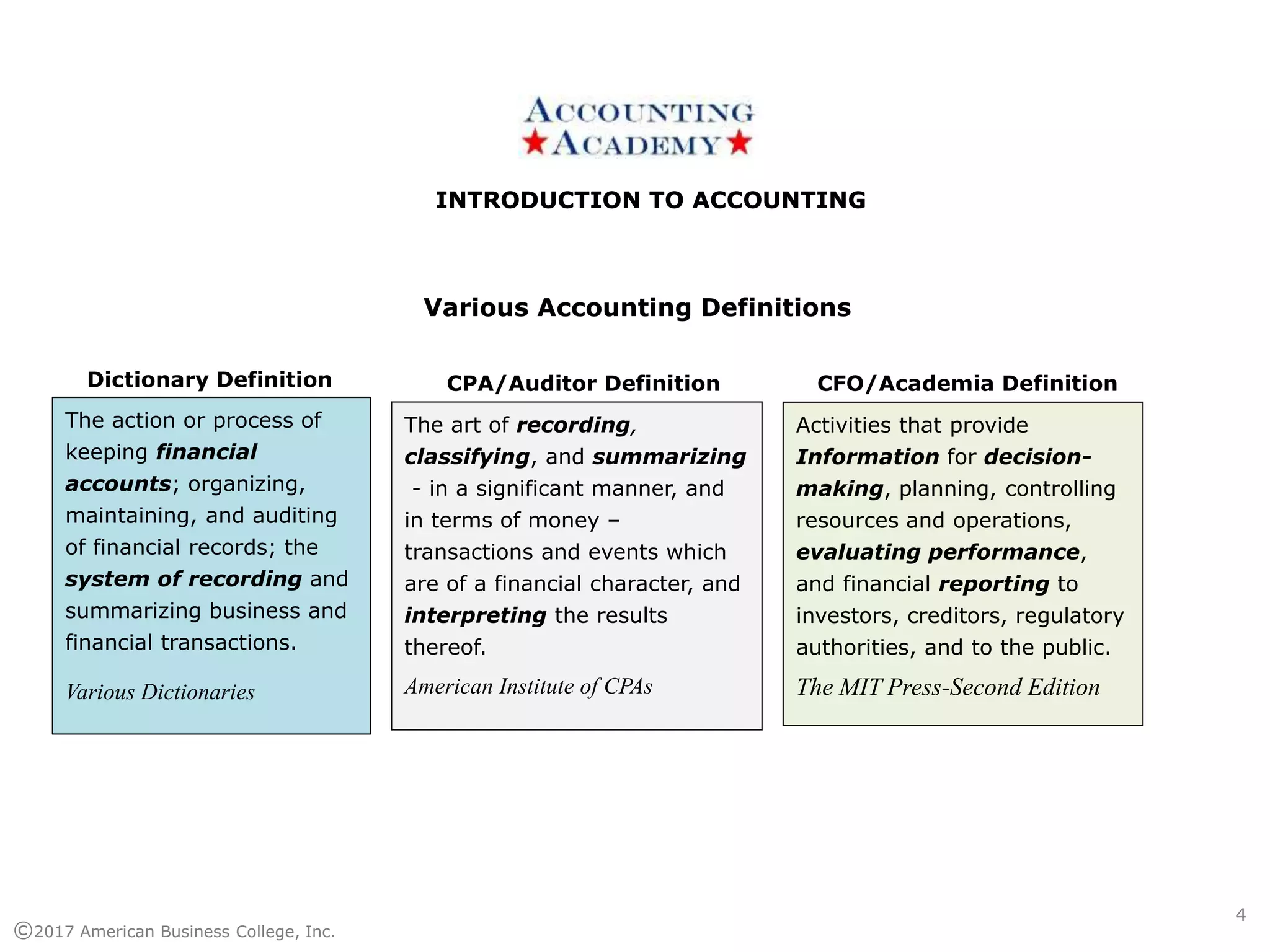

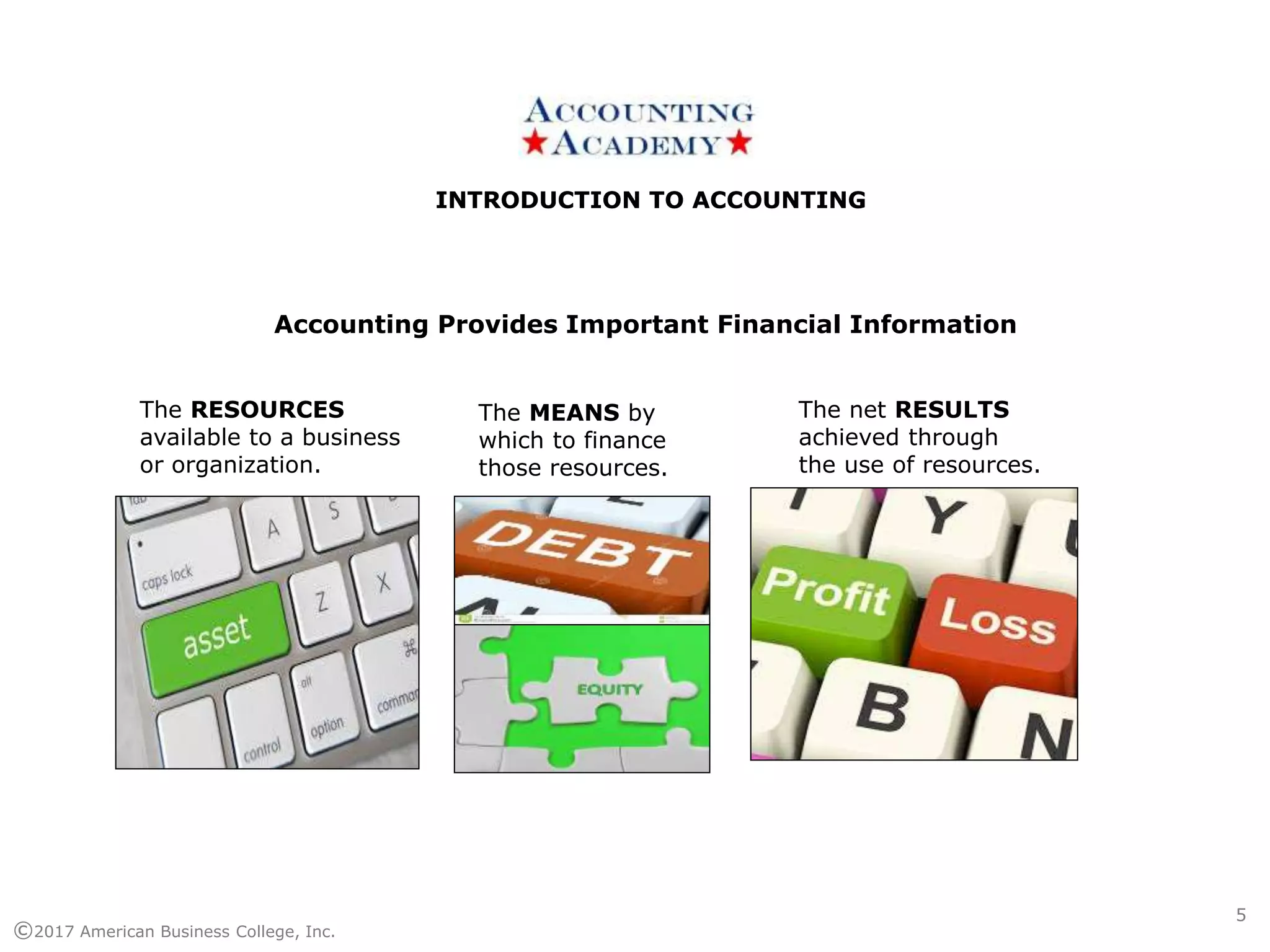

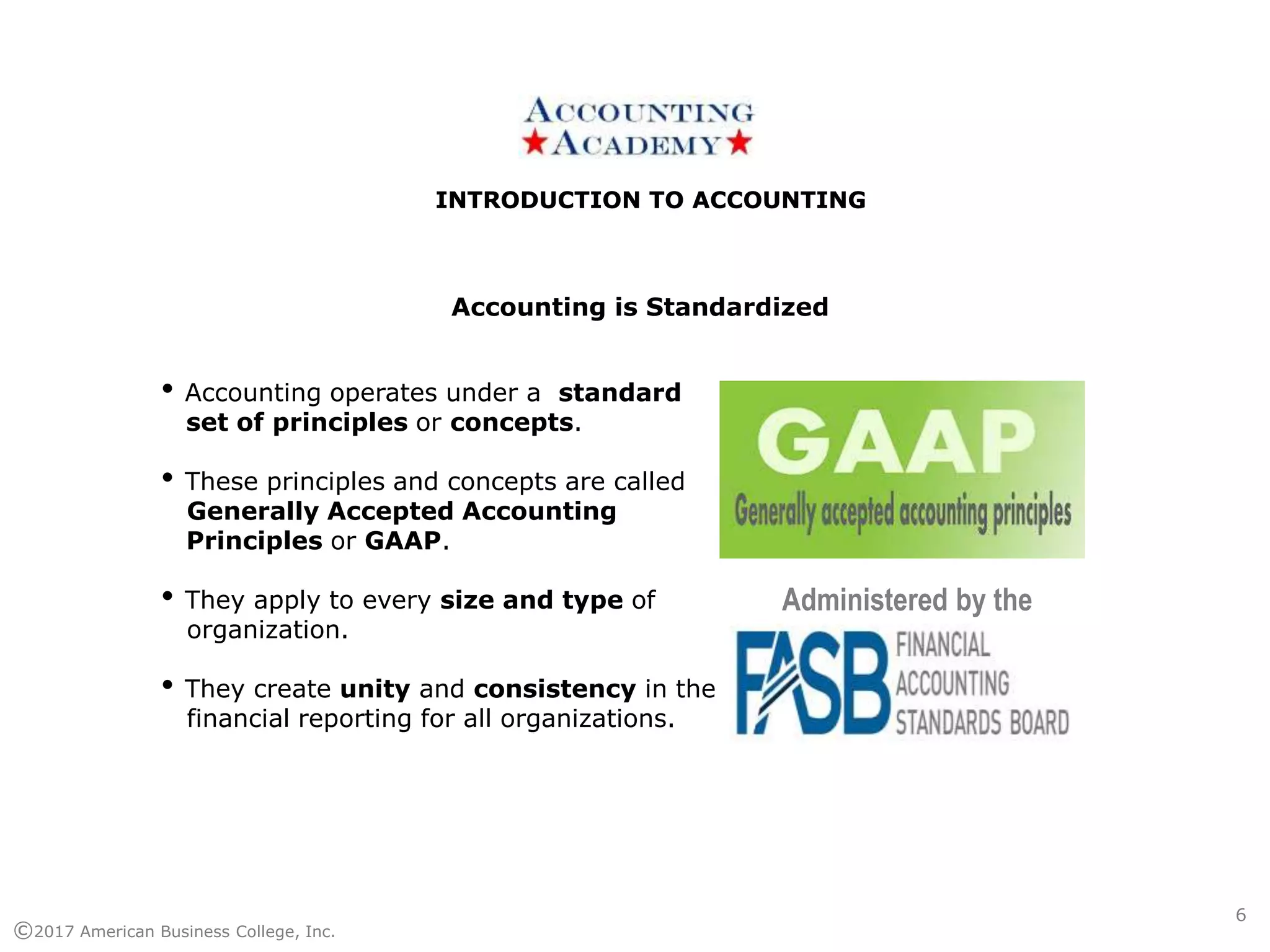

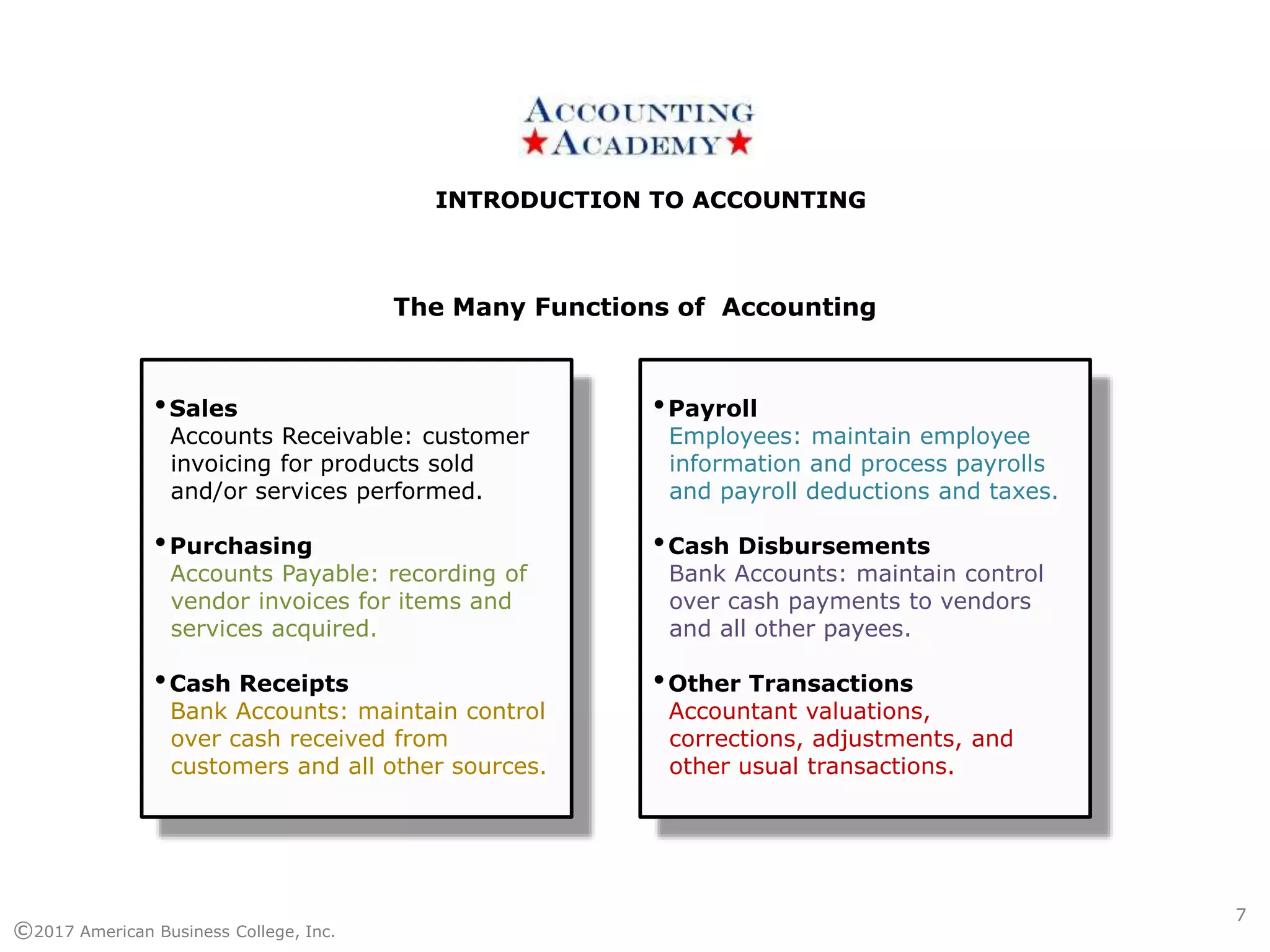

