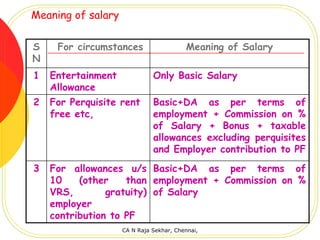

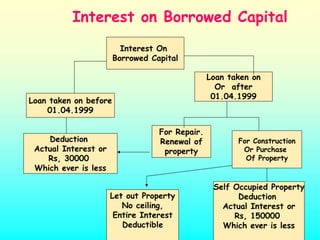

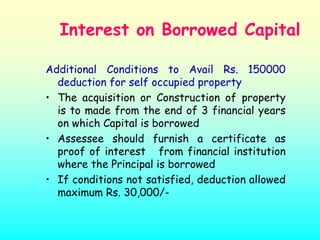

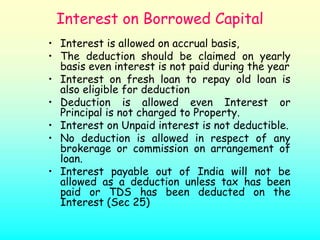

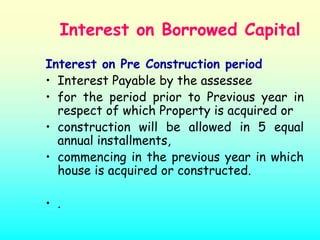

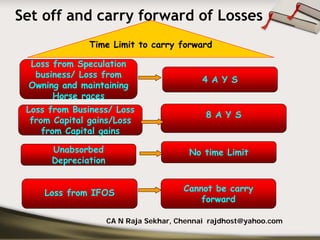

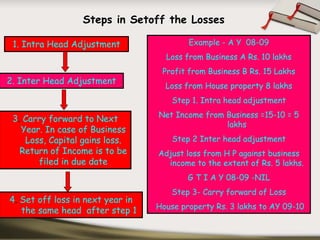

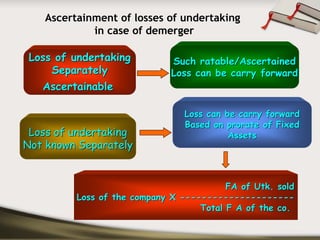

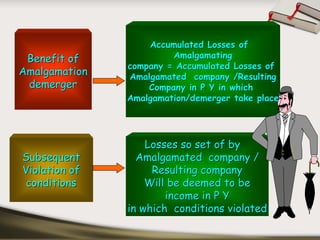

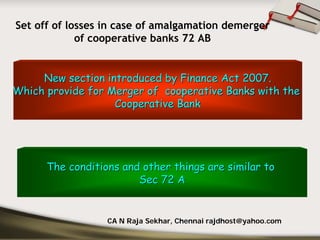

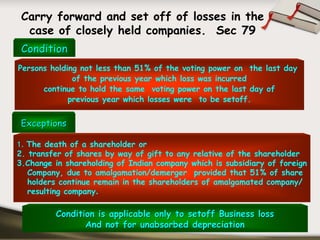

Downloaded 450 times

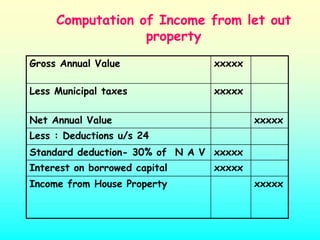

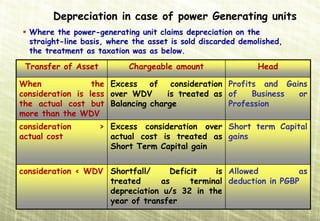

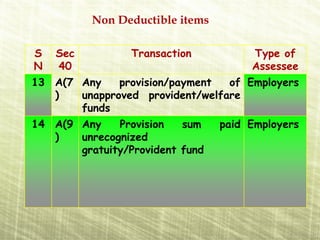

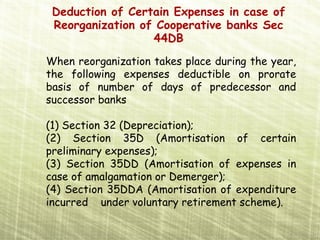

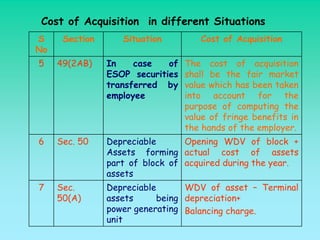

