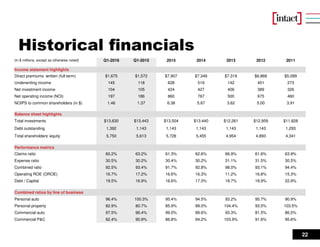

This investor presentation provides an overview of Intact Financial Corporation (IFC), Canada's largest property and casualty insurer. Some key points:

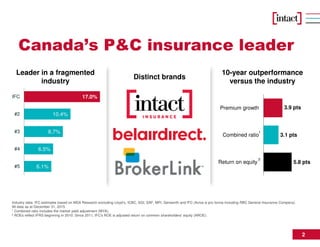

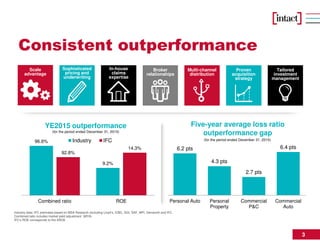

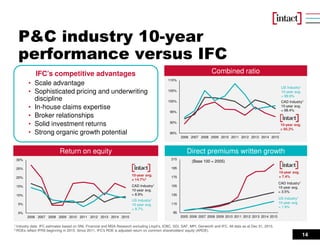

1) IFC has consistently outperformed the industry on measures like return on equity, combined ratio, and premium growth over the past 10 years.

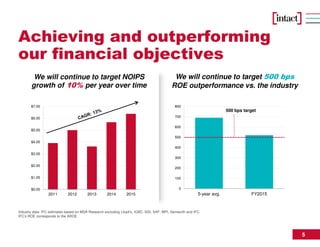

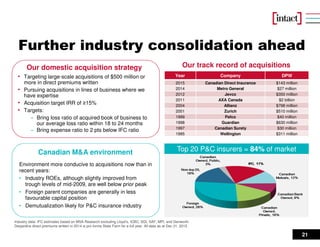

2) IFC aims to continue beating industry ROE by 500 bps annually and growing net operating income per share by 10% per year through initiatives like pricing segmentation, claims management, and acquisitions.

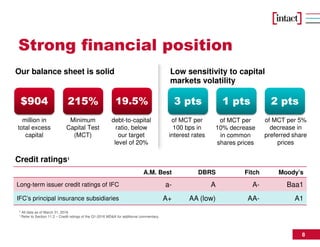

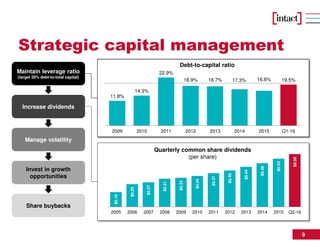

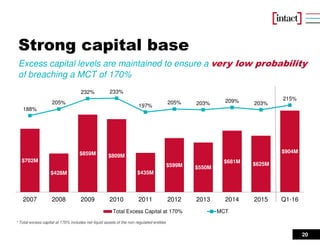

3) IFC has a strong capital position with $904 million in excess capital and a 215% Minimum Capital Test ratio as of Q1 2016. Management plans to continue increasing dividends and share buybacks