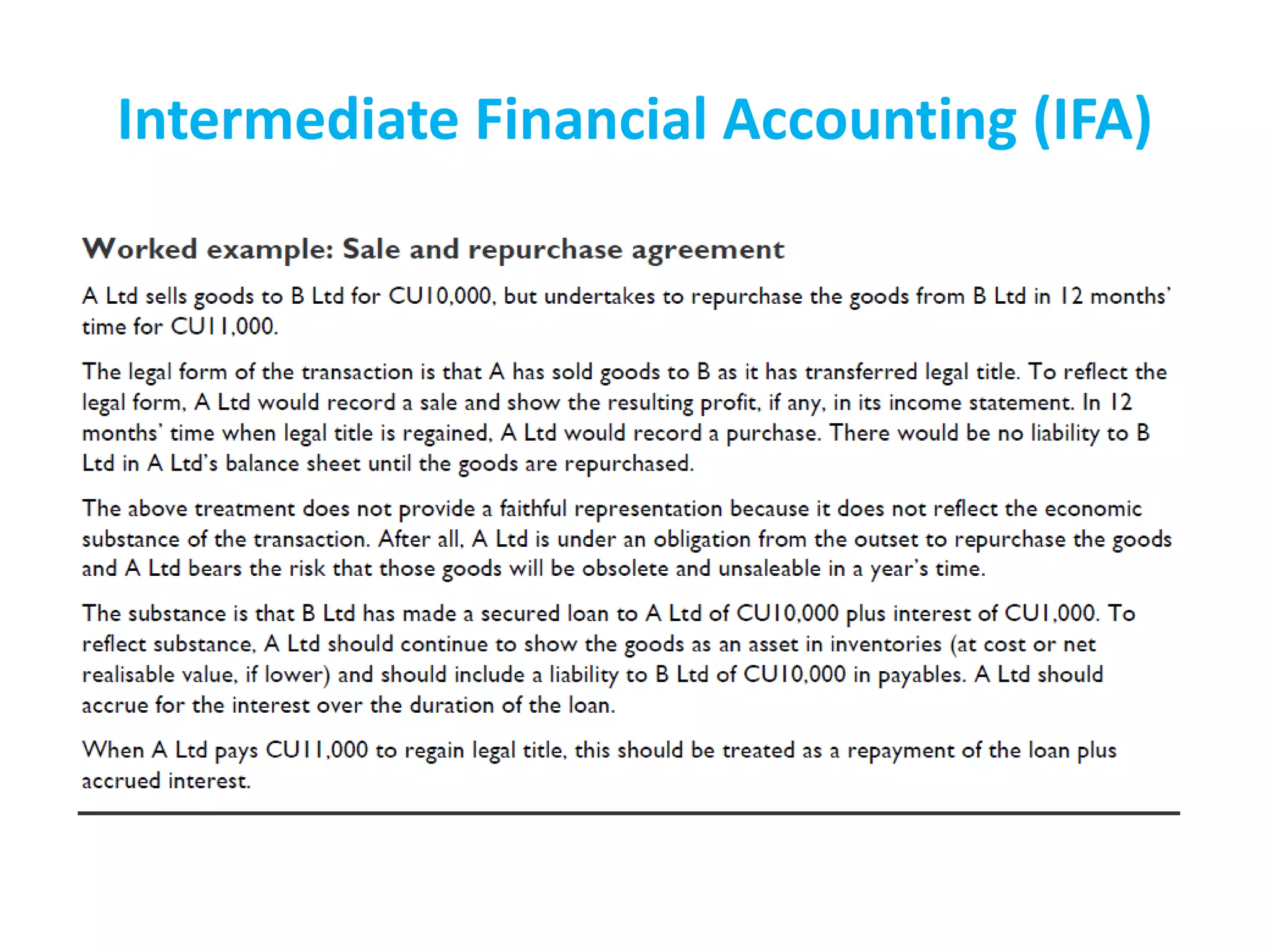

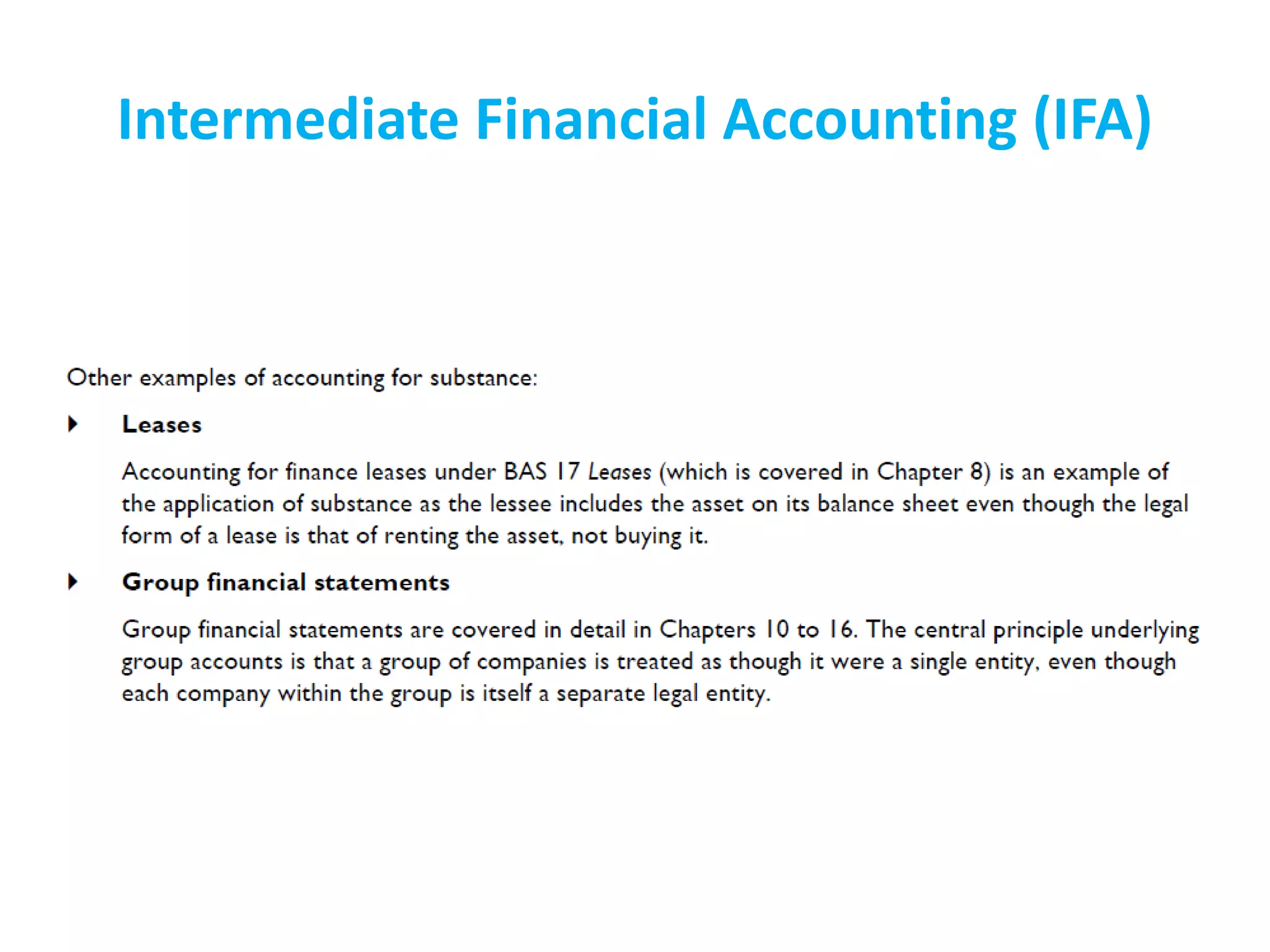

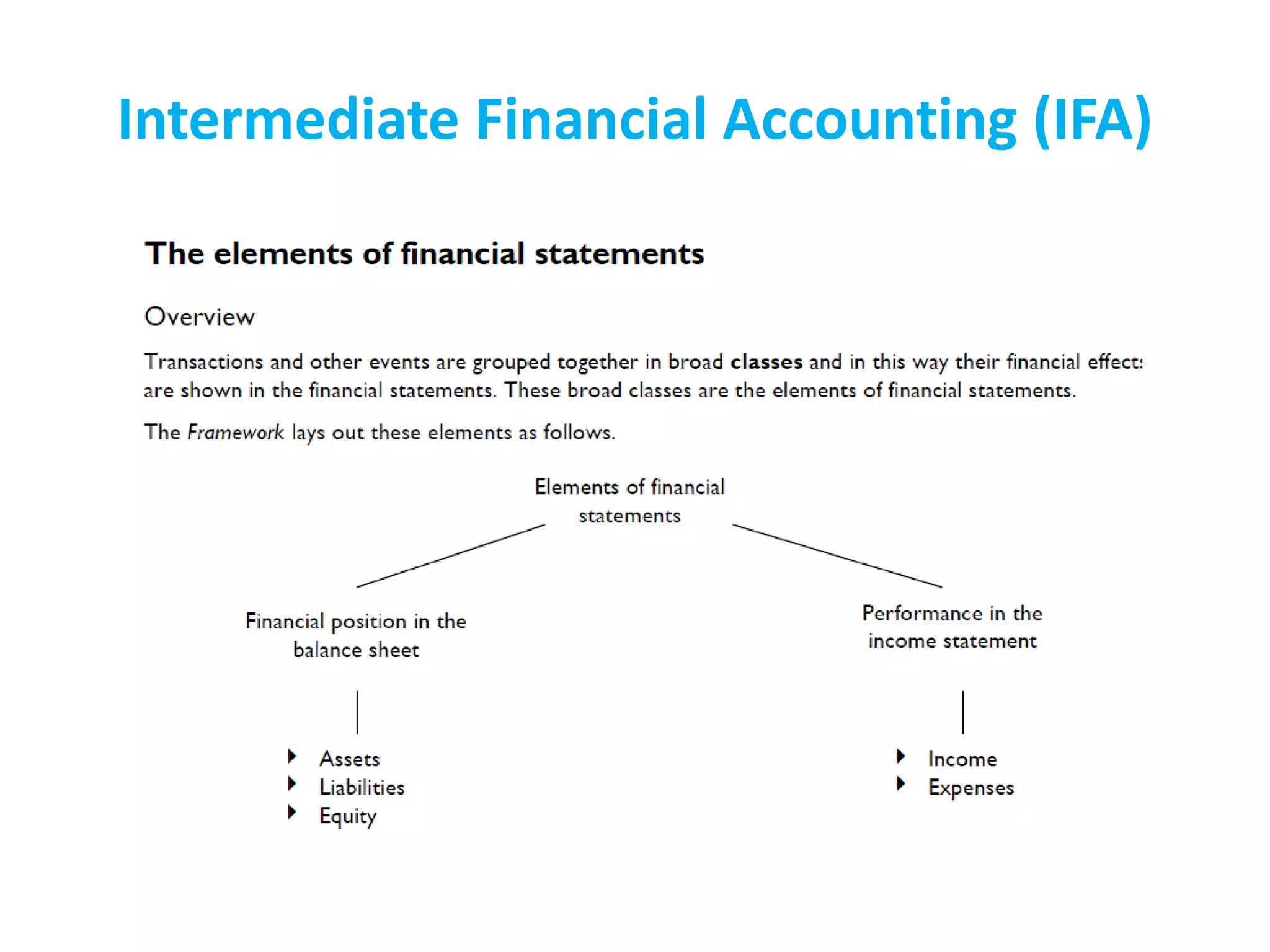