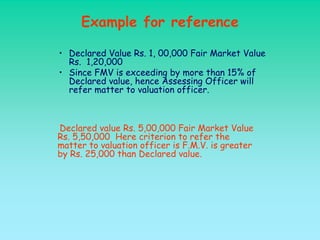

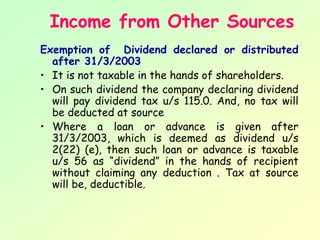

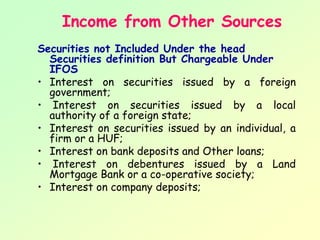

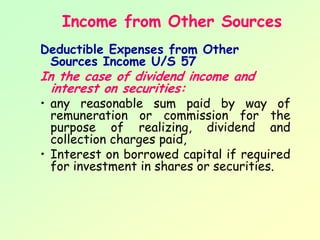

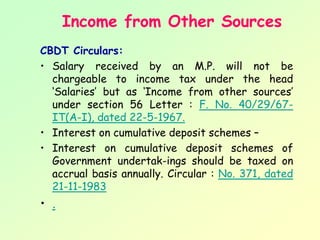

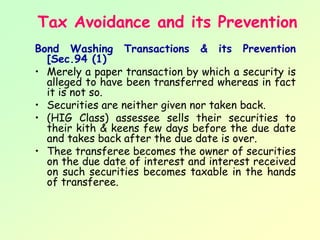

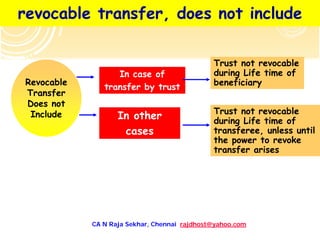

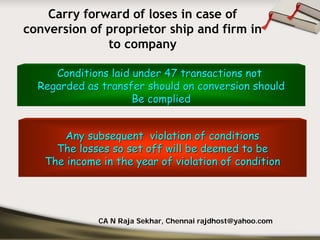

![Perquisites

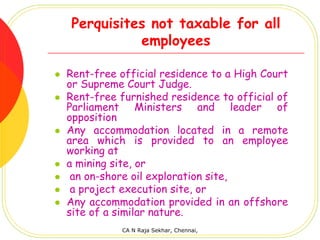

Perquisites taxable only in hands of

specified employees

Provision of domestic servants [Rule

3(3)]

Provision of gas/electricity/water

[Rule 3(4)]

Provision of free or concessional

educational facilities [Rule 3(5)

CA N Raja Sekhar, Chennai,](https://image.slidesharecdn.com/incometax-100624010225-phpapp02/85/Income-tax-40-320.jpg)

