The document outlines the various tax rates applicable to different entities in India for the fiscal year 2017-18, including individuals, HUFs, partnership firms, companies, LLPs, AOPs, BOIs, cooperative societies, and local authorities. It provides the basic exemption limits and tax slabs for individuals of different ages. It also summarizes the steps to compute taxable income and tax liability for these different entities. Key tax rates mentioned include 30% for firms/LLPs, 25-40% for domestic and foreign companies depending on income level, and 10-30% for cooperative societies based on taxable income.

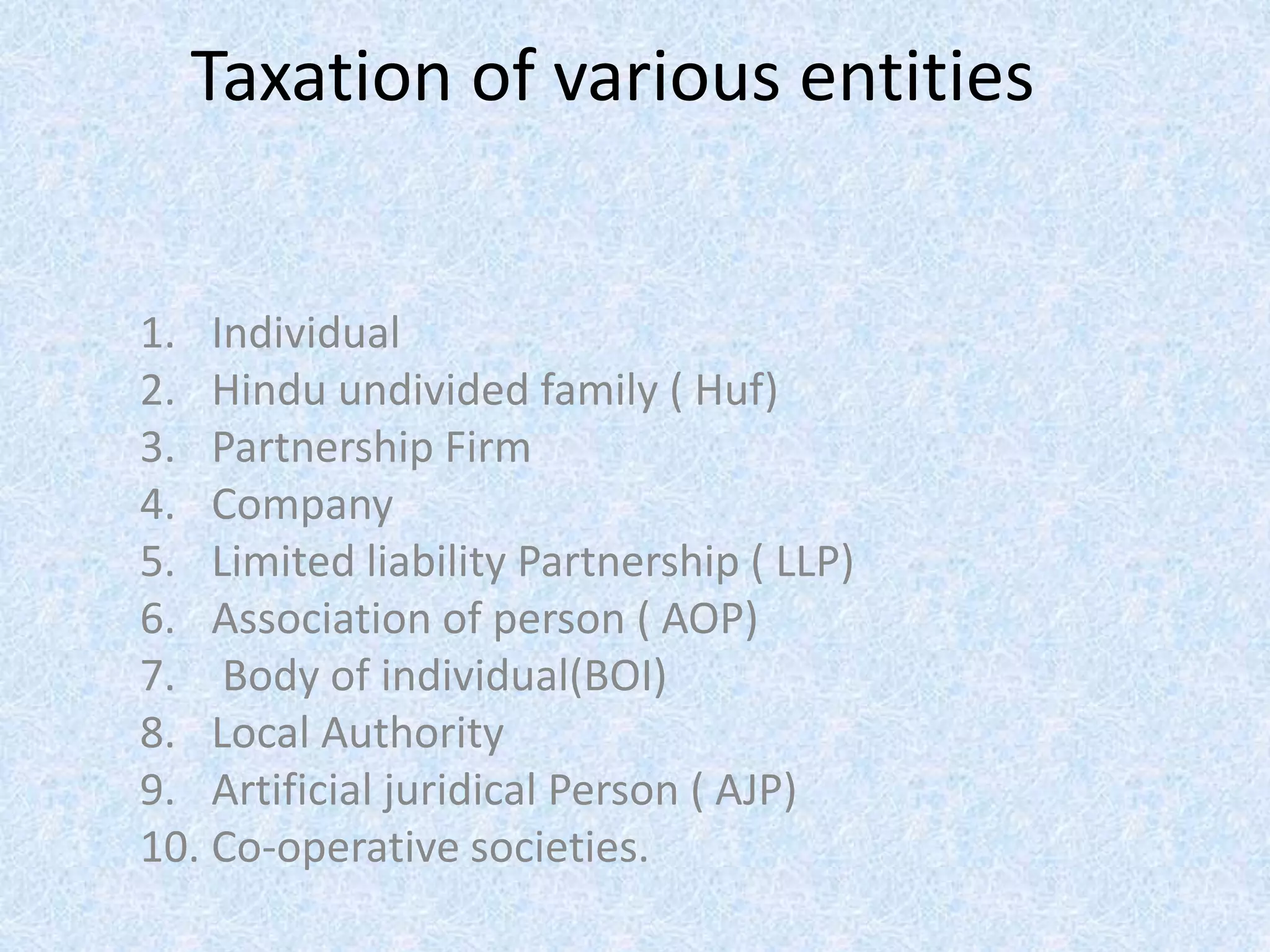

Taxation of variousentities

1. Individual

2. Hindu undivided family ( Huf)

3. Partnership Firm

4. Company

5. Limited liability Partnership ( LLP)

6. Association of person ( AOP)

7. Body of individual(BOI)

8. Local Authority

9. Artificial juridical Person ( AJP)

10. Co-operative societies.

2.

