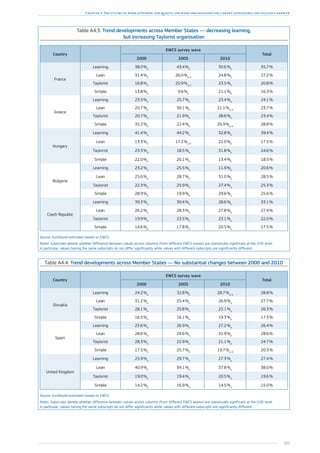

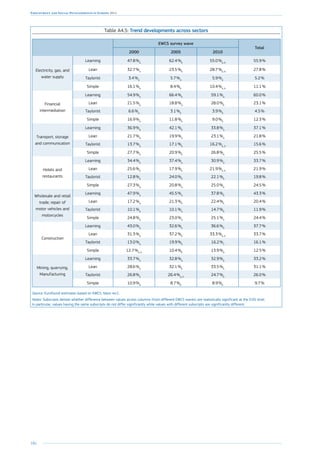

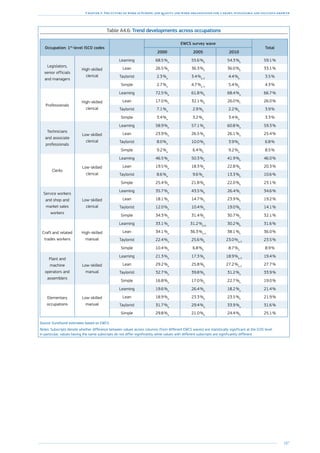

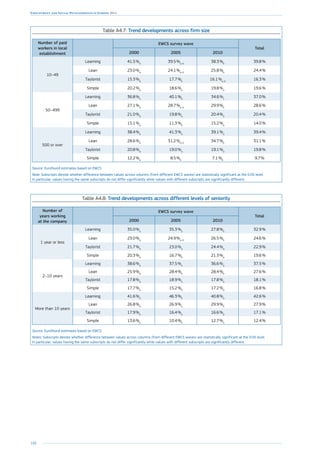

This document provides a summary and analysis of employment and social developments in Europe in 2014. It finds that while growth has resumed, obstacles to job creation remain, including weak demand, crisis legacies, and recurrent issues. Youth, the long-term unemployed, and low-skilled workers face particular challenges benefiting from growth. Job polarization is ongoing, emphasizing the need for lifelong learning. Household incomes declined in the crisis but are recovering, though poverty risks remain, requiring training, quality jobs, and effective social policies. Social and labor market imbalances can negatively impact GDP growth both domestically and across borders. The crisis had lasting effects on welfare systems, labor market institutions, and society, but countries that invested in human capital

![14

Employment and Social Developments in Europe 2014

rates (for 20-64) remain well below

pre-crisis levels (68.4 % in 2013 vs.

70.3 % in 2008) and a long way off

the Europe 2020 target of 75 %. While

6.7 million jobs were destroyed between

2008 and the first quarter of 2013, the

number of jobs increased by 1.8 million up

to the second quarter of 2014. Moreover,

a large proportion of the new jobs cre-

ated recently are temporary or part-time,

raising concerns about the robustness of

the recovery.

The impact of the crisis on employment

and the social situation increased as the

unemployment rate rose from less than

7 % in 2008 to 10.8 % in 2013, putting

9 million more people out of work. The

effects were unevenly spread across the

EU however, with unemployment rates in

2013 still only around 5 % in Austria and

Germany against over 25 % in Greece

and Spain.

While the economic recovery is expected

to strengthen only gradually, EU employ-

ment is foreseen to start growing from

this year onwards, leading to a decline

in the overall EU unemployment rate

towards 9.5 % by 2016, according to the

Commission autumn forecast.

Cross-country differences in employ-

ment are large. Between 2008 and mid-

2014 most of the jobs were destroyed

in Spain (-3.4 million), Italy (-1.2 million),

and Greece (-1.0 million), while the num-

ber of jobs increased by 1.8 million in

Germany, and by 0.9 million in the United

Kingdom during the same period.

Employment divergence was reflected in

cross-country differences in unemploy-

ment, particularly in the euro area, with

Southern/peripheral countries seeing a

massive increase while rates remained

stable and low in the Northern/core

countries (see Chart 2). The dispersion in

unemployment rates is expected to start

to decline only gradually, still remaining

well above the pre-crisis level.

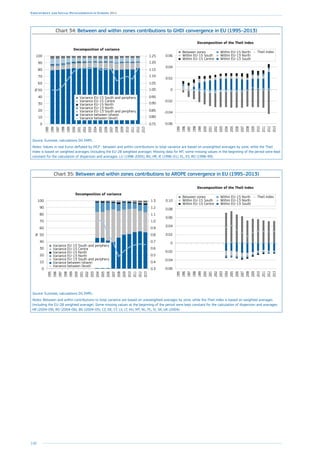

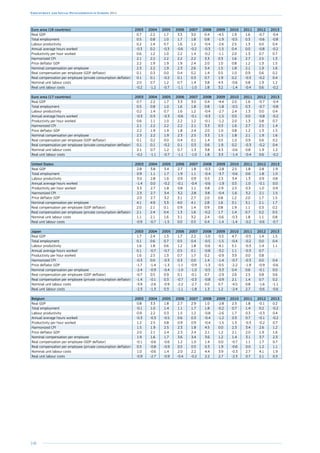

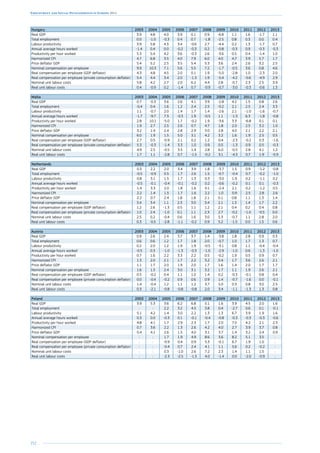

Chart 1: Growth in real GDP, real household disposable income

and employment, year-on-year change

-8

-6

-4

-2

0

2

4

Q2Q1Q4Q3Q2Q1Q4Q3Q2Q1Q4Q3Q2Q1Q4Q3Q2Q1Q4Q3Q2Q1Q4Q3Q2Q1Q4Q3Q2Q1

%changeonpreviousyear

GDP

GDHI

Employment

2007 2008 2009 2010 2011 2012 2013 2014

Source: Eurostat, National Accounts, data non-seasonally adjusted [namq_gdp_k]

Chart 2: Unemployment rates in the EU by group of Member States

0

5

10

15

20

201420132012201120102009200820072006200520042003200220012000

Non-EA South and peripheryEA North and core

EA South and peripheryNon-EA North

%oflabourforce15-74

Source: Eurostat, EU-LFS; DG EMPL calculations.

Note: EA North and core: AT BE DE FI FR LU NL, EA South and periphery: EE EL ES IE IT CY MT PT SI SK LV

Non-EA north: CZ DK PL SE UK, Non-EA South and periphery: BG HR LT HU RO.

Chart 3: Youth unemployment rates in the EU Member States

in August 2014 and the highest and lowest rates since 2008

%oflabourforce15-24

0

10

20

30

40

50

60

70

ESELITHRCYPTSKIEROFRBE

EA-18

PLBGLVSE

EU-28

LTHUFISICZUKLUMTEEDKNLATDE

August 2014

Highest rate since 2008

Lowest rate since 2008

Source: Eurostat, EU-LFS data, seasonally adjusted [une_rt_m].

Notes: EE EL HU UK Jul 2014 CY HR LV RO SI 2014Q2.

The convergence in the cyclical positions

and the ongoing labour cost adjustment

in high-unemployment countries would

contribute to further reduce the diver-

gence of labour market conditions in

the EU. Nevertheless, the present diver-

gence shows the need to look beyond

the traditional macro-economic adjust-

ment channels and consider changes in

socio-economic factors and cross-border

effects that may influence the depth and](https://image.slidesharecdn.com/fd1af655-5d67-4954-a059-19619f458af7-150123121918-conversion-gate01/85/KE-BD-14-001-EN-N-16-320.jpg)

![15

Job creation, productivity and more equality for sustained growth

persistence of an economic downturn as

well as the adjustment capacity of any

given economy (7

).

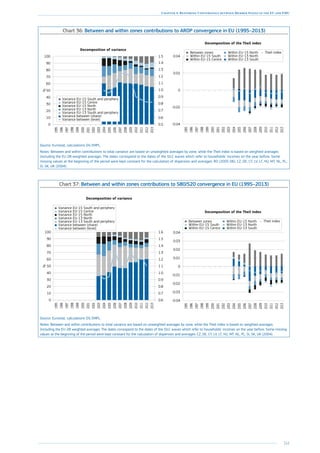

The situation of young people and the

long-term unemployed is of particular

concern. In almost two thirds of Mem-

ber States, youth unemployment rates in

July 2014 were still close to their historic

highs – EU average of 21.7 % compared

to about 15 % in the first half of 2008 –

(Chart 3) while the proportion of young

people not in education or employment

(NEET) reached 13 % in 2011 against

11 % in 2008 (Chart 4). Again, however,

it varies considerably between Mem-

ber States while remaining higher than

before the downturn.