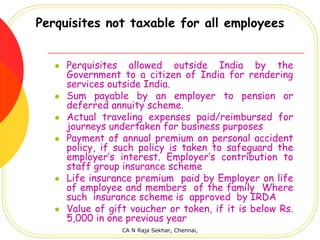

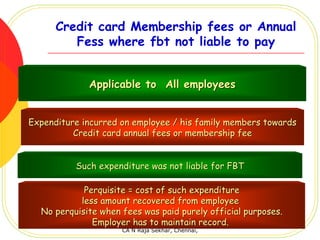

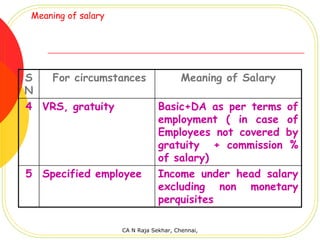

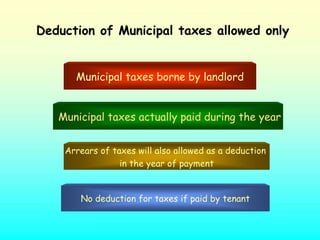

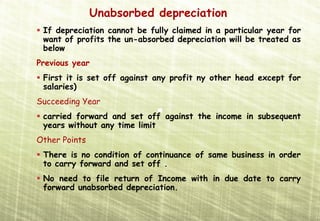

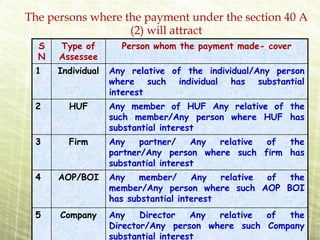

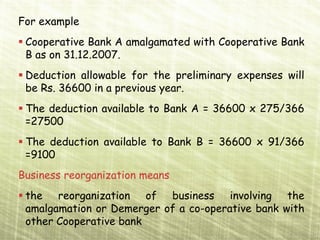

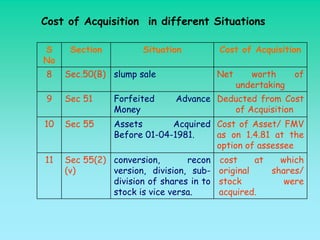

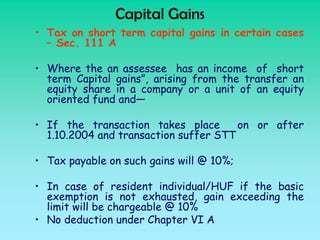

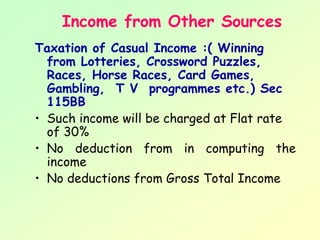

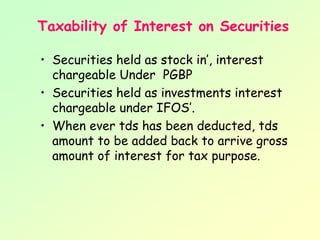

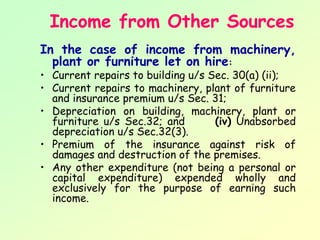

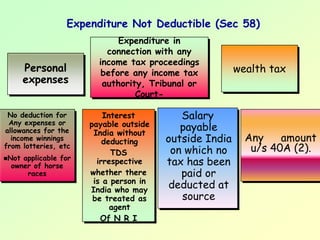

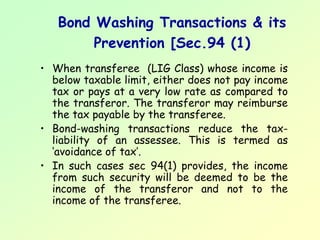

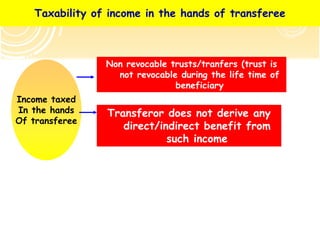

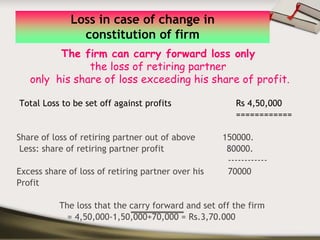

![F B T vs allowances

With the introduction of fringe benefit tax

the following perquisites/ allowances will

not be taxed in the hands of employee if

FBT was payable and paid by employer

Provision of car and other conveyances [Rule

3(2)]

