Downloaded 414 times

The document discusses the Karachi Inter-Bank Offered Rate (KIBOR) in Pakistan. Some key points: - KIBOR was launched in 2001 by the State Bank of Pakistan and Pakistan Banks Association as a standardized interest rate benchmark. - It is calculated daily based on rates submitted by 20 major commercial banks for different loan durations, from overnight to 3 years. - Banks use KIBOR as a reference rate to set interest rates for corporate and consumer loans. Adding a margin of 2-3% over KIBOR allows banks to earn a profit. - KIBOR promotes transparency and consistency in Pakistan's banking sector interest rates.

Names of the presenters in the group: Hanam Kausar, Sidra Nazar, Mohsin Habib, Umar Shaharyar.

KIBOR is the average lending interest rate for banks in Pakistan, used as a basis for lending rates.

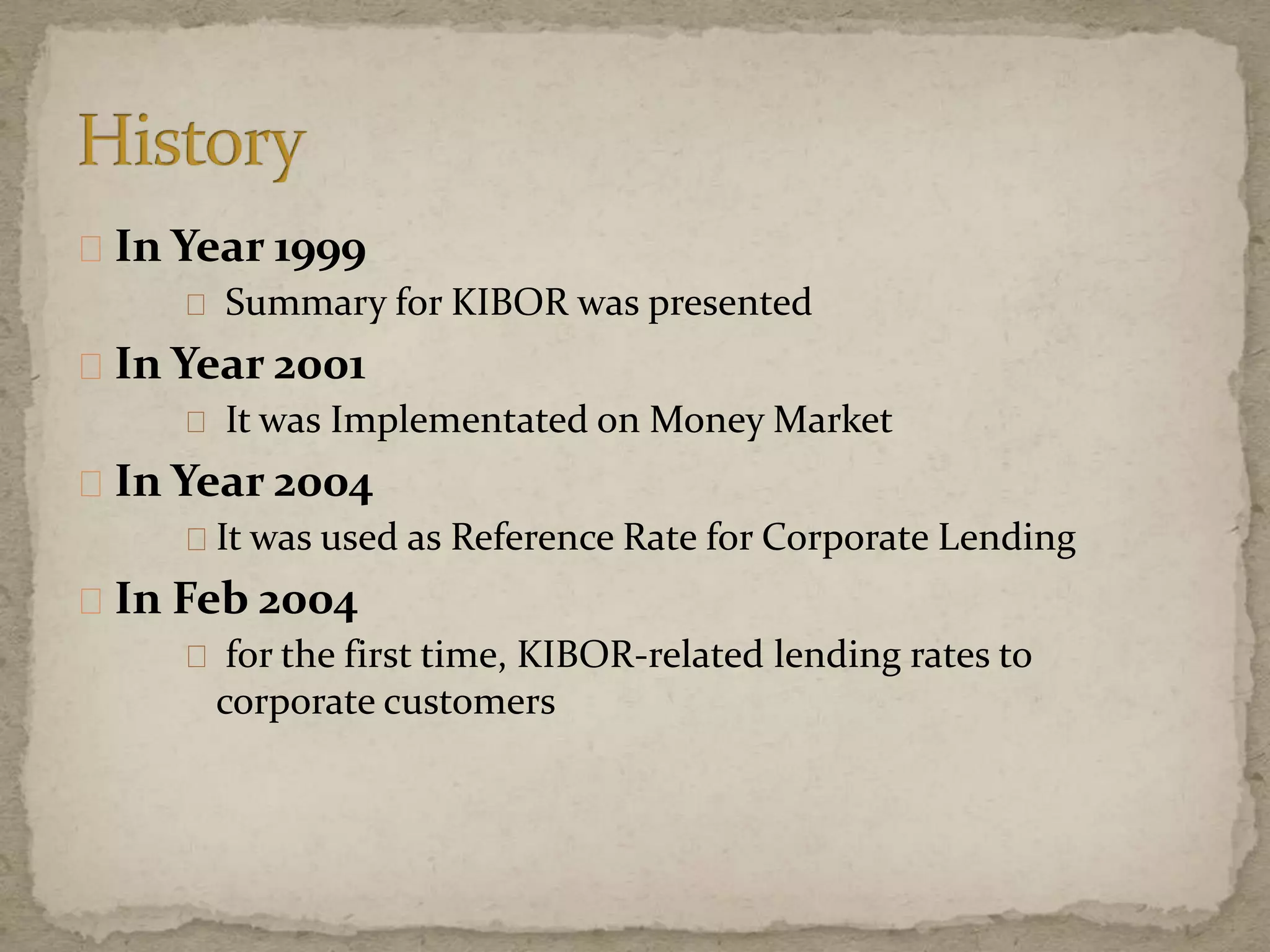

KIBOR summary presented (1999), implemented in the money market (2001), and expanded for corporate lending reference (2004).

Launched in 2001, KIBOR became a standard reference for corporate lending after consultations with SBP and PBA.