Such severe labour market deterioration

has had inevitable social consequences

with the number of people at risk of pov-

erty and social exclusion rising by more

than 6 million since 2008, reaching some

123 million in 2013, and taking us fur-

ther from the Europe 2020 target of hav-

ing at least 20 million fewer people in or

at risk of poverty and social exclusion.

Poverty and social exclusion among

those of working age (18-64 years)

has increased significantly in two thirds

of the Member States as a combined

result of rising levels of jobless and low

work intensity households, and in-work

poverty. In Greece, Ireland, Spain, Italy

and Hungary, poverty, social exclusion

and inequalities have increased signifi-

cantly from already high levels prior to

the crisis.

(7

) See also Chapter 4 of this review.

Chart 4: NEET rate for the EU, EA and Member States in 2013

and the highest and lowest rates since 2008

0

5

10

15

20

25

ITBGELCYESHRROIEHUPTSKUKLV

EU-28

EA-18

BEPLEEFRLTMTFISICZSEATDEDKNLLU

2013

Highest rate since 2008

Lowest rate since 2008

%ofpopulation15-24

Source: Eurostat, EU-LFS data [edat_lfse_20].

Chart 5: Evolution of the risk-of-poverty or social exclusion,

2008 and 2013

0

5

10

15

20

25

30

35

40

45

50

BGELHULTIEITCYESMTLUDKLVHRPTUKEU-28EEEA-18SISENLBEDEFRROPLSKATFICZ

2008 2012/2013

%ofpopulation

Decrease Stable Increase Strongincrease

Source: Eurostat, EU SILC [ilc_peps01], income year 2007, 2012.

Notes: ES 2013 break in series (classified as strong increase based on 2008-2012 change), AT and UK

2012 break in series, HR 2010 instead of 2008 and 2012 instead of 2013, IE 2012 instead of 2013,

EU-27 instead of EU-28 in 2008.

Chart 6: Inequality of income distribution (income quintile share ratio

S80/S20), 2008 and 2013

Ratio

Decrease Stable Increase Strongincrease

0

1

2

3

4

5

6

7

8

ELESITEEHRCYLUDKHULTIESESKSIBGPT

EA-18

EU-28

FRATCZROLVPLDEUKMTBEFINL

2008 2013

Source: Eurostat, EU SILC [ilc_di11], income year 2007, 2012.

Notes: ES 2013 break in series, AT and UK 2012 break in series, HR 2010 instead of 2008, IE 2012

instead of 2013, EU-27 instead of EU-28 in 2008.

2. Obstacles to job

creation

The legacy of the crisis poses significant

obstacles to job creation now, which add

to many of the obstacles that were pre-

sent before the crisis and are still in place.

2.1. Weak demand

hampers job creation

Weak demand is a major obstacle to

job creation. While EU GDP growth was

1.2 % year-on-year in the second quar-

ter of 2014, potential growth estimates

suggest little room for further accelera-

tion from there under ‘no policy change’

assumptions. Commission estimates put

potential growth in the EU at 1.0 % in

2015, accelerating slightly to 1.4 % in](https://image.slidesharecdn.com/fd1af655-5d67-4954-a059-19619f458af7-150123121918-conversion-gate01/85/KE-BD-14-001-EN-N-17-320.jpg)

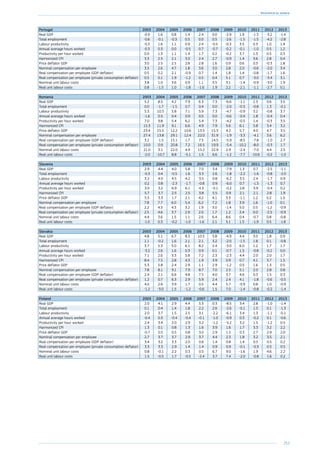

![32

Employment and Social Developments in Europe 2014

improvements in in-firm training, and

this requires a big change of attitude by

companies, skills and productivity will

continue to languish.

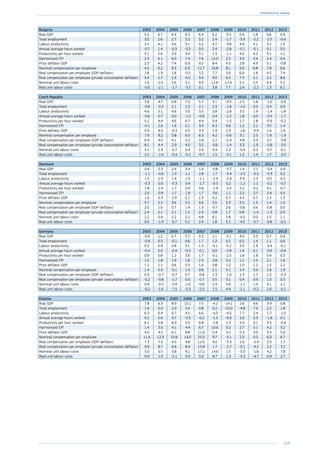

Chart 33: Real change in Gross Disposable Household Income by component in the EU

(year on year; 2005Q1 – 2014Q2)%changeonpreviousyear

-6

-4

-2

0

2

4

6

Q2Q1Q4Q3Q2Q1Q4Q3Q2Q1Q4Q3Q2Q1Q4Q3Q2Q1Q4Q3Q2Q1Q4Q3Q2Q1Q4Q3Q2Q1Q4Q3Q2Q1Q4Q3Q2Q1

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Compensation of employees

Compensation of self-employed

Net property income

Net social benefits

Net social contributions

Net other current transfers

Taxes on income, wealth (negative)

Real GDHI

Real GDP

Source: Eurostat, National Accounts, data non-seasonally adjusted [namq_gdp_k, nasq_nf_tr and namq_fcs_p] (DG EMPL calculations).

Note: GDHI EU aggregate for Member States for which data are available, GDP for EU-28.

5. Who will benefit

from income growth?

5.1. Household incomes

declined in the crisis but

have started to recover

After nearly four years of continuous

declines, gross disposable household

income in the EU (80

) increased in real

terms in the last quarter of 2013, as

result of the general economic recov-

ery and the associated improvements

in labour market conditions. The overall

decline in household incomes had mainly

been driven by job losses, reduced work-

ing hours and wage compression in some

Member States.

In the first years of the crisis, unemploy-

ment benefit systems played an impor-

tant role in stabilising income, while other

items of social expenditure (notably

pensions and health) also helped main-

tain aggregate demand (see Chart 33).

Since 2011, however, the stabilisation

impact of tax and benefit systems has

weakened over the prolonged recession.

This was due to various factors includ-

ing the increasing number of long-term

unemployed losing their entitlements,

the partial phasing-out of the stimulus

measures taken to counter the crisis,

and cuts in social expenditure under

(80

) Estimate based on data for

20 Member States.

pressure of budgetary consolidation.

According to a recent EUROMOD analy-

sis (81

), between 2008 and 2013 the

total impact of changes in the tax and

benefit systems on household dispos-

able income was particularly strong in

Ireland (-17 pps), Greece (-14 pps), Por-

tugal, Spain and Lithuania.

It is to be expected that the redistributive

impact of taxes and transfers increases

with unchanged policy settings when

unemployment increases significantly.

However, policy changes implemented

during the crisis also had an impact on

the income distribution. The analysis

based on EUROMOD (82

) shows that, in

many countries, the measures taken dur-

ing the crisis had either neutral or pro-

gressive impacts on income distribution,

with a few notable exceptions (Germany,

Estonia and Lithuania). It also shows that

similar types of tools can have different

distributional impacts depending on their

design, and independent of the size of

the adjustments.

5.2. Rising poverty

mainly affects the working-

age population and children

As could be expected, poverty and social

exclusion in the EU worsened during

(81

) De Agostini P., Paulus A., Sutherland H.

and Tasseva I. (2014), ‘The effect of tax-

benefit changes on income distribution in

EU countries since the beginning of the

economic crisis’, EUROMOD Working Paper

Series EM9/14 – 02 May 2014.

(82

) De Agostini P., Paulus A., Sutherland H.

and Tasseva I. (2014), ‘The effect of tax-

benefit changes on income distribution in

EU countries since the beginning of the

economic crisis’, EUROMOD Working Paper

Series EM9/14 – 02 May 2014.

the crisis and has shown little sign of

improvement up to 2013, especially in

Member States where economic condi-

tions continue to worsen. The deterio-

ration of labour market conditions has

significantly increased the number of

people on low income or living in jobless

households, with the overall reduction in

household incomes resulting in increased

hardship among the poorest segments

of the population, resulting in a rise in

material deprivation.

The working-age population has been

most affected, mainly due to rising levels

of jobless or low work-intensity house-

holds and increased in-work poverty. In

more than 20 Member States, the risk

of poverty or social exclusion for chil-

dren has risen since 2008, along with

a worsening situation for their (mostly

working-age) parents, with single-par-

ent households facing the highest risks.

Older people (65+) have been relatively

sheltered as pensions have remained

largely unaffected, while income levels

for the working-age population have

stagnated or fallen. In most countries,

women are still more affected by old-age

poverty than men.