Provision of transport facility by transport

undertakings [Rule 3(6)]

Provision of holiday tours [Rule 3(7)(ii)]

Provision of free food and non-alcoholic

beverages [Rule 3(7)(iii)]

Provision of gifts [Rule 3(7)(iv)]

Provision of credit card facility [Rule 3(7)(v)]

Provision of club facilities [Rule 3(7)(vi)]

CA N Raja Sekhar, Chennai,](https://image.slidesharecdn.com/incometax-100624010225-phpapp02/85/Income-tax-61-320.jpg)

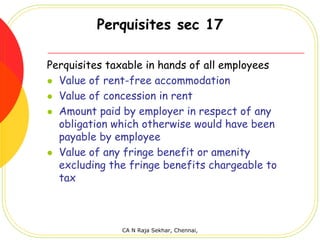

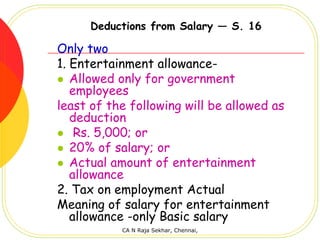

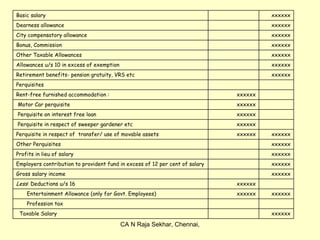

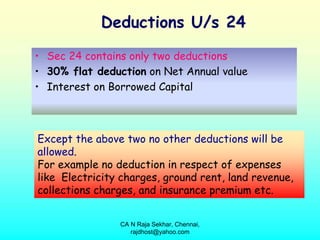

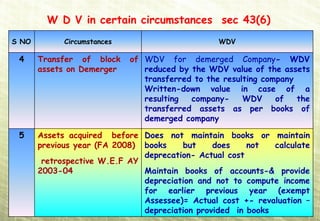

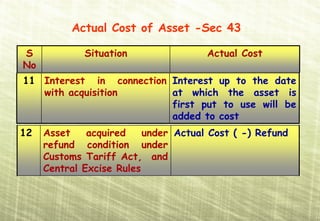

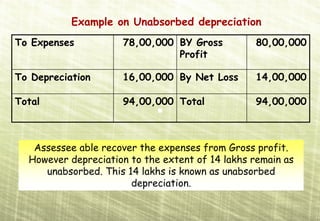

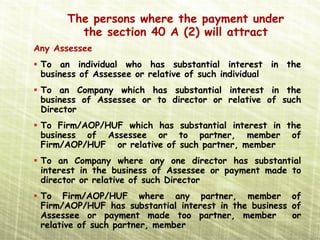

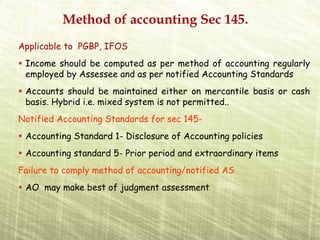

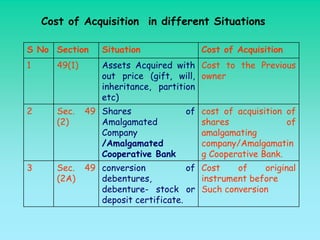

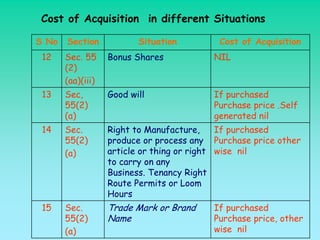