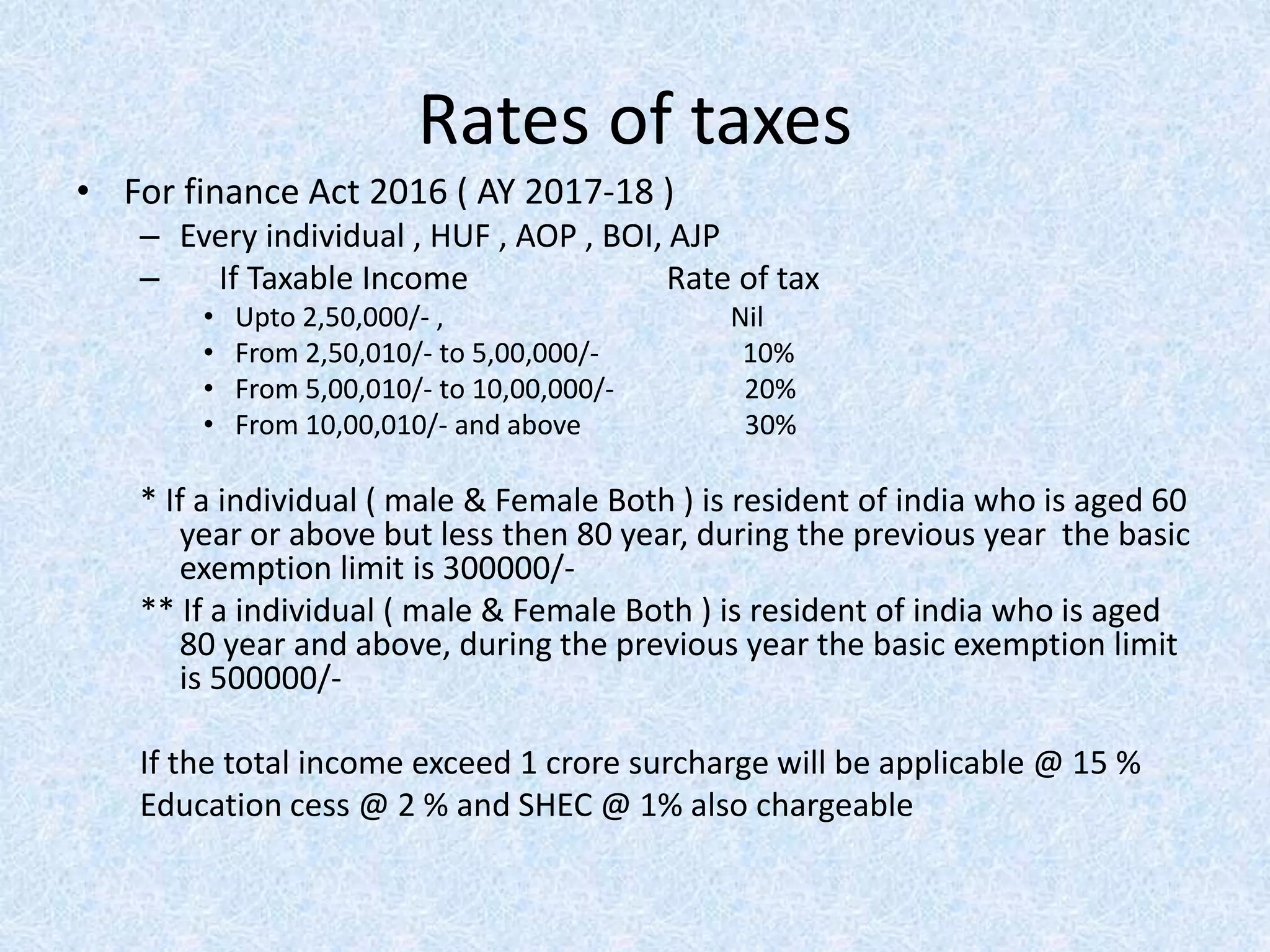

Rates of taxes

•For finance Act 2016 ( AY 2017-18 )

– Every individual , HUF , AOP , BOI, AJP

– If Taxable Income Rate of tax

• Upto 2,50,000/- , Nil

• From 2,50,010/- to 5,00,000/- 10%

• From 5,00,010/- to 10,00,000/- 20%

• From 10,00,010/- and above 30%

* If a individual ( male & Female Both ) is resident of india who is aged 60

year or above but less then 80 year, during the previous year the basic

exemption limit is 300000/-

** If a individual ( male & Female Both ) is resident of india who is aged

80 year and above, during the previous year the basic exemption limit

is 500000/-

If the total income exceed 1 crore surcharge will be applicable @ 15 %

Education cess @ 2 % and SHEC @ 1% also chargeable

3.

