Downloaded 33 times

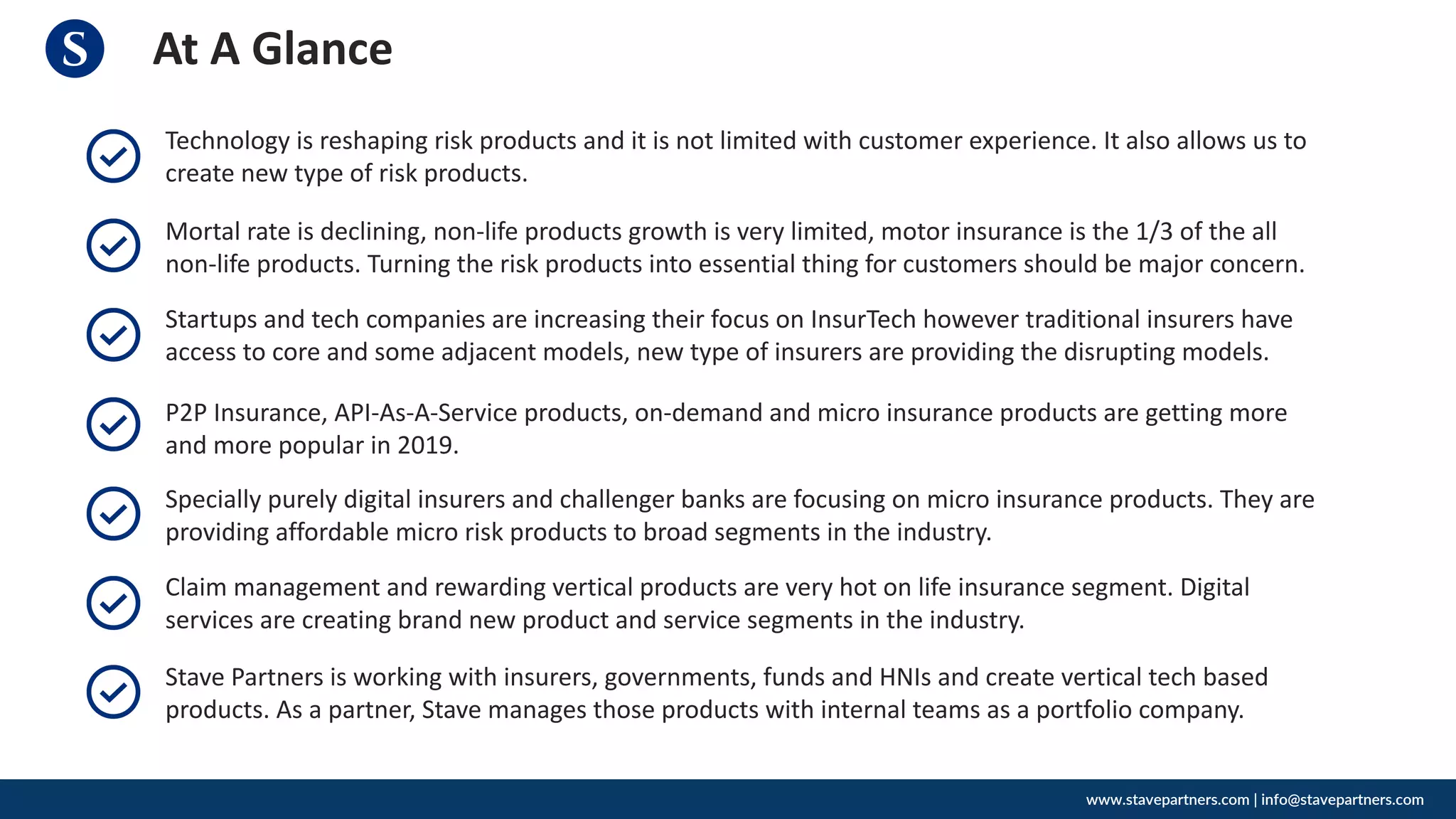

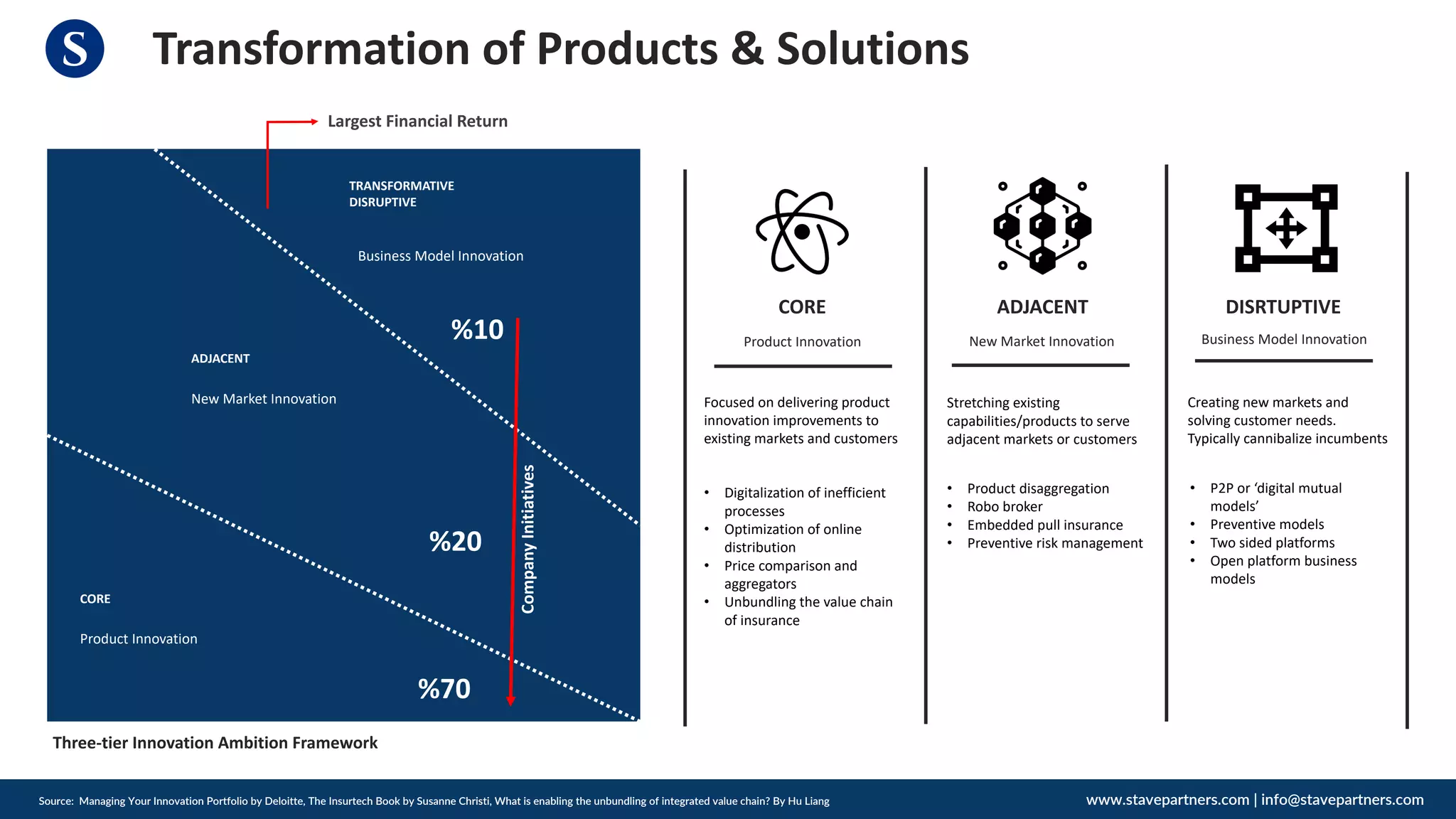

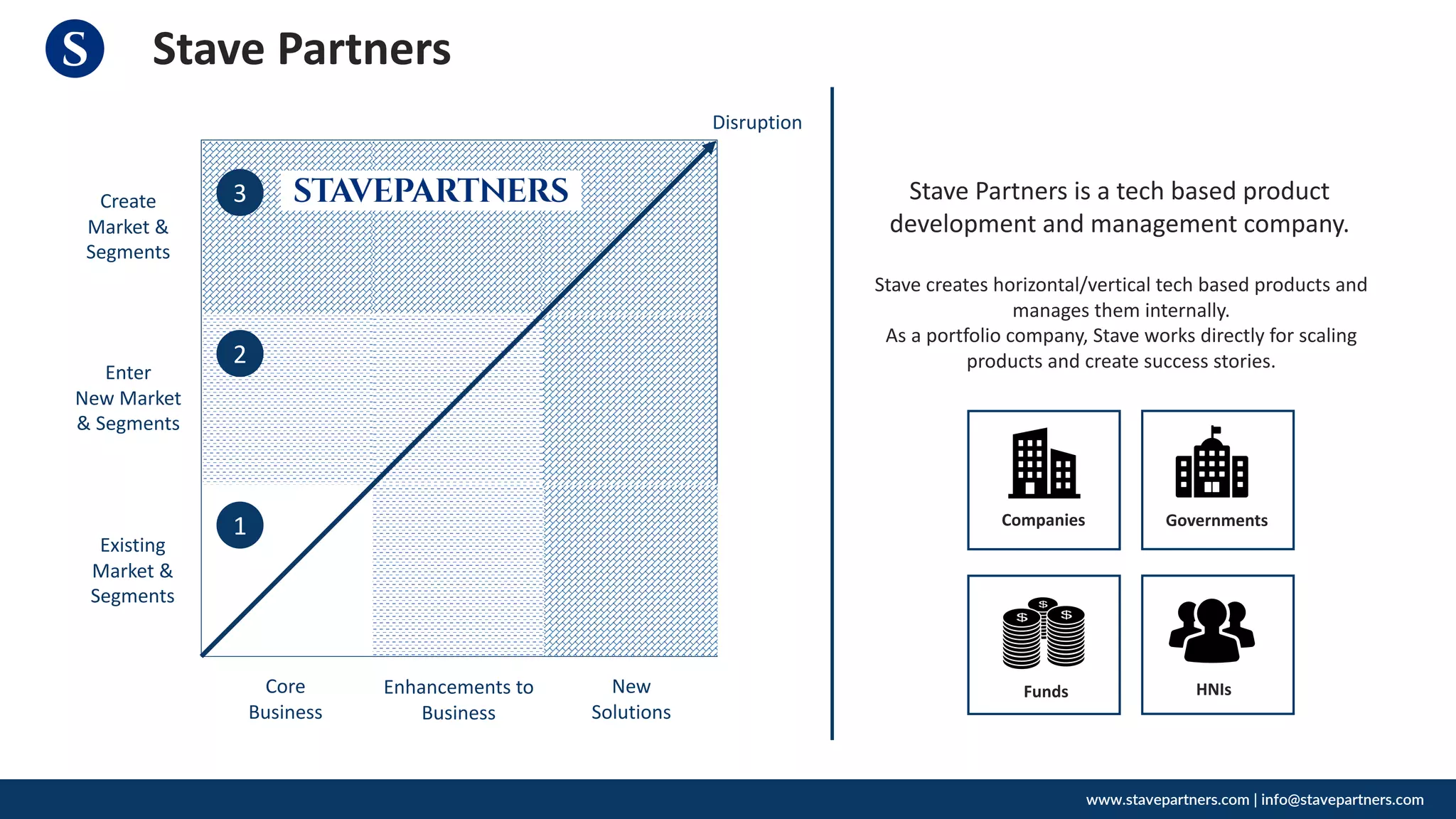

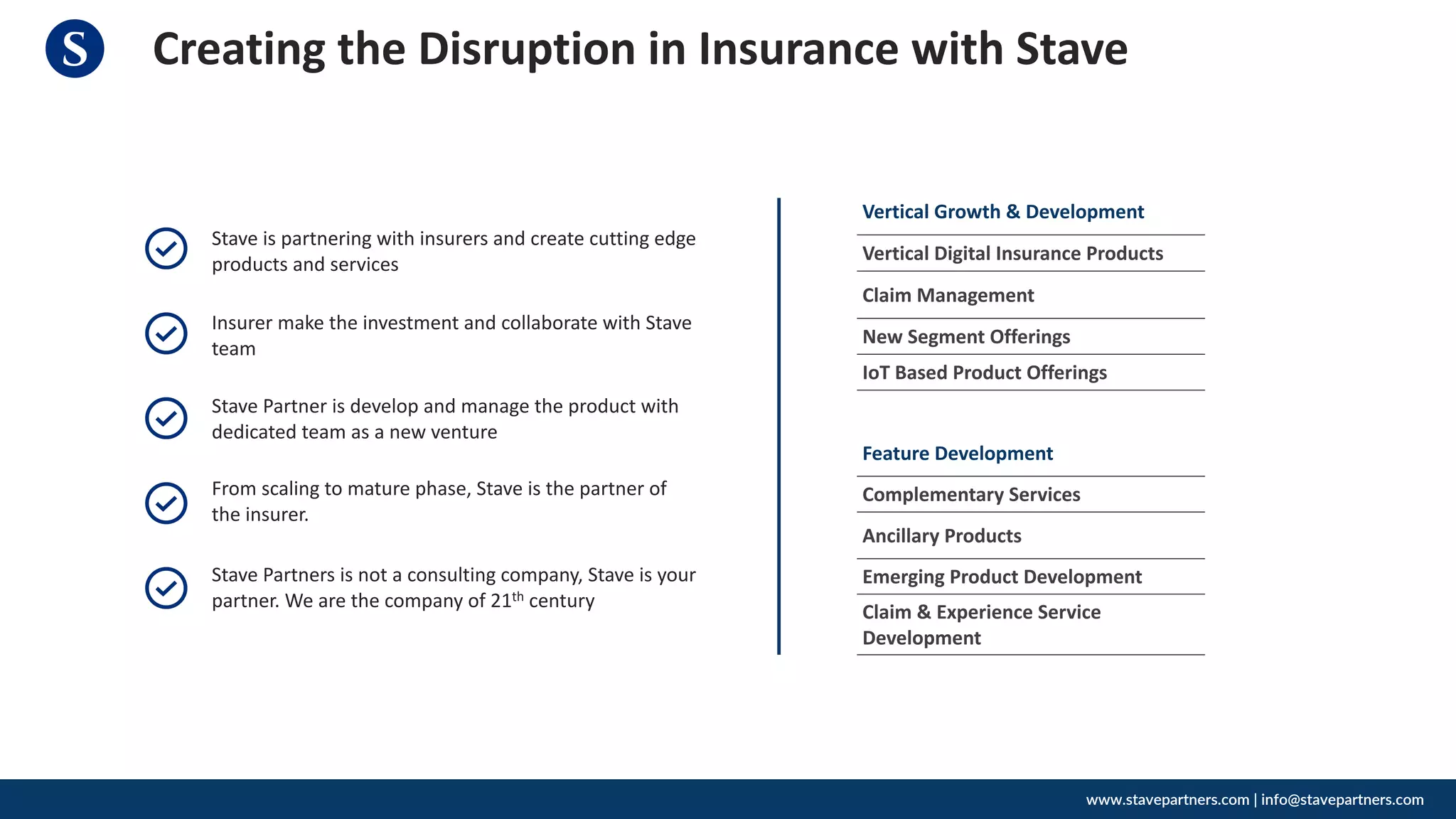

The document outlines the evolving landscape of the insurance industry, emphasizing the impact of technology and emerging insurtech startups that disrupt traditional models through innovative products such as P2P and micro insurance. It discusses key trends in life and non-life insurance markets, including challenges of stagnant premiums and changing customer expectations, while highlighting the importance of data-centric strategies for customer acquisition and retention. Stave Partners positions itself as a technology-based product development company that collaborates with insurers to create and manage transformative insurance solutions.

![Coded Agents – with UiPath SDK + LangGraph [Virtual Hands-on Workshop]](https://cdn.slidesharecdn.com/ss_thumbnails/codedagentsdeck-251215155422-5497c599-thumbnail.jpg?width=640&height=640&fit=bounds)