Keynote capitals india morning note november 1-'11

1. K E Y N O T E

INSTITUTIONAL RESEARCH

India Morning Note

Tuesday, November 1, 2011

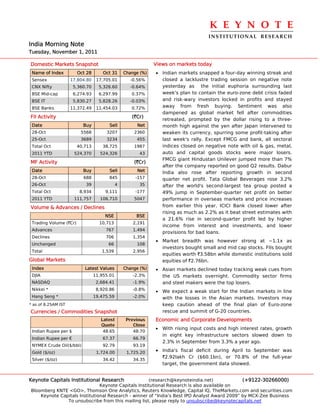

Domestic Markets Snapshot Views on markets today

Name of Index Oct 28 Oct 31 Change (%) • Indian markets snapped a four-day winning streak and

Sensex 17,804.80 17,705.01 -0.56% closed a lacklustre trading session on negative note

CNX Nifty 5,360.70 5,326.60 -0.64% yesterday as the initial euphoria surrounding last

BSE Mid-cap 6,274.93 6,297.99 0.37% week's plan to contain the euro-zone debt crisis faded

BSE IT 5,830.27 5,828.26 -0.03% and risk-wary investors locked in profits and stayed

BSE Banks 11,372.49 11,454.03 0.72% away from fresh buying. Sentiment was also

dampened as global market fell after commodities

FII Activity (`Cr)

retreated, prompted by the dollar rising to a three-

Date Buy Sell Net month high against the yen after Japan intervened to

28-Oct 5568 3207 2360 weaken its currency, spurring some profit-taking after

25-Oct 3689 3234 455 last week's rally. Except FMCG and bank, all sectoral

Total Oct 40,713 38,725 1987 indices closed on negative note with oil & gas, metal,

2011 YTD 524,370 524,326 43 auto and capital goods stocks were major losers.

FMCG giant Hindustan Unilever jumped more than 7%

MF Activity (`Cr)

after the company reported on good Q2 results. Dabur

Date Buy Sell Net India also rose after reporting growth in second

28-Oct 688 845 -157 quarter net profit. Tata Global Beverages rose 3.2%

26-Oct 39 4 35 after the world's second-largest tea group posted a

Total Oct 8,934 9,111 -177 49% jump in September-quarter net profit on better

2011 YTD 111,757 106,710 5047 performance in overseas markets and price increases

Volume & Advances / Declines from earlier this year. ICICI Bank closed lower after

rising as much as 2.2% as it beat street estimates with

NSE BSE

a 21.6% rise in second-quarter profit led by higher

Trading Volume (`Cr) 10,713 2,191

income from interest and investments, and lower

Advances 767 1,494

provisions for bad loans.

Declines 706 1,354

• Market breadth was however strong at ~1.1x as

Unchanged 66 108

investors bought small and mid cap stocks. FIIs bought

Total 1,539 2,956

equities worth `3.58bn while domestic institutions sold

Global Markets equities of `2.76bn.

Index Latest Values Change (%) • Asian markets declined today tracking weak cues from

DJIA 11,955.01 -2.3% the US markets overnight. Commodity sector firms

NASDAQ 2,684.41 -1.9% and steel makers were the top losers.

Nikkei * 8,920.86 -0.8% • We expect a weak start for the Indian markets in line

Hang Seng * 19,475.59 -2.0% with the losses in the Asian markets. Investors may

* as of 8.25AM IST keep caution ahead of the final plan of Euro-zone

Currencies / Commodities Snapshot rescue and summit of G-20 countries.

Latest Previous Economic and Corporate Developments

Quote Close

• With rising input costs and high interest rates, growth

Indian Rupee per $ 48.65 48.70

in eight key infrastructure sectors slowed down to

Indian Rupee per € 67.37 66.79

2.3% in September from 3.3% a year ago.

NYMEX Crude Oil($/bbl) 92.79 93.19

Gold ($/oz) 1,724.00 1,725.20 • India's fiscal deficit during April to September was

`2.92lakh Cr ($60.1bn), or 70.8% of the full-year

Silver ($/oz) 34.42 34.35

target, the government data showed.