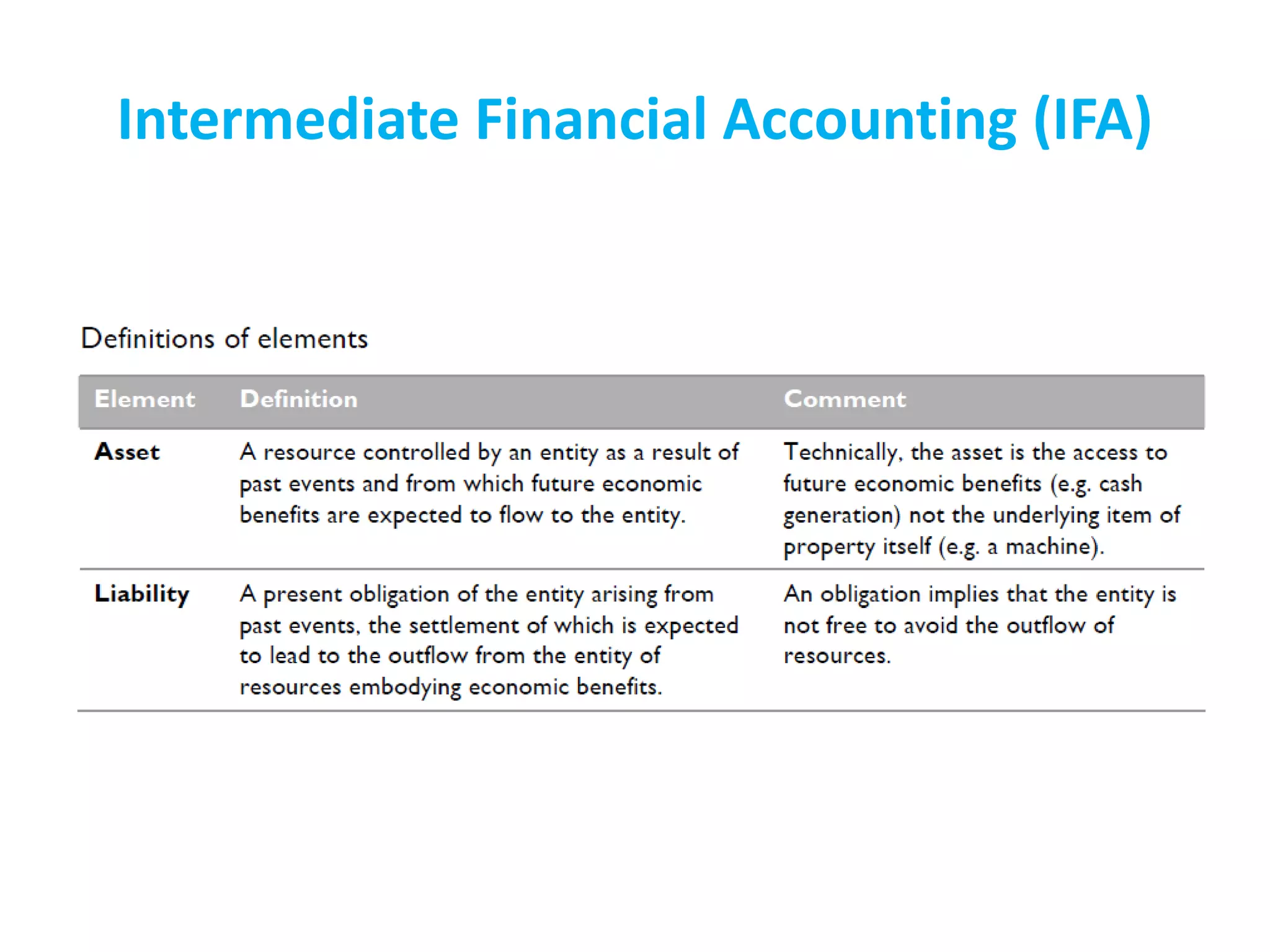

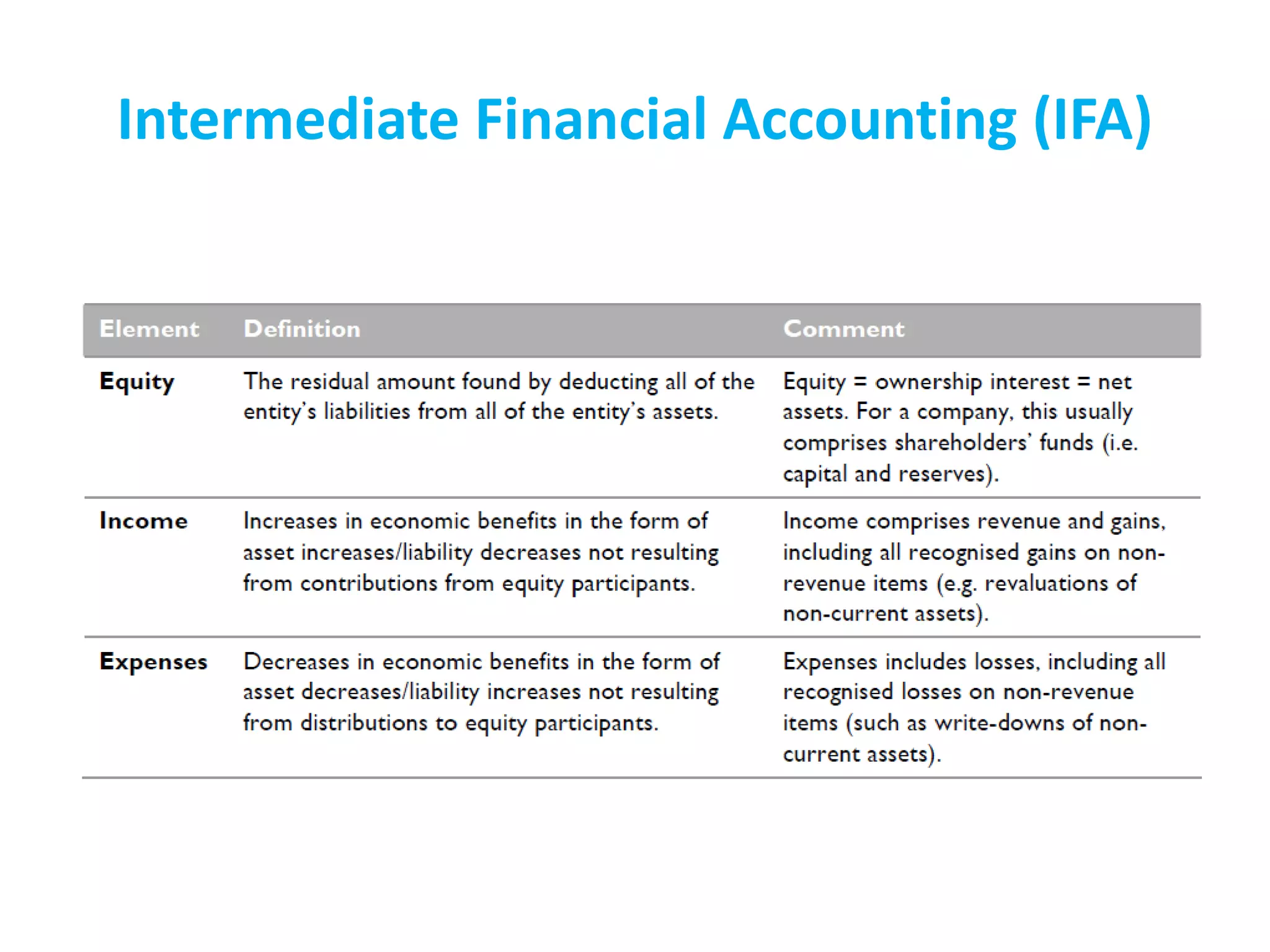

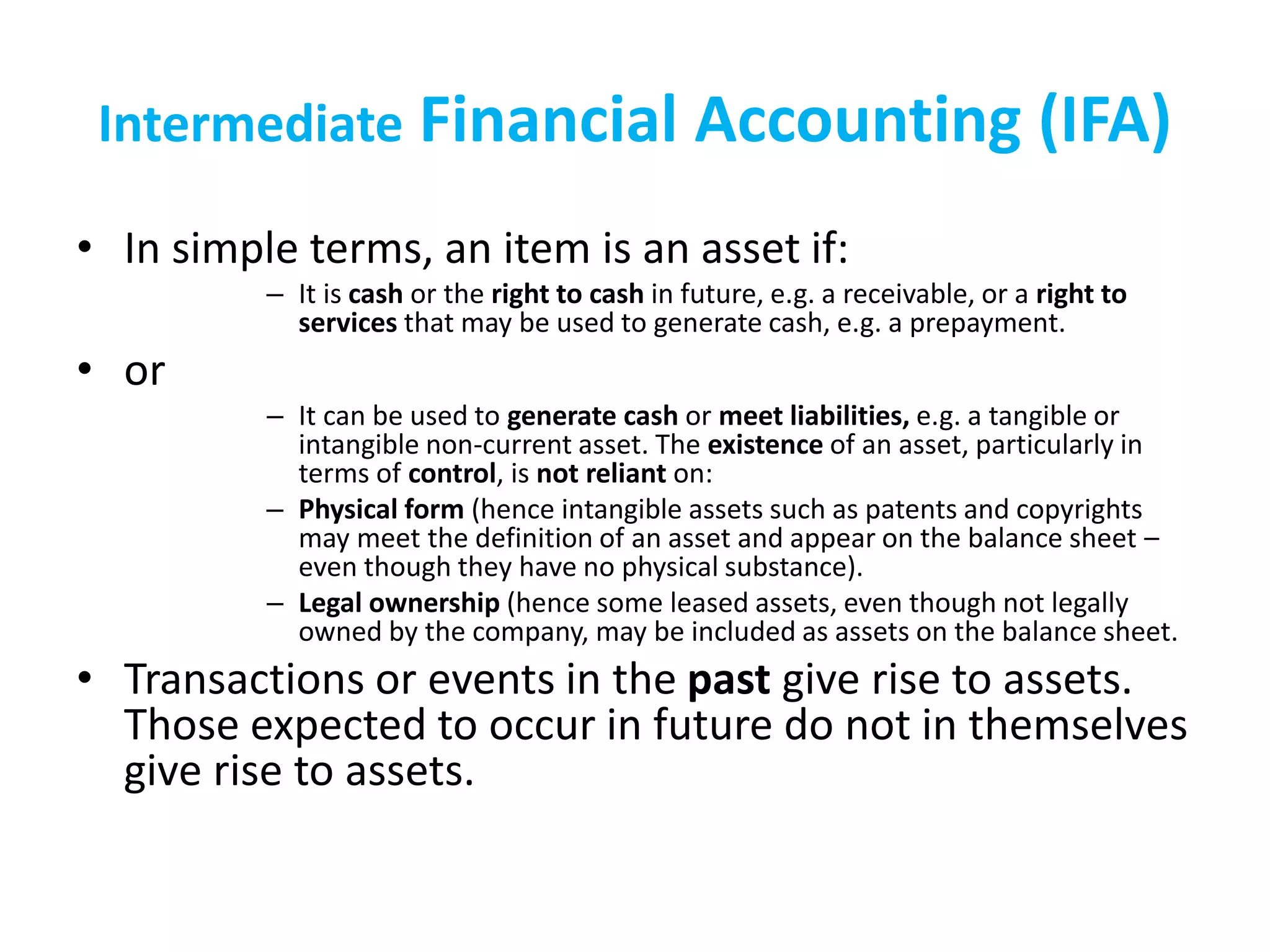

