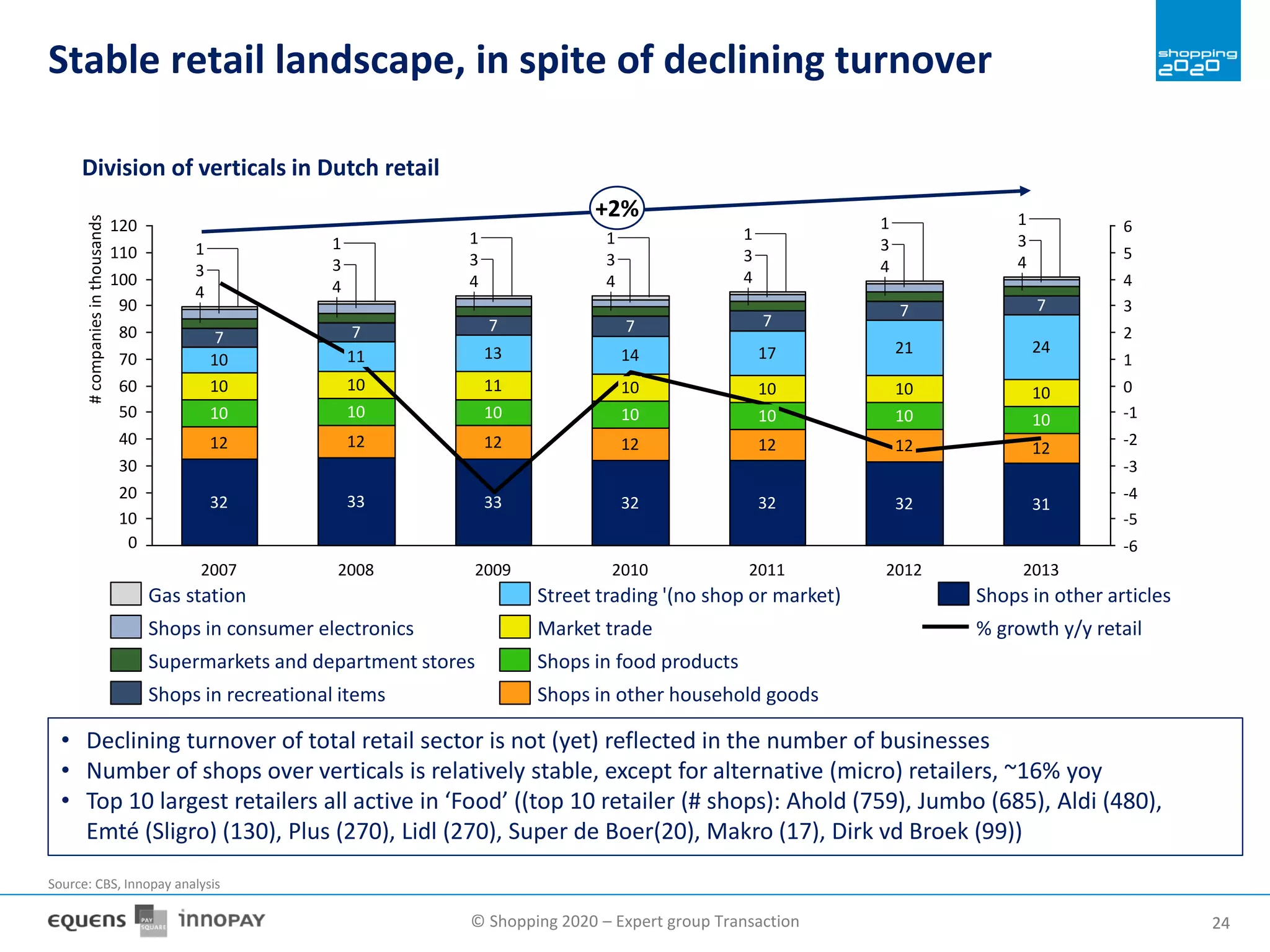

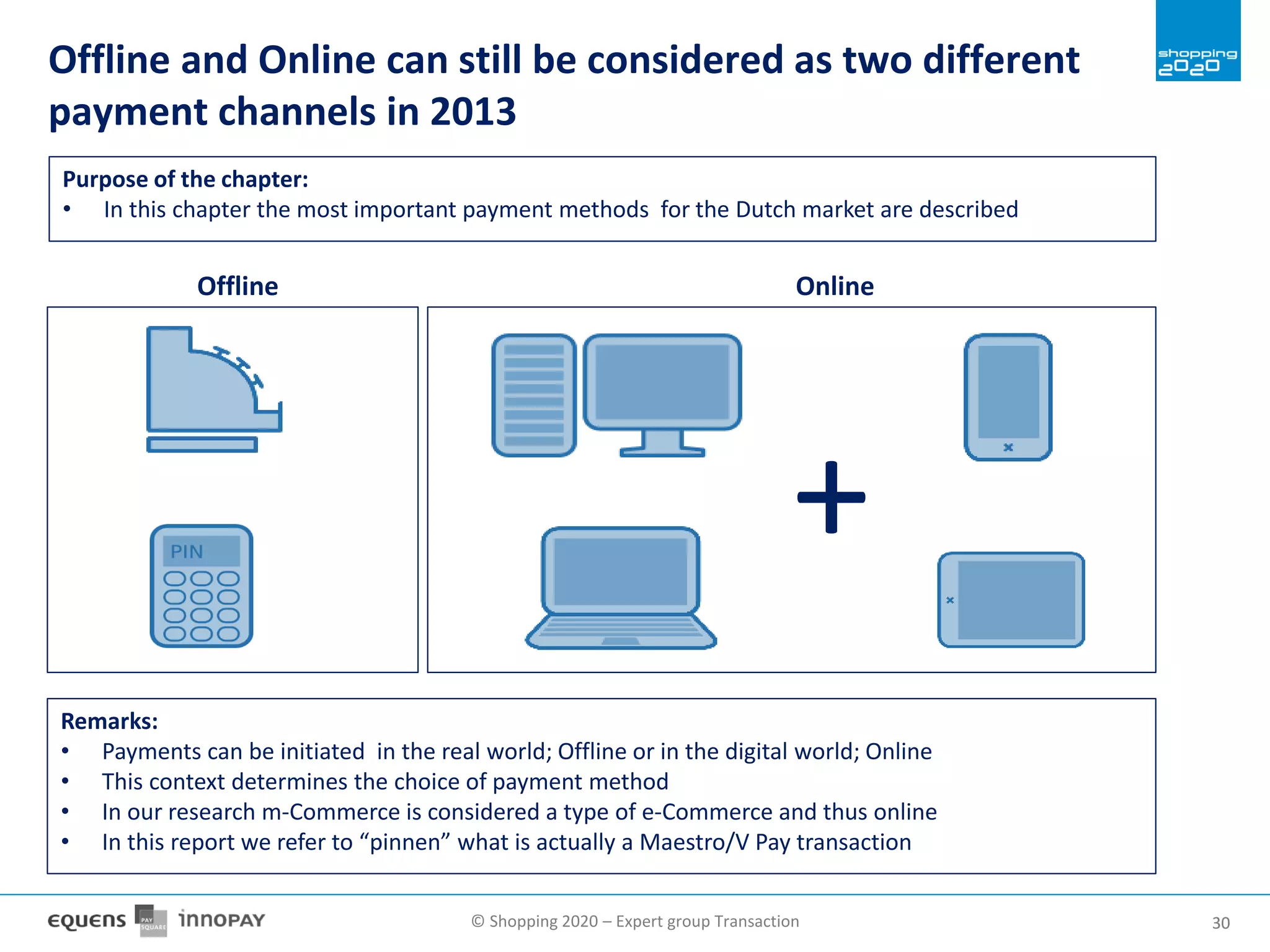

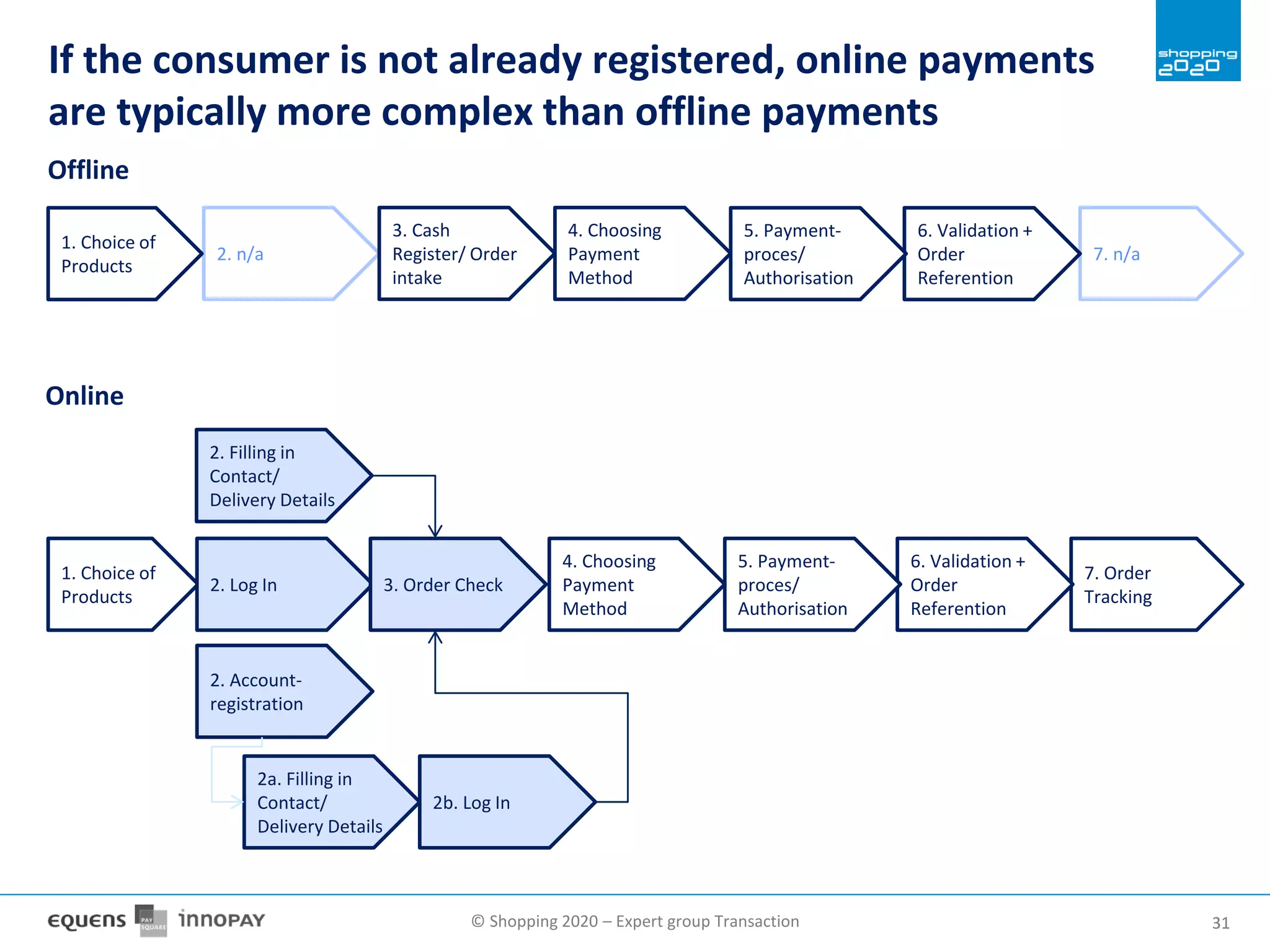