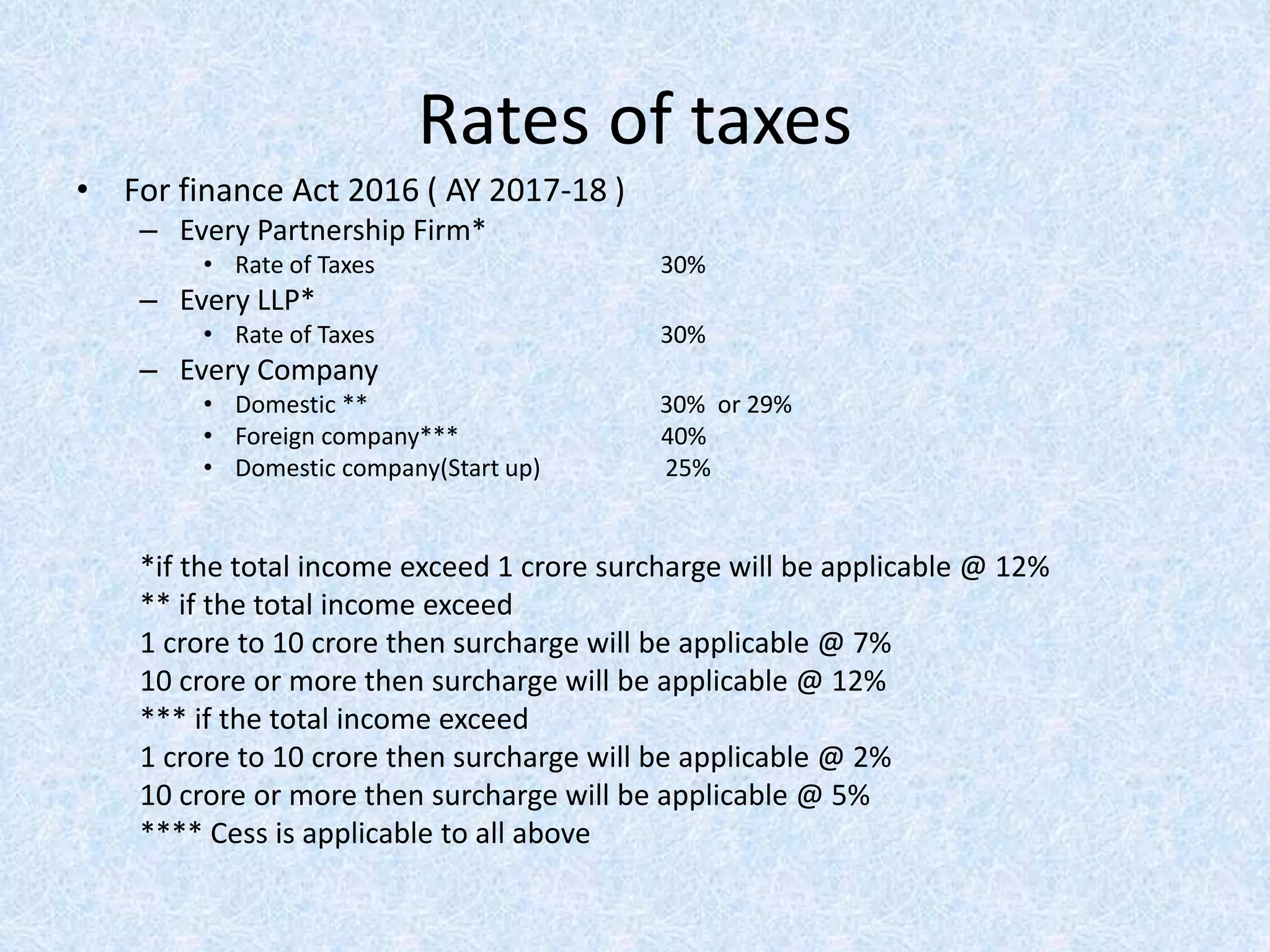

Rates of taxes

•For finance Act 2016 ( AY 2017-18 )

– Every Partnership Firm*

• Rate of Taxes 30%

– Every LLP*

• Rate of Taxes 30%

– Every Company

• Domestic ** 30% or 29%

• Foreign company*** 40%

• Domestic company(Start up) 25%

*if the total income exceed 1 crore surcharge will be applicable @ 12%

** if the total income exceed

1 crore to 10 crore then surcharge will be applicable @ 7%

10 crore or more then surcharge will be applicable @ 12%

*** if the total income exceed

1 crore to 10 crore then surcharge will be applicable @ 2%

10 crore or more then surcharge will be applicable @ 5%

**** Cess is applicable to all above

4.

Rates of taxes

•For finance Act 2016 ( AY 2017-18 )

– Every Co-operative Society

– If Taxable Income Rate of tax

• Up to 10000/- 10%

• From 10000/- to 20000/- 20%

• From 20000/- and above 30%

• If the total income exceed 1 crore surcharge will be

applicable @ 12 %

Education cess @ 2 % and SHEC @ 1% also chargeable

5.

Steps of Computationof

income of individual– Calculate the income from different head after

the deduction mentioned in respective heads of

income.

– Clubbing of income u/s 60 to 64.

– Carry forward and set off losses.

– Deduction u/s 80 C to 80 U.

– Calculate the Tax Liability.

– Relief u/s 89 if Any.

– Deduct TDS/Advance Tax.

– Refund or self assessment tax.

6.

Income taxable inhand of individual

1. Earned by himself with different Head of income

( 5 Head of income Respectively )

2. Earned as a partner of firm / LLP.

1. Profit from the firm/ LLP- Exempt

2. Remuneration - Taxable

3. Interest on Capital – Taxable

3. Earned as a member of AOP.- as per respective

rules.

4. Received as a member of HUF. – exempt.

5. Clubbing of income u/s 60 to 64.

7.