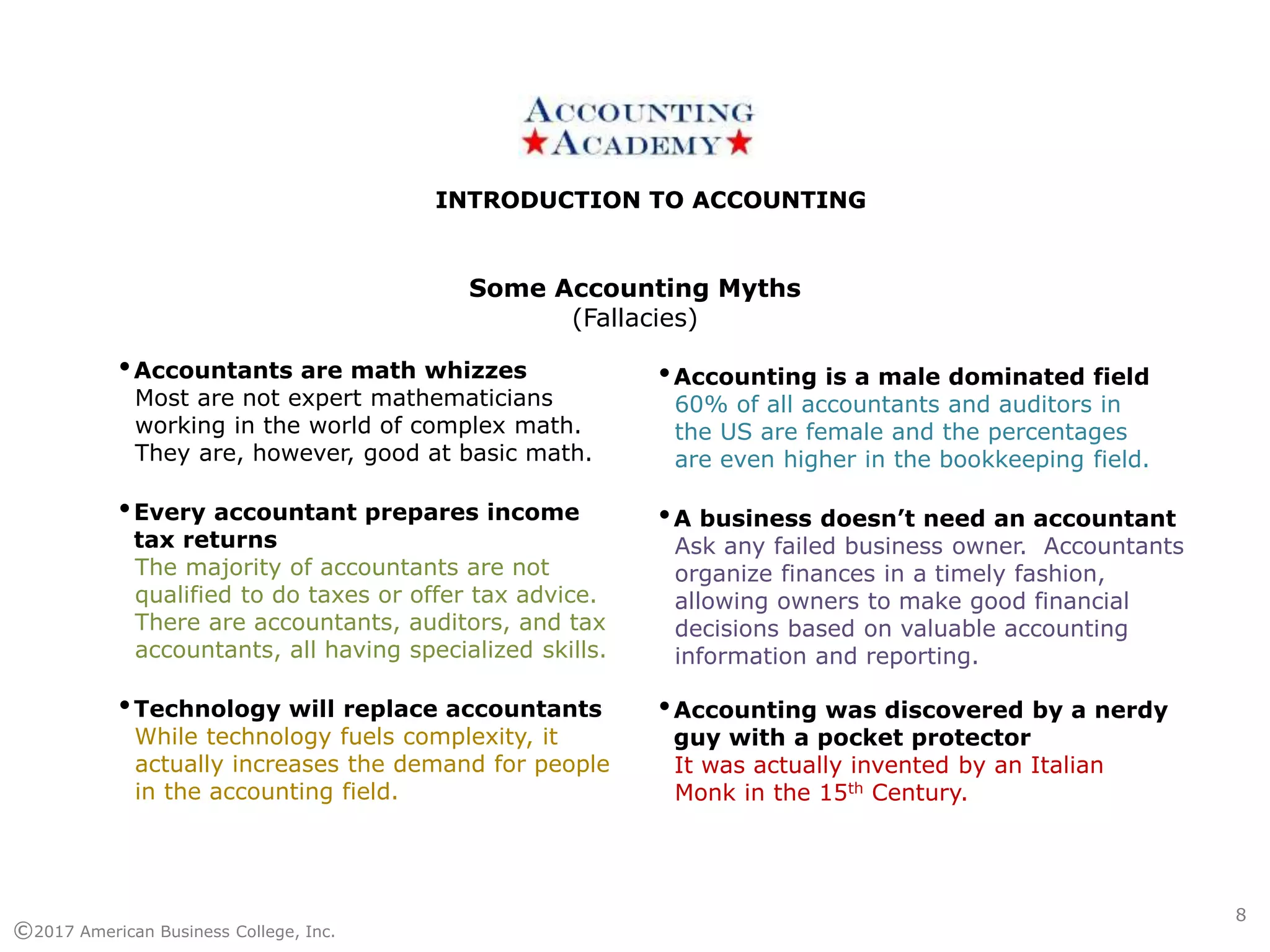

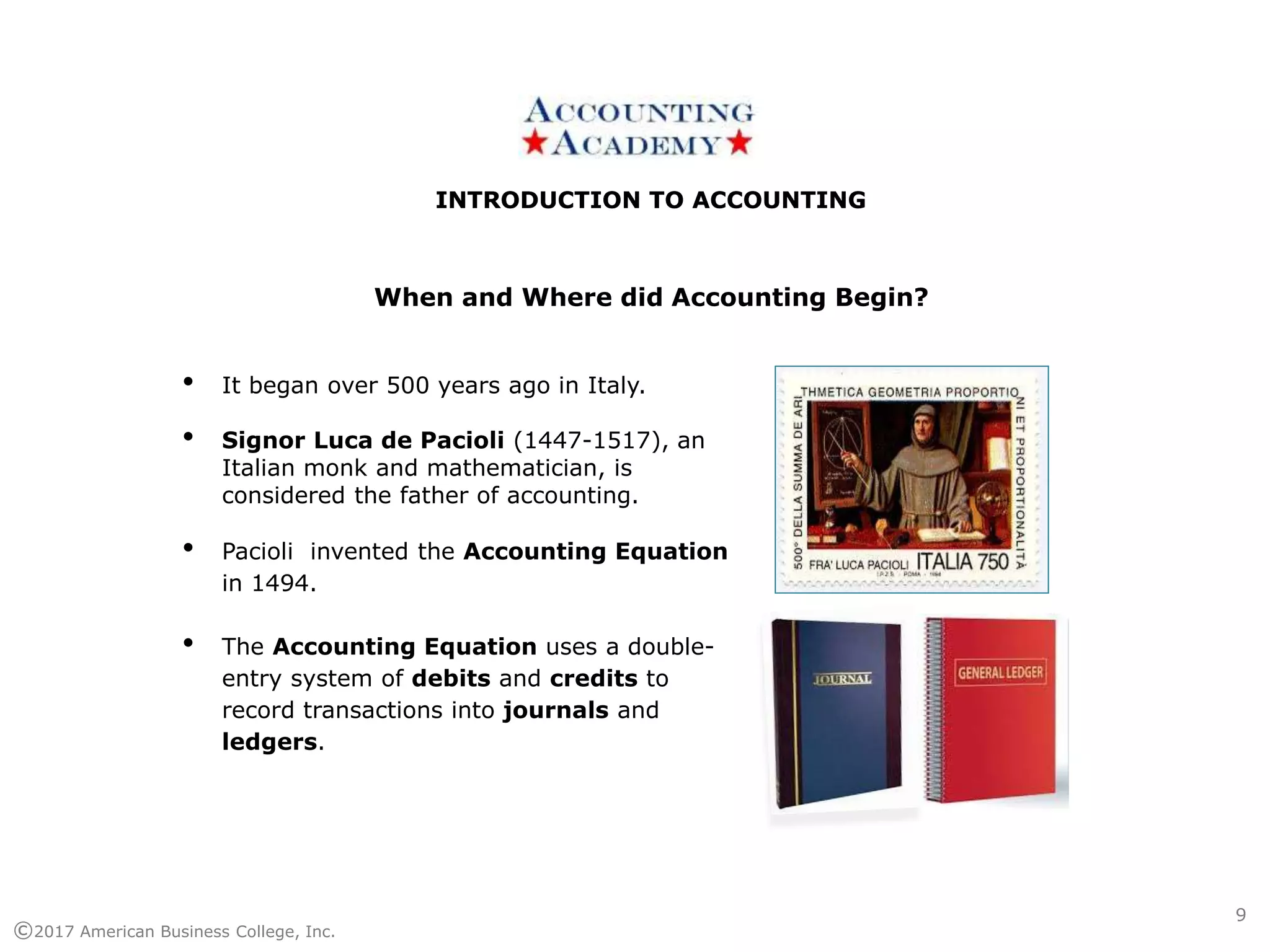

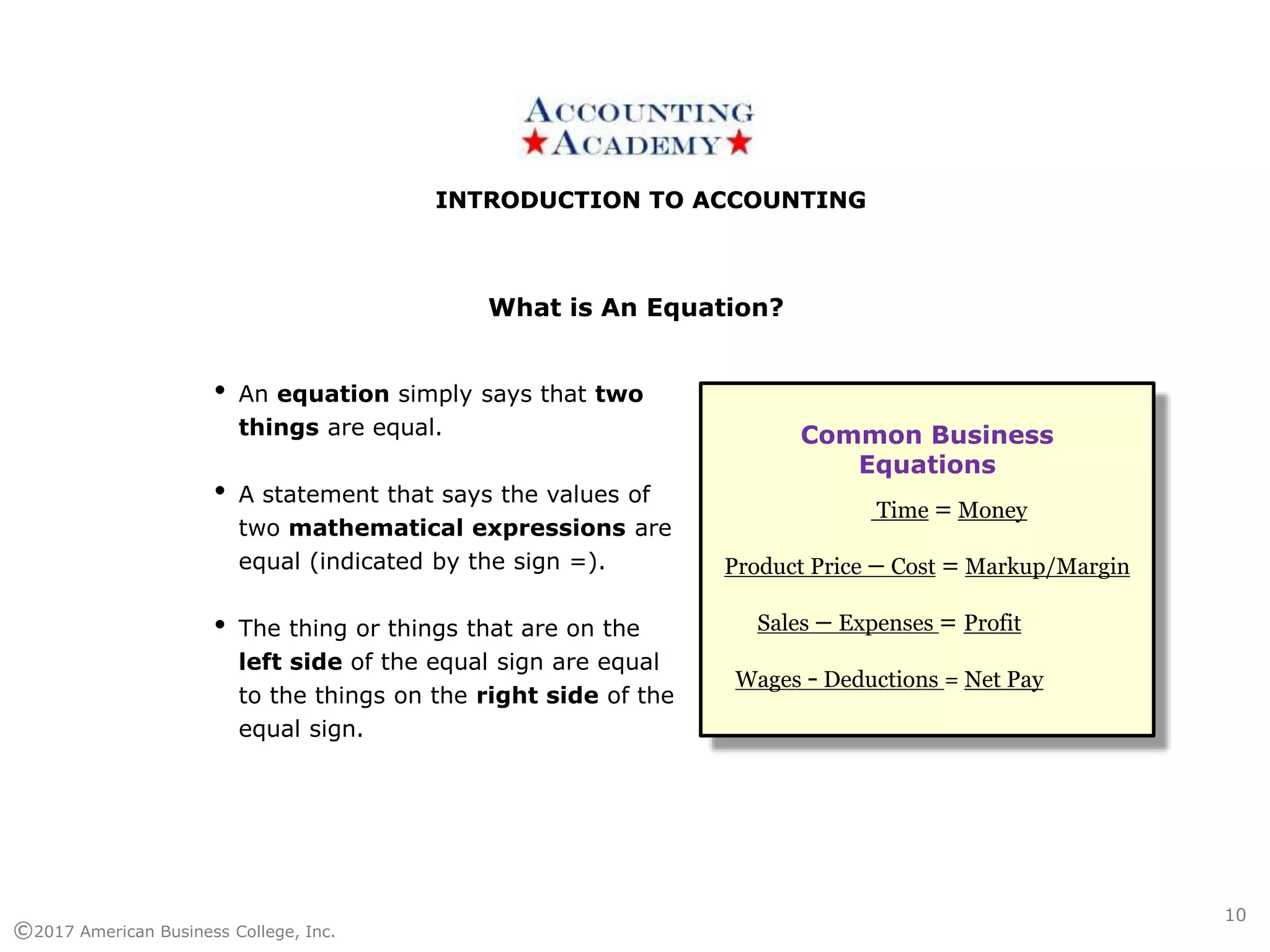

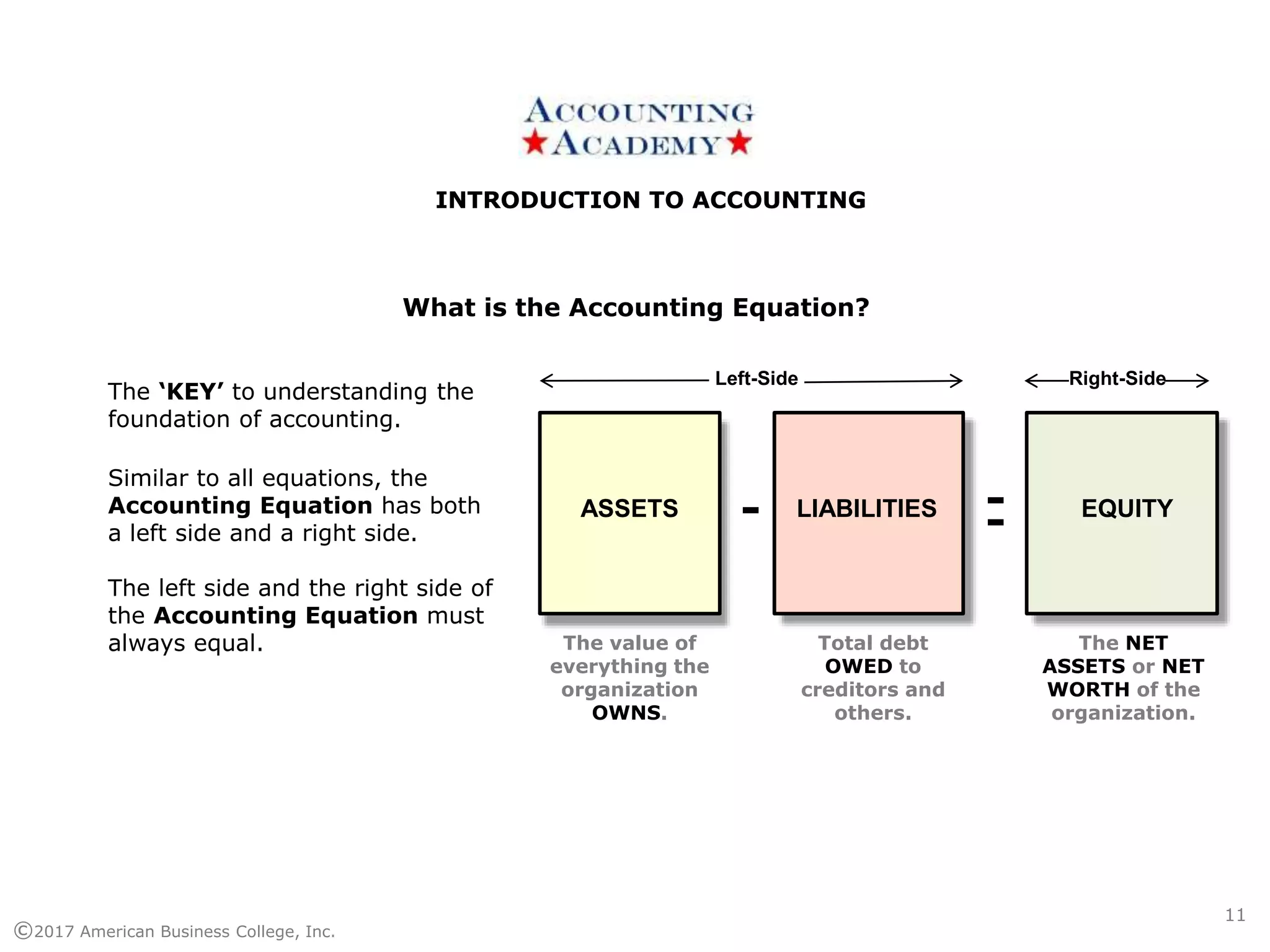

