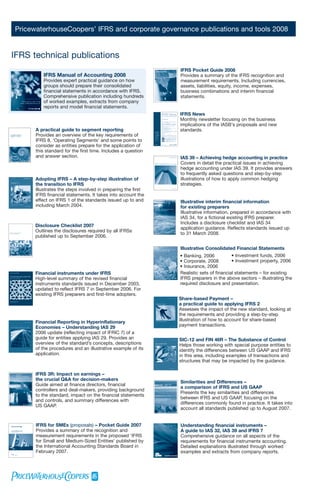

Downloaded 110 times

![IFRS GAAP plc – Illustrative IFRS corporate consolidated financial statements

(All amounts in C thousands unless otherwise stated)

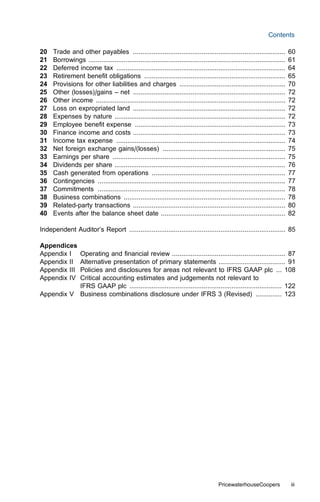

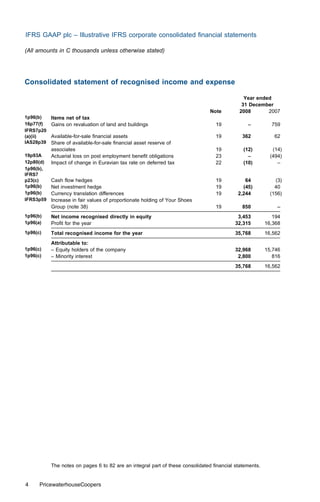

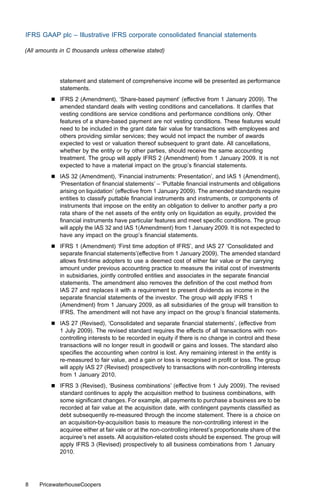

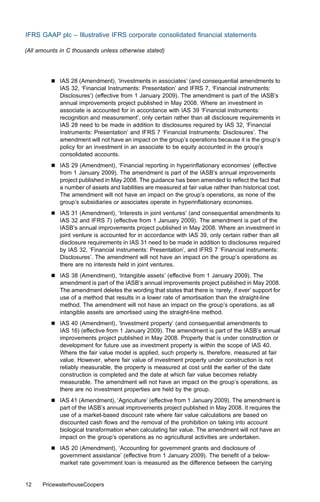

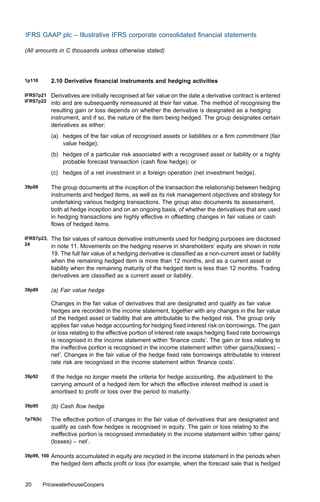

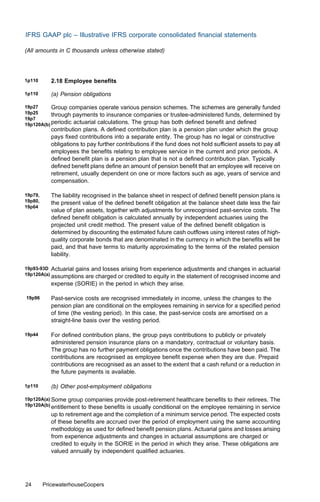

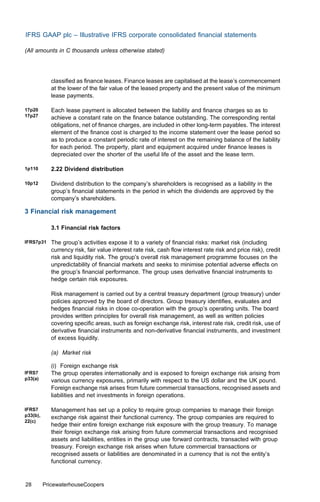

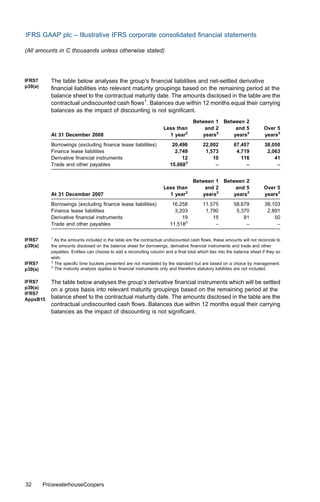

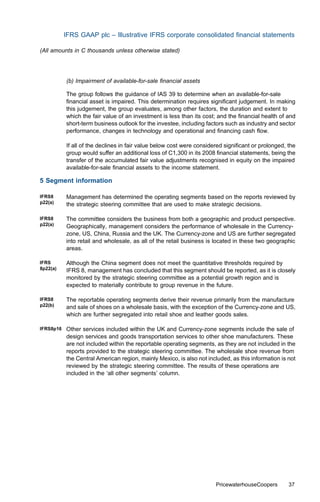

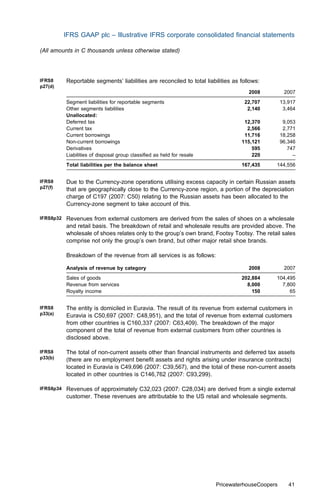

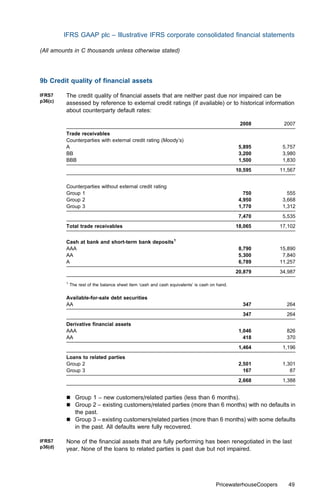

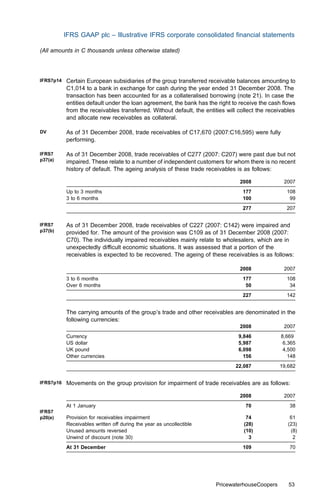

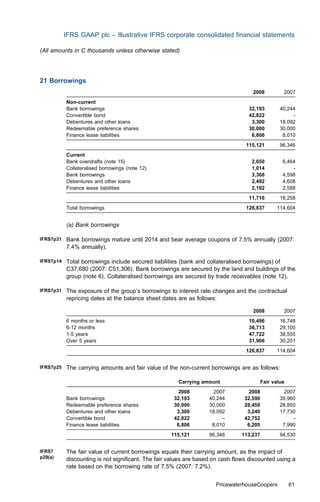

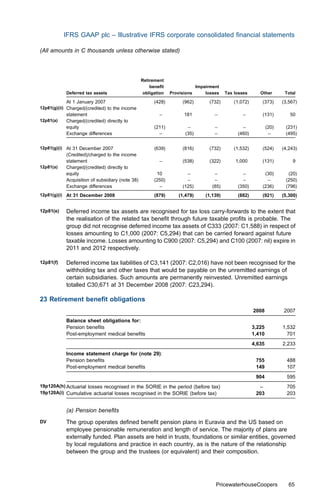

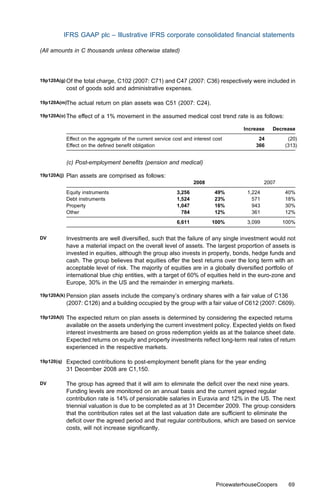

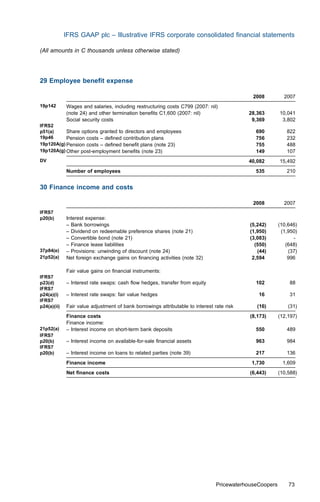

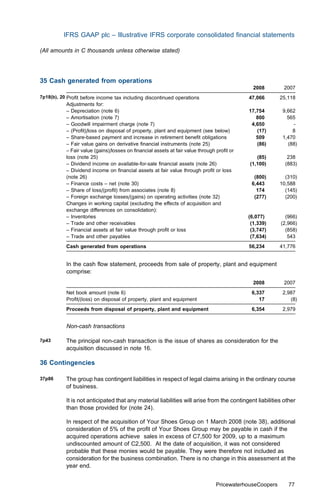

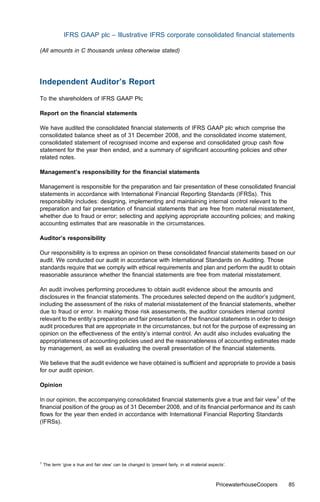

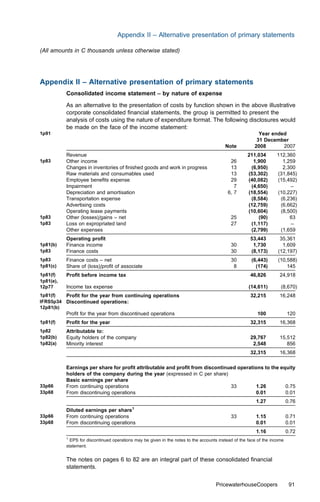

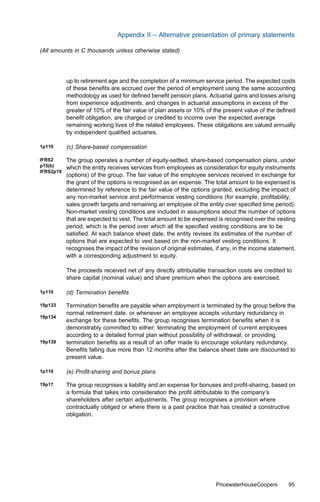

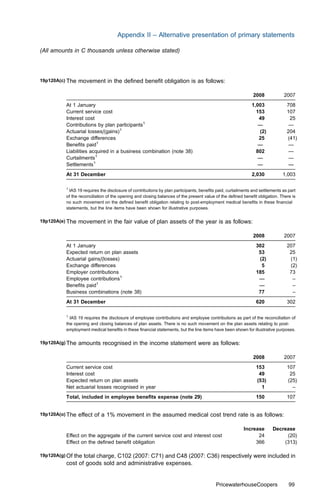

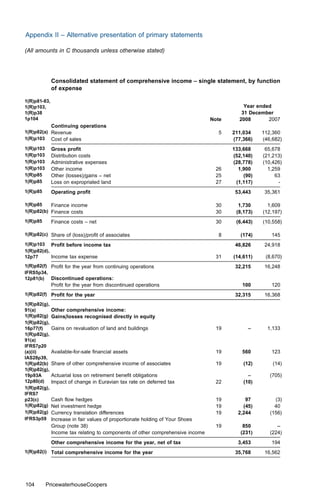

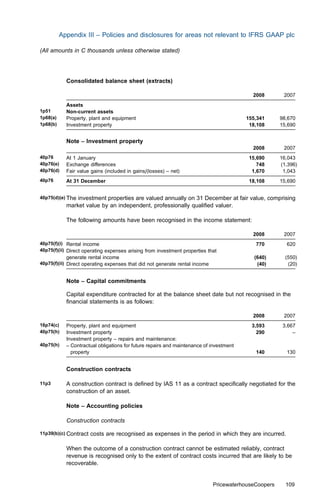

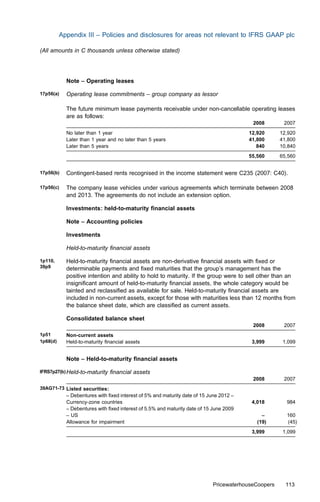

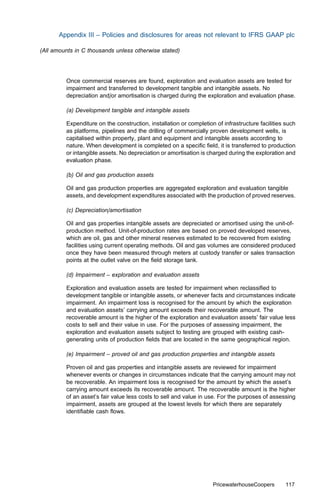

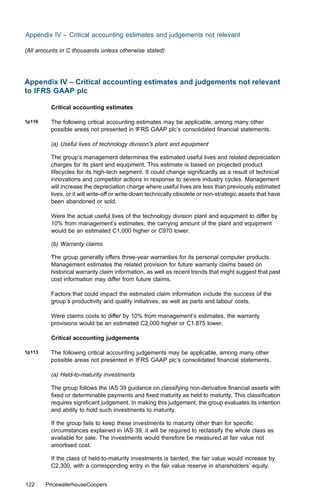

Between 1 Between 2

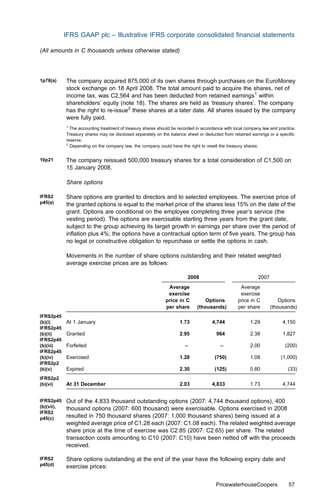