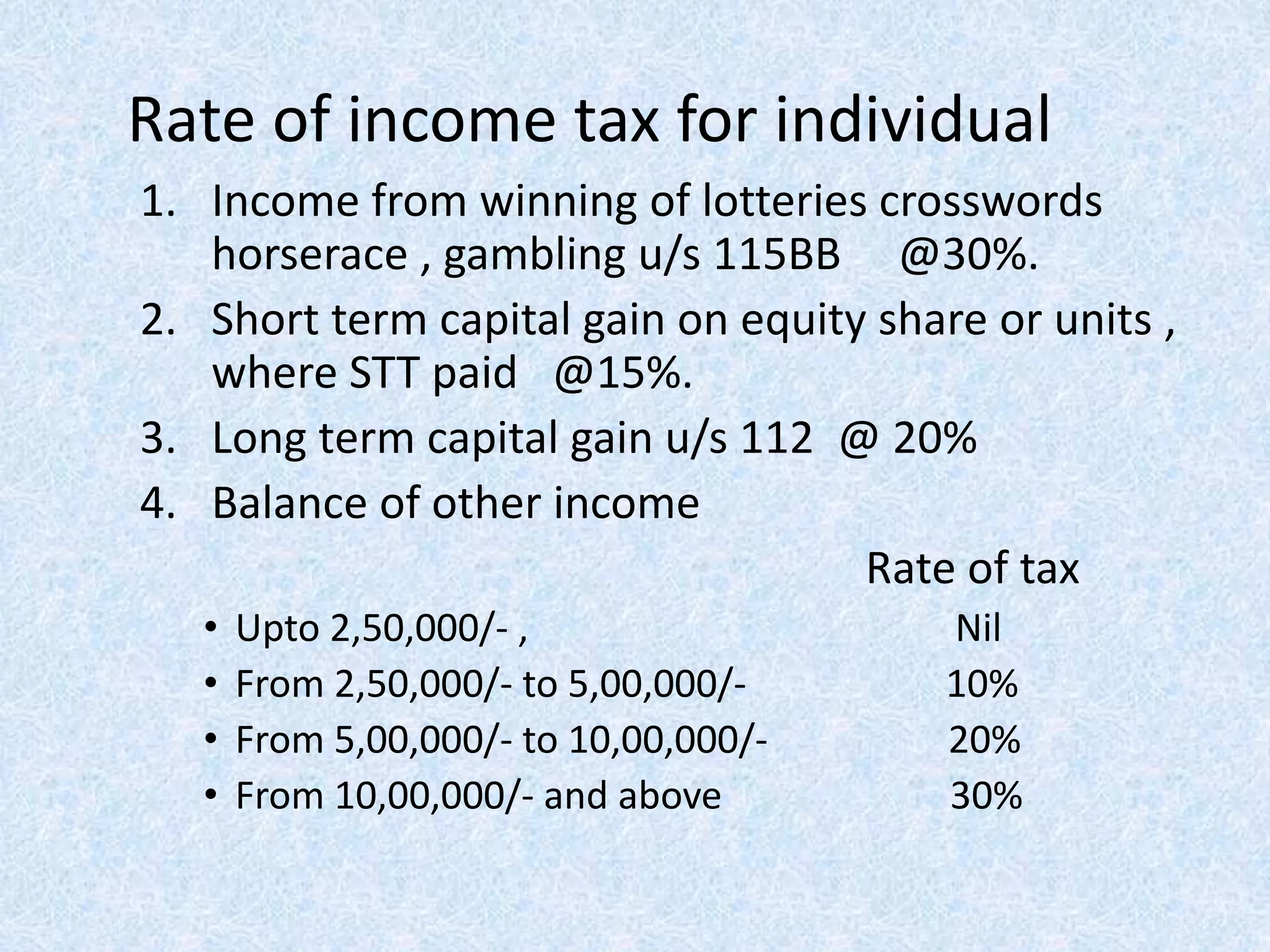

Rate of incometax for individual

1. Income from winning of lotteries crosswords

horserace , gambling u/s 115BB @30%.

2. Short term capital gain on equity share or units ,

where STT paid @15%.

3. Long term capital gain u/s 112 @ 20%

4. Balance of other income

Rate of tax

• Upto 2,50,000/- , Nil

• From 2,50,000/- to 5,00,000/- 10%

• From 5,00,000/- to 10,00,000/- 20%

• From 10,00,000/- and above 30%

8.

Income taxable inhand of HUF

Formation of HUF is based on grounds of 2 Acts

Hindu succession Act 1956

Hindu marriage Act 1955

– Hindu law is applicable also on Jains , Sikhs,

Buddist

– Now Daughter is also a coparcener and can be a

karta of her fathers HUF w.e.f. 09.09.2005.

– Creation of HUF

• By way if inheritant property

• Partition of Bigger HUF

• By way of Gift

9.

Steps of Computationof

income of HUF

– Calculate the income from different head after

the deduction mentioned in respective heads of

income other than salary.

– Clubbing of income u/s 60 to 63.

– Carry forward and set off losses.

– Deduction u/s 80 C to 80 U.

– Calculate the Tax Liability.

– Deduct TDS/Advance Tax.

– Refund or self assessment tax.

10.

Other benefits ofHUF

– Capital Gain on Sale of Property u/s 54.

– Capital Gain on Transfer of Agriculture land 54 B.

– Capital Gain on Compulsory Acquisition 54D.

– Capital Gain on Long Term Capital Assets u/s 54 EC

– Capital Gain on investment made u/s 54 F

– Capital Gain on Transfer of Shifting u/s 54G

11.

Rate of incometax for HUF

1. Income from winning of lotteries crosswords

horserace , gambling u/s 115BB @30%.

2. Short term capital gain on equity share or units ,

where STT paid @15%.

3. Long term capital gain u/s 112 @ 20%

4. Balance of other income

– Rate of tax

• Up to 2,50,000/- , Nil

• From 2,50,000/- to 5,00,000/- 10%

• From 5,00,000/- to 10,00,000/- 20%

• From 10,00,000/- and above 30%

12.

Assessment of Firm/ LLP

• Act cover

– Indian Partnership Act 1932.

– Limited Liability Partnership Act 2008.

13.

Calculation of BookProfits

• Income from Business and profession as per

section 28 to 44 D under Business Head .

• Add:- interest paid to partner excess of 12%

• Add:- Remuneration paid / payable to all

partner

14.

Remuneration Payable

• Asper section 40 (b)

– On first 300000/- of the book profit or in case of

loss ---------------- 150000/- or 90% of book profit

whichever is more.

– Balance of book profit ---------------- @ 60%.

15.

