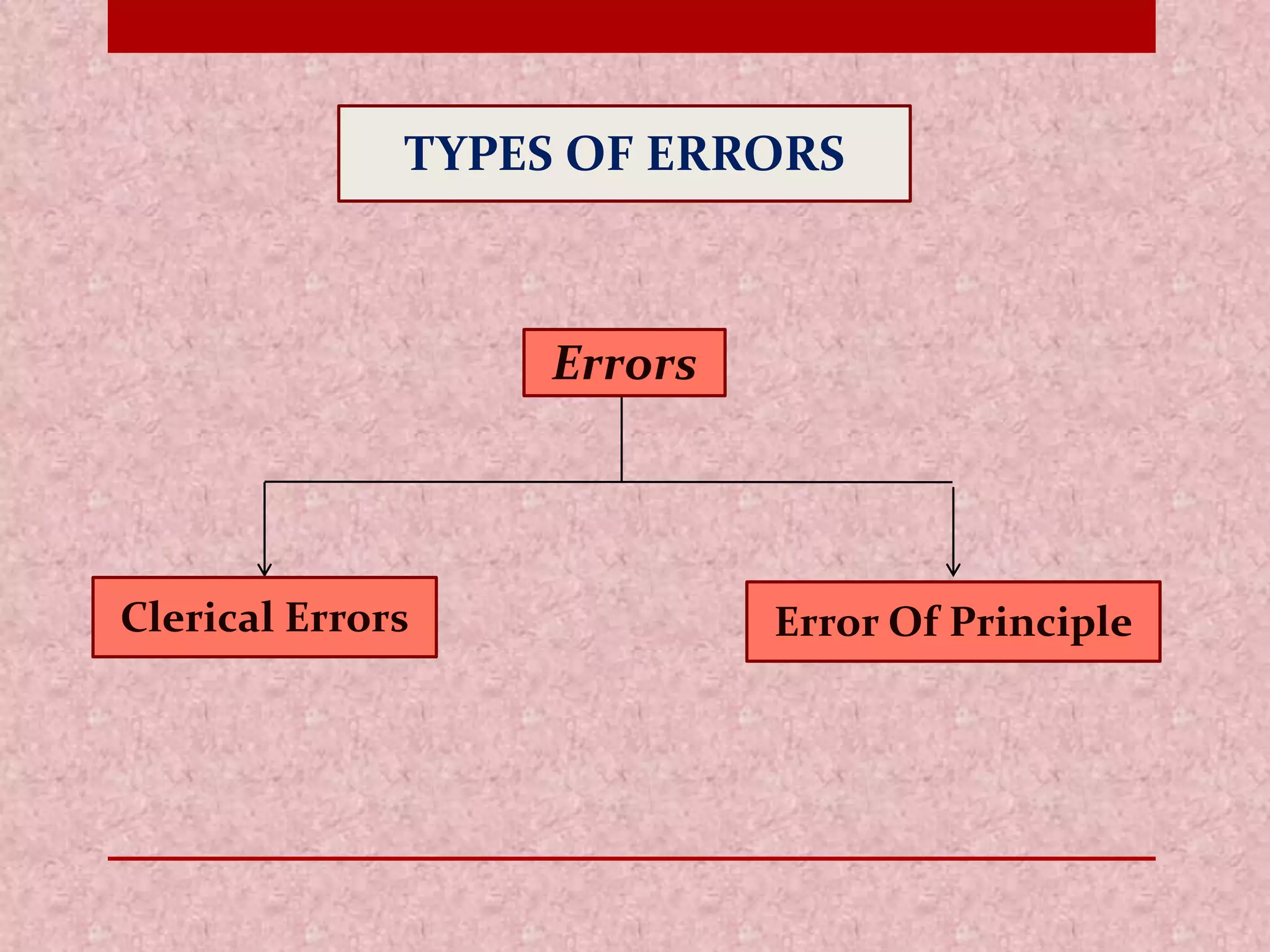

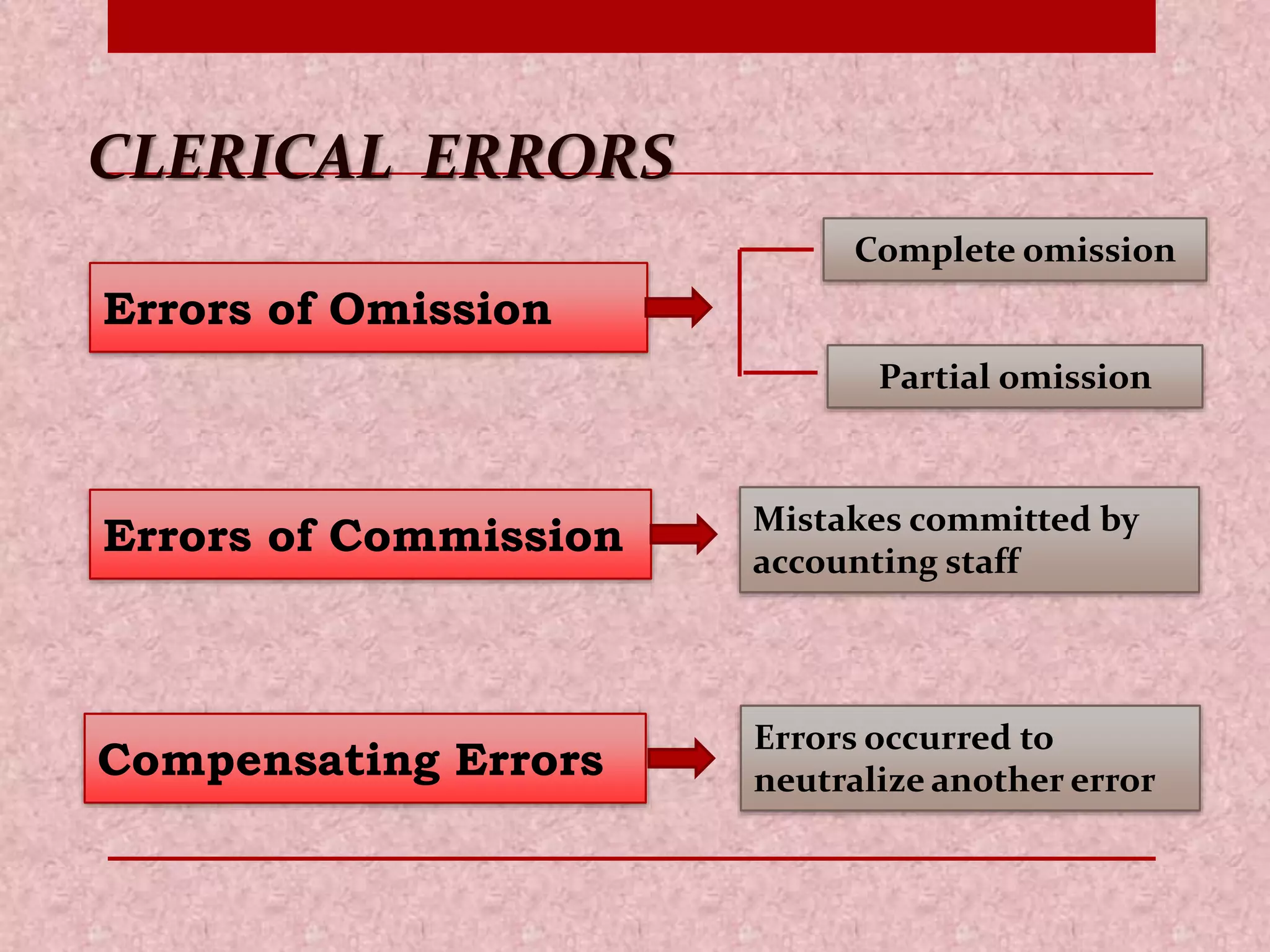

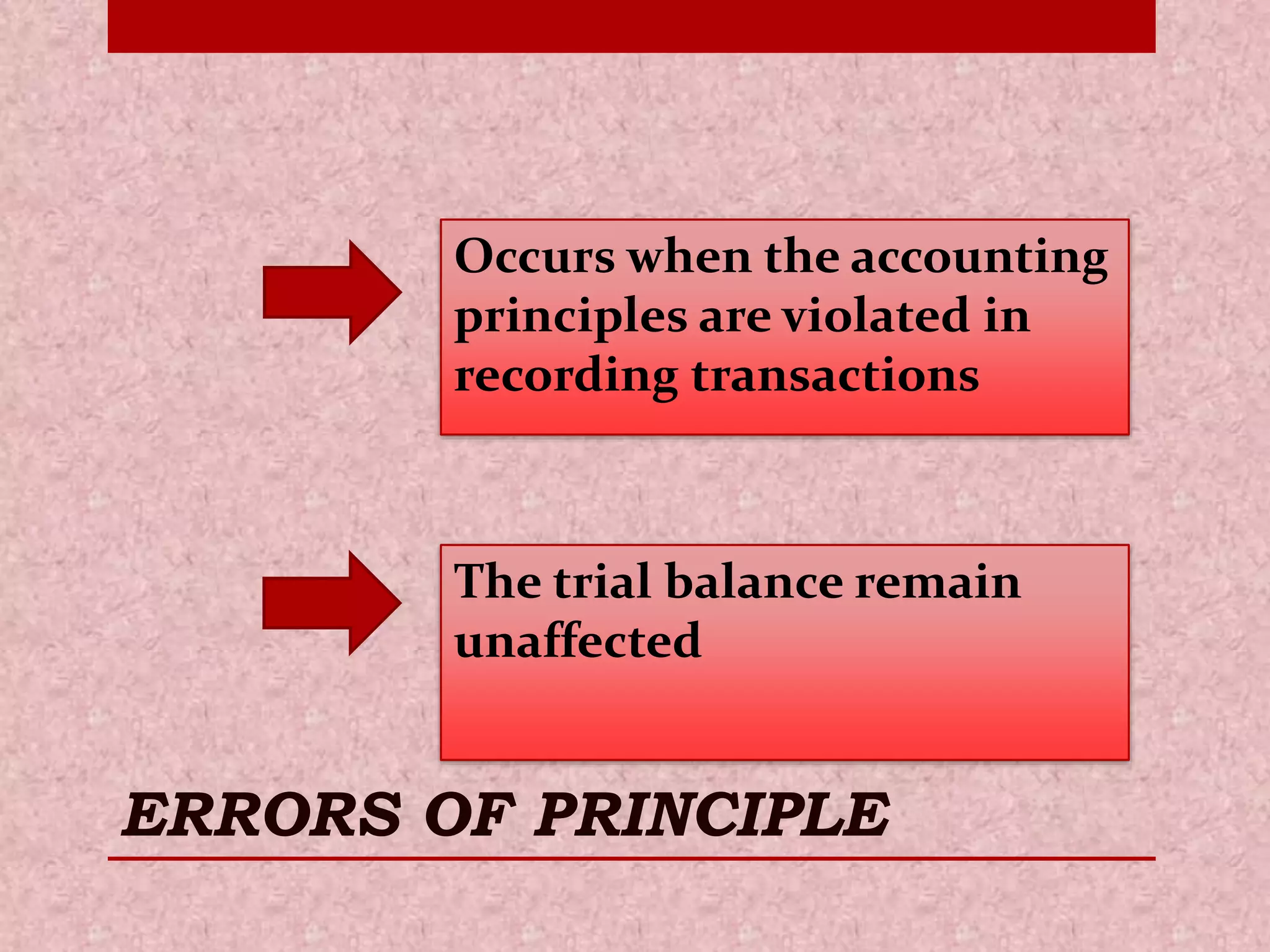

