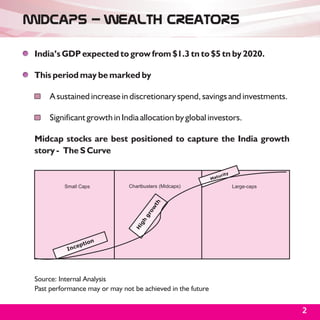

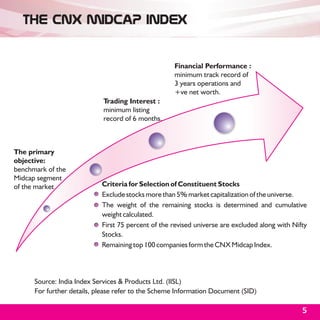

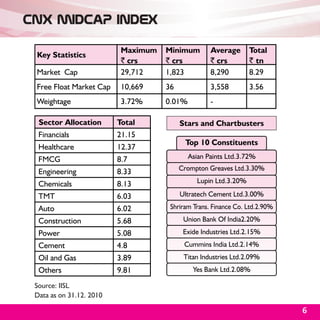

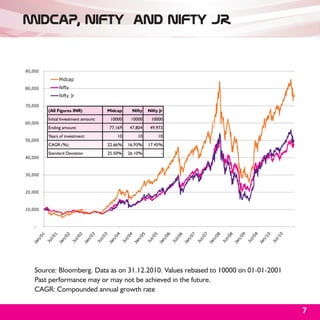

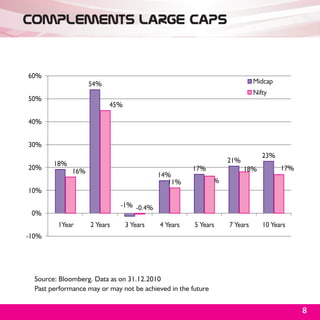

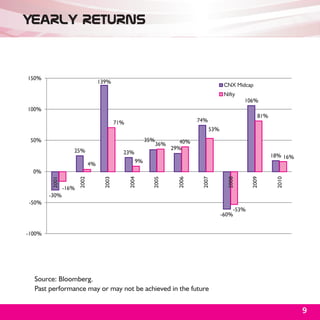

Motilal Oswal Mutual Fund presents m100 (An Open Ended Index Exchange Traded Fund) that tracks the CNX Midcap Index. The NFO opens on 12th January 2011 and closes on 24th January 2011. The document discusses that midcap stocks are well positioned to capture India's growth given India's GDP is expected to grow substantially by 2020. It provides statistics on the CNX Midcap Index such as sector allocation and top 10 constituents. Performance figures show midcap outperforming large caps over long periods while complementing large cap portfolios.

![[JMFL] Multi Commodity Exchange - Poised for comeback](https://cdn.slidesharecdn.com/ss_thumbnails/a18046ed-f590-444b-ad37-b829f529f4fc-160616063316-thumbnail.jpg?width=640&height=640&fit=bounds)