The likelihood of entering into and exit-

ing from poverty varies greatly across

Member States and between population

groups (83

). In some countries a significant

proportion of the population is trapped in

persistent poverty, while in others they

may exit poverty for a time but neverthe-

less return. The key risk factors include

(83

) See Chapter 2 in European Commission,

2013c, Chapters 3 and 4 in

European Commission, 2011a.](https://image.slidesharecdn.com/fd1af655-5d67-4954-a059-19619f458af7-150123121918-conversion-gate01/85/KE-BD-14-001-EN-N-34-320.jpg)

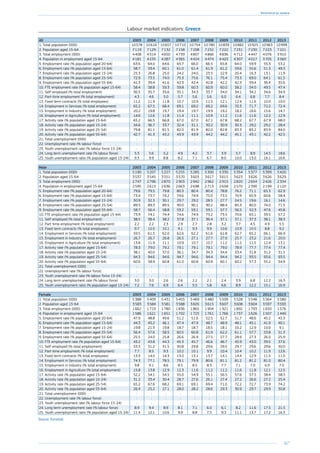

![42

Employment and Social Developments in Europe 2014

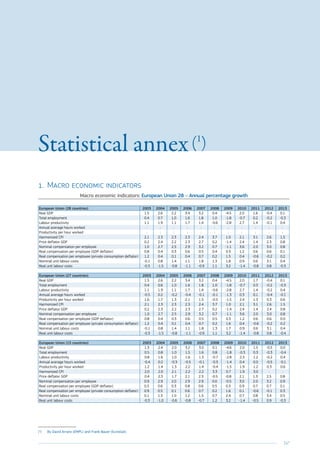

Chart 1: Real GDP in the EU, euro area and United States (left),

and percentage changes over the previous quarter (right)

80

85

90

95

100

105

110

Q1Q4Q3Q2Q1Q4Q3Q2Q1Q4Q3Q2Q1Q4Q3Q2Q1Q4Q3Q2Q1Q4Q3Q2Q1Q4Q3Q2Q1

-4

-3

-2

-1

0

1

2

3

4

5

6

EU-28 EU-28

USUS

Index 2007=100

2007 2008 2009 2010 2011 2012 2013 2014

Source: Eurostat, National Accounts, data seasonally adjusted [namq_gdp_k].

In the first phase of the crisis (2008–10)

the fall in employment in most EU Mem-

ber States was significantly less than the

decline in economic activity especially

when compared with the United States ( 4

).

However the decline in economic activity

had a much greater impact on employ-

ment in some Member States ( 5

) see

Chart 2. Some of this can be explained

by structural factors. In Spain, for

example, the disproportionate impact

on employment (almost twice as large

as the economic shock) ( 6

), reflected the

relative importance of the construction

sector and the country’s highly seg-

mented labour market ( 7

). In contrast,

the strong decline in GDP in Germany

was absorbed through a reduction of

working time (as well as productivity)

rather than a reduction of employment,

notably due to the widespread use of

short-time working arrangements (as

also used in Austria and Belgium) ( 8

).

Finally, it should also be noted that the

more or less large transmission in terms

of employment and income impacted

later on GDP through the channel of

aggregate demand.

Variations in the stabilising impact of

national welfare systems also explain

some of the differences in the impacts

of job losses and reduced working

time on household disposable income

across different countries (GDHI, see

Chart 3). For instance, in Italy, the

decline in employment resulted quickly

in a disproportionate drop in house-

hold incomes while the sharp decline

in employment in 2009 in Spain and

Ireland did not result in any immediate

(4

) European Commission (2010a), Employment

in Europe.

(5

) By contrast, in Germany the manufacturing

sector was badly hit by plummeting

exports but high productivity levels led to

a comparatively small fall in employment

relative to that in GDP.

(6

) i.e. employment volume declining by almost

7 % in the year to 2009 Q3, compared to a

decline of the GDP by around 4 %.

(7

) In Poland the high share of temporary

workers also explains the decline in

employment that occurred despite a rather

favourable change in terms of GDP (decline

in growth but no recession).

(8

) The cost of adjustment was spread

across the workforce instead of, in case

of extensive reliance on layoffs, being

concentrated on a relatively small number

of workers suffering large losses of income

(Cahuc and Carcillo (2011)).

fall in income due to the effects of a

fiscal stimulus and automatic stabilis-

ers (though income levels did drop later

as benefit payments ran out). In the

United Kingdom, the moderate impact

on employment was nevertheless fol-

lowed by a drop in household incomes,

while in Sweden and France the declines

in employment levels did not translate

into reduced income levels.

Chart 2: Change in GDP and employment

between 2008 and 2013, EU Member States, in %

-30

-25

-20

-15

-10

-5

0

5

10

15

20

PLSEMTSKDEATBELUEEFRUKEU-28ROLTBGCZDKNLHUFIIELVESPTITCYSIHREL

Employment

GDP

Source: Eurostat, nama_gdp_k and nama_aux_pem.](https://image.slidesharecdn.com/fd1af655-5d67-4954-a059-19619f458af7-150123121918-conversion-gate01/85/KE-BD-14-001-EN-N-44-320.jpg)

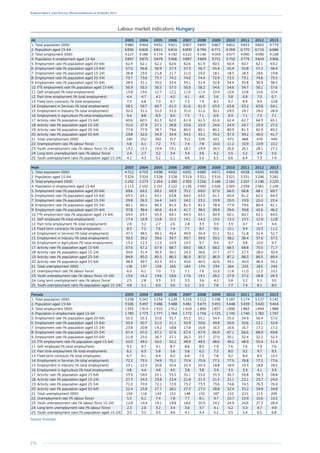

![43

Chapter 1: The legacy of the crisis: resilience and challenges

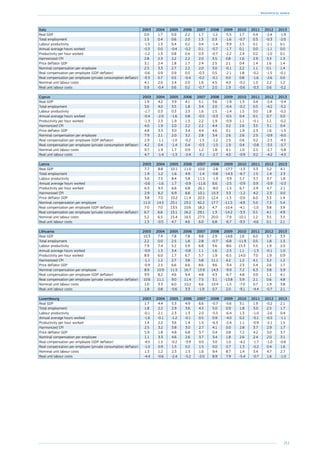

Chart 3: Real GDP growth, real Gross Disposable Household Income (GDHI) growth

and employment growth (No of persons employed), year-on-year change

-8

-6

-4

-2

0

2

4

6

8

10

Q1Q4Q3Q2Q1Q4Q3Q2Q1Q4Q3Q2Q1Q4Q3Q2Q1Q4Q3Q2Q1Q4Q3Q2Q1Q4Q3Q2Q1

EU-28

2007 2008 2009 2010 2011 2012 2013 2014

%changeonpreviousyear

GDHI

GDP

Employment

-8

-6

-4

-2

0

2

4

6

8

10

Q1Q4Q3Q2Q1Q4Q3Q2Q1Q4Q3Q2Q1Q4Q3Q2Q1Q4Q3Q2Q1Q4Q3Q2Q1Q4Q3Q2Q1

EA-17

2007 2008 2009 2010 2011 2012 2013 2014

%changeonpreviousyear

GDHI

GDP

Employment

-8

-6

-4

-2

0

2

4

6

8

10

Q1Q4Q3Q2Q1Q4Q3Q2Q1Q4Q3Q2Q1Q4Q3Q2Q1Q4Q3Q2Q1Q4Q3Q2Q1Q4Q3Q2Q1

DE

2007 2008 2009 2010 2011 2012 2013 2014

%changeonpreviousyear

GDHI

GDP

Employment

-8

-6

-4

-2

0

2

4

6

8

10

Q1Q4Q3Q2Q1Q4Q3Q2Q1Q4Q3Q2Q1Q4Q3Q2Q1Q4Q3Q2Q1Q4Q3Q2Q1Q4Q3Q2Q1

ES

2007 2008 2009 2010 2011 2012 2013 2014

%changeonpreviousyear

GDHI

GDP

Employment

-8

-6

-4

-2

0

2

4

6

8

10

Q1Q4Q3Q2Q1Q4Q3Q2Q1Q4Q3Q2Q1Q4Q3Q2Q1Q4Q3Q2Q1Q4Q3Q2Q1Q4Q3Q2Q1

FR

2007 2008 2009 2010 2011 2012 2013 2014

%changeonpreviousyear

GDHI

GDP

Employment

-8

-6

-4

-2

0

2

4

6

8

10

Q1Q4Q3Q2Q1Q4Q3Q2Q1Q4Q3Q2Q1Q4Q3Q2Q1Q4Q3Q2Q1Q4Q3Q2Q1Q4Q3Q2Q1

GDHI

GDP

Employment

IT

2007 2008 2009 2010 2011 2012 2013 2014

%changeonpreviousyear

Source: Eurostat, National Accounts [namq_gdp_k, namq_aux_pem, nasq_nf_tr and namq_fcs_p] (DG EMPL calculations).