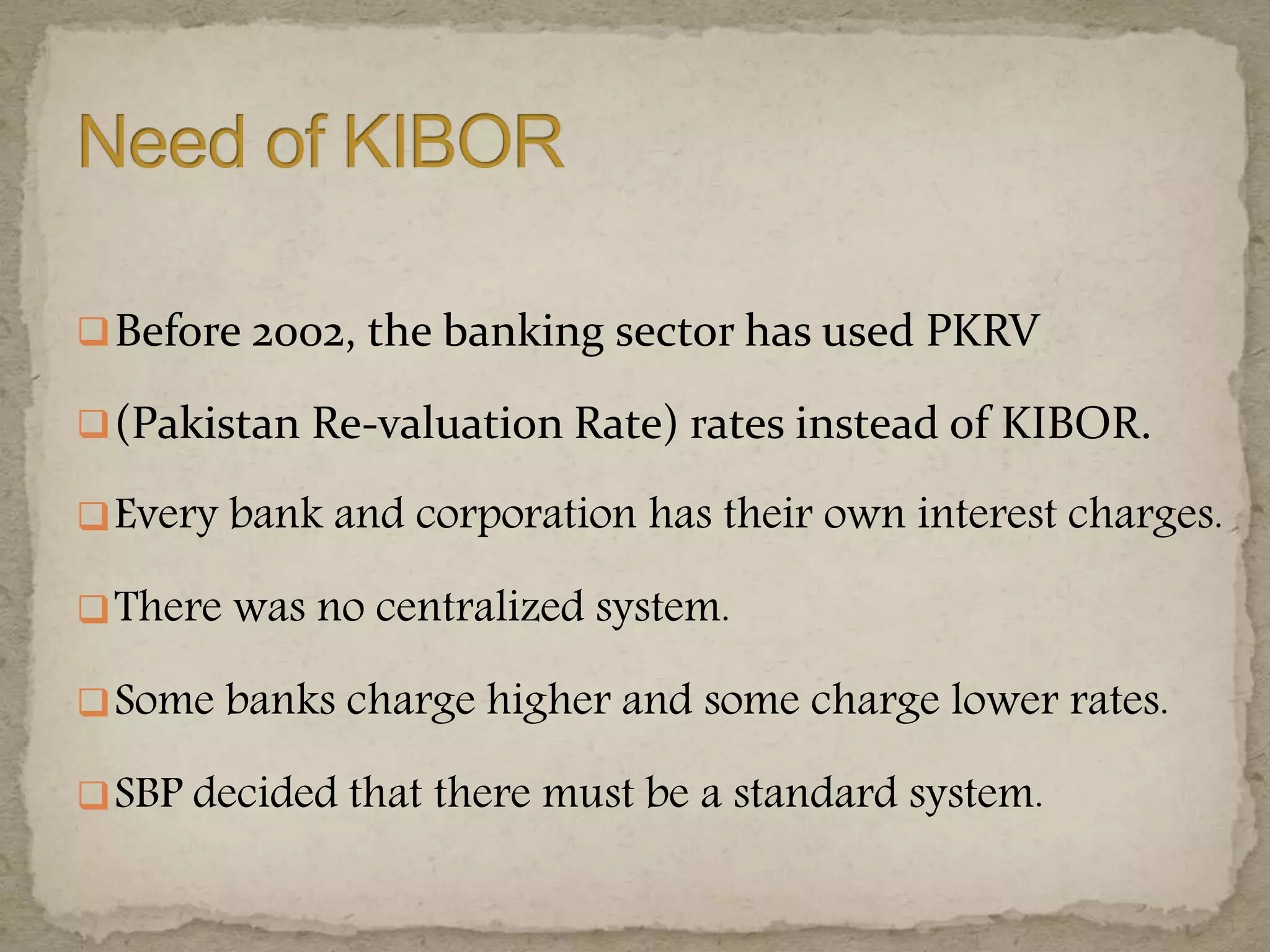

Prior to 2002, banks used PKRV rates with no central system, leading to variable interest rates.

Short (1-week to 6-month) and long tenures (1 to 3 years) offered under KIBOR.