Keynote Capitals Institutional Research (research@keynoteindia.net) (+9122-30266000)

Keynote Capitals Institutional Research is also available on

Bloomberg KNTE <GO>, Thomson One Analytics, Reuters Knowledge, Capital IQ, TheMarkets.com and securities.com

Keynote Capitals Institutional Research - winner of “India’s Best IPO Analyst Award 2009” by MCX-Zee Business

To unsubscribe from this mailing list, please reply to unsubscribe@keynotecapitals.net

2. K E Y N O T E

INSTITUTIONAL RESEARCH

TOP GAINERS Buzzing Stocks

(BSE A-Group) • Maruti suzuki develops customised school vans

Previous Current Change under brands Omni and EECO.

Company Name

Close (`) Price (`) (%)

• IVRCL and its subsidiary IVRCL Infrastructures and

HUL 349.45 375.25 7.38

Projects Ltd, on Monday received in-principle

Uco Bank 71.00 75.25 5.99

approval from their respective boards to pursue the

Indian Bank 205.25 217.25 5.85

proposal for amalgamation of IVCL Assets with IVRCL

Lanco Infra 15.70 16.45 4.78

Ltd.

IOB 97.80 102.40 4.70

• Reliance Industries denied that it is looking to buy

(BSE Mid-Cap) Valero Energy Corp.

Previous Current Change

Company Name • Tata Motors will challenge the Calcutta High Court

Close(`) Price(`) (%)

Essar Ports 66.95 80.30 19.94

order upholding the validity of the Singur Land and

Rehabilitation and Development Act. The company

JM Financial 16.60 19.00 14.46

on Monday filed an appeal in the division bench and

Vijaya Bank 55.85 61.15 9.49

the matter would be heard from tomorrow.

Himadri Chem 49.35 53.40 8.21

Gillette India 2091.90 2230.00 6.60 US markets

US stocks ended sharply lower Monday as a surge in

TOP LOSERS the U.S. dollar hit commodities and other assets viewed

(BSE A-Group) as relatively risky, fuelling the biggest one-day

percentage drop for the Dow Jones Industrial Average in

Previous Current Change

Company Name four weeks.

Close(`) Price(`) (%)

Gitanjali Gems 364.25 345.00 -5.28 Waning confidence over Europe’s plan to contain the

Oriental Bank 304.55 290.15 -4.73 region’s debt crisis also contributed to the session’s

Hindalco Inds 142.20 136.35 -4.11 decline. The S&P 500 Index and Nasdaq Composite

Sterlite Inds 132.90 127.45 -4.10 both up 11% from the end of September. The Dow

JPINFRATEC 62.35 59.90 -3.93 Jones Industrial Average fell 276.10 points, or 2.3%, to

close at 11,955.01. The S&P 500 Index shed 31.79

(BSE Mid-Cap)

points, or 2.5%, to 1,253.30 and the Nasdaq Composite

Previous Current Change dropped 52.74 points, or 1.9%, to 2,684.41.

Company Name

Close(`) Price(`) (%)

Gitanjali Gems 364.25 345.00 -5.28

Shree Global Trd 211.15 200.60 -5.00

VAARAD 79.40 75.45 -4.97

Shri Ganesh Spi 4.73 4.50 -4.86

A2Z Maint 182.75 174.40 -4.57

KEYNOTE CAPITALS LTD.

4th Floor, Balmer Lawrie Building, 5, J. N. Heredia Marg, Ballard Estate, Mumbai 400 001. INDIA

Tel. : 9122-2269 4322 / 24 / 25 • www.keynoteindia.net

Disclaimer: This report is purely for information purpose and is based on public information. News content is attributable to

various media, unless specified otherwise. All market related statistical data pertains to the immediately preceding trading day,

unless stated otherwise. Neither the information nor any opinion expressed in this report constitutes an offer, or an invitation to

make an offer, to buy or sell the securities mentioned herein. We or any of our directors, officers or employees shall not in any

way be responsible for any loss arising from the use of this report. Investors are advised to apply their own judgment before

acting on the contents of this report. The report has not been edited due to time constraints.