A strong and uneven impact

on unemployment

For the EU as a whole, the unemploy-

ment rate rose from 7.0 % in 2008

to 9.6 % in 2010, reaching 10.8 %

in 2013. Chart 4 shows that, in two-

thirds of EU countries, unemployment

increased mainly in the period up

to 2010 but that in those countries

that experienced a double recession,

unemployment rose substantially after

2011. The impact was strongest (in

terms of percentage points) for the

young, the low-skilled and non-EU

foreign workers — groups that already

faced higher risks of joblessness

before the recession.](https://image.slidesharecdn.com/fd1af655-5d67-4954-a059-19619f458af7-150123121918-conversion-gate01/85/KE-BD-14-001-EN-N-45-320.jpg)

![45

Chapter 1: The legacy of the crisis: resilience and challenges

While most countries with high exit rates

from short-term unemployment also

have high exit rates for the long-term

unemployed, a few countries (such as

Germany and the United Kingdom) that

manage to ensure rapid rates returns to

employment for the short-term unem-

ployed, have nevertheless relatively

low exit rates for the long-term unem-

ployed ( 15

), see Chart 6. In these countries,

a limited proportion of the unemployed

become long-term unemployed but when

they do, they have difficulties returning

to employment.

(15

) The gap between the exit rates for short

versus long-term unemployed is much

higher in the UK and Germany (respectively

22 and 19 pps) than the EU average

(11 pps, with rates of 38 % and 27 %). On

the contrary Denmark and Estonia manage

to maintain high exit rates into employment

also for the long-term unemployed and have

relative low gaps between the two rates

(respectively 8 and 6 pps).

Chart 6: Exit rate from short-term unemployment

(less than one year) and long-term unemployment

(more than 1 year) into employment between 2012/13Exitratefromlong-termunemployment

intoemployment(2012/2013)

Exit rate from short-term unemployment into employment (2012/2013)

0 10 20 30 40 50 60

0

10

20

30

40

50

60

UK

MT

DE

AT

SE

LT

LV

NL

HU

FR

IT

IE

HR

PL

CZ

PT

DK

CY

BG

ES

EE

FI

SI

EL

RO

SK

Source: Eurostat, EU-LFS, ad-hoc transition calculations based on longitudinal data. No data for BE

and LU. Exceptions to the reference year: NL: 2011/12 instead of 2012/13.

Exit rates out of long-term unemployment

seem less sensitive to changes in the eco-

nomic cycle ( 16

) than they are for the short-

term unemployed, which suggests that an

economic recovery may not bring back into

employment many of those who are cur-

rently long-term unemployed. This is likely

to have lasting negative consequences, such

as the depreciation of human capital, nega-

tive signalling effects for potential employ-

ers and demotivation for those concerned,

with further risks in terms of benefits

dependency, poverty and social exclusion.

It should also be noted that 20 % of the

long-term unemployed in 2013 have never

worked before and are likely to need vari-

ous forms of support in order to find a first

job. This raises concerns regarding access

to benefits and the risk of social and eco-

nomic marginalisation.

(16

) For instance, the coefficient of correlation with

changes in employment over 2008–10 is much

stronger for the exit rates out of short-term

unemployment into employment (0.92, significant

at 1 %) than with the exit rates out of long-term

unemployment (0.53, significant at 5 %).

Chart 7: Long-term unemployment in % of active population for EU Member States (2002–2008–2013)

0

2

4

6

8

10

12

14

16

18

20

ELESHRSKPTIEBGITCYLVSIEU-28LTHUPLFRBEEEROCZMTUKNLDELUDKFISEAT

20132002 2008

Source: Eurostat, EU-LFS [une_ltu_a].

Young people tend to experience shorter

spells of unemployment and higher transi-

tion rates into employment than other age

groups, but this is less true now than it was

in the past ( 17

), with an increase in the share

of long-term unemployed among the young

unemployed, especially for the age group

25–34 ( 18

). Significantly, however, having

a tertiary degree appears to be a form of

protection against long-term unemploy-

ment, albeit probably at the expense of

less qualified young people competing for

the same jobs.

(17

) According to longitudinal data of the EU-LFS

(European Commission (2012a), Chapter 1),

even if young people continued to have

better exit rates out of unemployment than

older workers, their situation worsened since

2008. In 2010-11, they had a much higher

chance of losing their job (8 %) compared

to prime-age (3 %) and older (2 %) workers.

In addition their transition rate back into

employment had sharply diminished, from

40 to 30 %. These findings are confirmed by

analysis of RWI (2014) drawing on micro-

data from the EU-SILC.

(18

) Strictly speaking the group of young people

is defined as those aged 15–24; however for

many indicators analysis of the age group

25–34 is also meaningful as this age group

has also been strongly affected by the crisis.](https://image.slidesharecdn.com/fd1af655-5d67-4954-a059-19619f458af7-150123121918-conversion-gate01/85/KE-BD-14-001-EN-N-47-320.jpg)

![46

Employment and Social Developments in Europe 2014

Chart 8: Youth unemployment in % of active population (aged 15–24)

0

10

20

30

40

50

60

70

ELESHRITCYPTSKBGPLHUIEFRBEROSEEU-28LVLTSIUKFICZEELUMTDKNLATDE

20132008

Source: Eurostat, EU-LFS [lfsa_urgan].

Chart 9: Temporary employment as percentage of the total number of employees

20132007

0

5

10

15

20

25

30

35

ESPLPTSINLSEFIFRDEEU-28CYITHRELDKATBECZIEHULUUKBGSKMTLVLTEERO

Source: Eurostat, EU-LFS [lfsa_etpgan].

Levels of unemployment among youth

tend to vary more than total unemploy-

ment because their job prospects are

more sensitive to the business cycle ( 19

)

and because of the variety of policies

and institutions supporting school to

work transitions (education and train-

ing systems, contractual arrangements,

minimum wage, etc.) ( 20

). In this respect,

the apprenticeship systems in Germany

and Austria are commonly highlighted

as being mechanisms that overcome

many of the obstacles and, in particu-

lar, ensure high transition rates from

(19

) According to IMF (2014), the business cycle

‘explains up to 70 % of changes in the youth

(15–24) unemployment rates in stressed

euro area countries’. It estimates that

an additional percentage point of annual

growth could lower the unemployment rate

from 0.8 pp in Greece and Portugal

to 1.9 pps in Spain.

(20

) Another factor explaining the wide variation

of the youth unemployment rate across

Member States is the very diverse level of

participation of young people in the labour

market while still being in education.

temporary to permanent contracts

(Eichhorst et al, 2012).

In 2013 the proportion of young people

aged 15–24 in the EU who were nei-

ther in employment, education or train-

ing (commonly called NEETs) was 13 %

in 2013 (compared to 10.8 % in 2008),

and exceeding 20 % in Greece, Bulgaria

and Italy ( 21

). In most countries, how-

ever, the increase in the NEET rate since

2008 has been mainly the result of an

increase in unemployment, rather than

inactivity ( 22

), which implies that most

(21

) In Bulgaria, Romania and Italy the majority

of young NEET were inactive, in Greece,

Spain or Croatia most of them (around 70 %)

were unemployed (i.e. looking for a job).

(22

) At EU level, the share of unemployed in the

whole age class 15–24 has risen by 2.6 pps

(from 6.6 % to 9.2 %) while the number of

inactive (not in education or training) only

slightly changed (by 0.3 pp, from 7.4 to

7.7 %).

‘newly’ NEET young people are actually

looking for work.

Changes affecting

those in work: non-

standard employment,

job quality and informality

Since the recession, not only has the

quantity of jobs been affected but also

their quality as reflected by various indi-

cators (see also Chapter 3). In this regard

the share of part-time jobs in overall

employment rose from 17.5 % in 2008](https://image.slidesharecdn.com/fd1af655-5d67-4954-a059-19619f458af7-150123121918-conversion-gate01/85/KE-BD-14-001-EN-N-48-320.jpg)

![49

Chapter 1: The legacy of the crisis: resilience and challenges

strongly in those Member States most

affected by the crisis (Spain, Italy, Ire-

land, Malta, United Kingdom). In some

Eastern/Southern countries where dep-

rivation had been improving before the

crisis, the trend reversed and material

deprivation increased dramatically after

the crisis (Lithuania, Latvia, Estonia,

Cyprus, Greece, Hungary and to a lesser

extent Bulgaria).

Working age adults have been especially

affected, reflecting the deterioration of

labour market conditions, with the worst

hit countries being Spain, Italy, Greece,

the Baltic States, but also the United

Kingdom ( 33

). Moreover, since many such

working age adults live in households

with children, child poverty has also risen

across Europe as a whole. In contrast, the

risk-of-poverty indicator for older people

showed a significant decline in most

Member States between 2008 and 2013

reflecting the fact that pensions have, to

a large extent, remain unchanged during

the crisis.

(33

) See European Commission (2014a).

Chart 13: Activity rate across EU Member States,

2003, 2008 and 2013, in % of population aged 15–64

55

60

65

70

75

80

85

SENLDKDEUKATFIEEESLVCYPTCZLTEU-28FRSILUSKIEBGELBEPLHUMTROITHR

20132003 2008

Source: Eurostat, EU-LFS [lfsi_act_a].