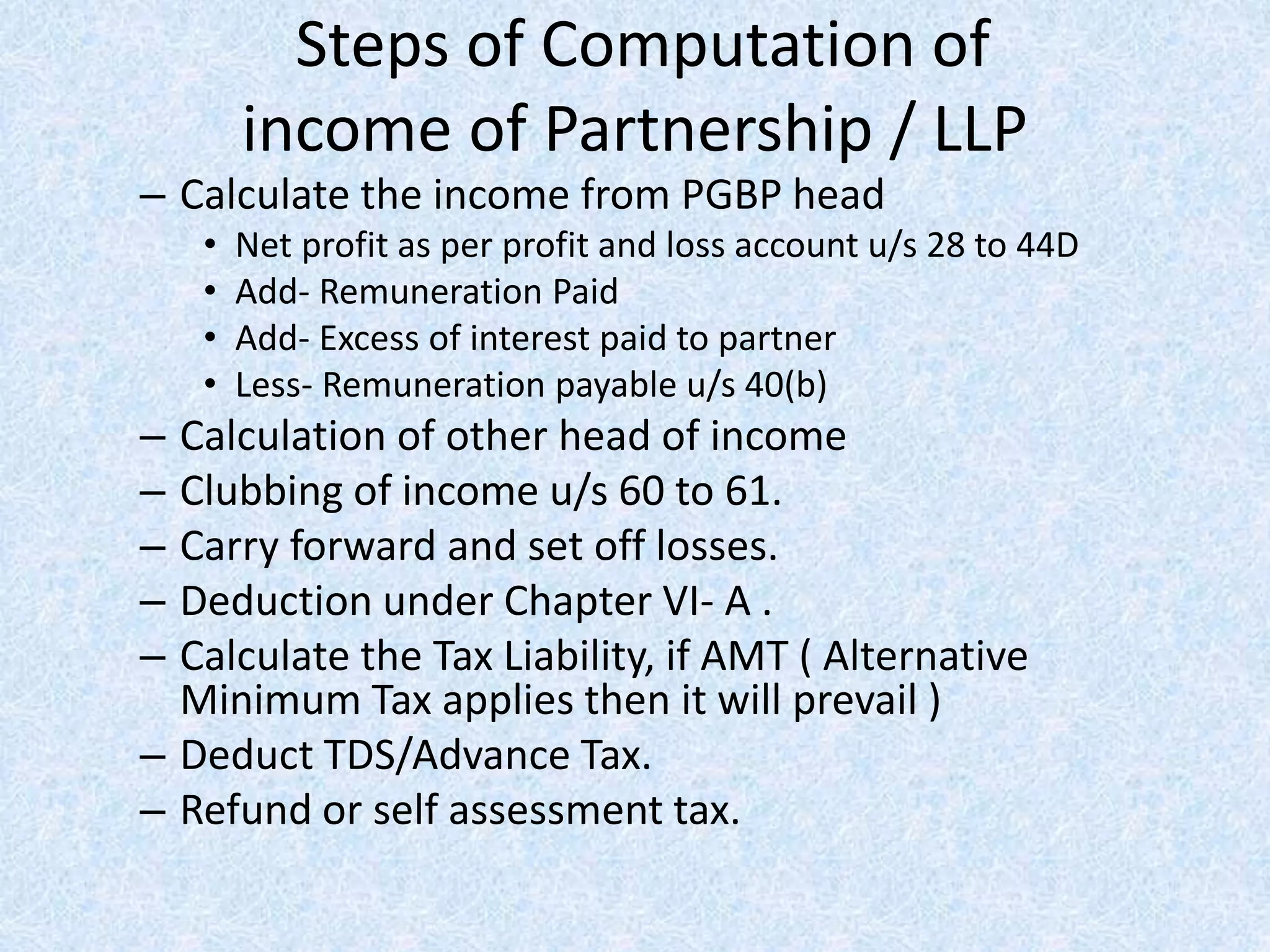

Steps of Computationof

income of Partnership / LLP

– Calculate the income from PGBP head

• Net profit as per profit and loss account u/s 28 to 44D

• Add- Remuneration Paid

• Add- Excess of interest paid to partner

• Less- Remuneration payable u/s 40(b)

– Calculation of other head of income

– Clubbing of income u/s 60 to 61.

– Carry forward and set off losses.

– Deduction under Chapter VI- A .

– Calculate the Tax Liability, if AMT ( Alternative

Minimum Tax applies then it will prevail )

– Deduct TDS/Advance Tax.

– Refund or self assessment tax.

16.

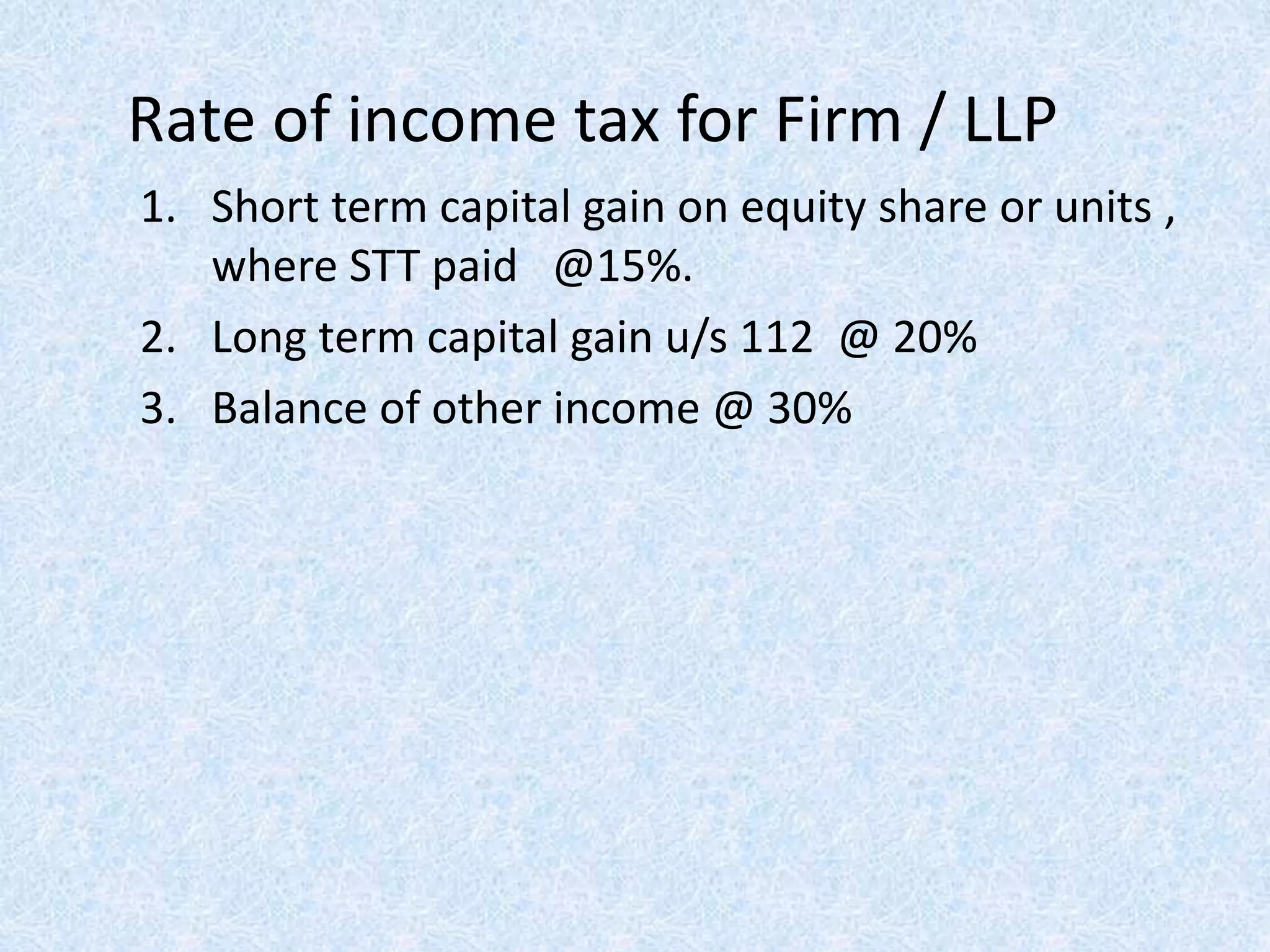

Rate of incometax for Firm / LLP

1. Short term capital gain on equity share or units ,

where STT paid @15%.

