Downloaded 43 times

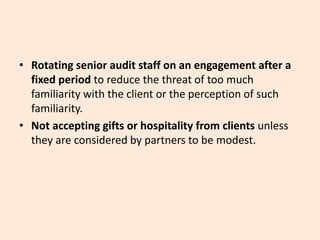

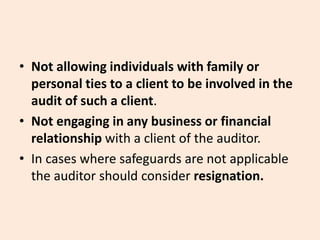

The auditor should take several measures to safeguard independence when providing other services to clients. This includes monitoring fees received from clients to reduce dependence, rotating senior staff periodically, not accepting gifts from clients, and not having family or business ties to clients. Independence involves both appearing independent and being independent. Providing additional services can threaten independence through familiarity, self-review, and self-interest. The auditor benefits from additional remuneration and expertise while the client benefits from a wider range of skills without permanent staff costs.