Downloaded 172 times

![Private Sector

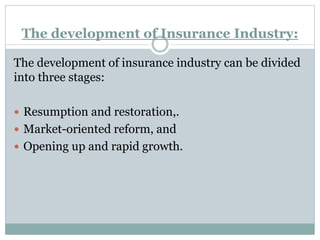

Edelweiss Tokio Life Insurance Co. Ltd.

AEGON Religare Life Insurance

Aviva India

Bajaj Allianz Life Insurance

Kotak Mahindra Old Mutual Life Insurance

TATA AIA Life INSURANCE

Reliance Life Insurance

Star Union Dai-ichi Life Insurance

HDFC Standard Life Insurance Company Limited

IDBI Federal Life Insurance

IndiaFirst Life Insurance Company

Birla Sun Life Insurance

Max Life Insurance[2]

ICICI Prudential Life Insurance Company

Canara HSBC OBC Life Insurance Company Pvt Ltd.

BHARTI Axa life insurance company

Exide Life Insurance company Ltd

L&T general insurance co LTD

SBI Life Insurance Company

DHFL Primerica life insurance](https://image.slidesharecdn.com/insuranceindustryanalyses-150325123913-conversion-gate01/85/Insurance-industry-analyses-12-320.jpg)

The document provides an overview of the insurance industry. It discusses key concepts like risk transfer, premiums, and risk management. It outlines the history and evolution of insurance from early practices in ancient China and Babylon to the modern insurance industry. It also describes the major players in the Indian insurance market like Life Insurance Corporation of India and lists the different types of insurance like auto, health and life insurance. Furthermore, it analyzes the industry using Porter's Diamond model and discusses strengths, weaknesses and future prospects of growth in the insurance sector in India.