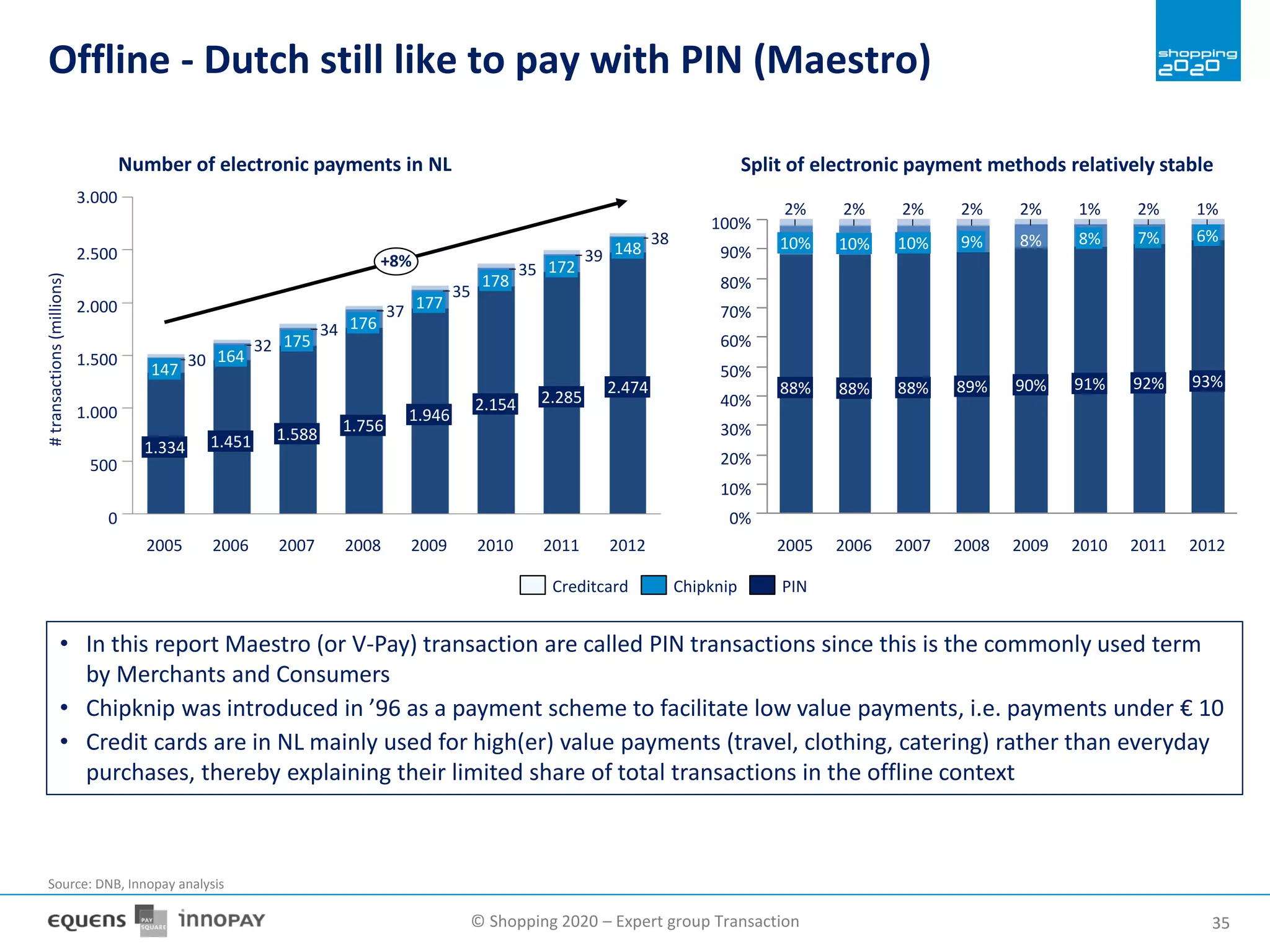

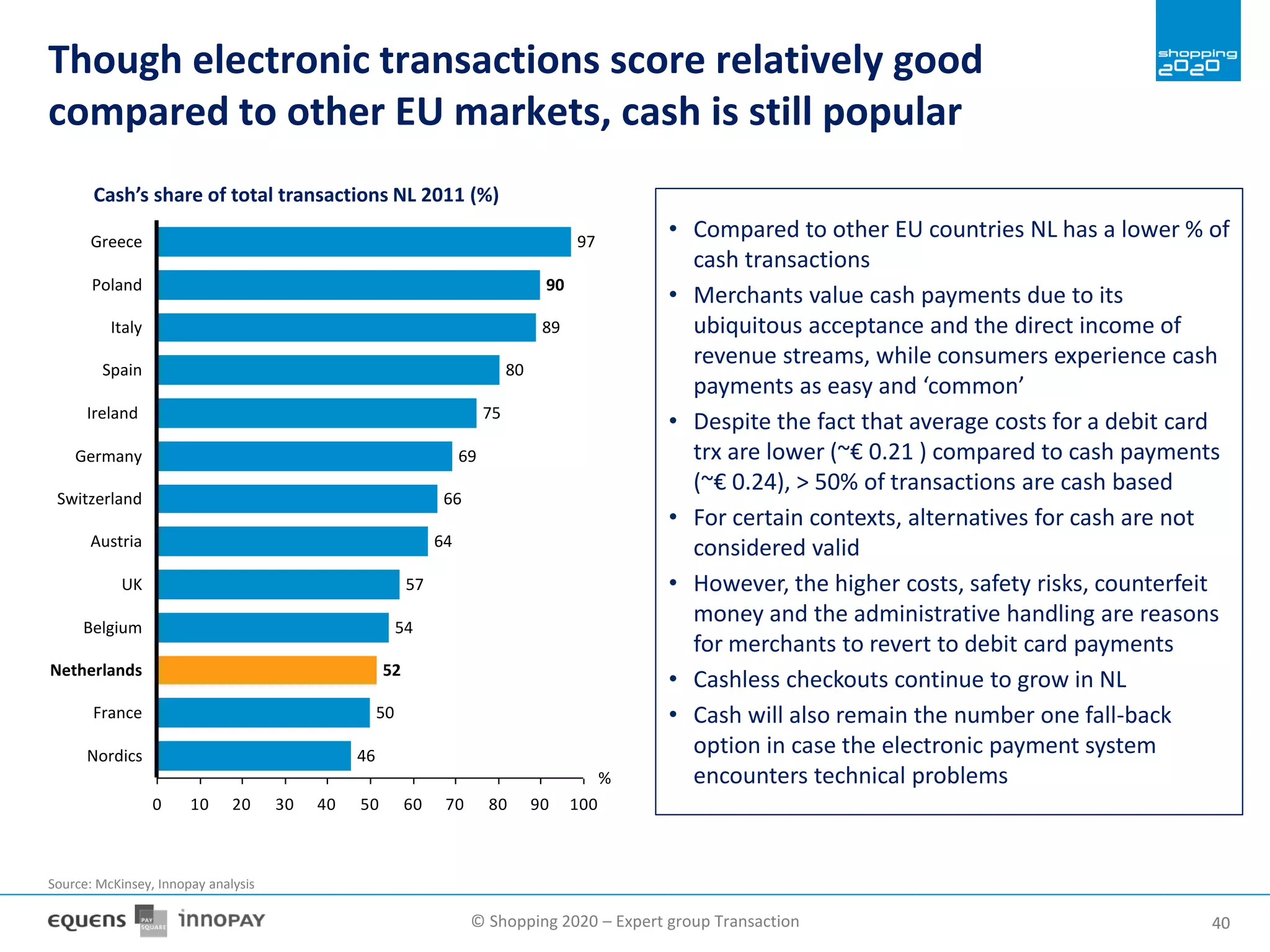

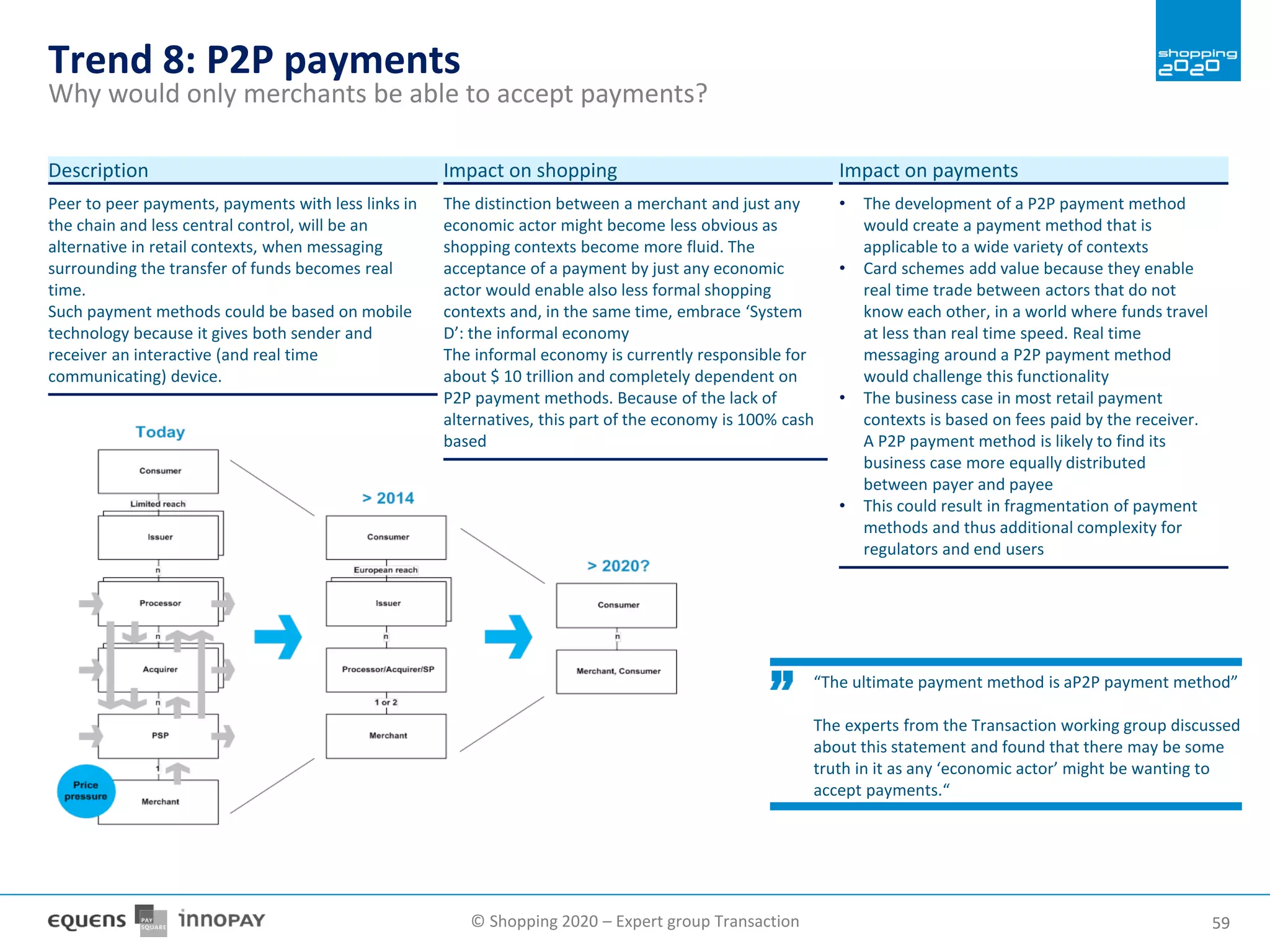