Chart 14: Activity rate (15–64) compared to 1990 and 2007 levels, for selected countries, in pps

-7

-6

-5

-4

-3

-2

-1

0

1

2

19981997199619951994199319921991

France US Italy

FinlandUKSweden

-4

-3

-2

-1

0

1

2

3

201320122011201020092008

Spain Germany Sweden

FinlandUK IrelandUS

Source: OECD. Source: Eurostat, EU-LFS and OECD data for the US.

Due to the combination of life expectancy,

lower participation in the labour market

and household composition (single parent

families), women are at higher risk of

poverty or social exclusion than men in

all Member States, with the exception of

Spain and Portugal.

2.2. Participation

in education and in the labour

market continued to rise

Economic participation, as measured by

the activity rate indicator ( 34

), has con-

tinued to increase since 2008 in most

Member States, in contrast to the experi-

ence in past recessions. While the employ-

ment rate declined from 65.7 % in 2008

to 64.1 % in 2013 for the EU as a whole, the

activity rate increased from 70.7 % in 2008

to 71.9 % in 2013. It implies that the drop

in the number of jobs mainly translated

into a rising number of unemployed and,

only to a limited extent, a rising number of

‘discouraged workers’ (see Section below).

This EU experience also contrasts with the

decline in activity rate witnessed in the

United States since 2008 ( 35

).

Reductions in activity rates in previous

crises are attributed to a higher share

of working-age persons withdrawing

(34

) The activity rate measures the share, among

the working-age population, of those being

economically active, i.e. either in employment

or unemployed, according to the ILO

definitions. While this indicator counts the

total number of people in employment and

unemployment and country-comparisons may

be influenced by differences in institutional

factors (such as incentives to be registered

as unemployed), the analysis of changes of

activity rate over time remains meaningful,

in particular to analyse behavioural changes

compared to previous recessions.

(35

) Note that for the US, several papers (e.g. Barnes

et al (2013)) show that the decline in

participation since 2008 reflects, to a great

extent, long-term demographic and behavioural

changes rather than cyclical developments.](https://image.slidesharecdn.com/fd1af655-5d67-4954-a059-19619f458af7-150123121918-conversion-gate01/85/KE-BD-14-001-EN-N-51-320.jpg)

![50

Employment and Social Developments in Europe 2014

from the labour market, resulting in their

decline between 1990 and 1994 and a

very slow return to previous levels, sub-

stantially so for Sweden and Finland,

while increasing slightly in France (and the

United States), see Chart 14. By contrast,

since 2007, activity rates have continued

to increase in many EU countries, even

those strongly affected by the recession.

Increase in activity continued

to be driven by women and older

workers

The increase in the activity rate since

2008 has mainly been driven by the

rising participation of women and older

workers throughout the recession see

Chart 15. This is seen to be due to a

number of factors: structural increases

in their activity rate due to cohort

effects and rising levels of education;

policy measures designed to encour-

age increased female and older workers

participation( 36

); and the fact that the

initial labour market shock did not hit

women and older workers as strongly as

prime-age males.

Chart 17 shows that the decline in activ-

ity rate for prime-age men was lim-

ited (–0.8 pp) compared to the decline in

(36

) The increase in older workers participation

over the last decades was also driven by

an overall improvement in their health

status, see European Commission (2011a),

Chapter 5.

their employment rate (–4.8 pps), indicat-

ing that they were the group least likely to

fall into inactivity if they lost their job. LFS

data for 2013 also shows that, if prime-

age men become unemployed, they are

more likely to receive unemployment ben-

efits (43 %) than young people (18 %) or

prime-age women (36 %), notably due

to their more favourable employment

histories. This is one of the factors that

promote continuation of job search rather

than ‘discouragement’ and inactivity.

Chart 15: Activity rate by group (age and sex), EU-28, 2002–13 (in %)

30

40

50

60

70

80

90

100

201320122011201020092008200720062005200420032002

Men 15-24 Men 25-49 Men 50-64

Women 25-49Women 15-24 Women 50-64

75.7

92.6

48.3

64.3

40.9

43.4

44.9

92.0

72.1

39.3

79.7

56.9

Source: Eurostat, EU-LFS, [lfsi_agan].

Chart 16: Change in the activity rate by group

(age and sex) in EU-28, 2008–13 compared

to 2002–08, in percentage points

-4

-2

0

2

4

6

8

2002-08 2008-13

15-24 25-49 50-64

WomenMenWomenMenWomenMen

7.2

6.3

3.3

4.5

-1.4

-0.2

-0.8

0.2

1.4

2.6

-2.8

-0.6

Source: Eurostat, EU-LFS, [lfsa_argan].

Chart 17: Change in the employment and activity

rates by group (age and sex) in EU-28, 2008–13,

in percentage points

-8

-6

-4

-2

0

2

4

6

8

WomenMenWomenMenWomenMen

15-24 25-49 50-64

Changes in ER (pps) Changes in AR (pps)

4.9

6.3

3.3

0.9

-1.4

-3.9

-0.8

-4.8

1.4

-1.6

-2.8

-6.1

Source: Eurostat, EU-LFS, [lfsa_argan] and [lfsa_ergan].

Since 2008, the activity rates of older

workers (55–64) increased substan-

tially in most countries even in the

most affected countries ( 37

) while they

had been decreasing during the 1990s

recession ( 38

). Several changes explain

this difference.

• Older workers have been (in com-

parison to the 1990s) less affected

by job losses (see Chart 18) nota-

bly because their educational levels

(37

) In Spain, Portugal and Ireland, decreases

for men were more than offset by increases

for women.

(38

) For instance: in the UK (–1.6 pps over

1990–95), Italy (–4.2 pps over 1991–95)

and Germany (–2.9 pps over 1992–96)

with more pronounced drops for men

(respectively –5.8 pps, –7.3 pps and 4.9 pps).](https://image.slidesharecdn.com/fd1af655-5d67-4954-a059-19619f458af7-150123121918-conversion-gate01/85/KE-BD-14-001-EN-N-52-320.jpg)

![51

Chapter 1: The legacy of the crisis: resilience and challenges

have improved ( 39

) and the sectors

in which they are employed have

changed. Moreover, employers are

often reluctant to lay off their most

experienced workers, who also often

benefit from a better protection

(higher severance pay) than younger

workers due to longer employment

histories ( 40

).

• If they become unemployed, older

workers are less likely than before

to withdraw from the labour market

not least because of policies intro-

duced over the last two decades

to extend working lives, such as

reforms in pension schemes (general

increase in the statutory retirement

age), and early retirement schemes.

Moreover, alternative options such

as disability schemes have been

closed or made less accessible ( 41

).

The continued increase in female activity

rates also results from a combination

of factors.

• Women tend to work in sectors that

are less hit by the recession ( 42

) (see

also European Commission (2013),

Chapter 3). This seems to explain

most of the better performance of

women’s employment during the

crisis, while the ‘added-workers’

effects may also have played a part

(see Box 1).

• There has been a structural increase in

the participation of women, mainly due

(39

) Between 1992 and 2008, the overall level of

education of older workers increased more

quickly than for prime-age workers, even

when excluding the effects of the rising level

of education among women. EU-LFS data

for EU-15 countries shows that the share

of low-educated among male older workers

dropped sharply, from 53.9 % in 1992 to

32.3 % in 2008 (–21.6 pp) compared to

prime age workers (from 40.2 % to 28.2 %

or –12.0 pps). The share of tertiary educated

persons among older men increased more

sharply than among prime-age workers.

(40

) The share of older workers under involuntary

temporary contract is also much lower

(4.4 % among those aged 55–64 compared

to 8.1 % for prime-age and 14.7 % for young

workers, i.e. EU-LFS data for EU-28 in 2013).

(41

) European Commission (2011), Chapter 5.

(42

) Female employment was less affected by

the recession than male (respectively –0.6 %

over 2008–13 against –4.7 %). While the

two male-dominated sectors (manufacturing

and construction) were strongly affected by

the crisis, the two main female-dominated

sectors (education and human health and

social work) resisted well.

to rising levels of education of women

over time ( 43

). This has brought the

behaviour of women in the labour mar-

ket much closer to that of men with a

rising share of dual-earner households.

• Measures supporting female par-

ticipation such as flexible working

arrangements, the removal of finan-

cial disincentives for second earners,

childcare and elderly care facilities

have also played a role, together

with measures to retain older women

longer in the labour market ( 44

).

Until 2013, there were no signs of

a reversal in the policies supporting

female participation (see Section 4)

(43

) For instance, among women aged 25–49

(50–64) the share of those with not more

than lower secondary education decreased

from 41 to 22 % (64 to 38 %) between 1995

and 2013, or –19 pps (–26 pps), to the profit

of the medium and high educational groups

(based on EU-LFS data on EU-15).

(44

) Analysis by age and education confirms that

the overall increase in female activity rate

is not only due to change in the composition

(i.e. increase in average level of education)

and affected most sub-groups of women.

although this may no longer be the

case in some countries that have

applied major fiscal consolidation

measures ( 45

). Moreover, women

tend to be over-represented in public

and non-market service sectors that

are now becoming more adversely

affected by fiscal consolidation in

many Member States ( 46

).