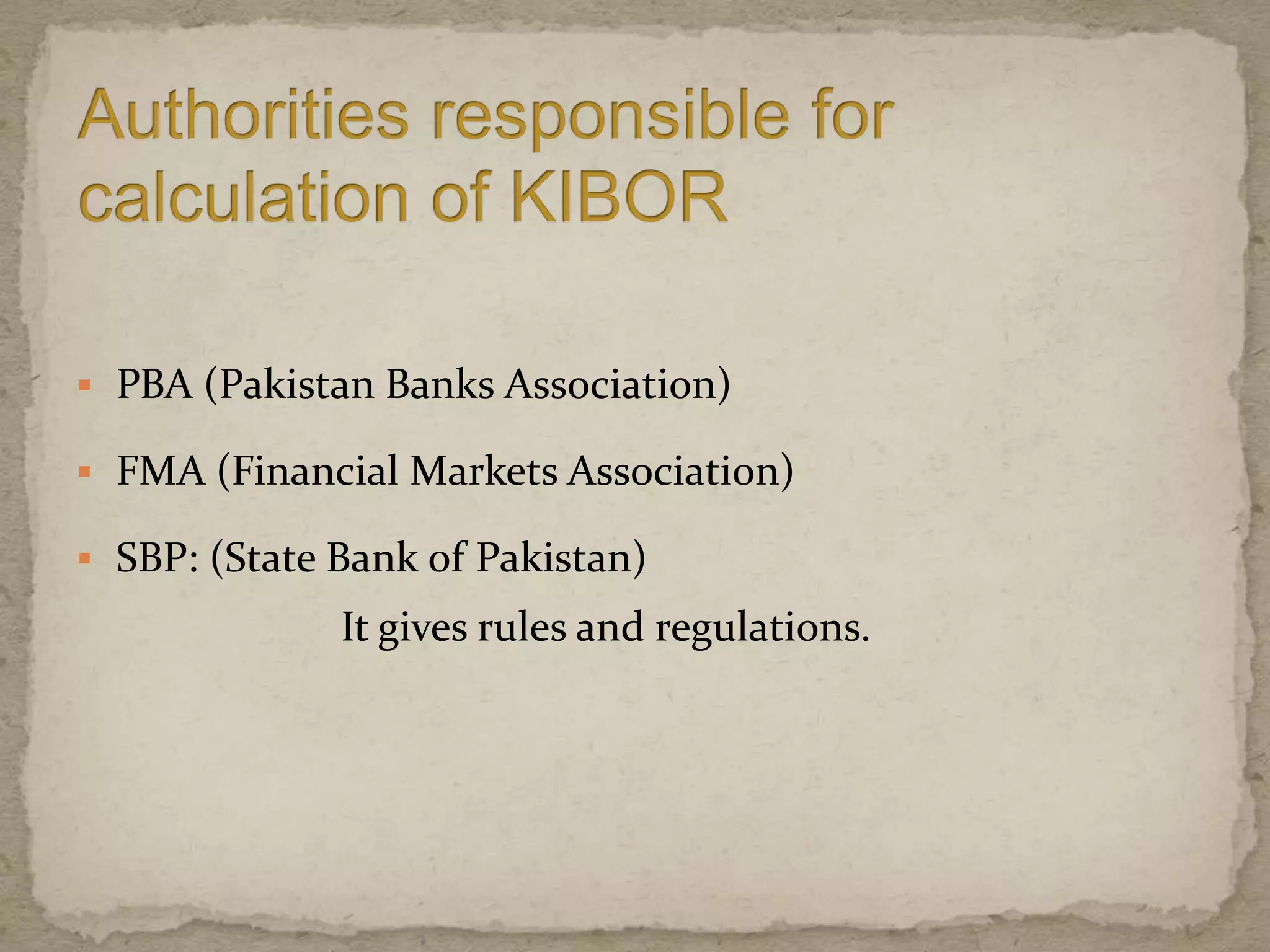

Key bodies involved: Pakistan Banks Association (PBA), Financial Markets Association (FMA), State Bank of Pakistan (SBP).

KIBOR is calculated without a specific formula; SBP collects rates from 20 banks each morning for market reflection.

SBP eliminates extremes in rates to find the daily KIBOR, confirmed by contributing banks.