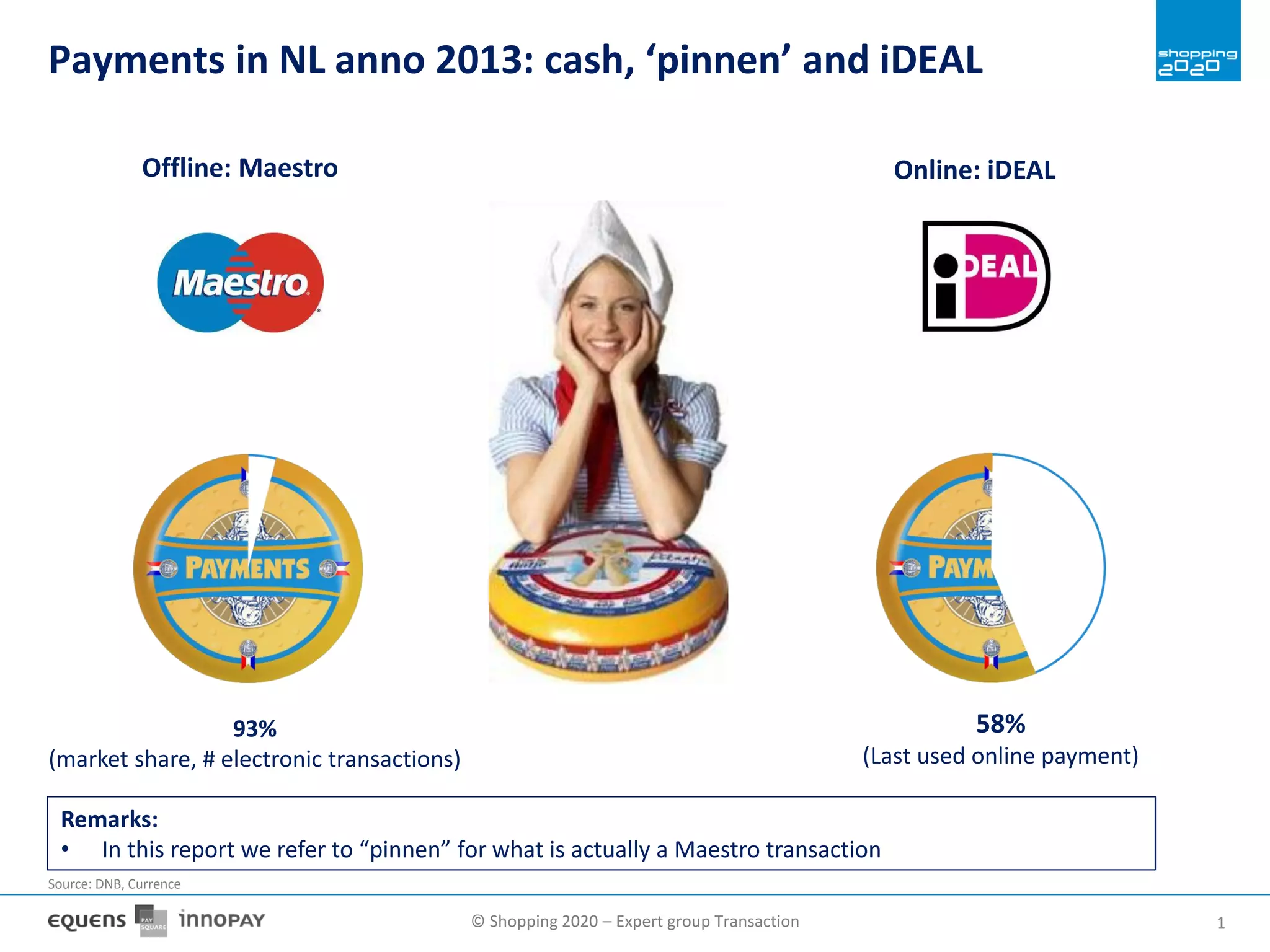

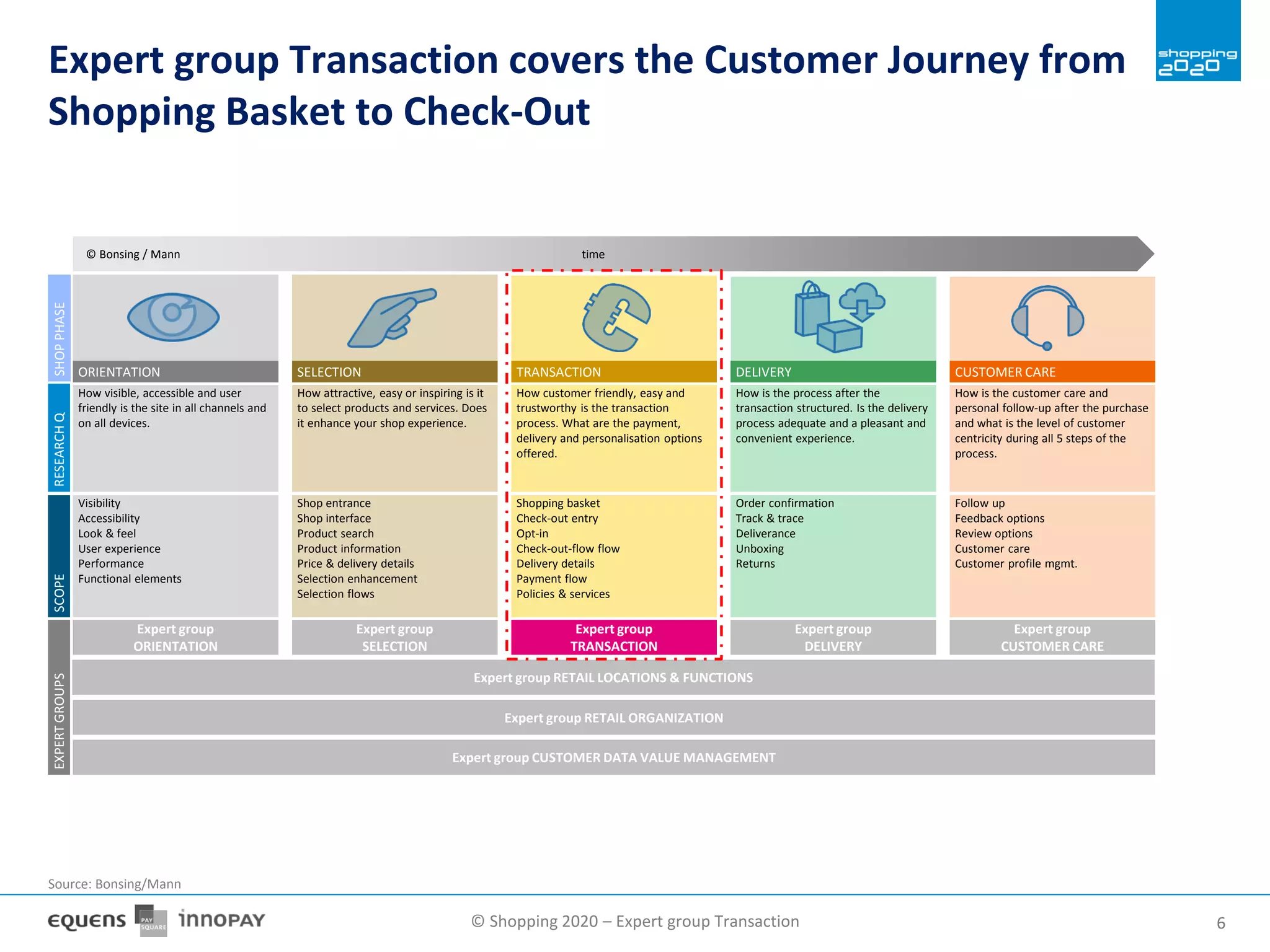

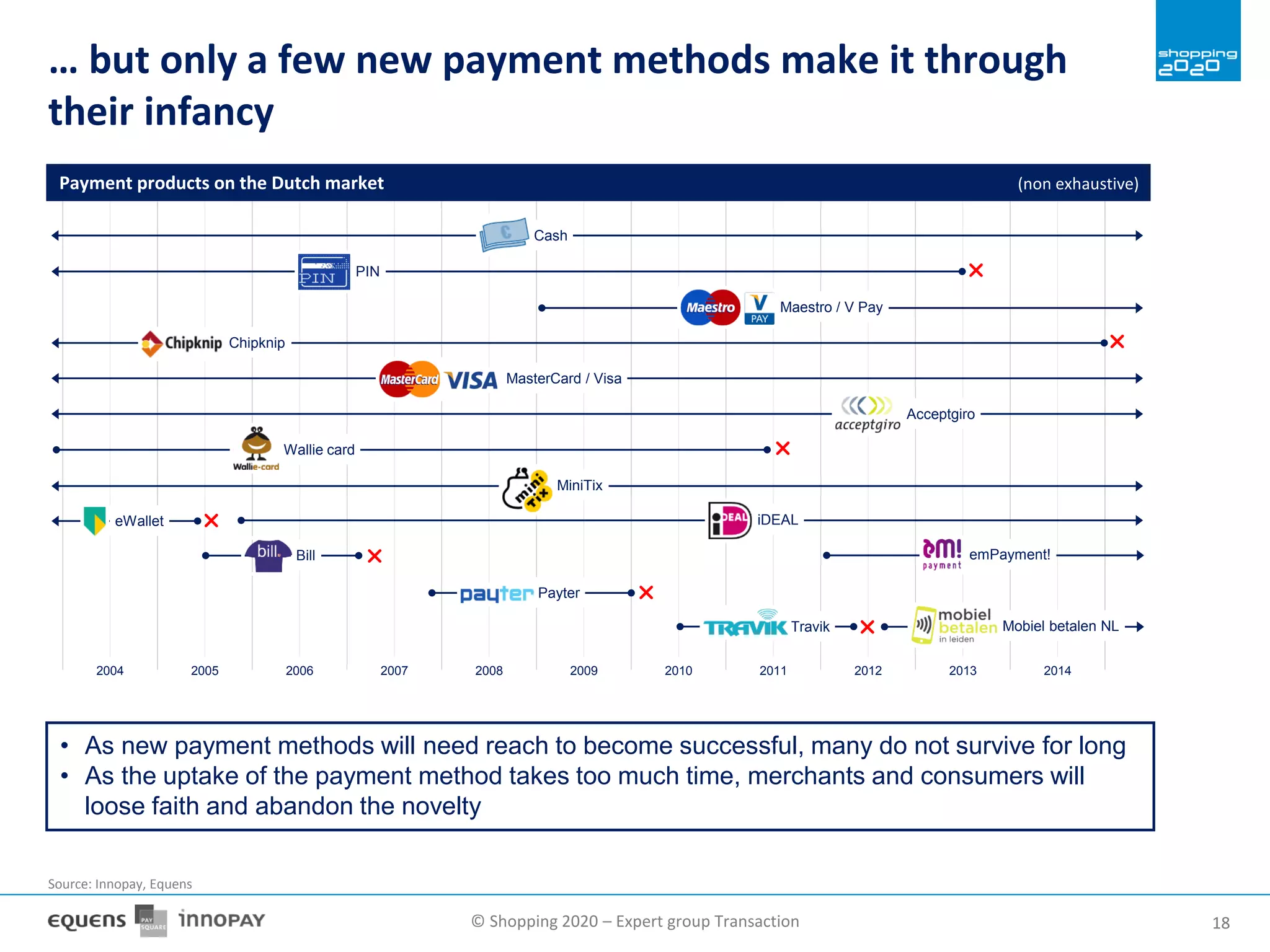

The document discusses payment methods used in the Netherlands in 2013, highlighting cash, 'pinnen' (Maestro), and iDEAL as the primary methods for transactions. It outlines the trends in Dutch shopping behavior, emphasizing the growth of online retail and the importance of payment methods that enhance consumer trust and convenience. Additionally, the report analyzes the evolving payment landscape which is influenced by changing consumer preferences and the rise of e-commerce.