2. Long term capital gain u/s 112 @ 20%

3. Balance of other income @ 30%

17.

Assessment of AOP/ BOI

• AOP/ BOI includes

– Society registered U/s 1860

• Private Trust

– Specific

– Discretionary

• Charitable Trust(Registered u/s 12A or

Unregistered )

• Oral Trust

• Joint Venture

• Mutual Association

• Any other AOP/BOI

18.

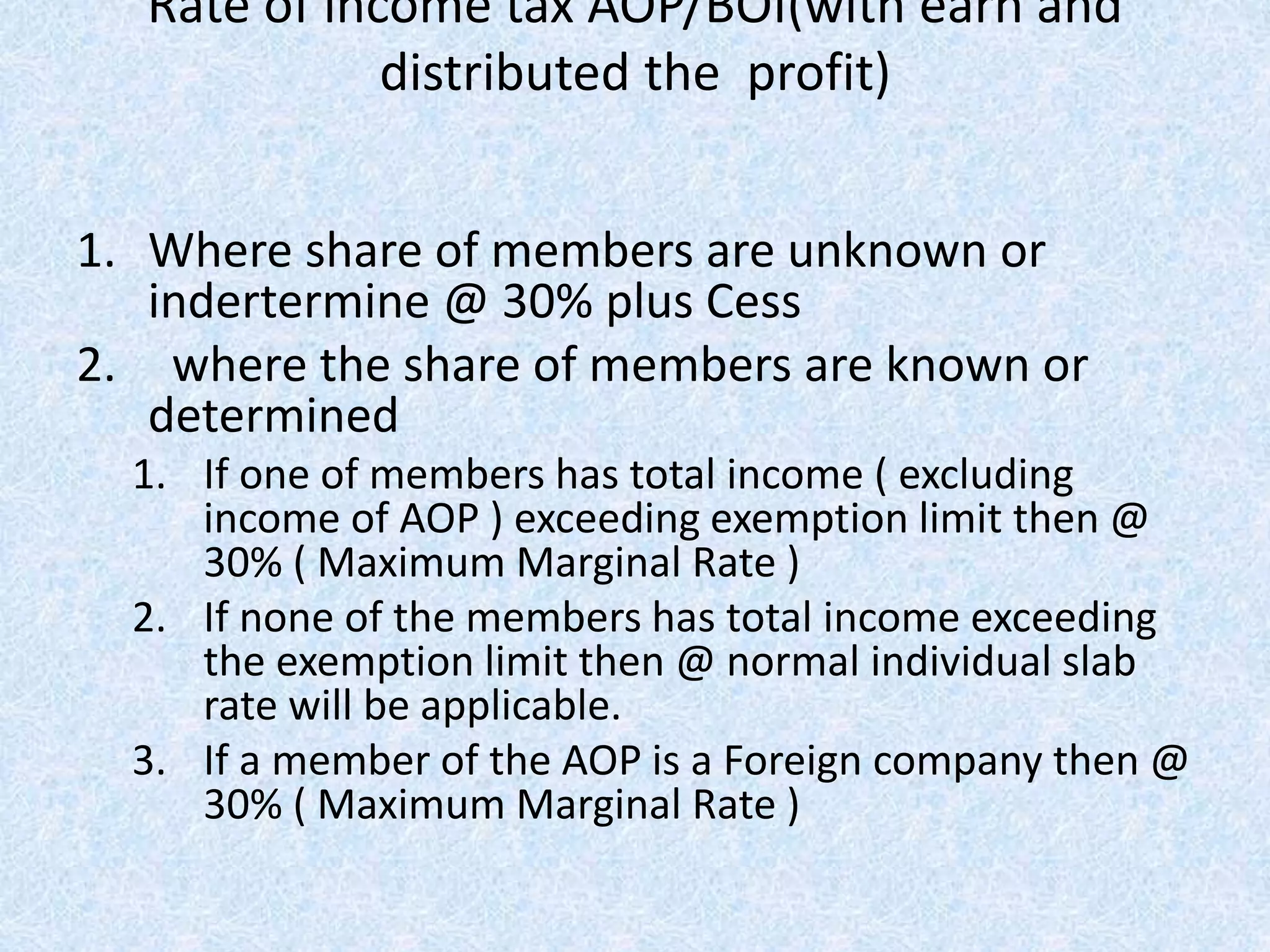

Rate of incometax AOP/BOI(with earn and

distributed the profit)

1. Where share of members are unknown or

indertermine @ 30% plus Cess

2. where the share of members are known or

determined

1. If one of members has total income ( excluding

income of AOP ) exceeding exemption limit then @

30% ( Maximum Marginal Rate )

2. If none of the members has total income exceeding

the exemption limit then @ normal individual slab

rate will be applicable.

3. If a member of the AOP is a Foreign company then @

30% ( Maximum Marginal Rate )

19.

