Download to read offline

![Infosys.

Key facts from Management Interview;

■ Management upgraded its earning guidance for FY14E from 9-10% to 11.5-12%. This

guidnace means the company only has to achieve flat growth in the fourth quarter to

meet the projection.

■ With 85% of the company’s revenues coming from clients based in US and Europe, the

company should hope the current economic recovery in developed countries would help

its revenues.

■They are seeing confidence coming back from client’s metrics. However, they expect

[their] budgets only remain stable from last year. Clients are still focused on cost.

■ The Company is looking to bring in about maximum 6,000 off-campus offers starting

late January early February, so there is a lot of activity going on that is bringing people in,

engaging and developing.

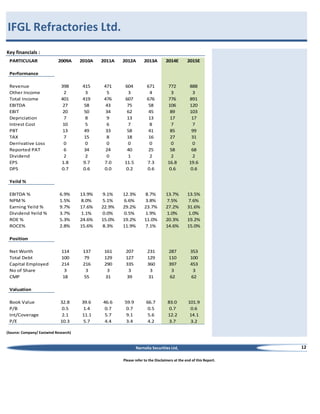

Financials

Rs in Cr,

Sales, INR

Employee Cost

Other expenses

Total Expenses

EBITDA

Depreciation

Other Income

EBIT

Interest Cost

PBT

Tax

PAT

Growth-%

Sales

EBITDA

PAT

Margin -%

EBITDA

EBIT

PAT

Expenses on Sales-%

Employee Cost

Other expenses

Tax rate

Valuation

CMP

No of Share

NW

EPS

BVPS

RoE-%

Dividen Payout ratio

P/BV

P/E

FY10

22742

12085

2792

14877

7865

905

982

7942

0

7942

1681

6261

FY11

27501

14856

3677

18533

8968

854

1211

9325

0

9325

2490

6835

FY12

33734

18340

4671

23011

10723

928

1904

11699

0

11699

3367

8332

FY13

40352

22565

6254

28819

11533

1099

2365

12799

0

12799

3370

9429

FY14E

50330

28185

8556

36741

13589

1371

2567

14785

0

14785

3992

10793

FY15E

59631

33691

10734

44425

15206

1624

3578

17160

0

17160

4633

12527

4.8%

9.3%

4.6%

20.9%

14.0%

9.2%

22.7%

19.6%

21.9%

19.6%

7.6%

13.2%

24.7%

17.8%

14.5%

18.5%

11.9%

16.1%

34.6%

34.9%

27.5%

32.6%

33.9%

24.9%

31.8%

34.7%

24.7%

28.6%

31.7%

23.4%

27.0%

29.4%

21.4%

25.5%

28.8%

21.0%

53.1%

12.3%

21.2%

54.0%

13.4%

26.7%

54.4%

13.8%

28.8%

55.9%

15.5%

26.3%

56.0%

17.0%

27.0%

56.5%

18.0%

27.0%

2615

57.4

23049.0

109.1

401.7

27.2%

25.1%

6.5

24.0

2765

57.4

25976.0

119.0

452.4

26.3%

45.9%

6.1

23.2

2865

57.4

31332.0

145.1

545.6

26.6%

24.0%

5.3

19.7

2400

57.4

37994.0

164.2

661.7

24.8%

45.1%

3.6

14.6

3793

57.4

45629.8

188.0

794.7

23.7%

23.0%

4.8

20.2

3793

57.4

54797.5

218.2

954.3

22.9%

19.8%

4.0

17.4

(Source: Company/Eastwind)

Narnolia Securities Ltd,

Please refer to the Disclaimers at the end of this Report.

9](https://image.slidesharecdn.com/iea5-140304231641-phpapp01/85/India-Equity-Analytics-Buy-stock-of-Eros-Media-and-Escorts-Ltd-9-320.jpg)

Escorts reported strong tractor volume growth in February 2014, with domestic sales up 6.8% YoY to 4,581 tractors. The company remains positive on growth prospects in FY2014 and beyond, expecting demand to improve with economic recovery. While cautious on the construction equipment segment, analysts revised estimates and rating on Escorts from "Reduce" to "Buy" with a revised target price of Rs. 175. The positive tractor volume performance in CY2013 and expected further demand growth support maintaining a positive view on the stock.