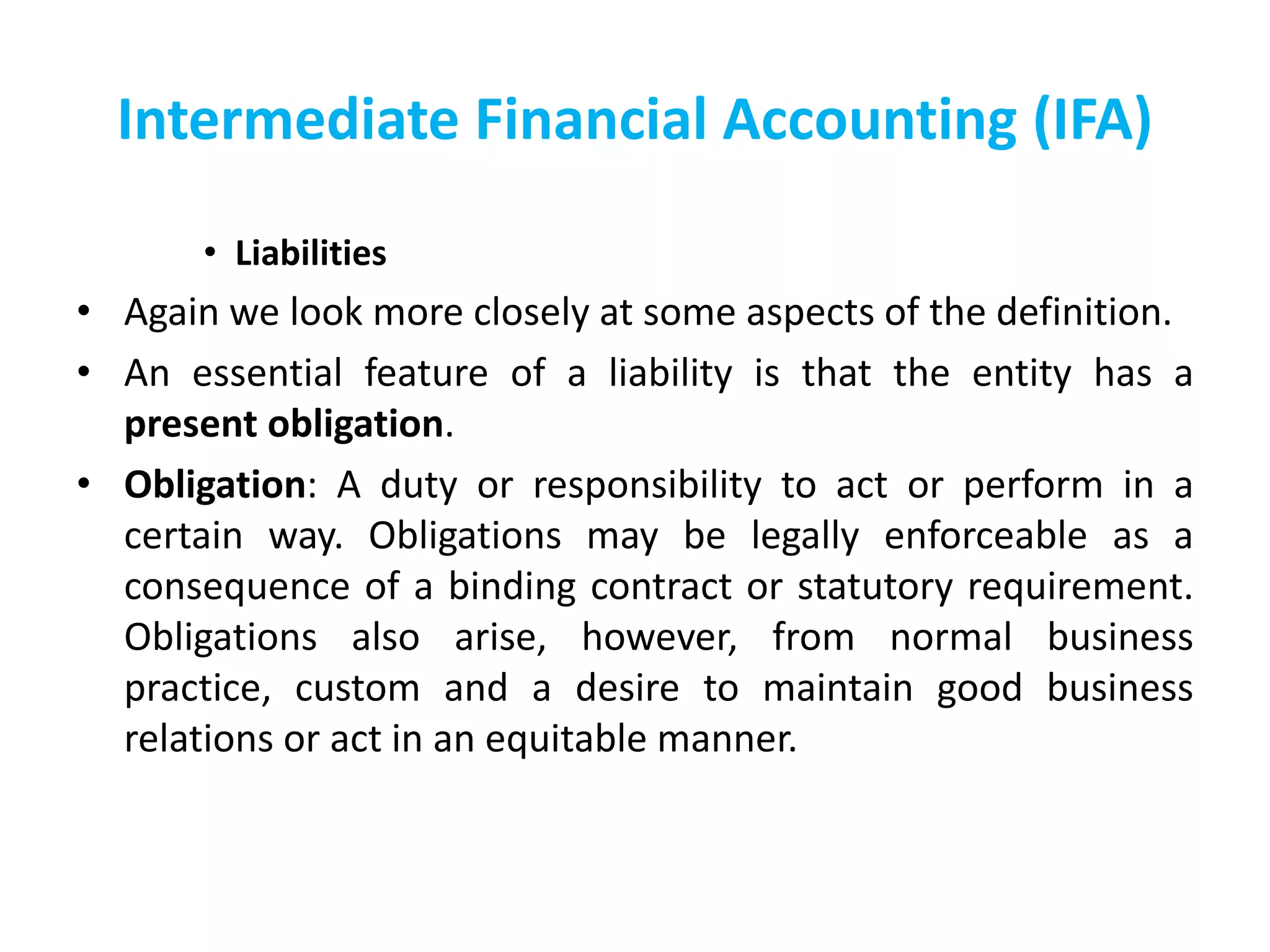

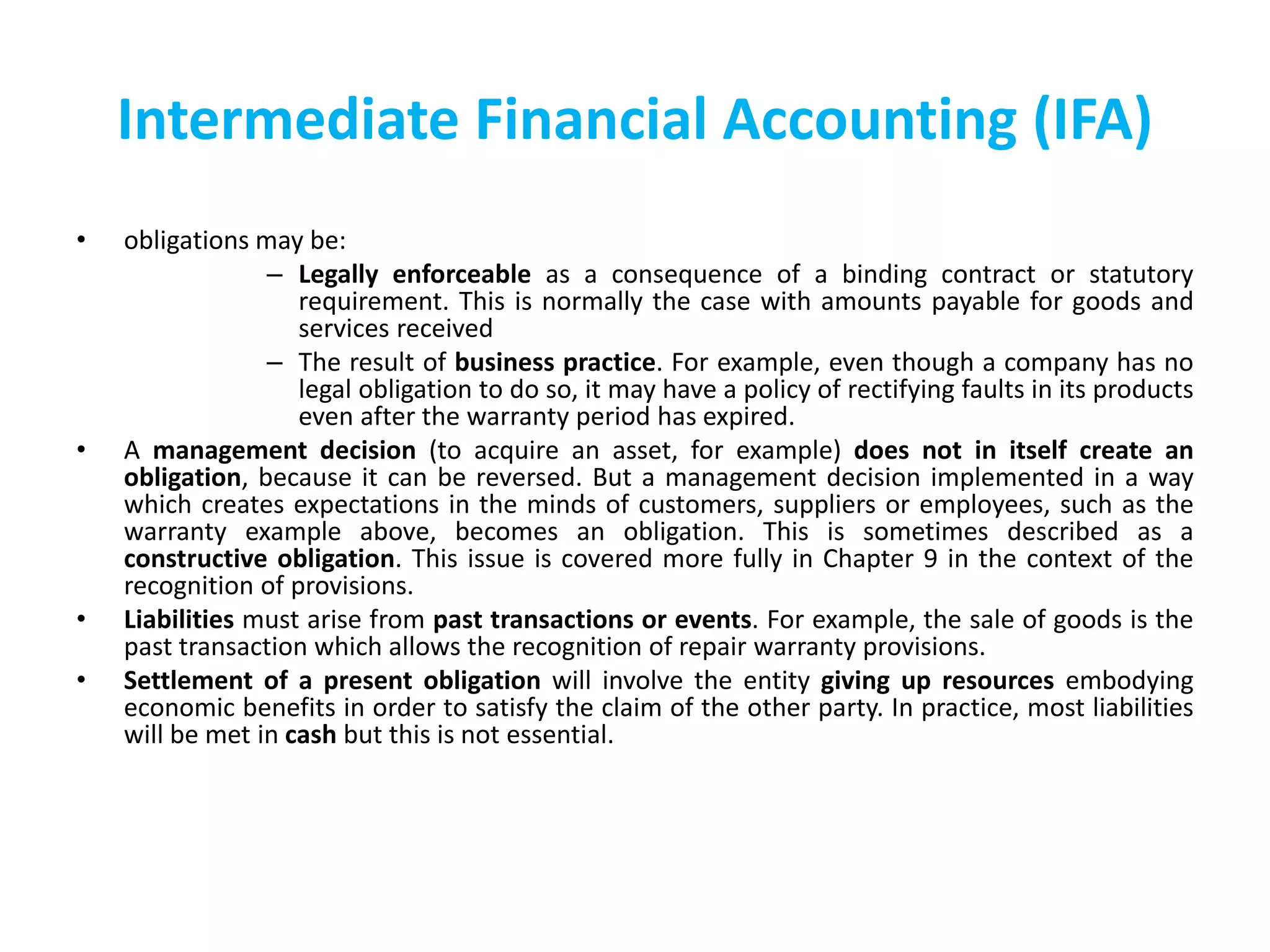

This document discusses key concepts in intermediate financial accounting, including the qualitative characteristics of useful financial information. It explains that substance over form, neutrality, prudence, completeness, comparability, timeliness, understandability, and relevance are important qualities of reliable financial reporting. The document also defines assets as future economic benefits controlled by the entity, and liabilities as present obligations arising from past events that will require settlement through an outflow of resources. Key aspects of assets and liabilities are described in further detail.