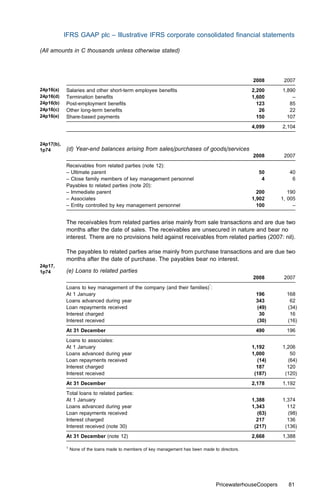

Less than 1 and 2 and 5 Over 5

At 31 December 2008 year1 years1 years1 years1

Forward foreign exchange contracts – cash

flow hedges2

IFRS7

p39(a)

IFRS7 Outflow 78,241 – – –

AppxB15

DV Inflow 78,756 – – –

Forward foreign exchange contracts –

held for trading2

IFRS7

p39(a)

IFRS7 Outflow 14,129 – – –

AppxB15

DV Inflow 14,222 – – –

Between 1 Between 2

Less than 1 and 2 and 5 Over 5

At 31 December 2007 year1 years1 years1 years1

Forward foreign exchange contracts – cash

flow hedges2

IFRS7

p39(a)

IFRS7 Outflow 83,077 – – –

AppxB15

DV Inflow 83,366 – – –

Forward foreign exchange contracts –

held for trading2

IFRS7

p39(a)

IFRS7 Outflow 6,612 – – –

AppxB15

DV Inflow 6,635

1

IFRS7 The specific time buckets presented are not mandated by the standard but are based on a choice by management.

p39(a) 2

IFRS 7 requires a maturity analysis only for financial liabilities [IFRS 7 para 39(a)]. In addition, IFRS 7 appendix B

paragraph 14 (d) specifies that contractual gross cash flows to be exchanged in a derivative contract should be

presented in that analysis. In our view, as a minimum, for financial instruments that are liabilities at the balance sheet

date, the cash outflows should be included in the maturity analysis. This will include the pay legs of gross-settled

derivatives and commodity contracts that are liabilities at the balance sheet date. While the standard only requires the

gross cash outflows (that is, the pay leg) to be included in the maturity analysis, separate disclosure of the

corresponding inflows (that is, the receive leg) might make the information more meaningful.

1p124A, 3.2 Capital risk management

124B, IG5

The group’s objectives when managing capital are to safeguard the group’s ability to

continue as a going concern in order to provide returns for shareholders and benefits for

other stakeholders and to maintain an optimal capital structure to reduce the cost of

capital.

In order to maintain or adjust the capital structure, the group may adjust the amount of

dividends paid to shareholders, return capital to shareholders, issue new shares or sell

assets to reduce debt.

PricewaterhouseCoopers 33](https://image.slidesharecdn.com/illustrativefinancialstatementsweboptimized-090715193115-phpapp02/85/Illustrative-Financial-Statements-Web-Optimized-41-320.jpg)

![IFRS GAAP plc – Illustrative IFRS corporate consolidated financial statements

(All amounts in C thousands unless otherwise stated)

Report on other legal and regulatory requirements

[Form and content of this section of the auditor’s report will vary depending on the nature of the

auditor’s other reporting responsibilities, if any.]