Moreover, recent trends have not led to

a substantial decrease in the large gen-

der inequalities in the labour market that

persist in many EU Member States to

the disadvantage of women, in terms of

activity and employment rates as well as

in terms of part-time work and earnings.

(45

) European Commission (2012b).

(46

) European Parliament (2014).

Chart 18: Older workers less affected by job losses since 2008

than in the 1990s: changes in employment rates for prime-age

(25–54) and older (55–64) age groups in 1992–96 and 2008–13,

in percentage points, selected Member States

-15

-10

-5

0

5

10

15

2008-13

1992-96

2008-13

1992-96

2008-13

1992-96

2008-13

1992-96

2008-13

1992-96

2008-13

1992-96

2008-13

1992-96

2008-13

1992-96

25-54 55-64

EU-15 DE ES FR IT FI SE UK

Source: Eurostat, EU-LFS, [lfsi_emp_a].](https://image.slidesharecdn.com/fd1af655-5d67-4954-a059-19619f458af7-150123121918-conversion-gate01/85/KE-BD-14-001-EN-N-53-320.jpg)

![52

Employment and Social Developments in Europe 2014

Box 1: Some mixed evidence about ‘added-worker

effects’ during the recession

A recession can impact on labour market participation of ‘partnered’ women in two

ways: (a) it can discourage women from looking for a job or postpone their decision

(discouragement effect) or (b) it can foster participation in order to compensate for

the job loss of the partner (added-worker effect). It is hard to determine whether

the increase in female participation was due partly to the latter — or whether it

was entirely caused by other structural factors due to education and cohort effects.

Several reports support the added worker hypothesis without being totally conclusive:

• European Commission (2011b) shows that the activity rate of married women

with children was more reactive to male unemployment and that it has increased

faster since 2008 than for other women*.

• OECD (2012a) shows that in many countries partnered women were more likely

to have increased their working hours during the crisis than single women.

• European Commission (2012b) points out that over 2007–09, dual-earner

couples had lost ground mainly to the benefit of female breadwinner couples.

• European Commission (2013) shows that over 2007–11, the share of working

women with a non-working male partner increased in most Member States.

• Bredtmann et al (2014) found that women whose partner becomes unemployed

have a higher chances of entering the labour market and changing from part-

time to full-time employment than women whose partner remains employed.

The added worker effect varies over both the business cycle and the different

welfare regimes within Europe**.

• EU-SILC*** data do not show such added-worker effect, as women’s transitions

from inactivity to employment and from part-time to full-time employment do

not increase between 2007 and 2012.

While there is no robust evidence of an added-worker effect during the crisis, the

stronger share of women in employment, hours worked and earnings and the

increasing share of dual-earner households has helped to cushion the impact of

the recession on household incomes (OECD (2014c)).

Notes: * However, this is not true for all countries and may be due to other effects — for instance

the increase in investment in childcare facilities. ** For instance, for the UK, Bryan and Longhi (2013)

found an increase in job searches but only among single earner couples —which does not translate

into more success in finding work (consistent with declining job-finding rate), at least in the short-

term. *** Eurostat, EU-SILC, [ilc_lvhl30]. Note that these indicators are not available for different

groups of women (partnered or not, with or without children).

Limited increase in discouraged

workers during the recession

The number of persons available and want-

ing to work but not looking for a job ( 47

) (the

‘discouraged workers’) increased from 7.4

million in 2008 to 9.3 million in 2013 (or

from 3.1 % to 3.8 % of the labour force).

This increase was much lower than the

increase in unemployment and long-term

(47

) These are jobless persons (neither employed

nor unemployed) who do not qualify for

recording as unemployed (from the ILO

definition) because they are not actively

looking for a job (anymore), despite the fact

that they want to work and are available

for work. According to Eurostat, they include

‘discouraged workers but also persons

prevented from job seeking due to personal

or family circumstances’. However, for

convenience, this Section uses the term

‘discouraged workers’ to refer to all the

inactive persons wanting to work but not

looking for a job.

unemployment ( 48

) and can be viewed as

a positive sign insofar as it means that

unemployed persons continue to look for a

job and can potentially benefit from activa-

tion or (re)training.

Institutional factors can contribute to

limiting the number of discouraged

workers. For instance, countries where

the share of discouraged workers is the

(48

) Since 2008, the number of unemployed

increased from 16.8 million to 26.4 million

in 2013, and the number of long-term

unemployed almost doubled in the same

period (from 6.2 million to 12.3 million).

highest tend to be those with relatively

limited support for the unemployed or

the long-term unemployed ( 49

). Gener-

ally speaking, the countries that recorded

increases in discouraged workers since

2008 ( 50

) were those that combined a

strong labour market impact of the crisis

and relatively weak support services to

the unemployed ( 51

), whether in terms of

spending on active labour market policies

or income support.

There can also be other explanatory fac-

tors such as the extent to which there

are, or are not, incentives to register

as unemployed, the link to social assis-

tance schemes, or the actual probability

of finding a job. The availability of care

services for children or dependents may

also affect the labour supply given that

36 % of ‘discouraged workers’ in 2013

were women of prime-age (25–54),

a group more likely to be affected by

issues related to the combination of work

and family life. This share was highest

in Spain (41 %), Italy (47 %) and Greece

(49 %), all countries recognised as being

poor performers in terms of supporting

improved work-life balance ( 52

).

Remaining in education

Since 2008, an increasing number

of young people have remained in, or

have returned to, education, notably

within the younger age group (18–24)

and especially in Member States where

youth unemployment was especially high

(Spain, Ireland and Portugal) and where

the share of young people in education

had been below the EU average in 2004.

In some countries however, participation

in education has either stalled (Greece,

Italy, Romania, the Czech Republic and

Slovakia), or even declined (Poland and

Hungary).

(49

) In 2013, a very low share of long-term

unemployed were receiving unemployment

benefits (or assistance) in Italy (2 %),

Croatia (10 %), Bulgaria (1 %), Latvia (3 %)

or Estonia (4 %), all characterised by a

higher than average share of discouraged

workers –while the receipt rate of benefits

was rather high in some of the countries

displaying a low share of ‘discouraged

workers’ such as France, Germany, Malta,

Belgium and Denmark.

(50

) Croatia and Cyprus (strong increase) and

Finland, Romania, Spain, Italy, Hungary,

Greece and Slovenia (significant increase).

(51

) According to typology presented in Stovicek

and Turrini (2012)

(52

) They display high gender employment gaps,

high incidence of inactivity due to family

obligations as well as relatively insufficient

provision of child and/or dependent care

facilities (see European Commission (2013),

Chapter 3).](https://image.slidesharecdn.com/fd1af655-5d67-4954-a059-19619f458af7-150123121918-conversion-gate01/85/KE-BD-14-001-EN-N-54-320.jpg)

![53

Chapter 1: The legacy of the crisis: resilience and challenges

Chart 19: Proportion of young people in education or training, 18–24, % of age group

-20

-15

-10

-5

0

5

10

15

20

-80

-60

-40

-20

0

20

40

60

80

EU-28SILUDKNLDEPLLTCZEESKKRBEELLVFIESHUFRPTBGIEITROATSEMTCYUK

2004-08 change (pps)

2008-13 change (pps)

% of young people in education (2013), rhs

Source: EU-LFS, Social Situation Monitor calculations.

Notes: Only young people in education or training not economically active are measured. Countries are sorted by 2013 levels.

Chart 20: Share of 20-24 having completed upper secondary education in 2008 in %

and changes over 2004-08 and 2008-13 in percentage points

-20

-15

-10

-5

0

5

10

15

20

-100

-80

-60

-40

-20

0

20

40

60

80

100

HRSKCZPLSILTIESEFICYATFRBGHUBEELEELVEU-28ROUKITNLDELUDKMTESPT

2004-08 change (pps)

2008-13 change (pps)

% of 20-24 having completed upper secondary education in 2008 (rhs, %)

Source: Eurostat, EU-LFS [edat_lfse_08]; sorted by 2008 level.

Chart 21: Over-qualification rate: share of tertiary-educated workers working in low or medium-skilled

occupations (in %), age group 25–34, 2008 and 2013

0

5

10

15

20

25

30

35

40

45

CYESIEELBGPLITUKEEEU-28FRSKLVROHRATBESESILTHUCZFINLPTDEDKMTLU

20132008

Source: Eurostat, EU-LFS and DG EMPL calculations.

Notes: tertiary-educated is defined as workers having the highest level of qualification equal or above ISCED 5–6; low and medium-skilled occupations are

defined as occupational groups ISCO 4 to 9.