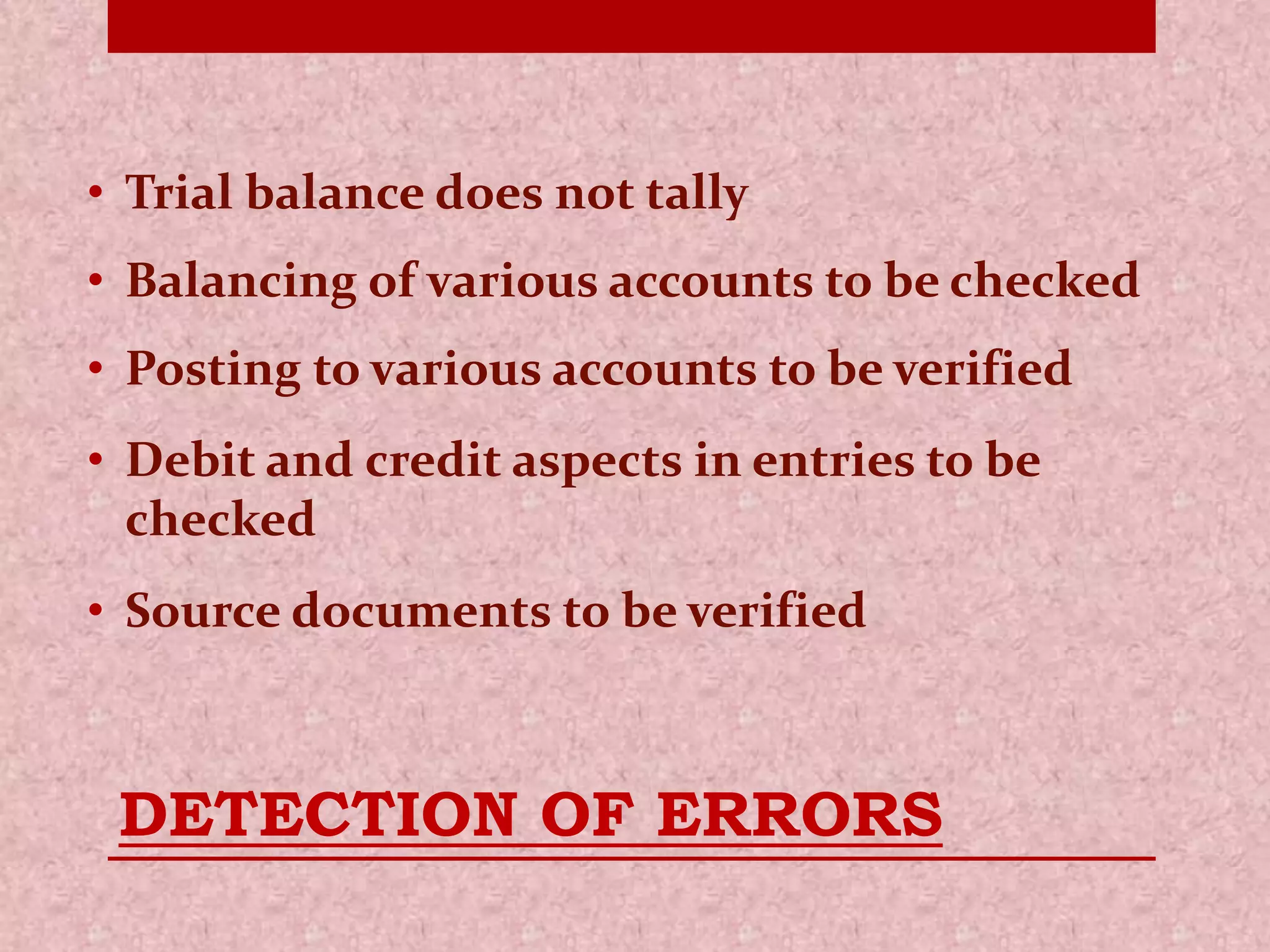

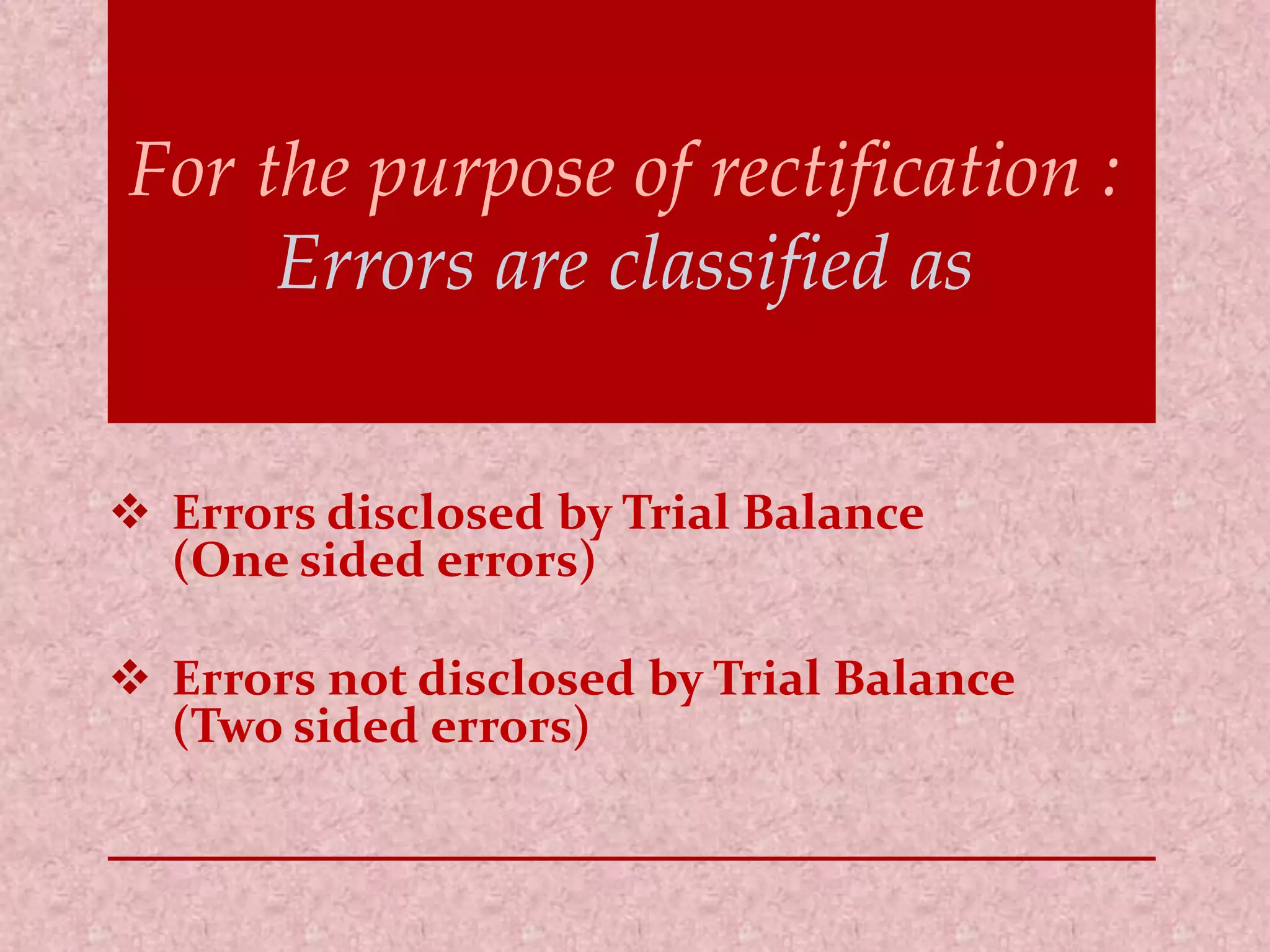

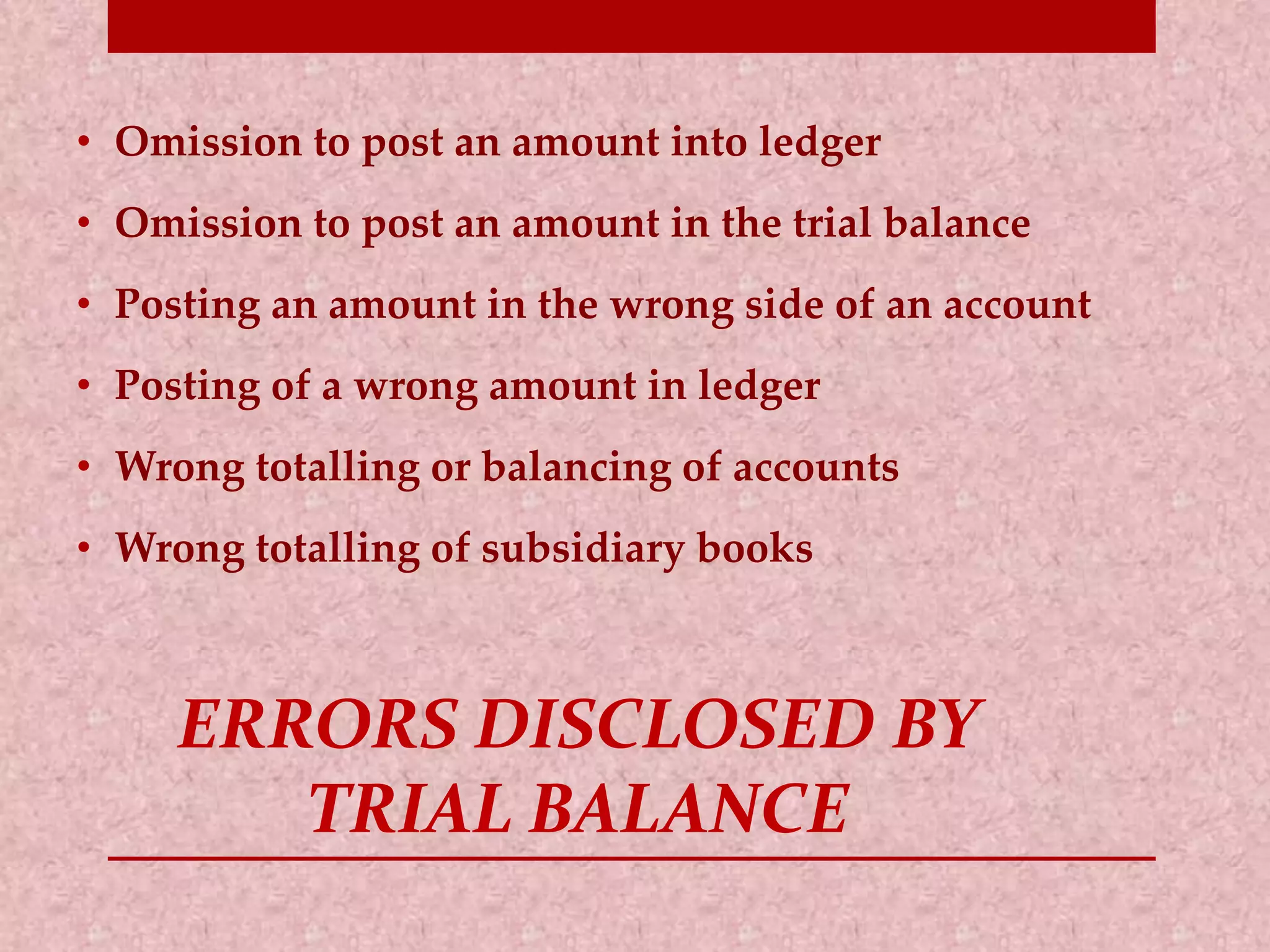