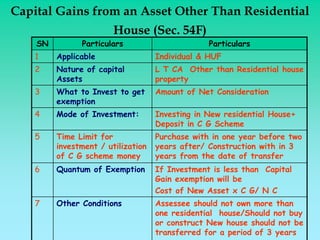

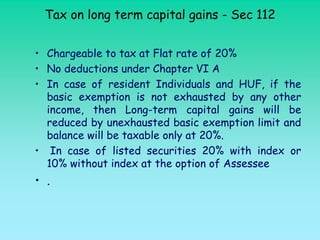

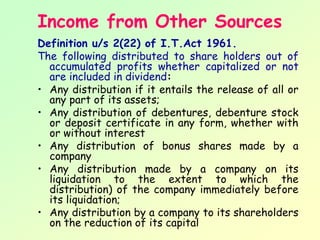

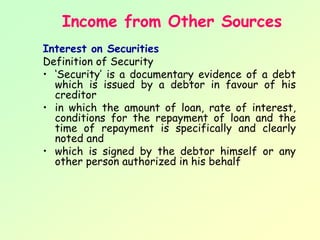

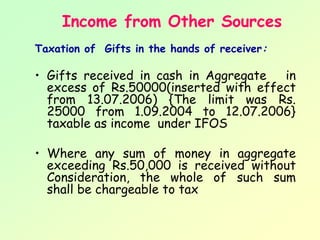

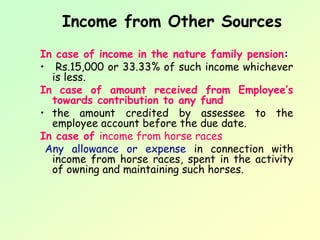

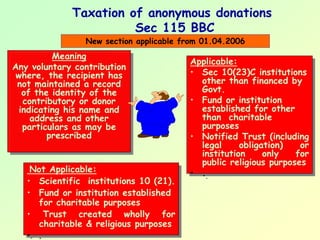

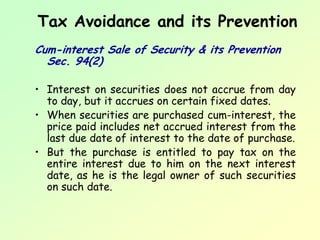

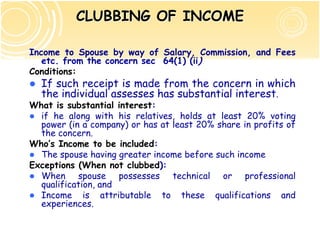

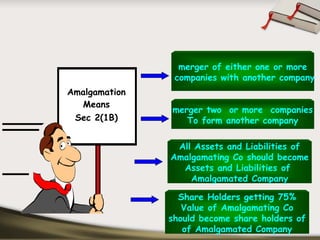

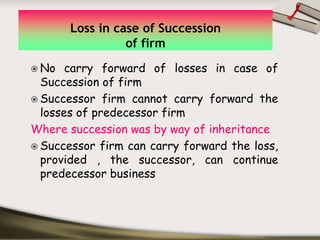

![Cost of Asset -Sec 43 Actual Cost of Asset -Sec 43

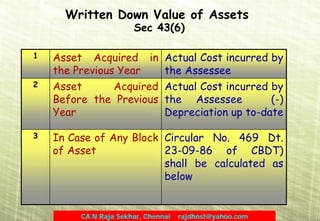

S Situation Actual Cost

No

8 Transfer of assets in Actual Cost will be.

between holding and W.D. V. to the

100% subsidiary company transferor company.

by each Other

9 Assets transferred Actual Cost i.e. W.D.V.

under a scheme of to the amalgamating

amalgamation [being company.

Indian Co(s)].