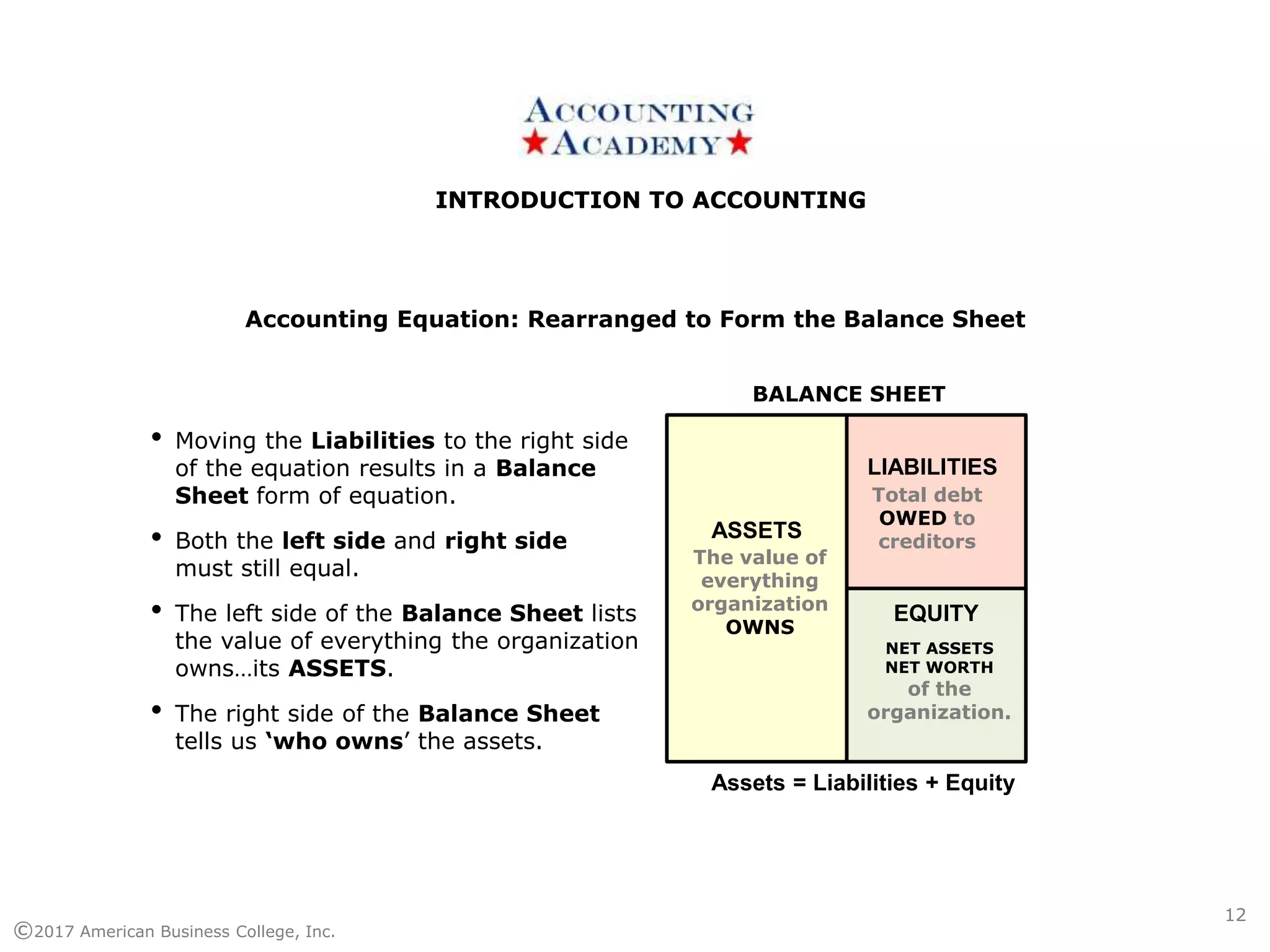

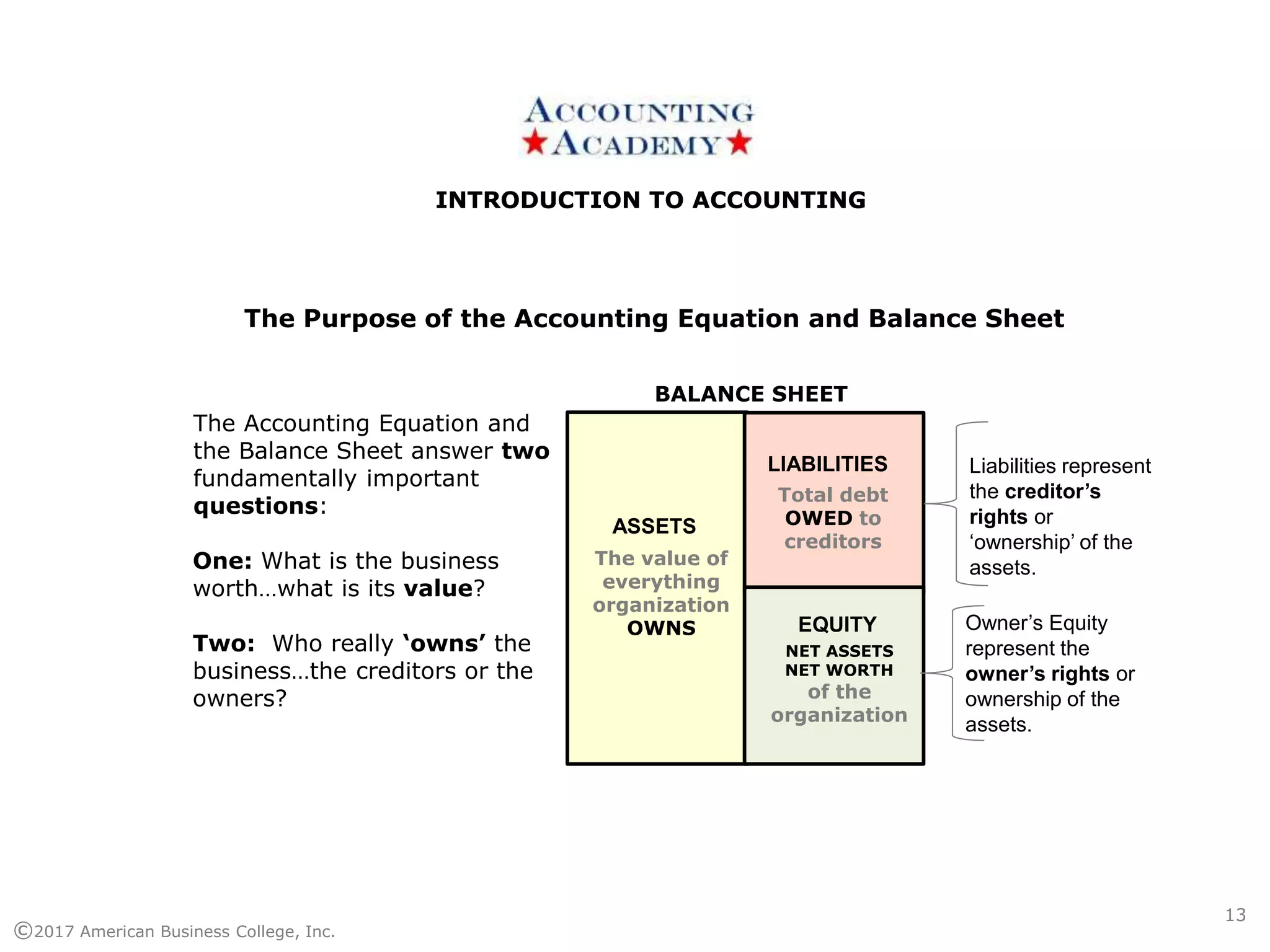

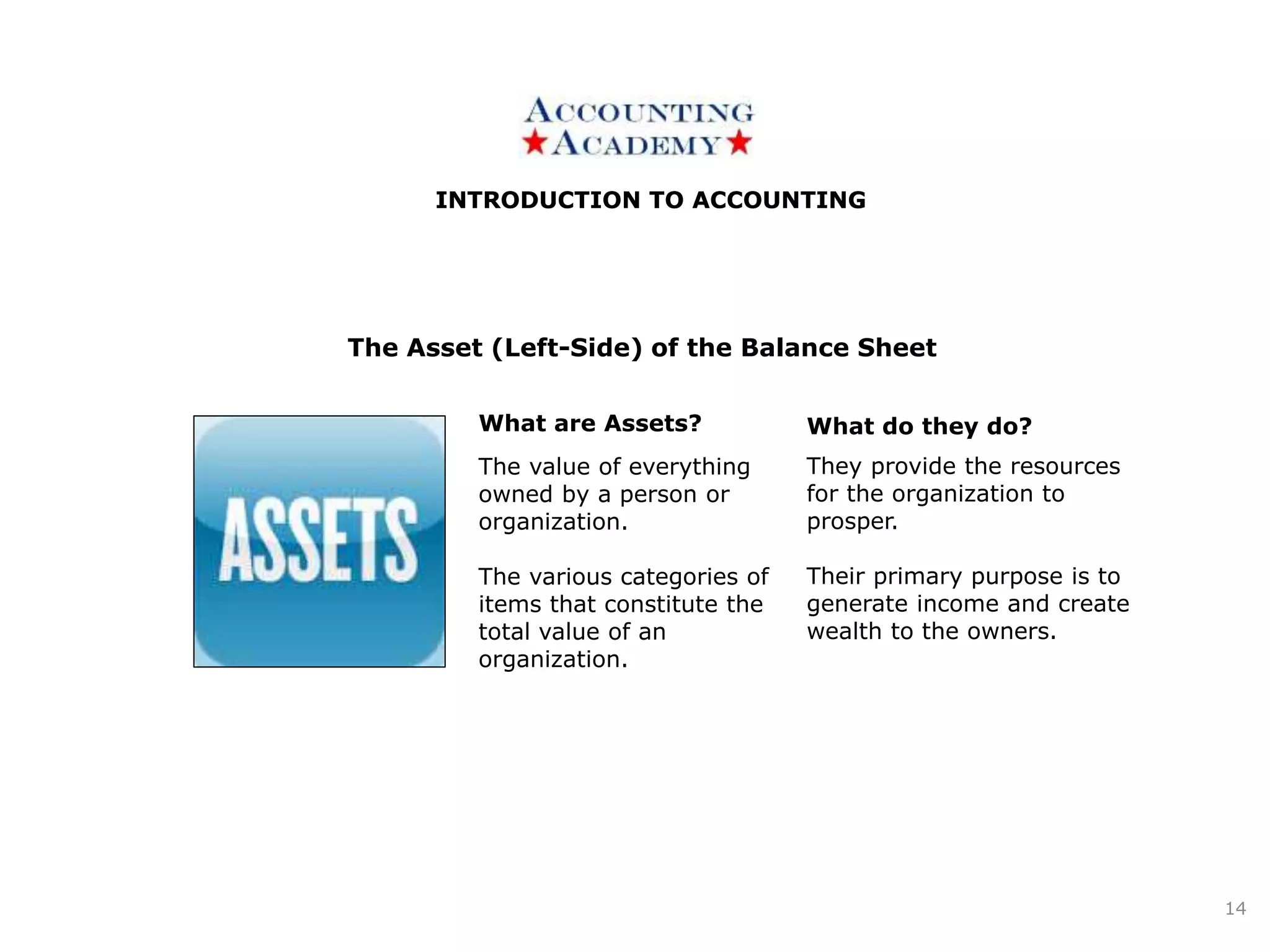

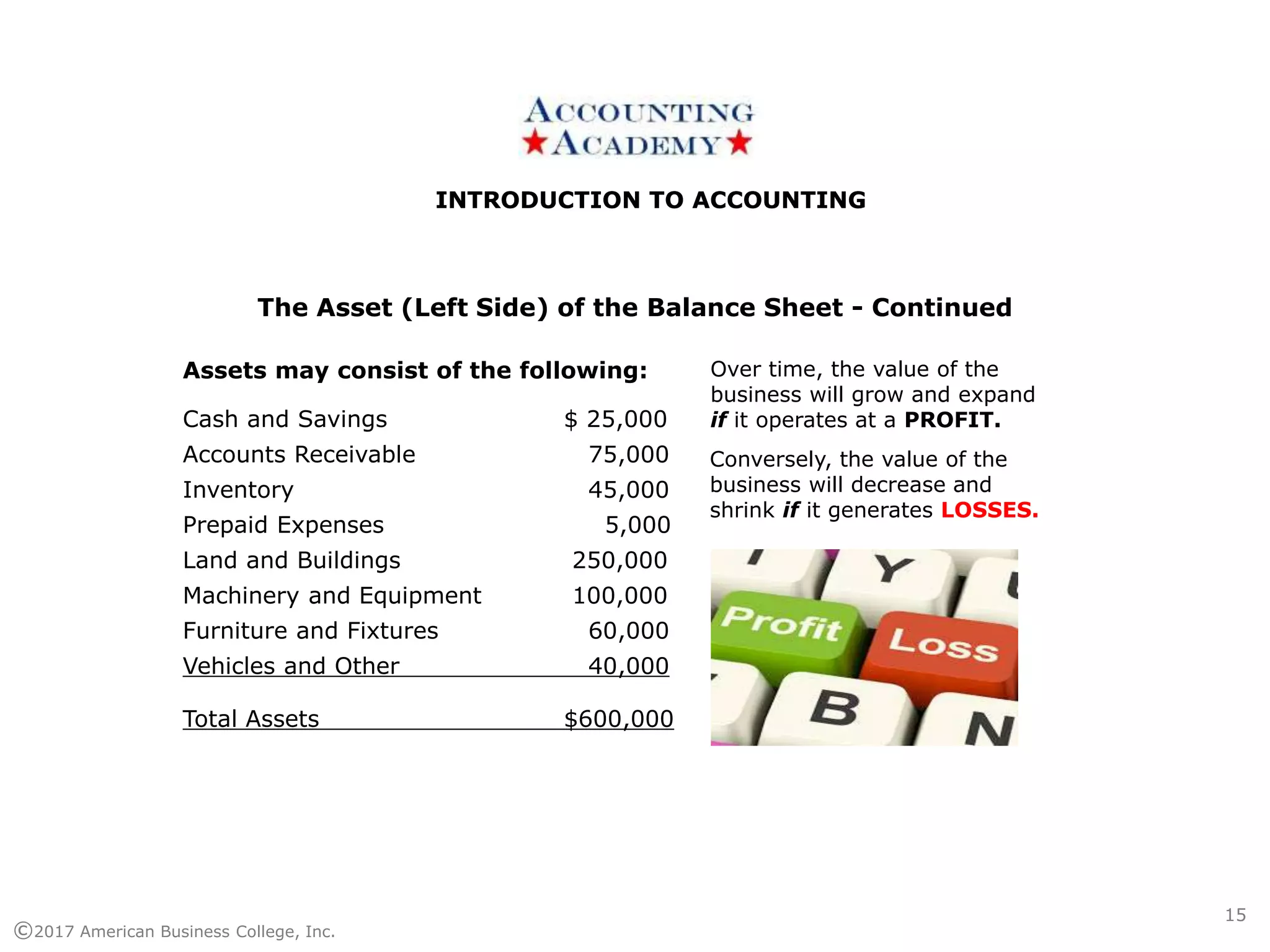