![© Shopping 2020 – Expert group Transaction 2323

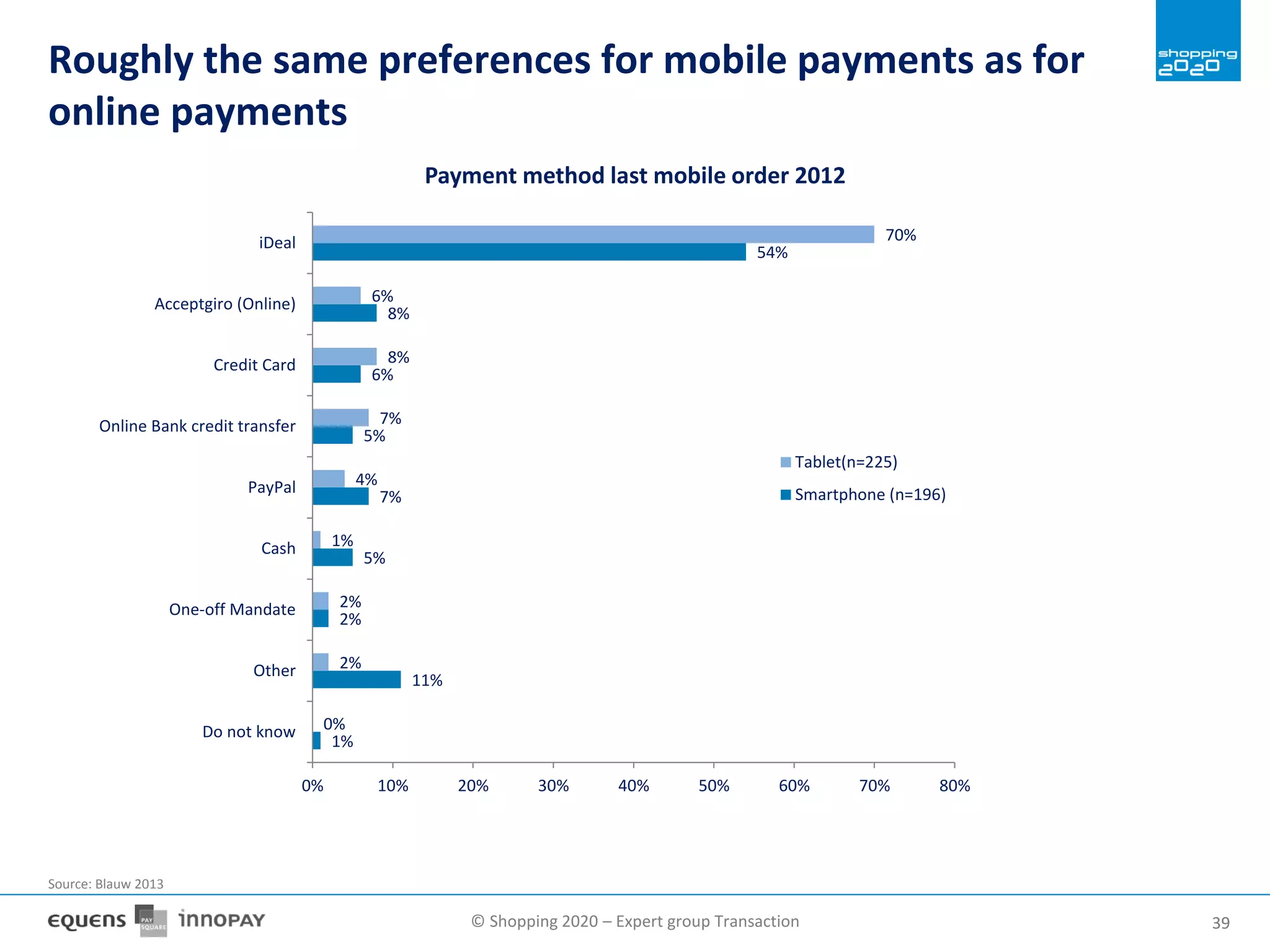

Online shopping is growing, while offline retail is declining

0

2

100

90

80

70

60

50

40

30

20

10

0

12

16

14

10

8

6

4

TurnoverinBillion€

2013

79

11

2012

83

10

2011

87

Percentage

89

8 9

2009

92

7

2008 2010

5

6

2007

83

90

Offline retail turnoverOnline retail turnover% online retail / total retail

+14%

Development online vs. offline retail (NL)

-10

-5

0

5

10

15

20

25

30

35

40

45

2005 2006 2007 2008 2009 2010 2011 2012

Percentage

Growth compared to the previous year

Retail Total Online Retail

• The Dutch online market is one of the most developed e-Commerce markets in EU (after UK ~96 Bn, DE ~50

Bn, FR ~45 Bn online sales of goods & services [2012])

• In NL online retail will account for 12% of total retail turnover in 2013

• The double digit e-Commerce growth in NL is stabilizing at ~ 10% per year since 2013

• The vast increase of online retail until 2030 is for nearly 30% at the expense of offline retail

• The prices in offline retail have increased, as the amount of goods sold (i.e. volume) have decreased

substantially since 2009, while recovery is not expected in the short term (> 2015)

Source: Thuiswinkel.org, ING Economisch Bureau, Internet World Stats, Emerce, E-commerce Europe, Roland Berger, CBS, Innopay analysis](https://image.slidesharecdn.com/howdothedutchpayin2013-131004010342-phpapp01/75/How-do-the-dutch-pay-in-2013-24-2048.jpg)