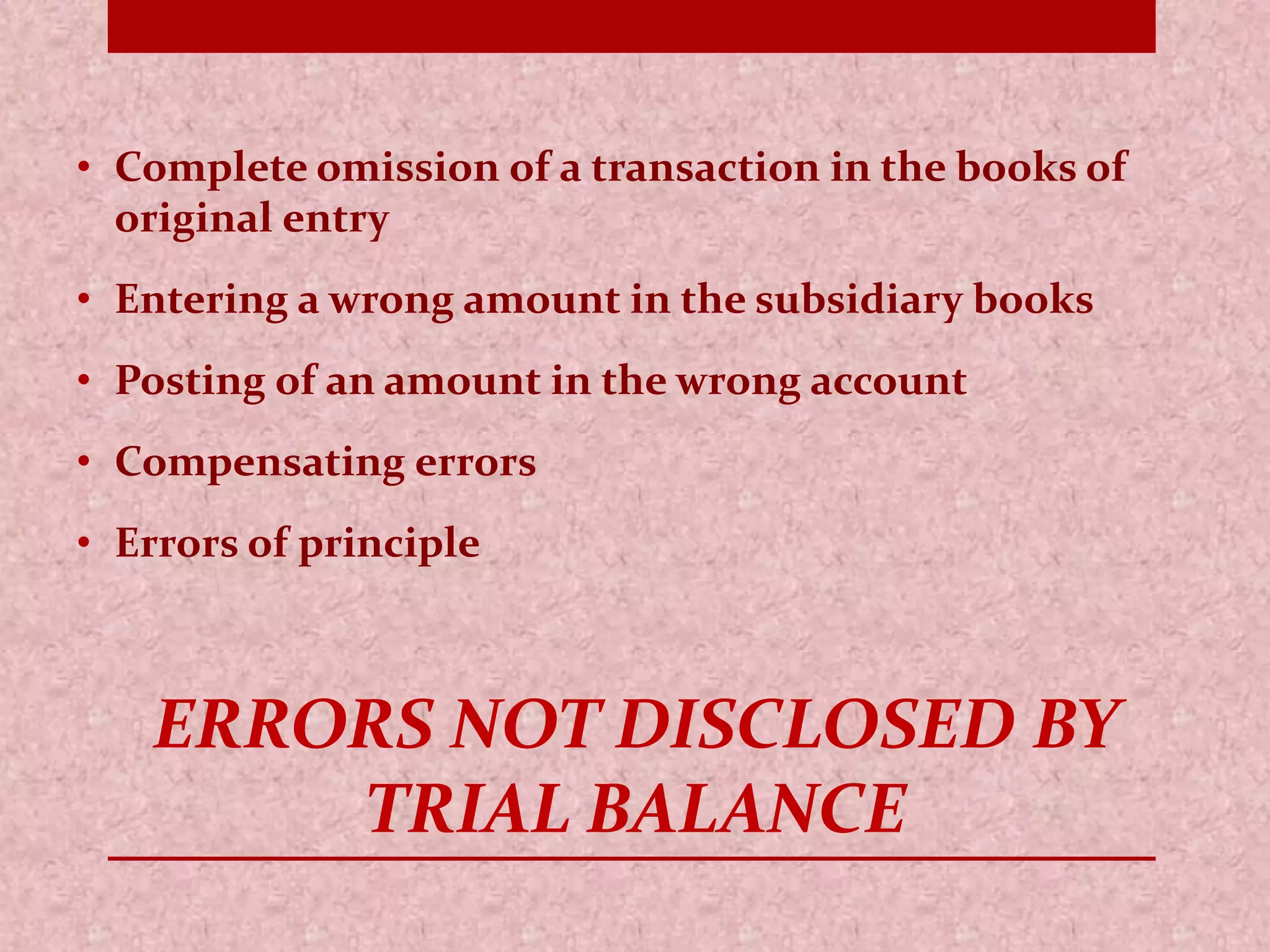

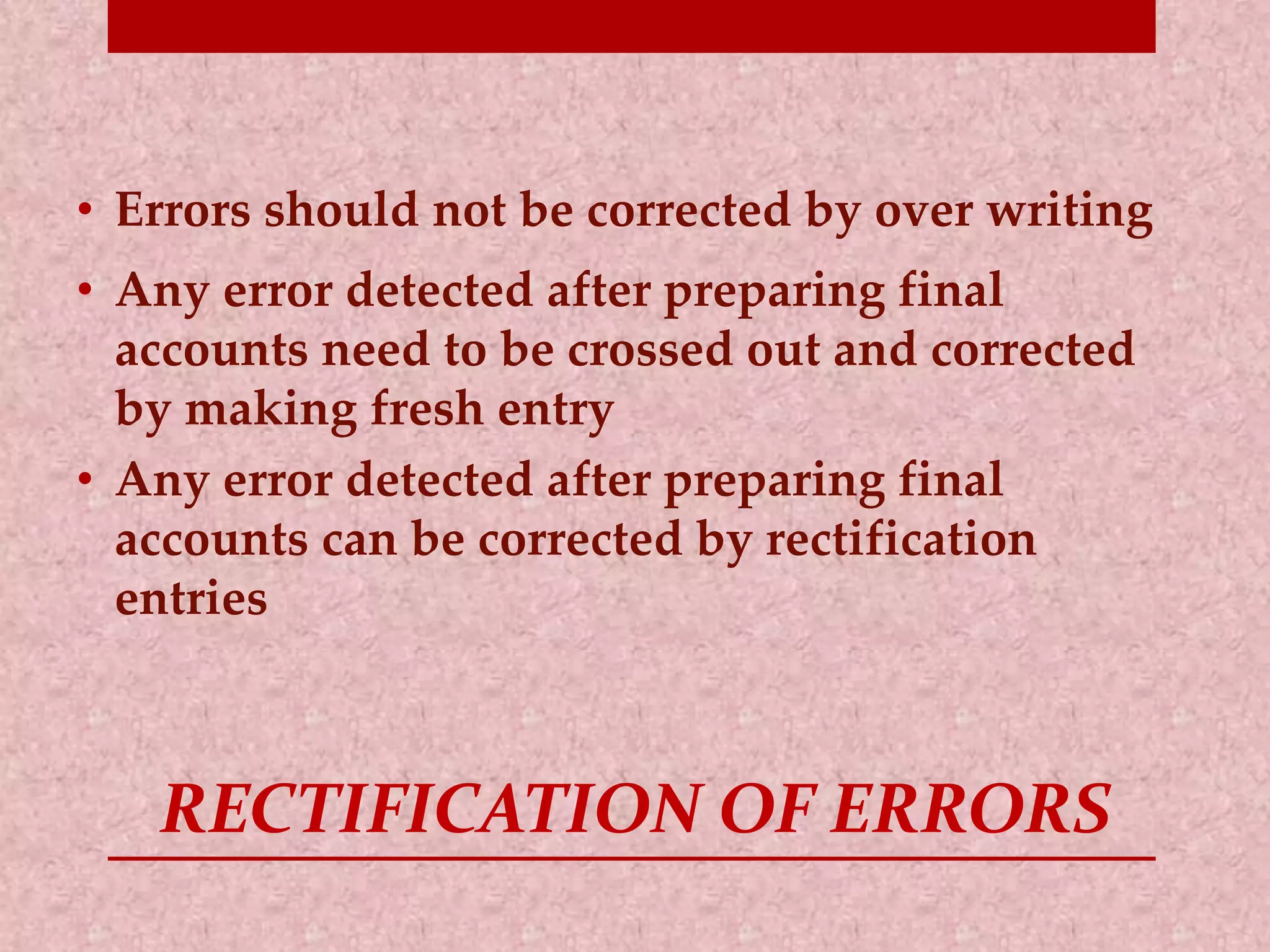

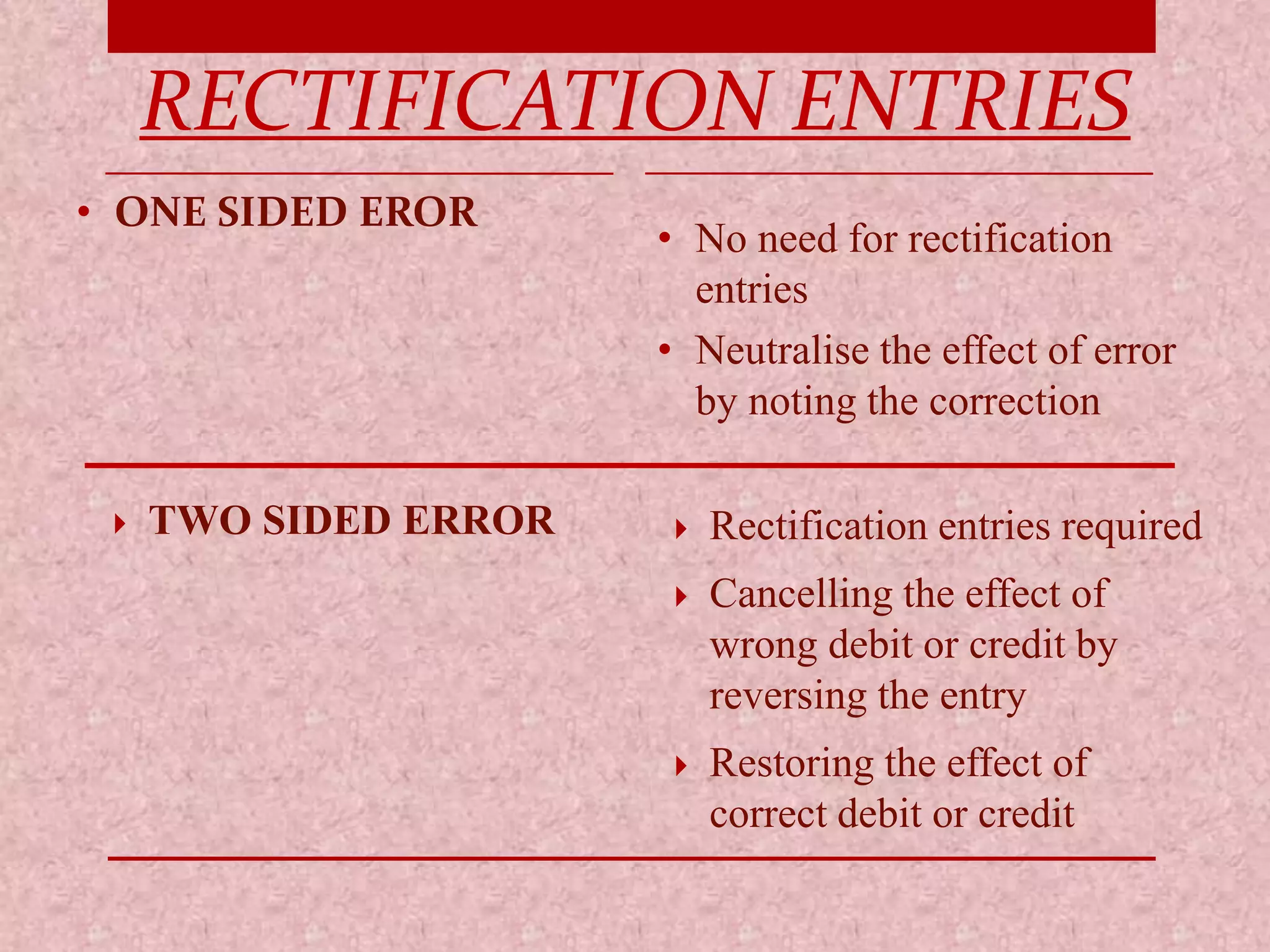

This document discusses the detection and rectification of accounting errors. It defines clerical errors and errors of principle. Clerical errors are errors of omission, commission, or compensation. Errors of principle occur when accounting principles are violated. Errors are classified as disclosed or not disclosed by the trial balance. Disclosed errors only affect one side, while undisclosed errors affect both sides. Rectification of errors involves reversing wrong entries and recording correct entries. Rectification entries are only needed for undisclosed two-sided errors.