10 Asset acquired on W.D. V. in the hands of

partition of H.U.F. coparceners which would

have been if the

partition would not taken](https://image.slidesharecdn.com/incometax-100624010225-phpapp02/85/Income-tax-130-320.jpg)

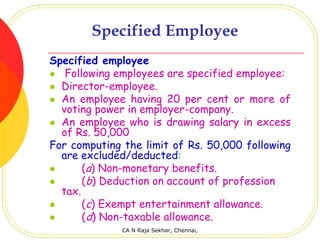

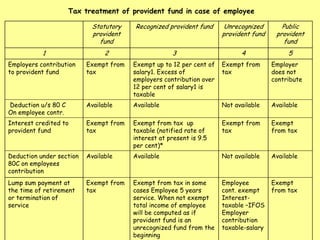

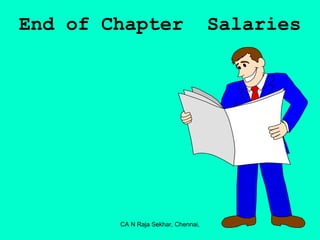

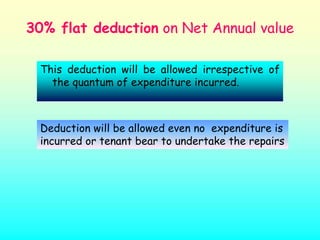

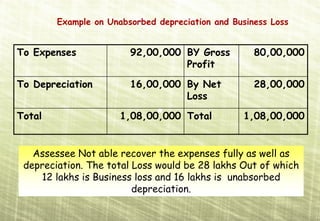

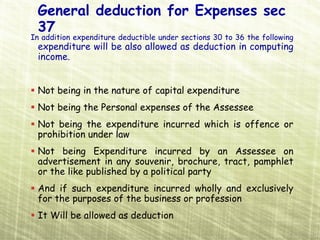

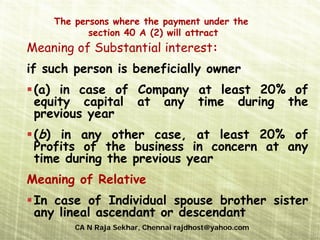

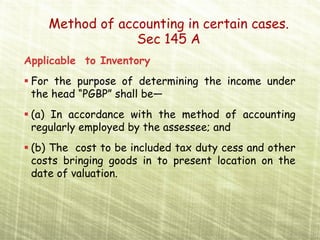

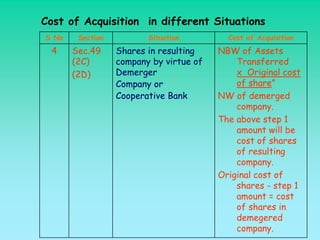

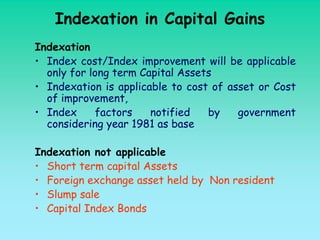

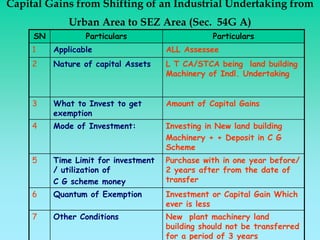

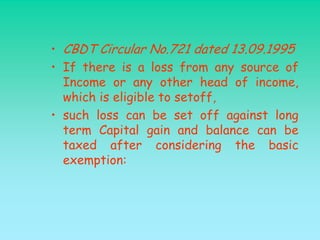

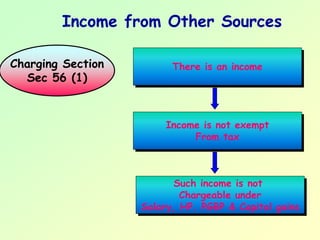

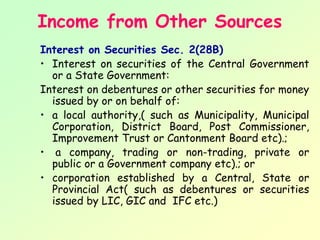

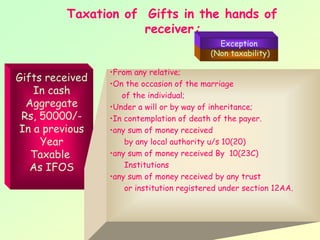

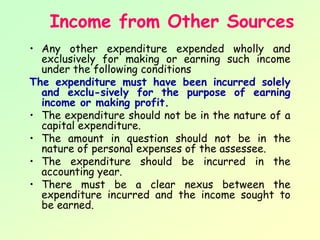

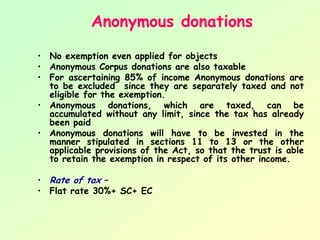

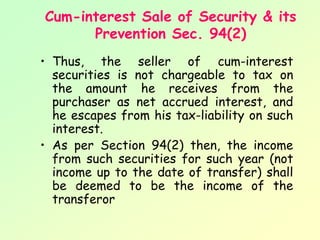

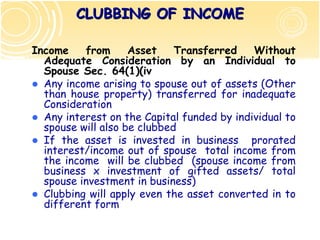

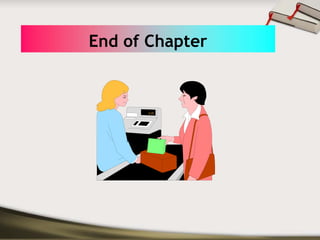

![Income from Other Sources

• Interest on cumulative deposit schemes of

private sector undertakings should be taxed on

accrual basis annually.Circular:No.409[F.No. 178

