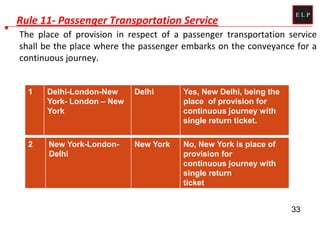

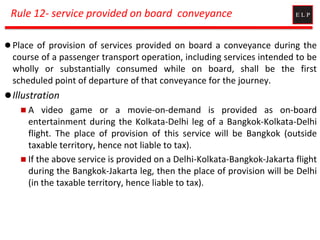

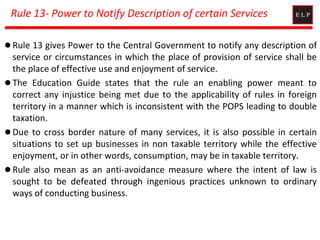

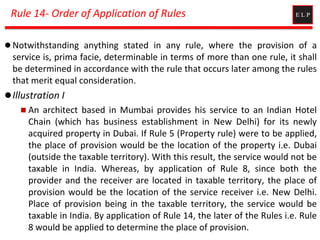

Download as PDF, PPTX

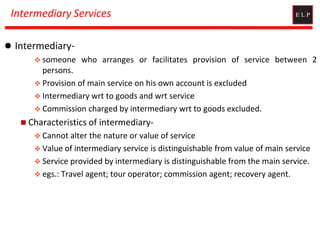

![Examples under Rule 9- Cont’d

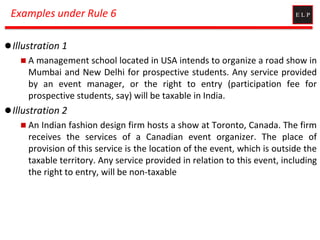

Examples of ‘intermediary services’:-

i) Travel Agent (any mode of travel)

ii) Tour Operator

iii) Commission agent for a service [an agent for buying or selling of goods is

excluded]

iv) Recovery Agent

Examples of Hiring of Means of Transport

i) Land vehicles such as motorcars, buses, trucks;

ii) Vessels;

iii) Aircraft;

iv) Vehicles designed specifically for the transport of sick or injured persons;

v) Mechanically or electronically propelled invalid carriages;

vi) Trailers, semi-trailers and railway wagons.](https://image.slidesharecdn.com/issuesinpopsfinal-180315092224/85/Issues-in-pops-final-25-320.jpg)

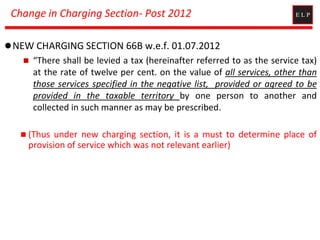

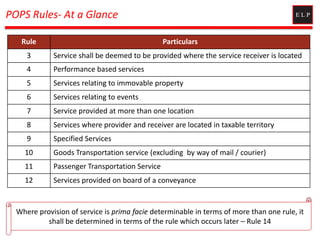

The document summarizes key changes to the rules for determining the place of provision of services under the service tax regime in India post 2012. Some key points: 1. A new charging section was introduced requiring determination of place of provision of service. 2. The Place of Provision of Services Rules, 2012 (POPS Rules) were introduced to determine whether a service was provided in the "taxable territory". 3. Under the main Rule 3, the location of the service receiver determines the place of provision. Exceptions are provided in Rules 4-6 and 9-12.