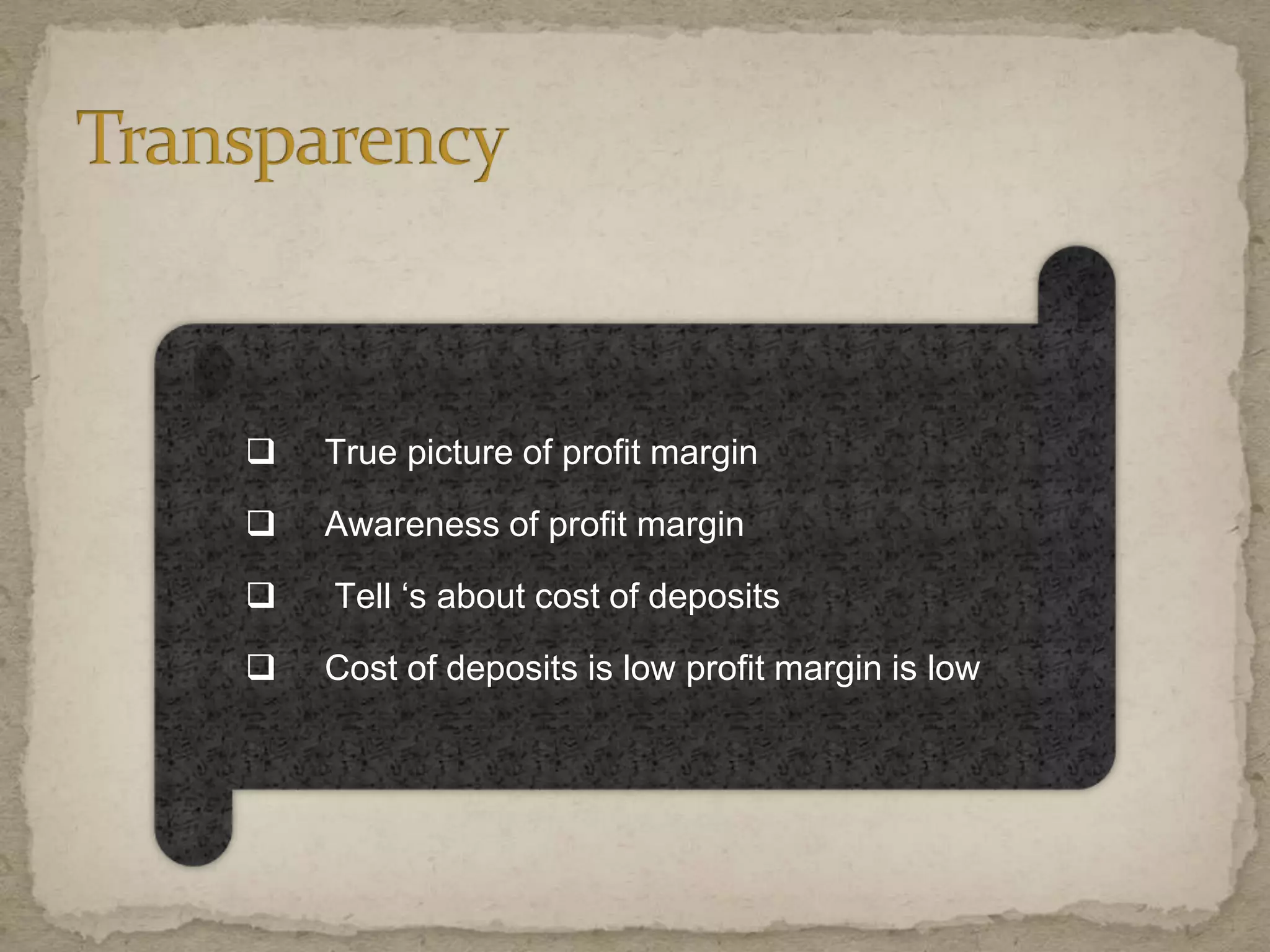

Benchmarking promotes transparency and consistency in market pricing while managing banks' risk.

Understanding profit margins and costs associated with deposits help evaluate interest rates.

KIBOR protects against market risks and assures customers are not overcharged.

KIBOR facilitates unsecured loans, meaning banks require no collateral.

Banks profit by lending more than KIBOR and borrowing less than KIBOR.

Top 5 banks contributing 75% of the sector: HBL, MCB, NBP, UBL, ABL.

KIBOR is updated daily at 11:30 AM on SBP and FMA websites, and via Reuters.

KIBOR rates are first reported by Reuters, playing a significant role in financial reporting since 2001.

