Download to read offline

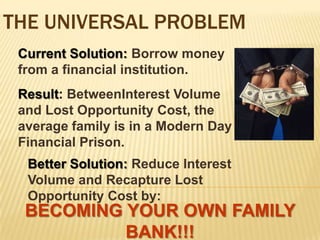

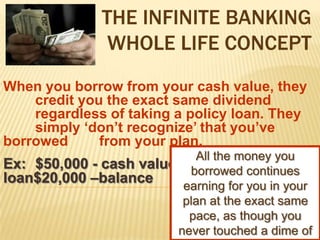

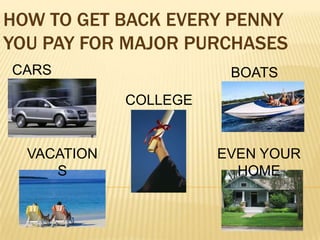

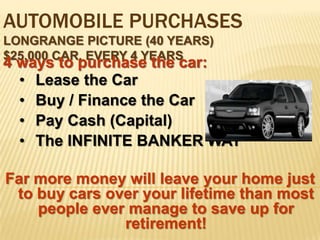

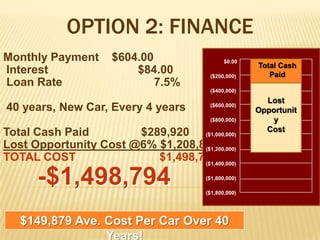

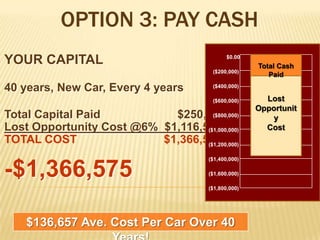

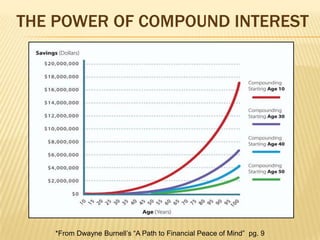

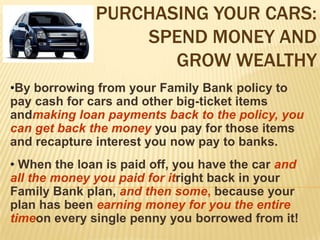

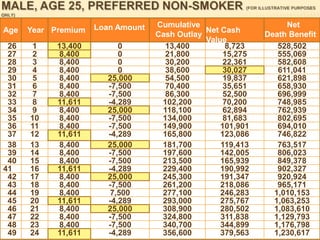

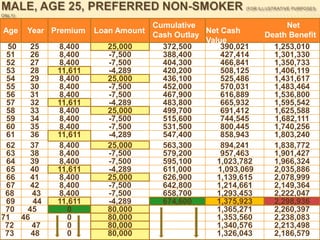

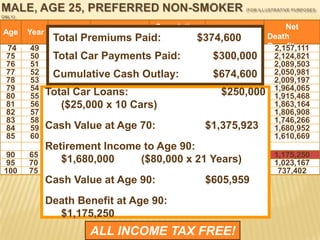

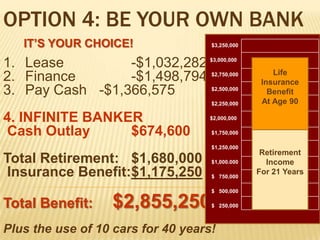

This document discusses the concept of "Infinite Banking" which is presented as a strategy for becoming your own bank through the use of whole life insurance policies. It notes some key benefits as becoming the banker, borrower, and depositor which eliminates risk and turns liabilities into assets. An illustration is provided showing how purchasing cars over 40 years through policy loans and repayments results in getting all money back plus interest earnings. The strategy is positioned as allowing one to fund major purchases like education and vacations while growing wealth over the long term in a tax-advantaged manner.

![Banking Strategies 8 09[1]](https://cdn.slidesharecdn.com/ss_thumbnails/bankingstrategies8091-12530535974621-phpapp03-thumbnail.jpg?width=640&height=640&fit=bounds)