Signature

Date

Address

The format of the audit report will need to be tailored to reflect the legal framework of particular

countries. In certain countries, the audit report covers both the current year and the comparative

year.

86 PricewaterhouseCoopers](https://image.slidesharecdn.com/illustrativefinancialstatementsweboptimized-090715193115-phpapp02/85/Illustrative-Financial-Statements-Web-Optimized-94-320.jpg)

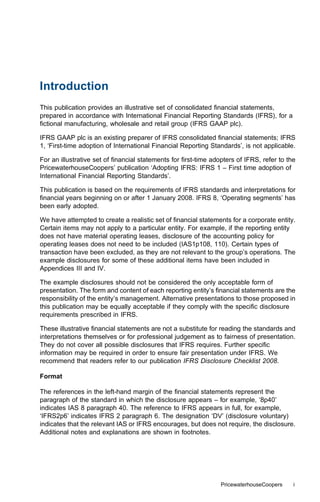

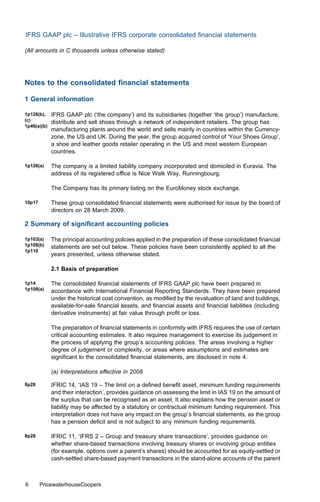

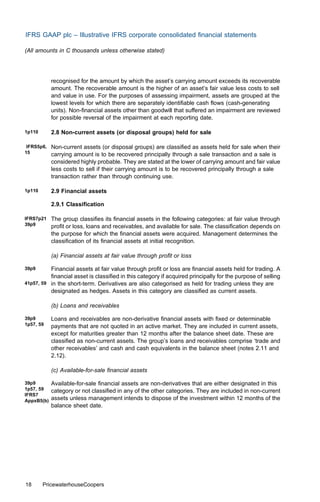

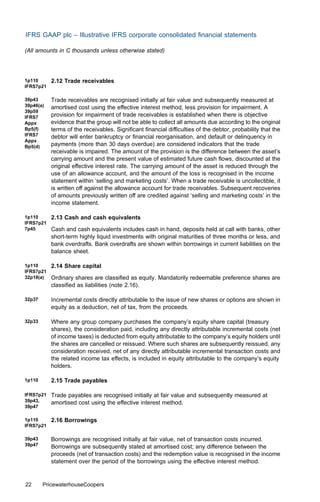

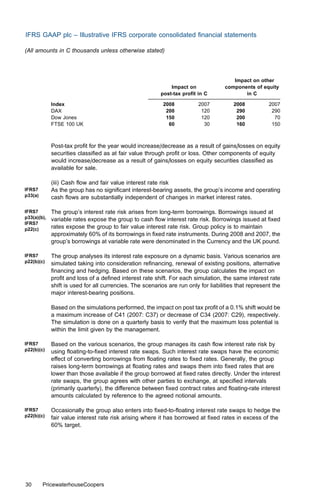

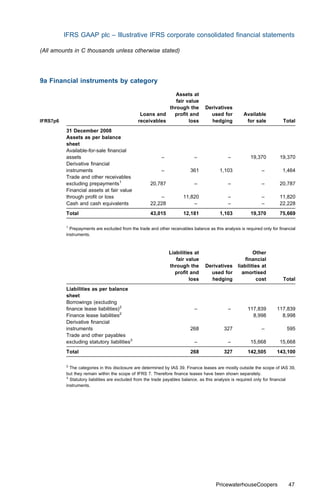

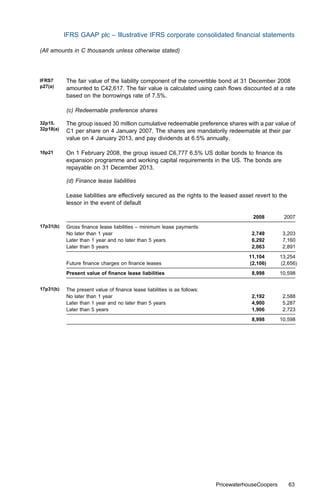

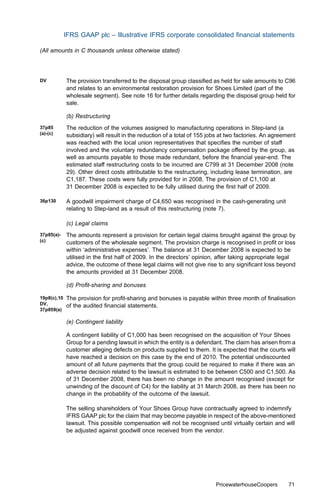

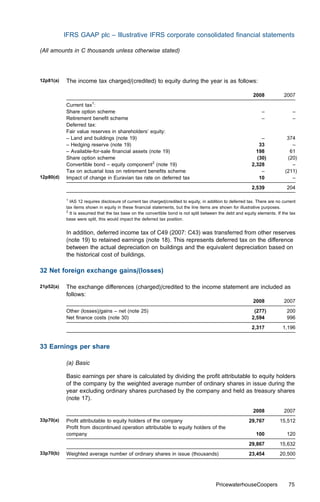

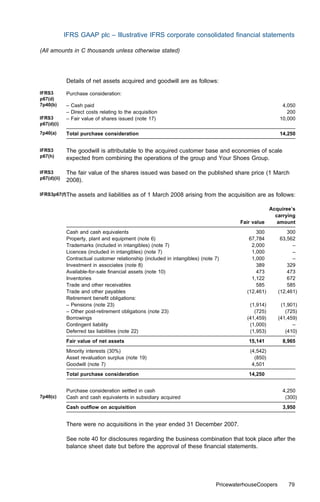

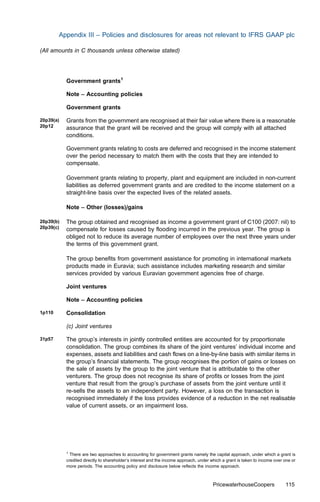

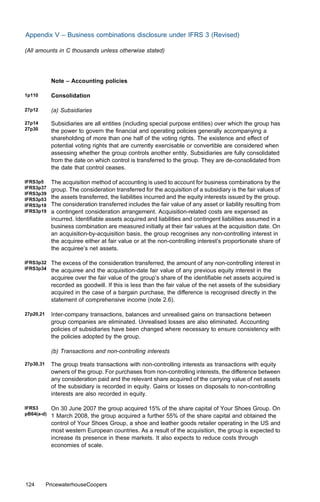

![Appendix II – Alternative presentation of primary statements

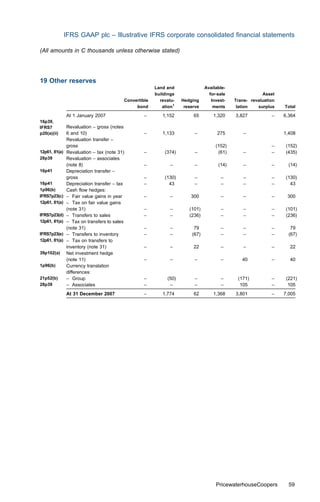

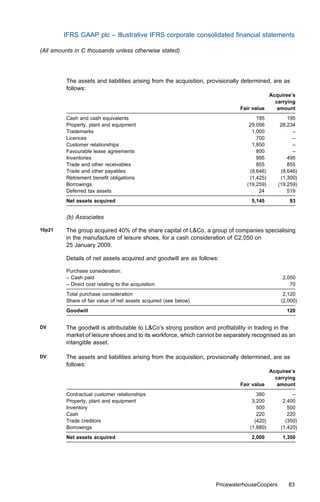

(All amounts in C thousands unless otherwise stated)