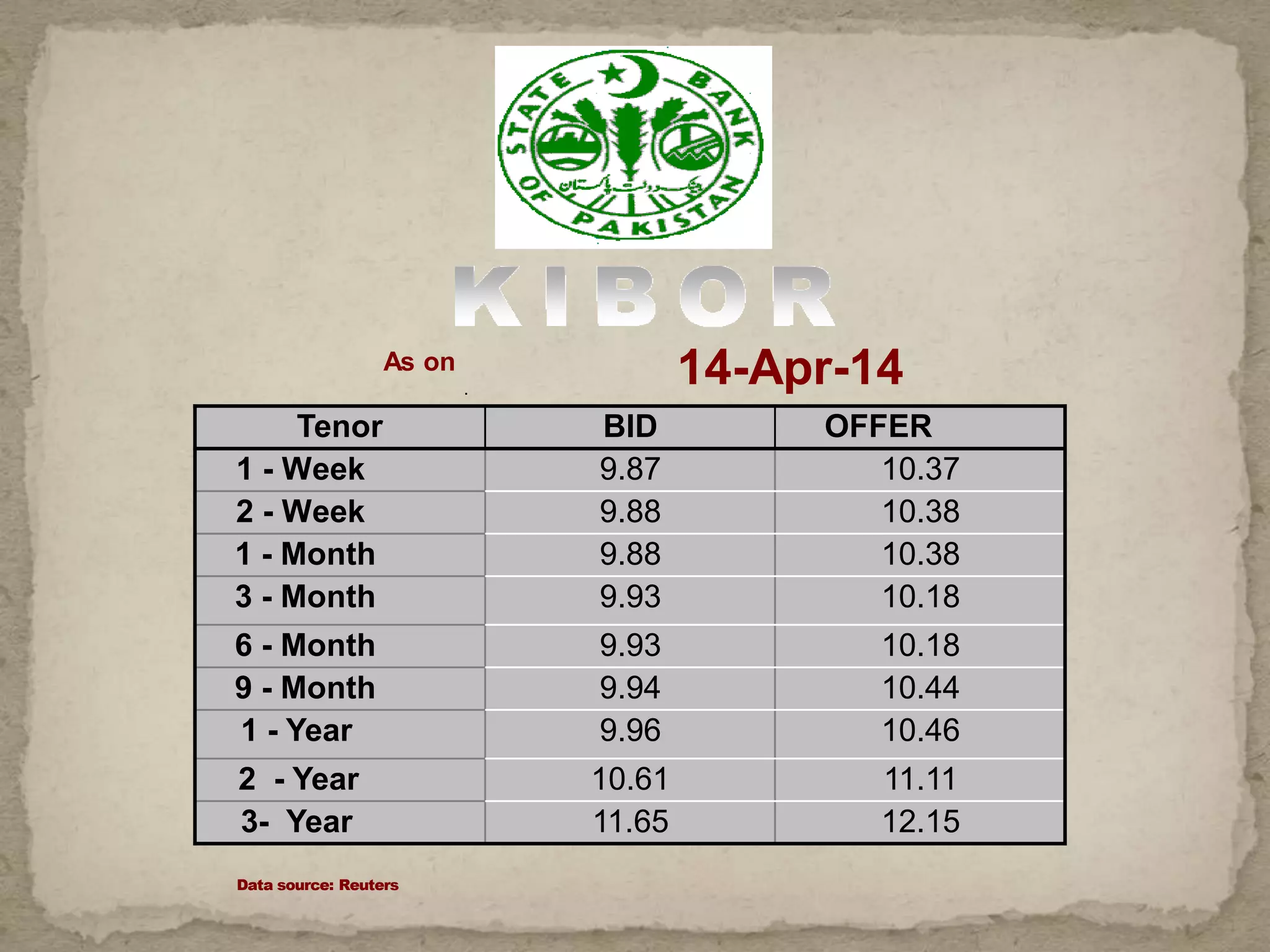

As of 14-Apr-14, various KIBOR rates showcased for different tenors, showing market dynamics.

