HDFC Morning Market Note - HDFC Sec

•

1 like•177 views

- Indian stock indices ended lower on August 6, with the Sensex falling 0.94% and the Nifty declining 0.96%, led by losses in banking and metal stocks. - US stocks edged slightly higher despite tensions between Russia and Ukraine, while major European indices closed lower. - The rupee hit a five-month low of 61.51 against the dollar on stronger US economic data. Gold and oil prices rose marginally. - Asian markets opened lower on August 7 following declines in Chinese and Hong Kong shares, while SGX Nifty futures indicated Indian markets may open in negative territory.

Recommended

More Related Content

What's hot

What's hot (20)

Similar to HDFC Morning Market Note - HDFC Sec

Similar to HDFC Morning Market Note - HDFC Sec (20)

More from IndiaNotes.com

More from IndiaNotes.com (20)

HDFC Morning Market Note - HDFC Sec

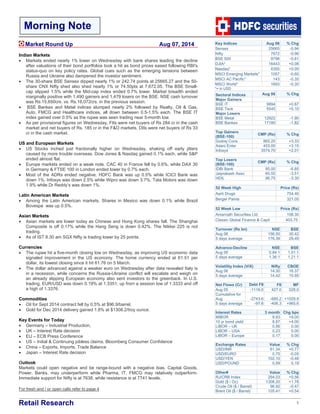

- 1. Retail Research 1 Key Indices Aug 06 % Chg Sensex 25665 -0.94 Nifty 7672 -0.96 BSE 500 9798 -0.81 DJIA* 16443 +0.08 Nasdaq* 4355 +0.05 MSCI Emerging Markets* 1057 -0.60 MSCI AC Pacific* 143 -0.35 MSCI World* 1693 -0.30 *= in USD Sectoral Indices Aug 06 % Chg Major Gainers BSE IT 9894 +0.67 BSE Teck 5545 +0.10 Major Losers BSE Metal 12922 -1.90 BSE Bankex 17180 -1.82 Top Gainers (BSE-100) CMP (Rs) % Chg Godrej Cons 865.25 +3.33 Adani Enter 453.00 +3.15 Infosys 3574.70 +2.01 Top Losers (BSE-100) CMP (Rs) % Chg IDBI Bank 85.00 -6.85 Jaiprakash Asso 60.55 -3.51 HDIL 96.75 -3.30 52 Week High Price (Rs) Aarti Drugs 754.40 Berger Paints 321.05 52 Week Low Price (Rs) Amarnath Securities Ltd. 108.30 Classic Global Finance & Capit 403.75 Turnover (Rs bn) NSE BSE Aug 06 156.50 30.42 5 days average 176.39 29.49 Advance-Decline NSE BSE Aug 06 0.84:1 1.01:1 5 days average 1.36:1 1.21:1 Volatility Index (ViX) Nifty CBOE Aug 06 14.30 16.37 5 days average 14.42 15.95 Net Flows (Cr) Debt FII FII MF Aug 05 -1116.0 427.0 228.0 Cumulative for Aug -2743.6 -685.2 +1029.9 5 days average -97.8 -406.3 +965.6 Interest Rates 3 month Chg bps MIBOR 8.93 +9.00 10 yr bond yield 8.87 +4.00 LIBOR – UK 0.56 0.00 LIBOR – USA 0.23 0.00 LIBOR – Europe 0.17 0.00 Exchange Rates Value % Chg USD/INR 61.34 +0.77 USD/EURO 0.75 -0.05 USD/YEN 102.10 -0.48 USD/POUND 0.59 0.19 Other# Value % Chg RJ/CRB Index 294.03 +0.56 Gold ($ / Oz) 1308.20 +1.78 Crude Oil ($ / Barrel) 96.92 -0.47 Brent Oil ($ / Barrel) 105.41 +0.54 Market Round Up Aug 07, 2014 Indian Markets • Markets ended nearly 1% lower on Wednesday with bank shares leading the decline after valuations of their bond portfolios took a hit as bond prices eased following RBI's status-quo on key policy rates. Global cues such as the emerging tensions between Russia and Ukraine also dampened the investor sentiment. • The 30-share BSE Sensex dipped nearly 1% or 242.74 points at 25665.27 and the 50- share CNX Nifty shed also shed