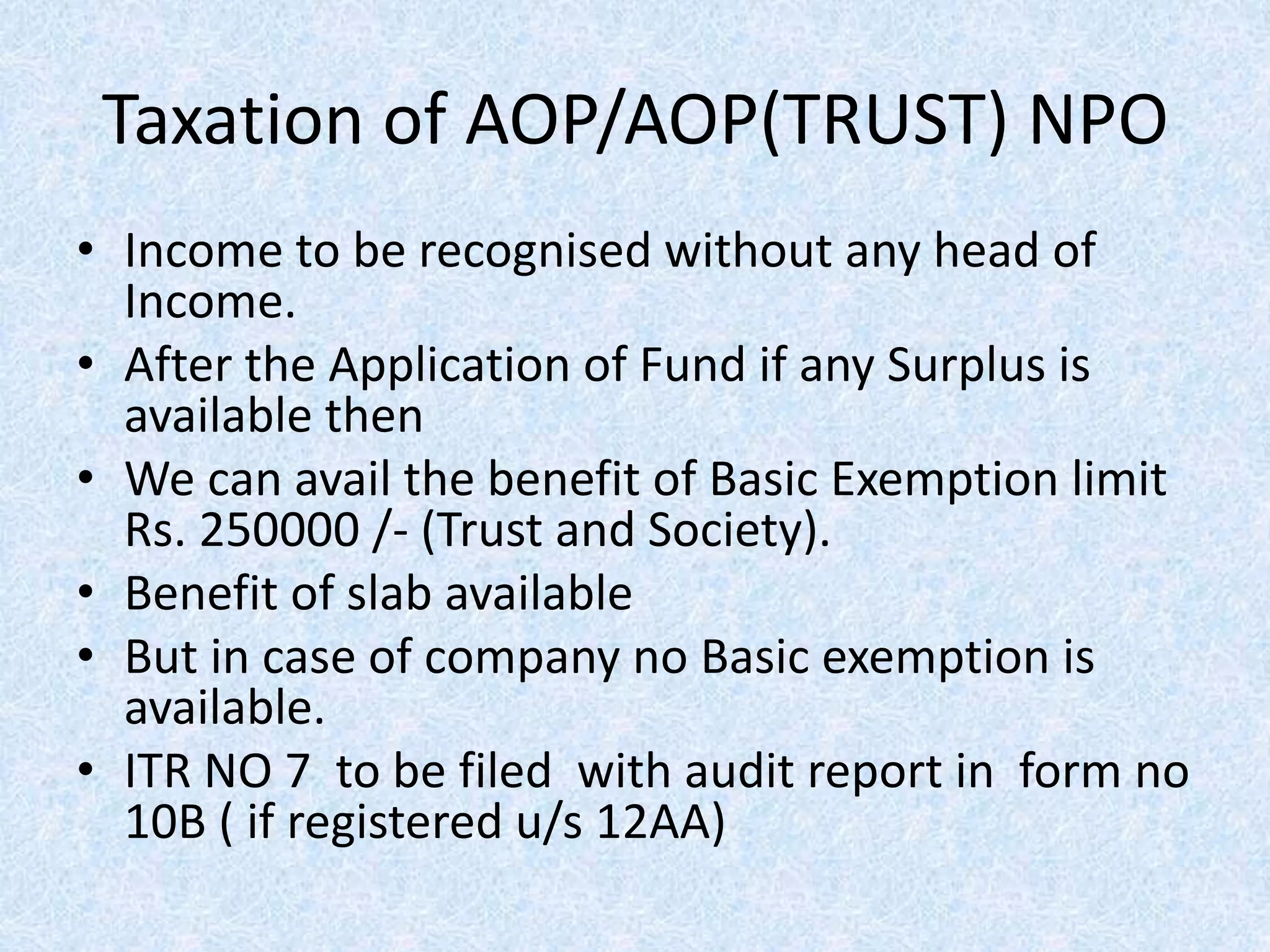

Taxation of AOP/AOP(TRUST)NPO

• Income to be recognised without any head of

Income.

• After the Application of Fund if any Surplus is

available then

• We can avail the benefit of Basic Exemption limit

Rs. 250000 /- (Trust and Society).

• Benefit of slab available

• But in case of company no Basic exemption is

available.

• ITR NO 7 to be filed with audit report in form no

10B ( if registered u/s 12AA)

20.

Taxation of AOP/AOP(TRUST)NPO

Charged @ maximum marginal rate (@30%)

• Any direct or indirect benefits transfer to the

related person refer section 13(3).( excess of

Market Rate.)

• Any part of the income applied to related

person refer section 13(3). ( excess of Market

Rate.)

• Income received from the investment which

are not as per section 11(5).

• Anonymous donation as per section 115 BBC

Steps of Computationof

income Co- operative society

– Calculate the income from Four head

– Deduction under Chapter VI- A ( 80 G to 80 P).

– Tax calulation

– Deduct TDS/Advance Tax.

– Refund or self assessment tax.

23.

Deduction u/s 80P

• 100% deduction is allowed of the profits

– Profit attributable to certain specified Activity

• Carrying of business of banking and credit facility to its

members.

• cottage industry

• Marketing of agriculture produce by its members

• Fishing and allied Activities by its members

• Society engaged in supply of milk ,oil seeds , vegetable fruits

by its member

• Income from investments with other co-operative society

• Income from letting out of go down or where house for

agriculture produce

24.

Deduction u/s 80P

• Where the co- operative society engaged in

other Activity mentioned above

– If consumer co-operative society then 100000/-

– If other society then it will be 50000/-

25.

Rates of taxesco-operative society

• For finance Act 2015 ( AY 2016-17 )

– Every Co-op rative Society

– If Taxable Income Rate of tax

• Up to 10000/- 10%

• From 10000/- to 20000/- 20%

• From 20000/- and above 30%

• If the total income exceed 1 crore surcharge will be

applicable @ 12 %

Education cess @ 2 % and SHEC @ 1% also chargeable

26.

Assessment of Companies

–Calculate the income from all four head

– Clubbing of income u/s 60 to 61.

– Carry forward and set off losses.

– Deduction under Chapter VI- A .

– Calculate the Tax Liability, if MAT (Minimum

Alternative Tax applies then it will prevail )

– Deduct TDS/Advance Tax.

– Refund or self assessment tax.

27.

Rates of taxesof companies

1. Income from winning of lotteries crosswords horserace ,

gambling u/s 115BB @30%.

2. Short term capital gain on equity share or units , where STT

paid @15%.

3. Long term capital gain u/s 112 @ 20%

4. Tax of income by way of dividend declared or paid by foreign

company u/s 115 BBB @15%

5. Every Company

• Domestic ** 30%

• Foreign company*** 40%

** if the total income exceed

1 crore to 10 crore then surcharge will be applicable @ 7%

10 crore or more then surcharge will be applicable @ 12%

*** if the total income exceed

1 crore to 10 crore then surcharge will be applicable @ 2%

10 crore or more then surcharge will be applicable @ 5%

**** Cess is applicable to all above

28.