Overall, educational outcomes have

improved in most Member States (see

Chart 20) but especially so in those

countries where they were less favour-

able ten years ago and the share of

early school leavers from education

and training decreased. Delaying labour

market entry by remaining in educa-

tion is a rational response in times of

recession, but it is not yet clear whether

this will result in better labour market

outcomes in terms of human capi-

tal and skills development. The long-

term impact of increased educational

level will notably depend on the qual-

ity of education, on whether the skills

acquired are adapted to labour market

needs, as well as on whether cuts in

spending affect the quality of educa-

tion in the short to medium term (see

Section 4.3).](https://image.slidesharecdn.com/fd1af655-5d67-4954-a059-19619f458af7-150123121918-conversion-gate01/85/KE-BD-14-001-EN-N-55-320.jpg)

![62

Employment and Social Developments in Europe 2014

Across the EU as a whole, there is little

evidence that the recession as such led to

any major change as regards young peo-

ple living with their parents (see Chart 36)

although there have been substantial

increases (e.g. + 4 percentage points) in

the proportion of young people living with

their parents in Ireland, Spain, and Greece

since 2008. Qualitative research shows

that people sometimes have had no other

choice than to rely on family solidarity

(see Annex 3, Extract 4).

3.3. Impact on health

and access to healthcare

The potential long-term impact of the

crisis on health determinants (i.e., unem-

ployment, quality of work, precarious liv-

ing conditions) is threatening to increase

health inequalities between social groups

and Member States. There is extensive

research documenting the negative

impact of economic hardship on the

health status of individuals, which in a

recession may be further exacerbated by

greater difficulties in accessing or paying

for healthcare.

Many studies report that, during reces-

sions, individuals are more likely to suf-

fer from depression and stress (Cooper,

2011). Otterbach (2014) also reports, on

the basis of long-lasting panel data, that

being unemployed or insecure in one’s

job has a strong negative effect on life

satisfaction and health.

OECD (2014d) also notes evidence of a

possible link between the economic crisis

and obesity. Many families, especially in

the worst hit countries, have been forced

to cut food consumption or to switch to

lower-priced and less healthy foods.

Brenner (2013) identified unemploy-

ment as an important risk factor for

heart disease mortality at the start of the

2008/9 recession. Stuckler et al. 2011,

Reeves et al. 2012 reports a higher sui-

cide rate during recessions. In Italy, the

suicide rate increased by 10 % among

men younger than 65 between 2006 and

2010, with an increase by 25 % within

the 50–54 age group ( 70

).

(70

) Source: Eurostat, Causes of death —

crude death rate per 100 000 inhabitants

[hlth_cd_acdr].

Chart 36: Access to autonomy: changes in the share of young people

living with their parents (2004–13), in percentage points

-10

-8

-6

-4

-2

0

2

4

6

8

10

12

EU-28CYIEESELFRPTHRUKITATLULVNLMTDKSKFIHULTPLEERODESIBECZBGSE

2004-08

2008-13

Recent decrease Recent increase

ppchange(2004-13)

Source: Social Situation Monitor, based on LFS data.

Chart 37: Unmet need for healthcare by employment status

0

5

10

15

20

25

30

LVBGROEEELITPLCYPTDEFRHUSEEU-28BEFISKMTLUHRNLLTATDKUKESCZSIIE

Employed persons

Unemployed persons

%

Source: EU-SILC, Eurostat. Unmet need for healthcare is measured as the share of individuals

renouncing healthcare because of: cost, i.e. the person cannot afford to pay for it (too expensive); the

waiting list; or distance or means of transportation ( 1

).

(1

) This definition also applies to the European Core Health Indicator (ECHI) on Equity of access to

healthcare service (ECHI 80) for total population and by educational level.

Chart 38: Correlation of real expenditure per capita on sickness,

healthcare, disability and unmet healthcare needs, 2007–11

Percentagepointschange(2007-11)

inunmethealthcareneed

Growth (2007-11) in real public expenditure per capita in sickness and disability, %

NL

LV

PT

FI

BG

HU

EE

PLCY

LT

IELU

EL IT

ES

CZ

BE

DK

DE

FR

MT

AT ROSI

SK

SE

UK

-25 -15 -5 5 15 25 35 45 55

-10

-8

-6

-4

-2

0

2

4

Source: ESSPROS for expenditure in sickness, healthcare and disability and EU-SILC, Eurostat for unmet

need for healthcare.

The harmful and hazardous use of

alcohol and other substances are also

key factors in the development of

social and health inequalities in the

EU, influenced by unemployment and

economic downturns (European Com-

mission, 2013, Marmot et al. 2013).

Chart 37 shows that, in many Mem-

ber States, the unmet need for

healthcare is much greater among the

unemployed than among the employed.

Eurofound (2014, forthcoming) also

identified situations in which peo-

ple lost access to healthcare during](https://image.slidesharecdn.com/fd1af655-5d67-4954-a059-19619f458af7-150123121918-conversion-gate01/85/KE-BD-14-001-EN-N-64-320.jpg)

![77

Chapter 1: The legacy of the crisis: resilience and challenges

Large costs and rights differences between

the use of permanent and non-standard

work ( 100

) contracts may encourage compa-

nies to opt for the latter. From an employ-

ee’s point of view, however, these jobs may

be much less effective as stepping-stones

to permanent employment and they may

increase the risk of being excluded from

lifelong learning opportunities as well as

social protection (including pension rights)

and financial compensation in cases of

termination without fault.

Despite the trend towards an overall

reduction in EPL and a narrowing of

the legislative gap between temporary

and permanent contracts, the transition

from one to the other has been stead-

ily decreasing since the onset of the

recession in 2008 (Chart 59), signalling

a reduction of the ‘stepping stone’ poten-

tial of temporary contracts and potential

increase in labour market segmentation.

Even in countries where the EPL gap

reduced substantially during the reces-

sion (Czech Republic, Spain and Portugal,

2008–11) transition rates from tem-

porary to permanent contracts did not

increase. In contrast, countries with the

greatest gaps (such as Sweden and Ger-

many) saw some of the highest transi-

tion rates from temporary to permanent

contracts, suggesting that EPL alone can-

not be used to either explain or address

labour market segmentation concerns,

although the 2012 reform of the Spanish

labour market seems to have produced

some signs of improvement in transi-

tion rates from temporary to permanent

contracts compared to the previous year.

(100

) Such as fixed-term contracts, temporary

agency work, part-time work and

independent contract work.

Chart 59: Transition rate from temporary to permanent contracts for selected Member States, 2008–12

%oftemporaryyearbefore

0

10

20

30

40

50

60

70

80

SEDESIFIPTCYPLNLESFRATBEHULVCZLUDKITELMTEEROUKBGSKLT

2012

2010

2008

Low level of temporary

contracts [0-5%]

Medium level [5-10%] High level [10%]

Source: Eurostat, EU-SILC. Member States grouped by level of temporary contracts in total employment: low = 0–5 %, medium = 5–10 %, high = 10 %. For CY,

PL, PT, LU, HU, SK, SE, LT, RO and MT 2011 values used instead of 2012. No data for UK in 2008. No data for IE and HR. No data for DK prior to 2012 and none

reported for LT and LV due to break in series in 2012. Countries which reduced their EPL gap between 2008 and 2011 indicated by the white bars.

Chart 60: ALMP expenditure per person wanting to work (2010)

and exit rates out of short-term unemployment (2010–11)

ALMP expenditure (cat. 1.1-7) per person wanting to work 2010, pps

TransitionsfromSTUtoemployment2010-11,%

NL

LV

PT

FI

HU

EE

PL

CY

LT

IE

EL

ES

CZ

DE

FR

AT

RO

SI

SK

SEUK

0 1000 2000 3000 4000 5000 6000 7000

0

10

20

30

40

50

60

70

R² = 0.25

Correl coeff = 0.50

Source: EU-LFS, EU-LMP database and DG EMPL calculations. For NL and PT transitions from STU to

employment 2011-12 figures used due to availability of data.

5.3. The development

of activation during

the recession: investment

in human capital and

activation yielded positive

labour market outcomes

5.3.1. ALMP design and

funding have been subject

to many changes across the EU

Active labour market policies (ALMPs) that

provide training and job search assistance

to those out of work as well as incentives

to firms to hire them, are seen to contribute

positively to a well-functioning labour mar-

ket, most notably by speeding their return

to employment ( 101

). This is reflected in the

(101

) Section 4.2 above already touches on spending

on active and passive unemployment measures

in its analysis of social investment during

the crisis. However, its assessment of mostly

active measures does not include several

measures such as supported employment and

rehabilitation measures, direct job creation and

start-up incentives, which are included in the

ALMP calculations here.

findings of a study by Kluve (2010) which

examined the conclusions of 137 pro-

gramme evaluations from 96 academic

studies from 19 countries, and which

found that most ALMP measures (with

the exception of direct public employment

programs and programs targeting young

people) had a modest to high likelihood of

producing a significant positive impact on

employment rates ( 102

). This is echoed by

Chart 60. Empirical findings also note that

active labour market policies are also asso-

ciated with a higher matching efficiency

(European Commission, 2014c).

Across the EU as a whole, most of this

expenditure goes on supply side policies,

with some 59 % being devoted to PES and

training,withtheproportionspentontraining

being on the increase. In terms of type of

activelabourmarketpolicies,agreatdealof

divergence exists between Member States.