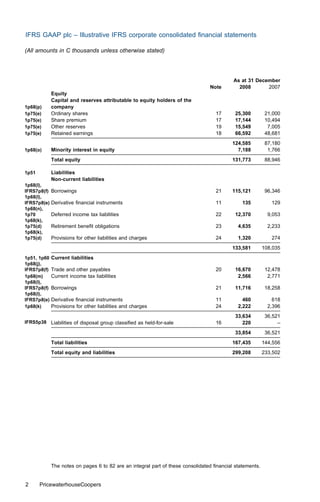

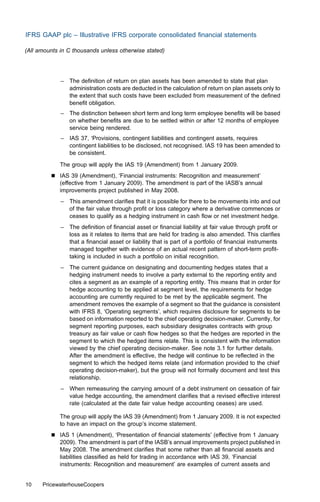

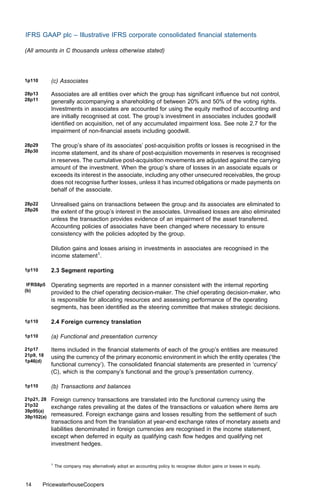

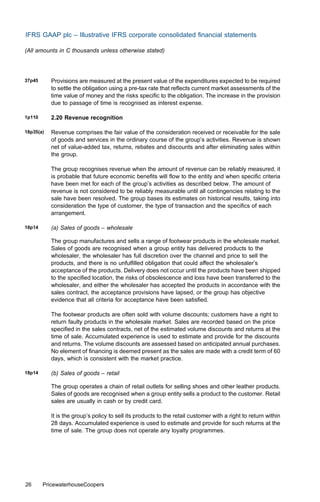

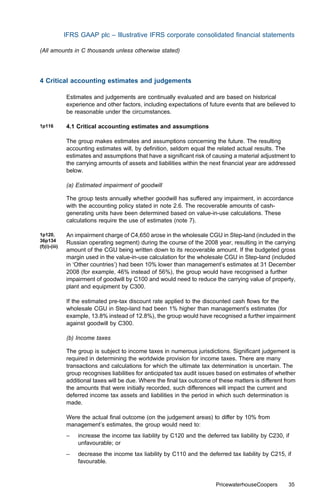

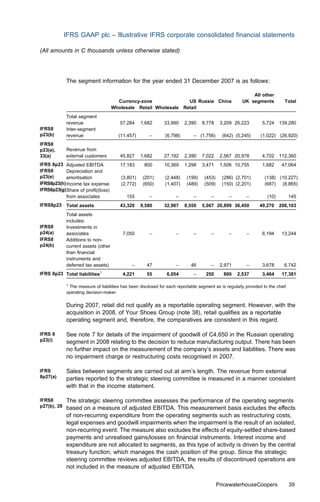

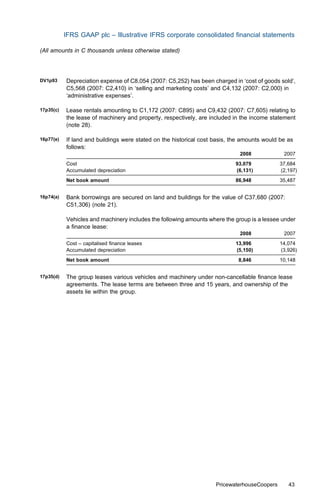

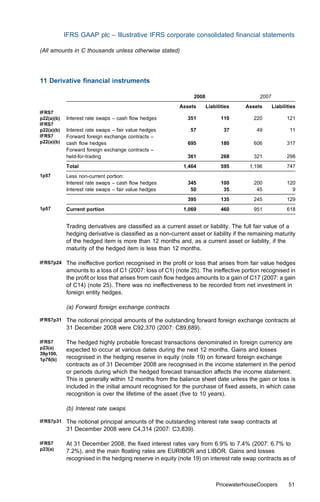

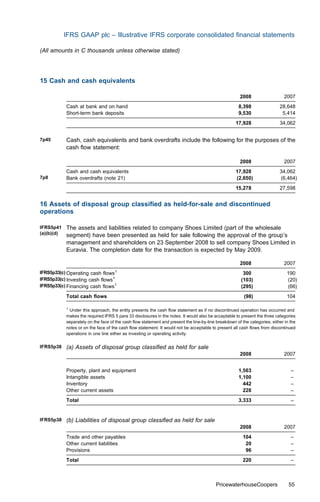

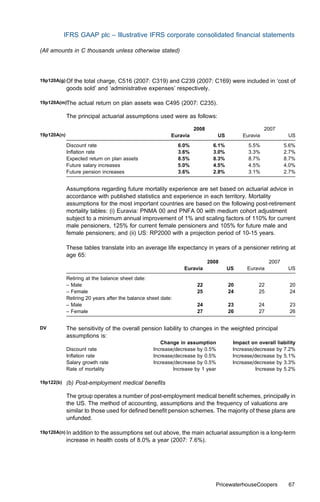

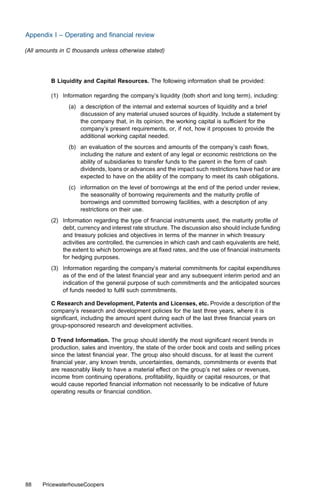

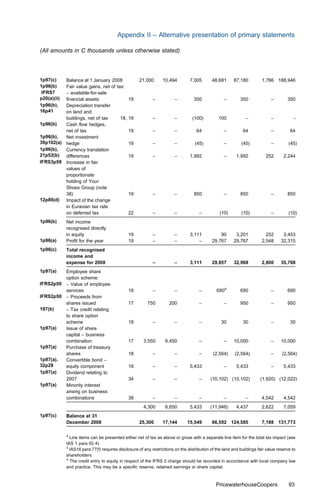

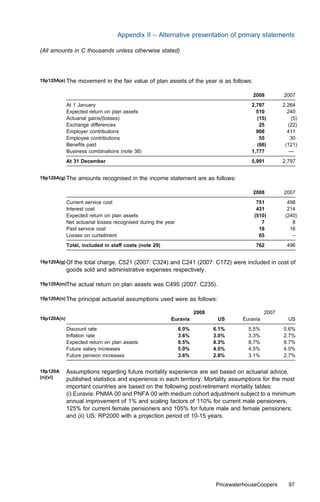

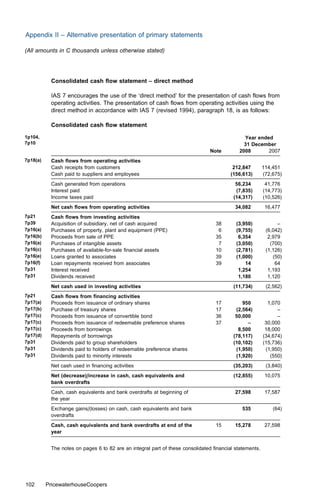