nearly 1% or 74.50pts at 7,672.05. The BSE Small- cap slipped 1.5% while the Mid-cap index ended 0.7% lower. Market breadth ended marginally positive with 1,490 gainers and 1,479 losers on the BSE. NSE cash turnover was Rs.15,650crs. vs. Rs.16,072crs. in the previous session. • BSE Bankex and Metal indices slumped nearly 2% followed by Realty, Oil & Gas, Auto, FMCG and Healthcare indices, all down between 0.5-1.5% each. The BSE IT index gained over 0.5% as the rupee was seen trading near 5-month low. • As per provisional figures on Wednesday, FIIs were net buyers of Rs 284 cr in the cash market and net buyers of Rs. 185 cr in the F&O markets. DIIs were net buyers of Rs 33 cr in the cash market. US and European Markets • US Stocks inched just fractionally higher on Wednesday, shaking off early jitters caused by more trouble overseas. Dow Jones & Nasdaq gained 0.1% each, while S&P ended almost flat. • Europe markets ended on a weak note. CAC 40 in France fell by 0.6%, while DAX 30 in Germany & FTSE 100 in London ended lower by 0.7% each. • Most of the ADRs ended negative. HDFC Bank was up 0.5% while ICICI Bank was down 1%. Infosys was down 2.5% while Wipro was down 3.7%. Tata Motors was down 1.9% while Dr Reddy’s was down 1%. Latin American Markets • Among the Latin American markets, Shares in Mexico was down 0.1% while Brazil Bovespa was up 0.5%. Asian Markets • Asian markets are lower today as Chinese and Hong Kong shares fall. The Shanghai Composite is off 0.17% while the Hang Seng is down 0.42%. The Nikkei 225 is not trading. • As of IST 8.30 am SGX Nifty is trading lower by 25 points. Currencies • The rupee hit a five-month closing low on Wednesday, as improving US economic data signaled improvement in the US economy. The home currency ended at 61.51 per dollar, its lowest closing since it hit 61.76 on 5 March. • The dollar advanced against a weaker euro on Wednesday after data revealed Italy is in a recession, while concerns the Russia-Ukraine conflict will escalate and weigh on an already slipping European economy also sent investors to the greenback. In U.S. trading, EUR/USD was down 0.19% at 1.3351, up from a session low of 1.3333 and off a high of 1.3376. Commodities • Oil for Sept 2014 contract fell by 0.5% at $96.9/barrel. • Gold for Dec 2014 delivery gained 1.8% at $1308.2/troy ounce. Key Events for Today • Germany – Industrial Production, • UK – Interest Rate decision • EU – ECB Press Conference • US – Initial & Continuing jobless claims, Bloomberg Consumer Confidence • China – Exports, Imports, Trade Balance • Japan – Interest Rate decision Outlook Markets could open negative and be range-bound with a negative bias. Capital Goods, Power, Banks, may underperform while Pharma, IT, FMCG may relatively outperform. Immediate support for Nifty is at 7638, while resistance is at 7741 levels. For fresh and / or open calls refer to page 4 Morning Note