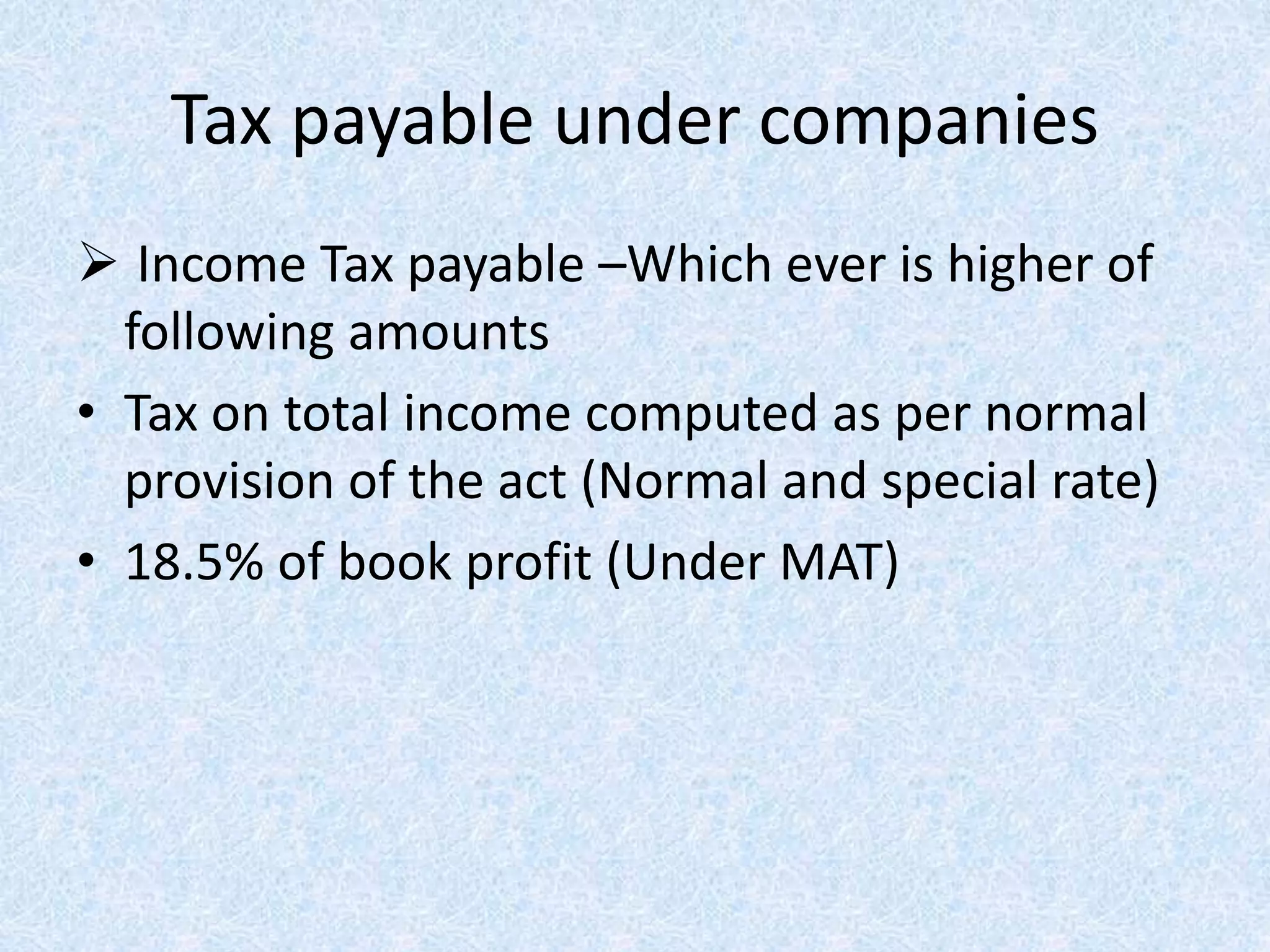

Tax payable undercompanies

Income Tax payable –Which ever is higher of

following amounts

• Tax on total income computed as per normal

provision of the act (Normal and special rate)

• 18.5% of book profit (Under MAT)

29.

Calculation of MAT

•Profit as per profit and loss account

– Where amount shown is debited in the profit and

loss account to be added back

• Income tax paid or payable

• Amount transfer to any reserve

• Amount by way of provision of loss by subsidiary

company

• Amount of proposed dividend

• Amount of depreciation

• Amount of deferred tax provision

30.

Calculation of MAT

•Profit as per profit and loss account

– Where amount shown is credited in the profit and loss

account to be Reduced

• Withdrawal of any reserve or provisions.

• Amount of income u/s 10

• Amount of depreciation ( excluding depreciation of

revaluation of fixed assets )

• Amount withdrawal from revaluation reserve.

• Amount of loss brought forward or unabsorbed depreciation

whichever is less as per books of accounts

• Amount of profit derived from tonnage taxation scheme 115

VO

31.

Taxability of entity– income are

exempt u/s 10 (23) (c)

• Prime minister national relief fund.

• Any university or institutions wholly or substantially financed by

government.

• Any hospital or institutions substantially financed by government.

• Any university or institution solely for education purpose whom

annual receipt do not exceed 1 crore.

• Any hospital or institute who’s gross receipt do not exceed 1 crore.

• Any fund or institutions for charitable purpose approved by

prescribed authority of any states.

• Any university or education institute solely for education purpose

who’s annual receipt exceed 1 crore Approved with income tax

Authority.

• Any hospital or other institute who’s gross receipt exceed 1 crore

and Approved with income tax authority.

![[wacc] weighted average cost of capital](https://cdn.slidesharecdn.com/ss_thumbnails/anuragmathur-210703072911-thumbnail.jpg?width=640&height=640&fit=bounds)