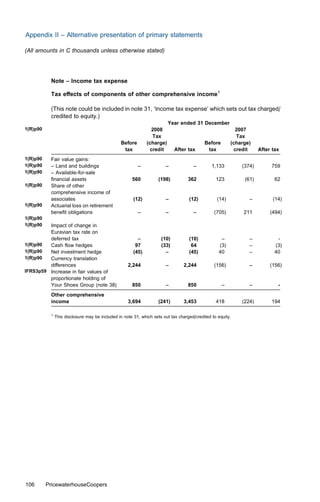

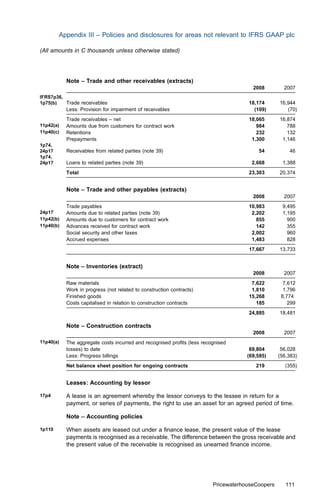

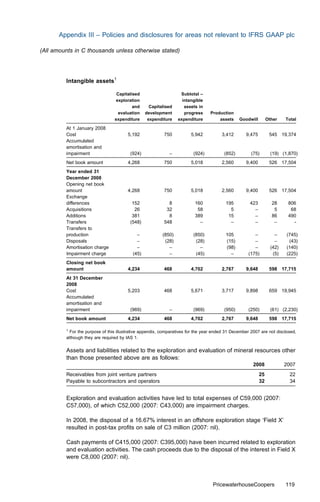

19p120A(p) 2008 2007 2006 20051

At 31 December

Present value of defined benefit

obligation 11,391 5,495 4,187 3,937

Fair value of plan assets 6,611 3,099 2,471 2,222

Deficit/(surplus) in the plan 4,780 2,396 1,716 1,715

Experience adjustments on plan

liabilities (326) 125 55 –

Experience adjustments on plan

assets (17) (6) (197) –

1

IAS 19 requires a five-year record, but this does not have to be applied retrospectively [IAS 19 para 160].

