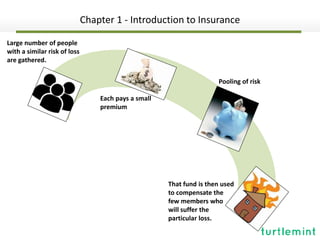

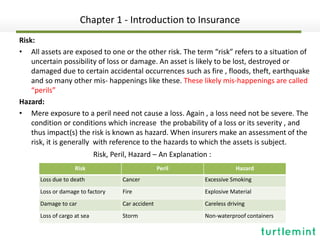

Insurance allows individuals and organizations to transfer risk by paying premiums to an insurance company, which then reimburses the insured for covered losses. It works by pooling risks from a large number of similar individuals and entities - the few who suffer losses are paid from premiums paid by the many. Key concepts include risk as an uncertain possibility of loss, perils as events that can cause losses, and hazards as conditions increasing the likelihood or severity of losses. Insurance spreads risks but does not guarantee that perils will not occur - it only provides compensation if insured events happen.