be responsible for any loss arising from the use of this report. Investors are advised to apply their own judgment before acting on the contents of this report. The report has not been edited due to time constraints.