1) The document summarizes the causes of the recent financial crisis, tracing problems back to the 1980s and failures to address underlying issues over the long term.

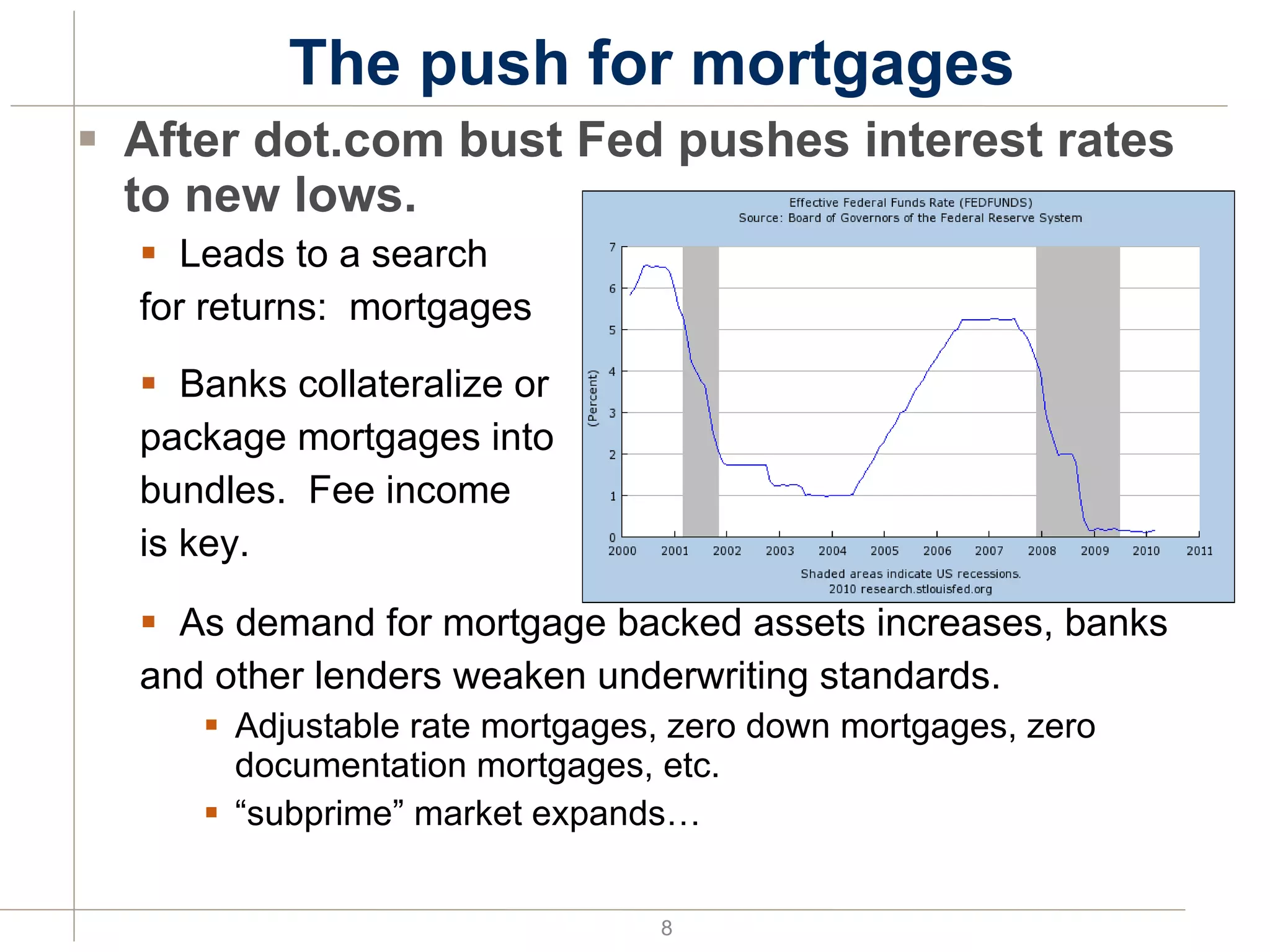

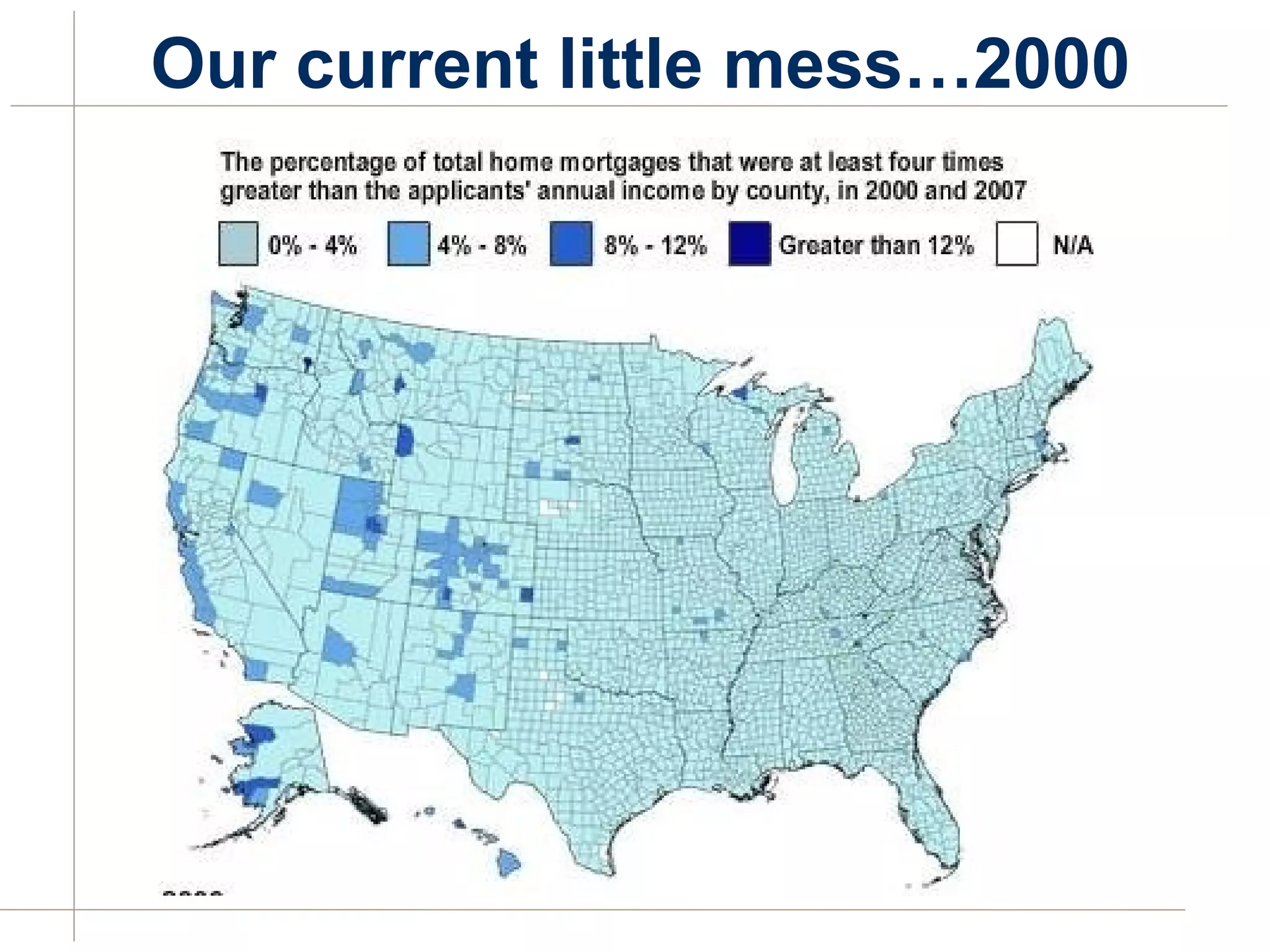

2) Key factors included the over-expansion of the mortgage market due to lowered standards and a focus on short-term profits rather than long-term stability.

3) Regulators could not prevent problems resulting from a lack of ethical behavior in financial markets and misaligned incentives.

![Q & A ask about anything… [email_address] http://blogs.mccombs.utexas.edu/brandl Twitter: MichaelBrandl Facebook: Michael.Brandl](https://image.slidesharecdn.com/jwu-speech-april-2010v2-1272068514-phpapp02/75/JWU-April-2010-speech-21-2048.jpg)