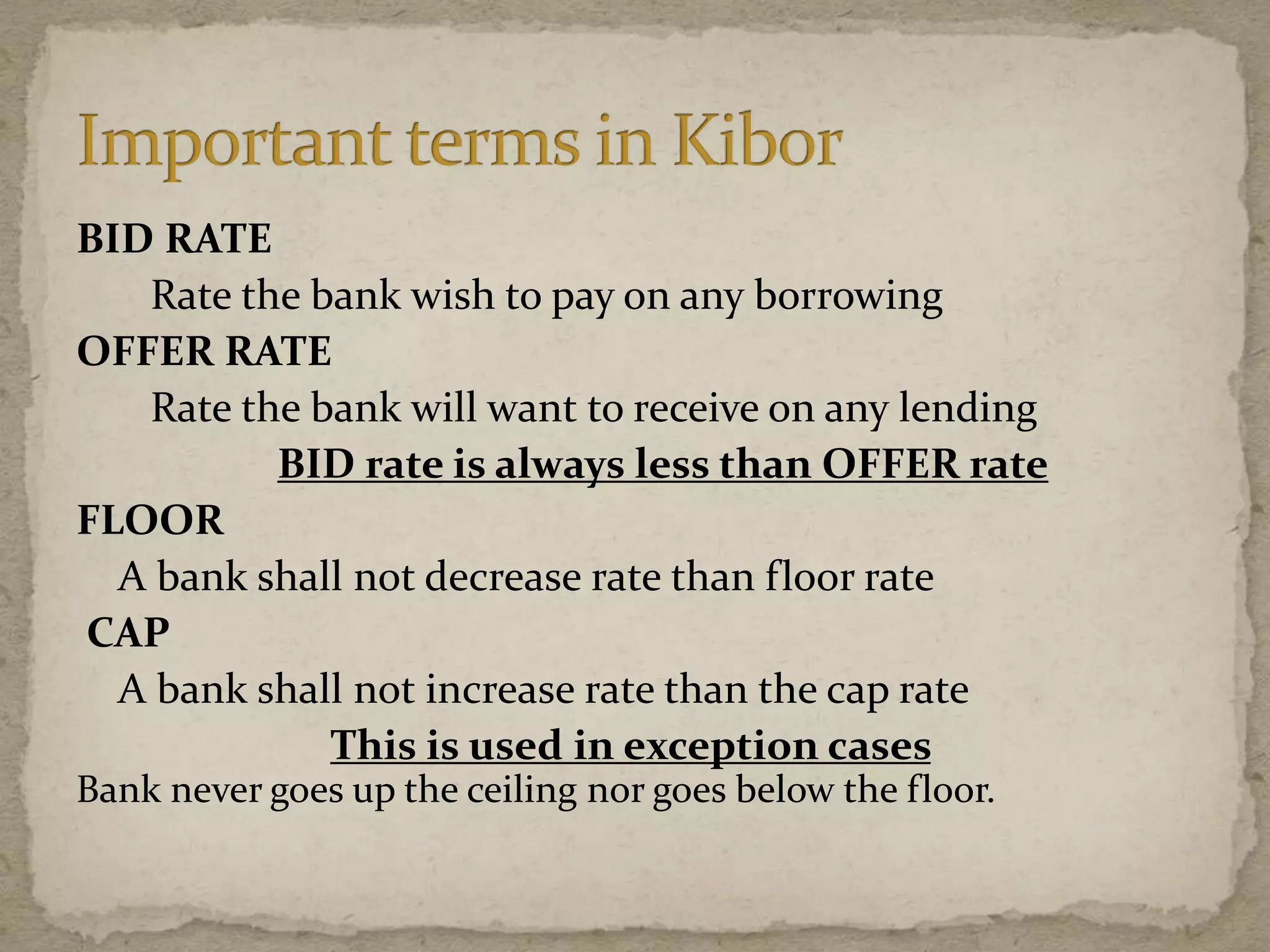

Definition of bid and offer rates, including bank restrictions on floor and cap rates.

Key factors: tenor, liquidity level, and credit quality influence the defined margin.

Bank costs include deposits, administrative expenses, and the need to adjust to market demands.

Parties can adjust tenor if current KIBOR rates are not acceptable for their loan agreements.

Factors affecting KIBOR include direct relationships with interest rates and inflation.

KIBOR applies to various financial instruments including term loans and financed certificates.

KIBOR applies to export finance, consumer financing, and existing overdraft facilities pre-2004.

KIBOR aids banks in developing improved customer financial products.

PBA represents the banking industry in Pakistan, focusing on collaboration and progress.

KIBOR serves as a reference rate for corporate lending, enhancing market-driven interest rates.

FMAP coordinates among financial dealers and is recognized as a self-regulatory organization.

FMAP ensures timely updates of KIBOR rates and coordinates among banks.

FMAP establishes basis points adjustments for different tenors of KIBOR.

KONIA rate for overnight lending is updated daily, specifying timing for updates.

Comparison between KIBOR and IBOR, with KIBOR being a benchmark in Islamic finance.

KIBOR serves as a benchmark in Islamic banking, maintaining market standardization.