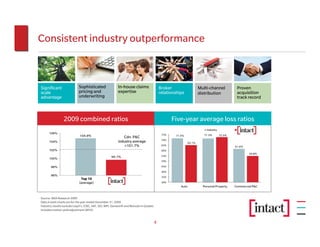

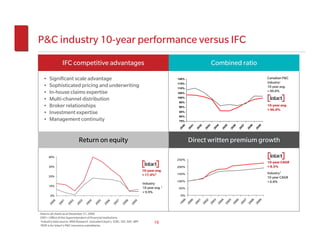

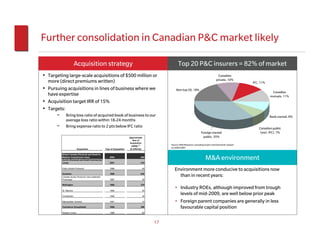

This document provides an investor presentation for Intact Financial Corporation (IFC) from September 2010. IFC is Canada's largest provider of property and casualty insurance, with over $4 billion in annual premiums written. The presentation outlines IFC's strong financial position, industry-leading underwriting performance, and growth strategies. Key points include IFC's consistent outperformance of the Canadian P&C industry benchmarks on measures like combined ratio and return on equity. The presentation also discusses IFC's excess capital position, debt capacity, and acquisition strategy to capitalize on consolidation opportunities in the market. Multiple avenues for organic growth are outlined, including leveraging IFC's multi-channel distribution network and expanding product offerings.