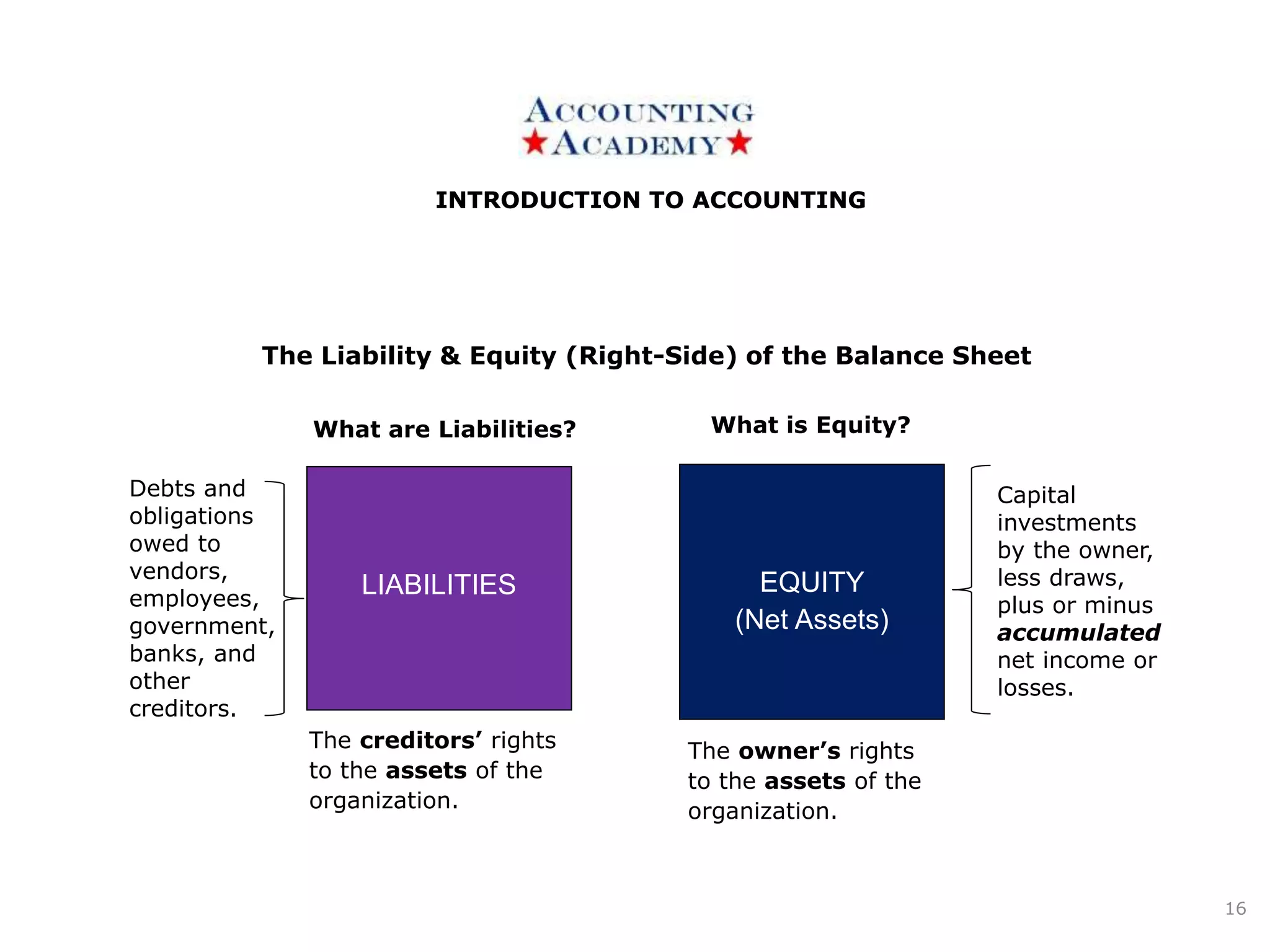

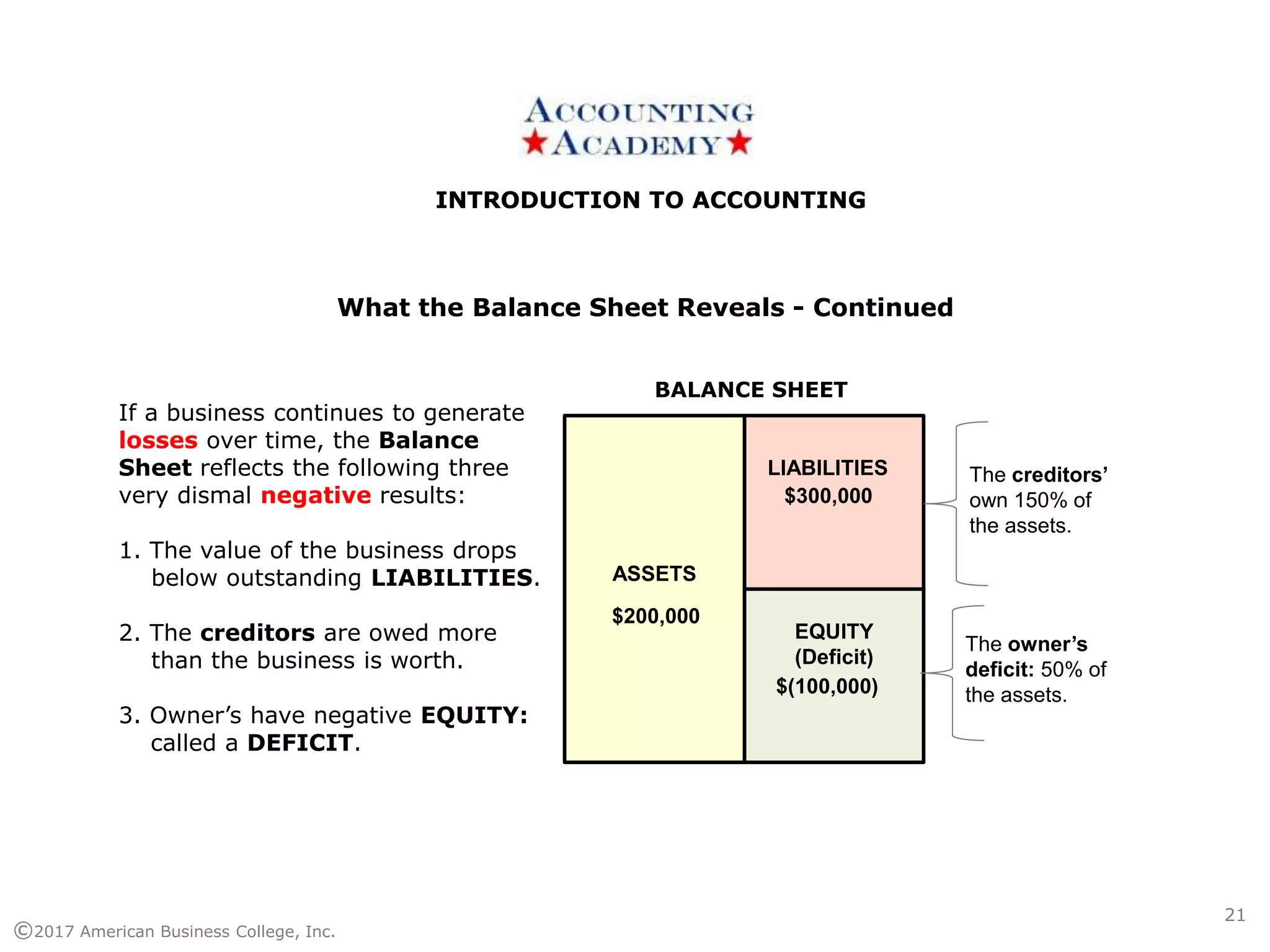

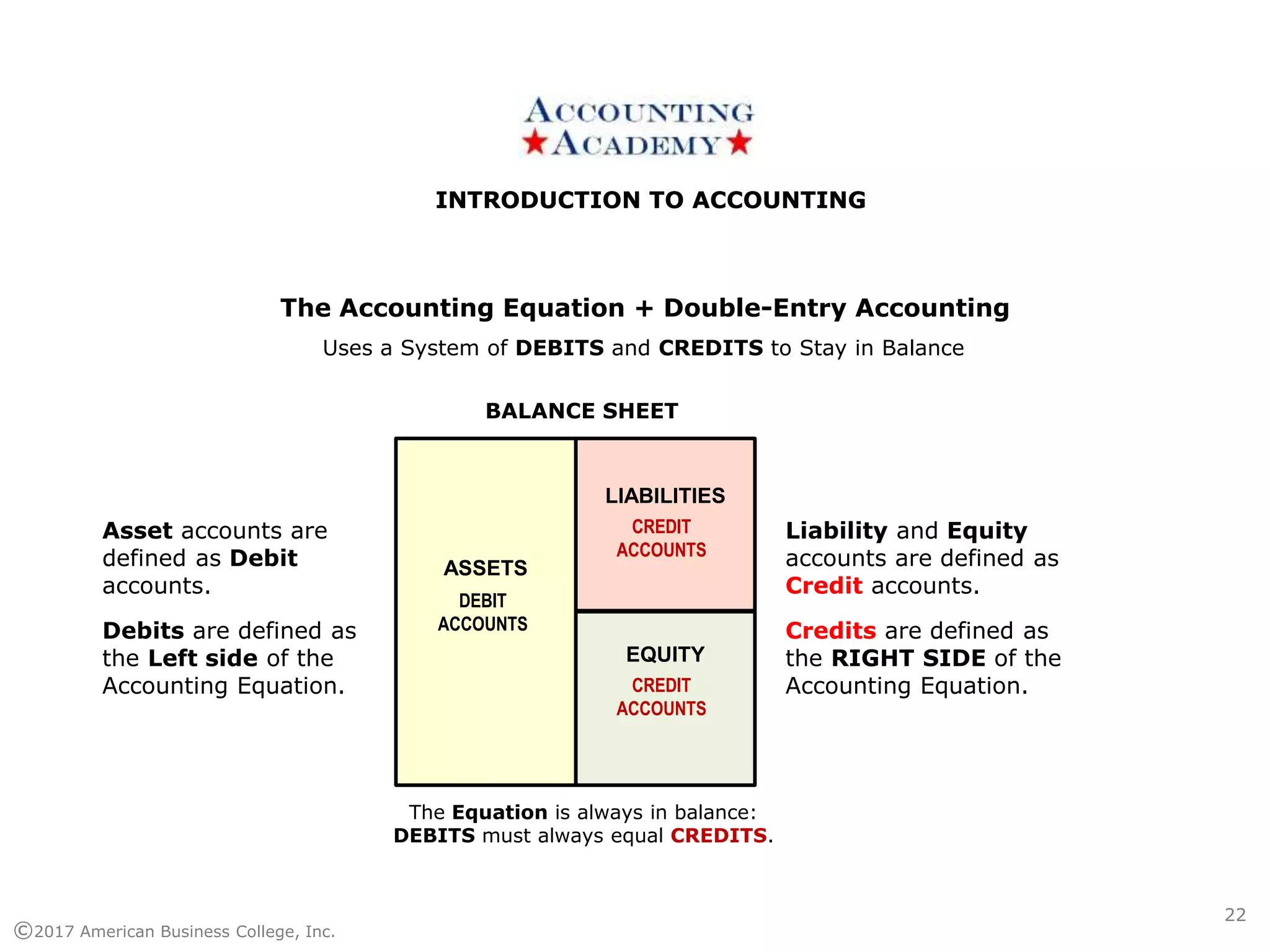

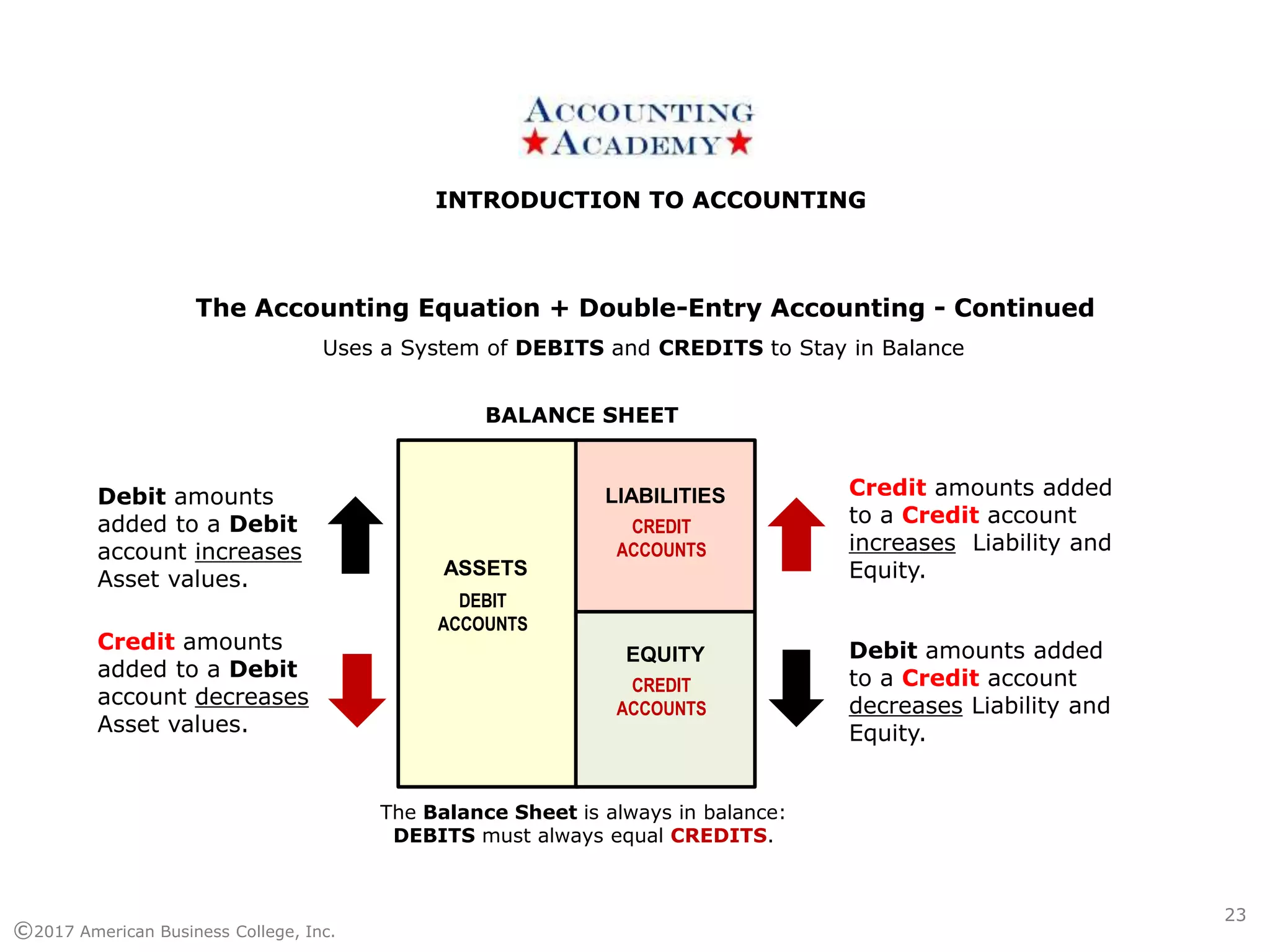

The document provides an introduction to accounting. It defines accounting as a systematic process of recording, measuring, and communicating financial information. It discusses the accounting equation and balance sheet, which show that assets must equal liabilities plus equity. Assets represent what is owned, and liabilities and equity represent who owns the assets. Debits and credits are used to keep the accounting equation and balance sheet in balance. The document also outlines accounting standards, functions, history, and some common myths.

![ACT 201 ch0accounting 201 intro to 1[1].ppt](https://cdn.slidesharecdn.com/ss_thumbnails/act201ch011-250706073840-7f4e295a-thumbnail.jpg?width=640&height=640&fit=bounds)