Download as PDF, PPTX

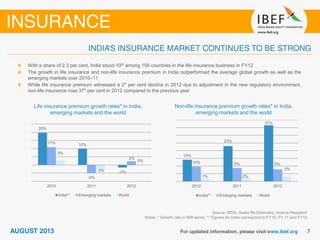

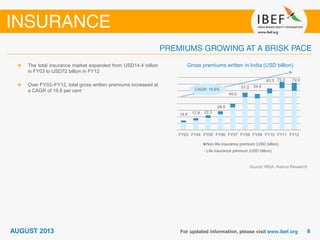

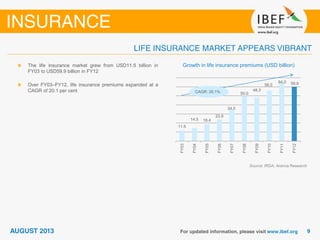

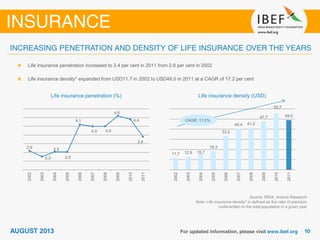

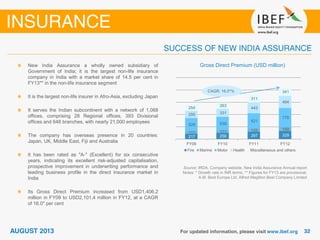

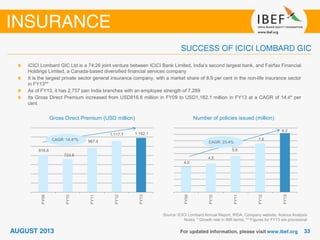

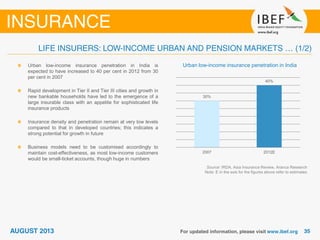

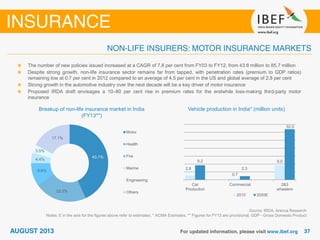

The insurance industry in India has grown rapidly in recent years. Life insurance premiums grew at a CAGR of 20.1% from 2003-2012, while non-life premiums increased at 18%. Private sector participation also increased substantially over this period. Key growth areas for the insurance industry include health, motor, and crop insurance. The government has introduced several policies to support the development of the insurance industry in India.