(102

) Kluve, J., ‘The effectiveness of European active

labor market programs’, Labour Economics

01/2010, Vol. 17, No 6, pp. 904–18.](https://image.slidesharecdn.com/fd1af655-5d67-4954-a059-19619f458af7-150123121918-conversion-gate01/85/KE-BD-14-001-EN-N-79-320.jpg)

![95

Chapter 1: The legacy of the crisis: resilience and challenges

Annex 3: Coping

strategies during

the recession —

Qualitative analysis

This project ( 117

), which was launched

in July 2013 in DG EMPL, investigates

the coping strategies of individuals and

households hit by the crisis, and that as

a result of this, either lost their job, and

therefore their main source of income,

or did not manage to find a regular job

in the first place. Specifically, it seeks to

understand what happens to family and

social ties in the course of a job loss;

what individuals do to remain active;

(117

) Facing the crisis - The coping strategies

of unemployed people in Europe (2014),

available at : http://ec.europa.eu/social/main.

jsp?catId=738langId=enpubId=7729typ

e=2furtherPubs=yes

and, whether individuals’ trust towards

institutions stays intact.

The project is novel in its approach, as it

goes beyond the use of traditional, quan-

titative methods, which help to describe

the economic and social situation of

individuals but oftentimes lack the abil-

ity to provide insights into the behaviour

response of individuals experiencing

hardship. Therefore, in order to uncover

the coping mechanisms for the impact

of the crisis, the project uses qualitative

research methods in addition to quantita-

tive research methods.

The main part of this qualitative research

forms a study, which consists of over

100 face-to-face interviews, conducted

with the help of national experts and the

coordination efforts of a high-level expert

using a sociological approach in seven EU

Member States (Germany, Greece, Spain,

France, Ireland, Portugal and Romania).

As such, in addition to the novelty lying in

the use of a mixed methods approach, the

project is also unique to its kind because of

its broader coverage, enabling international

comparison in times of crisis. The main

qualitative research component is then

complemented by a focus group study con-

ducted by TNS to enable a deeper insight

into coping mechanisms through group dis-

cussion, a specific quantitative research

component using EU-SILC data to analyse

the deprivation profile of households fac-

ing a severe economic shock, and a range

of EU-wide surveys (Eurobarometer, EQLS,

LFS and SHARE) to illustrate trends in dif-

ferent socioeconomic indicators.

Extracts below illustrate different aspects

of the trends reported in the core of

the chapter:

Extract 1: Informal work

Interviews with people having experienced long-term unemployment show that working in the informal economy is a matter of surviving:

‘Yeah, that’s right, if you have no choice, you have no choice... I wasn’t even receiving the RSA [earned income supplement], due to an

incomprehensible administrative hold-up, I had zero income, I mean zero, … I was doing computer repairs out of my house, undeclared,

and I was doing undeclared odd jobs, like mowing lawns, hanging wallpaper, parqueting floors.’ No 52. FR, M, 45 years

Also show that informal economy puts people into fragile situations. A women living in Athens explains how she was working in the

informal sector and was injured:

‘I’m working without insurance and they’re always late in paying me.’ No 21. EL, F, 43 years

‘Last month I had an accident at work...… After 25 days, I’d reached the point where the doctor told me I could walk again, so I returned

to work, …They said, “You better come back to work soon or else we’ll find someone else.”’ No 21. EL, F, 43 years

Extract 2: Running into debt

Interviews with people having experienced long-term unemployment illustrate that people hit by economic hardship face

difficulties in accessing credit and find low support from banks.

Family and friends are a frequent source of loans. Respondents prefer these informal routes to formalised loan agreements,

although such loans are not always emotionally stress free. However, such solutions remain limited as sometimes friends

and family members also experience financial difficulties.

‘Sometimes I have needed to ask a pal for €20 if my money hasn’t lasted over the last few days of the month. That’s normal,

that’s okay, even though it’s not great.’ (DE)

Loans were taken out for two main reasons: A one-off expense, either unexpected (such as a medical expense) or more pre-

dictable (such as a loan to pay one’s taxes); and to help cover daily expenses such as paying utility bills or paying for food.

‘I borrow €50 from a friend of mine at the beginning of each month. I use the money to pay the supermarket. I give back the

money at the end of the month only to borrow it again at the beginning of the next month. I do not seem able to break from

this pattern no matter what.’ (EL, Group 3)

Respondents were generally reluctant to approach banks for loans. Some respondents also mentioned struggling with loans

that they had incurred before the crisis. There was some, but limited mention of using overdraft facilities. Banks are also not

looked upon favourably as they are seen as part of the cause of the financial crisis.

‘I went to the bank to see whether I could delay payments on my mortgage and they told me I couldn’t, I would have to find

a way to take out a loan, they didn’t make it easy for me.’ (ES, Group 3)

Such situations are often reported to generate stress.

‘When someone lends you money your first reaction is relief, but later it’s just one more problem.’ (FR, Group 3)](https://image.slidesharecdn.com/fd1af655-5d67-4954-a059-19619f458af7-150123121918-conversion-gate01/85/KE-BD-14-001-EN-N-97-320.jpg)

![96

Employment and Social Developments in Europe 2014

Extract 3: Adjusting consumption

Interviews with people having experienced long-term unemployment show that people hit by economic hardship first cut expendi-

ture related to holidays and leisure activities, and this is the case whatever the country.

‘We’ve had no holidays in three or four years, maybe four or five.’

However, in countries most strongly hit by the crisis, restrictions are going much further. Restrictions in food and clothes expenditure

are reported. While in France or Germany, food deprivation is not considered an issue, this is not the case in other Member States,

where some cases of food restriction were reported in other Member States.

‘Well, it was quite tough. I mean myself and my wife might not eat for a day or two just to make sure the kids have food, that

kind of thing. […] We’ve just cut everything back as much as we could. We don’t put the lights on until necessary and the same

with the heating and all that kind of stuff.’ No 73. IE, M, 47 years

Energy bills are also a leverage to limit expenditures, and many individuals reported restrictions in this areas.

‘I get, when it’s really cold, I turn the heat up a little and I immediately turn it off and I wear, woollen jumpers, I wear warm

clothes, blankets, and I watch TV. So, I have no problem.’ No 38. ES, F, 53 years

Lastly, keeping a car means a lot to keep employability and efforts are generally being made to keep a car in the household,

but its use is also strongly limited.

‘It is a change in a way because they were never things we had to worry about, there were never things like, you know, putting

€10 or €5 of petrol in the car. This was something I never did, I just filled it up, you know what I mean. […] you’re conscious of

what journey you’re going to make. My daughter lives in Bray which is the other side of Dublin, so you’re sort of thinking, you

decide to go over to see her you’ve got to pay two tolls and petrol.’ No 68. IE, M 51 years

Extract 4: Pooling resources — family solidarities

The coping strategies during the great recession project illustrates that, despite the cultural differences in perceiving the role of intra-

family financial support, people have sometimes no other choice than relying on family solidarity. Among the seven Member States

investigated during the project, support from family was not perceived to a comparable extend in France or Germany compared to

southern Europe Member States. The norm of autonomy varies. Nevertheless, even in Member States where cultural norms would

tend to strengthen family solidarity, adults relying on their parents report that they do so because they have no other income support.

They also clearly say that they are living with their parents because they have no financial means to live independently.

‘I’m only 62 years old, […] I’m not entitled to anything: neither retirement nor unemployment benefit, not even the Social Integration

Income. I am supposed to live off what?! […] Every morning I have to expect… my mother to give me a euro (that’s the truth!) for a

coffee. Then, when I’m out of cigarettes, I don’t drink the coffee, and I say to my mother… “Mother, I need 2€ to buy something…”’

No 89. PT, F, 62 years

‘They’re struggling now themselves because my mam only works three days a week, so she doesn’t get much money at all, and

my dad’s pay got cut as well, recently, so they really have no money to be going out spare; they’re struggling themselves…. So, they

would really like, they are always at me to get a job but, look, I have been trying my hardest lately and there’s nothing coming up for

me.’ No 65. IE, Woman, 22 years

Extract 5: Impact on health and access to healthcare

People hit by economic shock and unemployment often report deterioration in their health status.

In addition to increased medical needs related to economic adverse circumstances, many interviewees report difficulties in meeting

health-related expenses.

‘I am missing many teeth and I cannot make it. In fact, I have several broken teeth, (...) because doing root canals, that’s worth a lot

of money that I do not possess. And, for me, man, I understand that the mouth is essential for food and for all that but I still have a

few teeth and with those I am still managing.’ No 46. ES, M, 43 years

‘I have cholesterol […] if I take pills... if I take the pill my wife and daughters end up not eating and no, I’d rather stay without it than...

all I have is for them.’ No 44. ES, M, 49 years

This adds up to greater difficulties in accessing healthcare, which might be itself reduced subsequently to cuts in expenditure.

‘There is too much discrimination in the healthcare system. Forget it if you want to go to the dentist. You need a thousand euros for

your teeth. If you need an emergency X-ray, you’ll wait a month and a half. Even if you have very advanced cancer, without money,

you can’t get treatment.’ No 17. EL, F, 51 years,

However, there are large national variations in reporting such difficulties. In France and Germany very few interviewees report dif-