PricewaterhouseCoopers 101](https://image.slidesharecdn.com/illustrativefinancialstatementsweboptimized-090715193115-phpapp02/85/Illustrative-Financial-Statements-Web-Optimized-109-320.jpg)

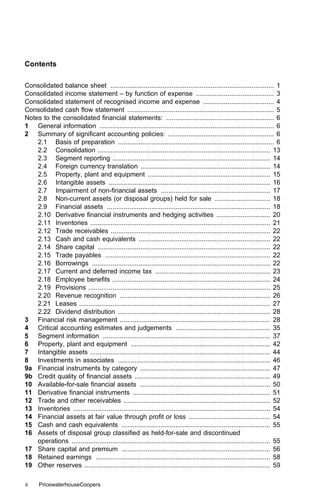

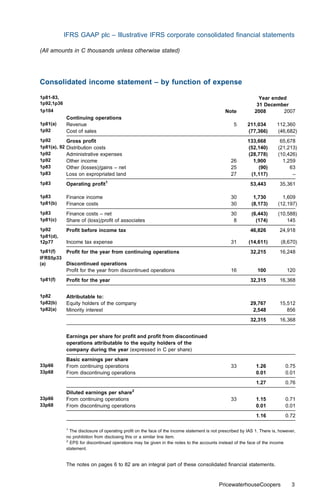

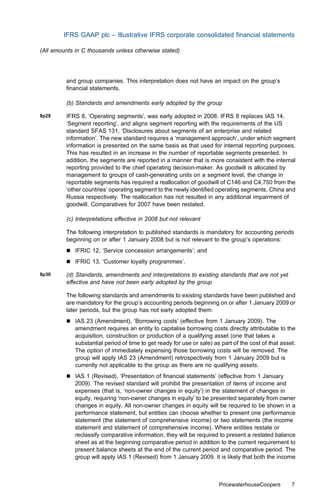

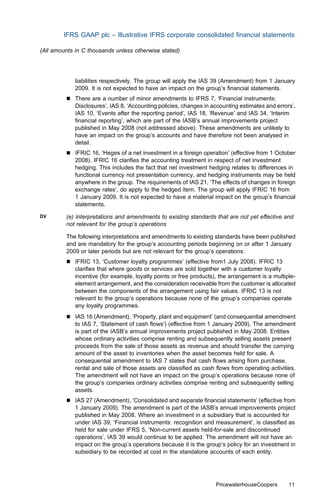

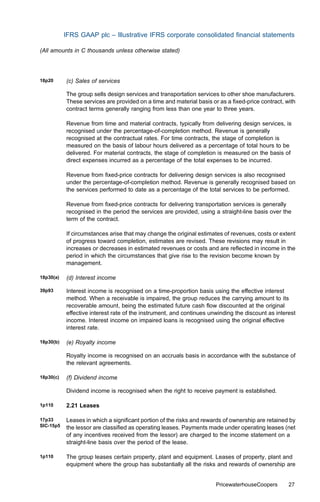

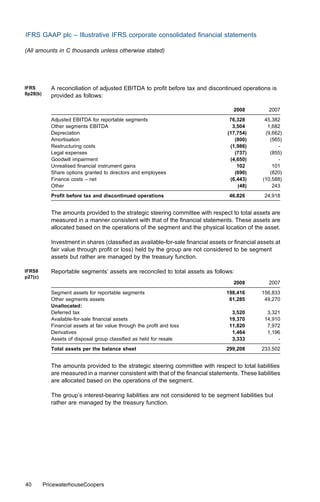

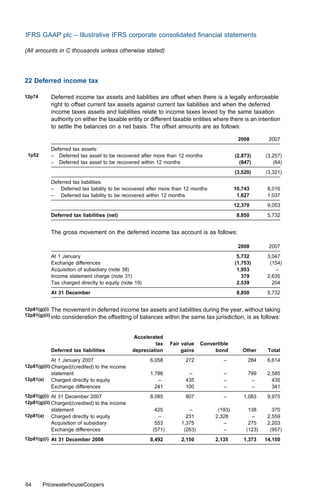

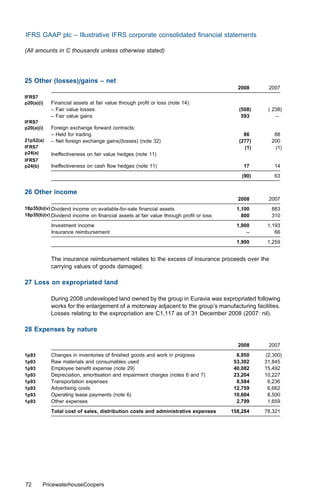

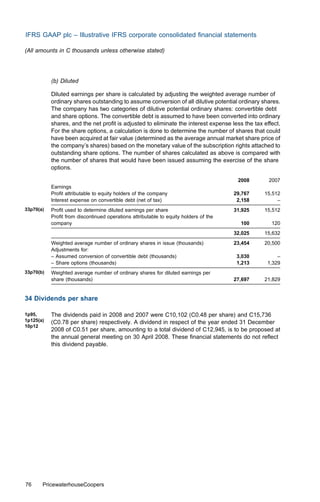

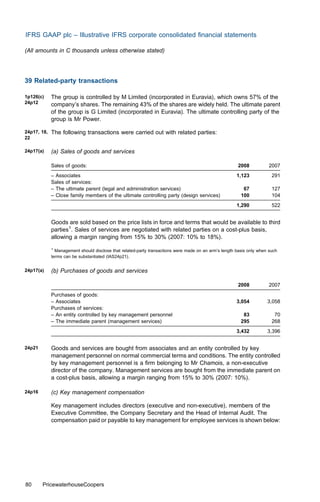

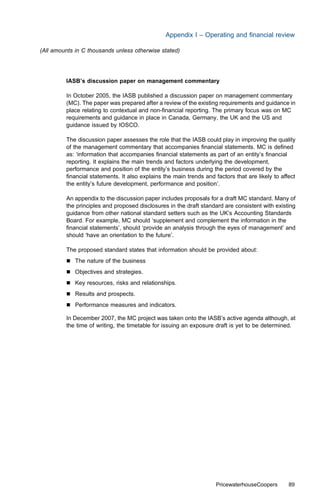

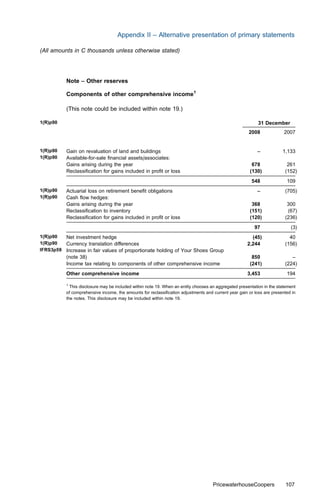

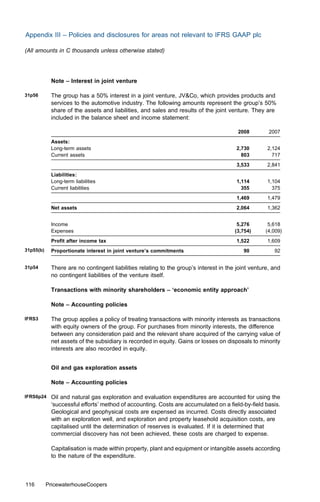

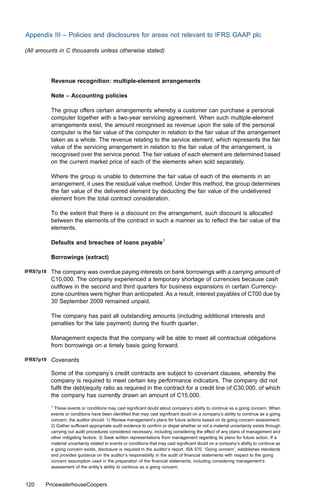

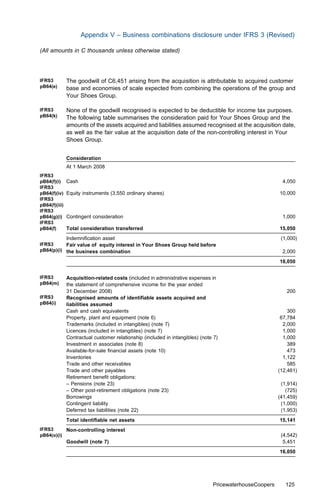

![Appendix III – Policies and disclosures for areas not relevant to IFRS GAAP plc

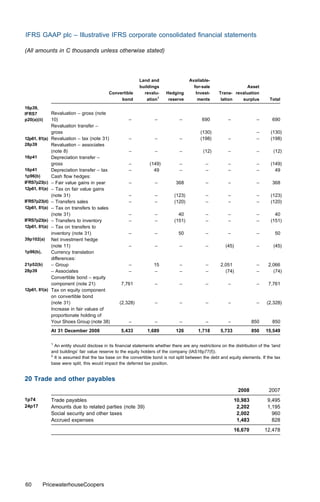

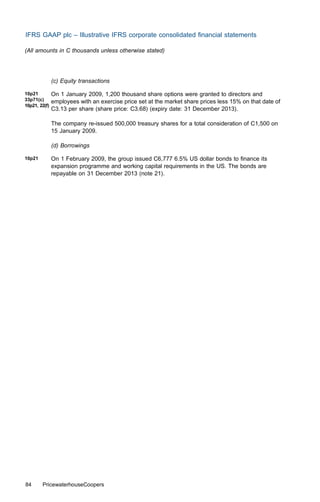

(All amounts in C thousands unless otherwise stated)

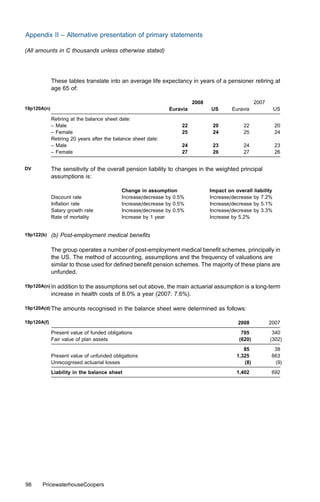

Appendix III – Policies and disclosures for areas not relevant to IFRS

GAAP plc

Investment property1

40p5 Investment property is defined as property (land or a building – or part of a building – or

both) held (by the owner or by the lessee under a finance lease) to earn rentals or for

capital appreciation or both, rather than for: (a) use in the production of supply of goods or

services or for administrative purposes; or (b) sale in the ordinary course of business.

Note – Accounting policies

(a) Basis of preparation2

The consolidated financial statements have been prepared under the historical cost

convention as modified by the revaluation of land and buildings, available-for-sale

financial assets, financial assets and financial liabilities at fair value through profit or loss

and investment properties, which are carried at fair value.

1p110 (b) Investment property2

40p75(a)(d) Investment property, principally comprising freehold office buildings, is held for long-term

rental yields and is not occupied by the group. Investment property is carried at fair value,