/ 2/85-IT(A-I)],dated12-2-85.

• Gross dividend is taxable –

• The gross dividend (net dividend plus the tax

deducted at source) receivable by the

registered shareholder on behalf of the

beneficial shareholder will be assessed in the

hands of the latter as ‘income from other

sources’ in the year in which it is declared,

distributed or paid. Circular : No. 3 dated 30-3-

1967. Circular : No. 648, dated 30-3-1993.](https://image.slidesharecdn.com/incometax-100624010225-phpapp02/85/Income-tax-296-320.jpg)

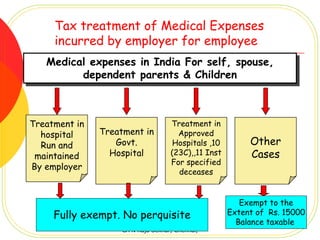

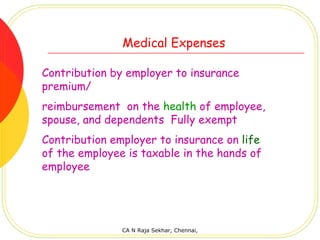

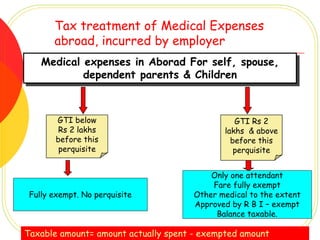

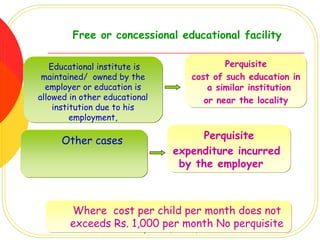

This document discusses topics related to income tax, including heads of income, clubbing of income, and set off and carry forward. It covers all amendments made up to the 2008 Finance Act. The author aims to upload case studies to help final year students and disclaims any responsibility for errors, though every effort was made to avoid them. Medical expenses incurred by an employer for an employee's treatment are exempt up to certain limits depending on where the treatment occurs and the employee's gross total income.