representing open market value determined annually by external valuers. Fair value is

based on active market prices, adjusted, if necessary, for any difference in the nature,

location or condition of the specific asset. If the information is not available, the group

uses alternative valuation methods such as recent prices on less active markets or

discounted cash flow projections. These valuations are reviewed annually by [A Valuers]3.

Changes in fair values are recorded in the income statement as part of other income.

(c) Rental income from investment property is recognised in the income statement on a

straight-line basis over the term of the lease.

40p6, 25 Land held under operating lease is classified and accounted for as investment property

when the rest of the definition of investment property is met. The operating lease is

accounted for as if it were a finance lease.

1

The above investment property disclosures are given for corporate entities that hold property to earn rentals or for

capital appreciation or both. It does not cover all the disclosures that would be required for an investment property

company. For investment property companies, refer to the PwC industry-specific illustrative financial statements.

2

To be approximately amended if the cost method is applied.

3

To include the name of the external valuer.

108 PricewaterhouseCoopers](https://image.slidesharecdn.com/illustrativefinancialstatementsweboptimized-090715193115-phpapp02/85/Illustrative-Financial-Statements-Web-Optimized-116-320.jpg)

The document provides illustrative IFRS corporate consolidated financial statements for a fictional entity, IFRS GAAP PLC, adhering to International Financial Reporting Standards as of 2008. It includes detailed guidance on various accounting aspects, such as consolidation, segment reporting, and financial instrument management, with hundreds of examples, extracts, and model statements. Additionally, it emphasizes the importance of adhering to specific IFRS standards and offers practical insights for finance professionals in preparing accurate financial reports.