- 2. Retail Research 2 Technical Analysis – Market Pulse Aug 07, 2014 Yesterday’s action saw the markets correcting after two sessions of positive closings. Zooming into the 15-min intraday charts (See above), we observe that the Nifty was consistently making lower tops and lower bottoms. The selling intensified after 2.0 pm. We observe that the Nifty has reacted after testing the 61.8% retracement levels of the recent down move from 7838 to 7593. We now need to see if the Nifty can hold above the immediate supports of 7638 in tomorrow’s trading session. This support also coincides with a trend line that has held the recent lows of the Nifty. With the short term (7-21 days) trend continuing to remain down, the odds do seem higher that the immediate supports of 7638 are likely to break down. This would bring into focus the next downside targets at 7593 and 7422. Nifty Perspective Support Resistance 13 Day SMA 7672.00 Bearish 7638 – 7622 7741 – 7753 7731 Nifty Trend Target Reversal Near Term (1 day) Down 7638 7730 Short Term (7-21 days) Down 7422 7799

- 3. Retail Research 3 For forthcoming Board Meeting on Aug 07, 2014 click on the following link http://www.bseindia.com/mktlive/board_meeting.asp#1 News Flash Aug 07, 2014 Economy News • The oil companies have sought a subsidy of around Rs 13,140 crore for the first quarter of the current financial year 2014-15. • FIPB has approved foreign direct investment (FDI) proposals worth Rs 1,528.38 crore from 14 firms including ACME Solar Energy and Sinclairs Hotels. • A sharp drop in cotton prices overseas and a weak monsoon have raised India's imports in recent weeks, which could lift shipments more than 25% above the official forecast for this season ending September and help support cotton futures. Corporate News • Infosys’s former chief financial officers (CFOs) – T V Mohandas Pai and V Balakrishnan and former senior vice-president D N Prahlad – writing to the company’s board to “immediately” consider a Rs 11,200 crore (approx $2 billion) buyback of shares. • Apollo Tyres plans to invest Euros 500 million to construct a green field facility in Eastern Europe as part of its overseas expansion plans. Company reported 37.36 per cent jump in consolidated net profit at Rs 227.94 crore for the quarter ended June 30 on the back of higher other income. • Suven Life Sciences Limited has secured one product patent from Australia and another from Eurasia corresponding to the new chemical entities (NCEs) for the treatment of disorders associated with neurodegenerative diseases. The patents are valid through 2030 and 2029 respectively. • Amara Raja Batteries Limited has posted a net profit of Rs 106 crore for the first quarter of 2014-15, a rise of 8% from the corresponding quarter last year. Net sales increased by 16% to Rs 1,025 crore from Rs 887 crore in the same period. • Lupin Limited signed a strategic distribution agreement with LG Life Sciences of South Korea to launch Insulin Glargine, a novel insulin analogue under the brand name Basugine. According to the agreement, Lupin would be responsible for marketing and sales of Basugine in India. Bulk Deals Scrip Name Quantity (in lakhs) Fund Name Price Atul Auto +3.00 HDFC MUTUAL FUND 615.03 Samkrg Pistons +0.70 IFB AUTOMOTIVE PVT LTD 100.30 Key Corporate Action SCRIP NAME BC/RD BC/RD FROM EX-DATE PURPOSE GHCL Ltd BC 11/08/2014 07/08/2014 AGM, 20% Dividend GVK Power Infra BC 09/08/2014 07/08/2014 AGM LIC Housing Finance BC 09/08/2014 07/08/2014 AGM, 225% Dividend Munjal Show BC 09/08/2014 07/08/2014 AGM, 175% Dividend UPL BC 09/08/2014 07/08/2014 AGM, 200% Dividend Venkys India BC 11/08/2014 07/08/2014 AGM, 50% Dividend

- 4. Retail Research 4 Stock Ideas Aug 07, 2014 Update of Index Futures Date B/S Positional Call Entry at Sloss Targets Exit Price / CMP Exit Date % G/L Comments Time Horizon Avg. Entry Abs. Gain/Loss 6-Aug-14 S Nifty Aug Fut 7724.9 7760.0 7670.0 7705.0 6 Aug 14 0.3 Premature Profit Booked 1-5 days 7724.9 19.9 4-Aug-14 B Nifty Aug Fut 7710 7660.0 7810.0 7738.0 5 Aug 14 0.4 Premature Profit Booked 1-5 days 7710.0 28.0 Update of Stock and Nifty Options Calls: Date B/S Positional Call Entry at Sloss Targets Exit Price / CMP Exit Date % G/L Comments Time Horizon Avg. Entry Abs. Gain/Loss 5 Aug 14 B Buy Tata Motors Aug 450 Calls 18.45 12.8 33.0 14.5 -21.4 Hold 1-5 days 18.45 -4.0 4 Aug 14 B Coal India 350 Put 8.30 5.3 17.0 7.1 4 Aug 14 -14.5 Exit 1-3 Days 8.30 -1.2 4 Aug 14 B INFY 2450 Call 84.00 55.0 130.0 100.0 4 Aug 14 19.0 Premature Profit Booked 1-5 Days 84.00 16.0 4 Aug 14 B Cairn 320 Call 7.85 5.3 15.0 5.7 -27.4 Hold 1-5 Days 7.85 -2.2 28 Jul 14 B Hindalco 190 Put Aug 7.75 5.5 25.0 10.0 4 Aug 14 29.0 Premature Profit Booked 3-7 Days 7.75 2.3 Update of Momentum / Intra Day/Futures Calls: Date B/S Positional Call Entry at Sloss Targets Exit Price / CMP Exit Date % G/L Comments Time Horizon Avg. Entry Abs. Gain/Loss 6-Aug-14 B Munjal Showa 140, 146 137.0 160.0 153.5 6-Aug-14 5.1 Premature Profit Booked 2-3 days 146.00 7.5 6-Aug-14 B Naukri 725.35 695.0 800.0 748.0 6-Aug-14 3.1 Premature Profit Booked 1-5 days 725.35 22.7 6-Aug-14 B Cosmo Films 82.50 79.0 89.0 83.5 1.2 Hold 2-3 days 82.50 1.0 6-Aug-14 B Chennaipetro 88.65 85.0 97.8 88.9 0.3 Hold 2-3 days 88.65 0.3 6-Aug-14 B Bindal Agro 33.00 31.0 37.8 33.5 1.5 Hold 2-3 days 33.00 0.5 5-Aug-14 B Jindal Poly 266.45 262.0 280.0 274.7 6-Aug-14 3.1 Premature Profit Booked 2-3 days 266.45 8.3 5-Aug-14 B Aarti Ind 228, 237.70 223.5 255.0 244.7 6-Aug-14 2.9 Premature Profit Booked 2-3 days 237.70 7.0 5-Aug-14 B JK Lashmi Cement 277.00 271.0 290.0 271.0 5-Aug-14 -2.2 Stop Loss Triggered 2-3 days 277.00 -6.0 5-Aug-14 B DCM Shreeram 183.00 174.0 195.0 191.3 5-Aug-14 4.5 Premature Profit Booked 2-3 days 183.00 8.3 5-Aug-14 B Seamec Ltd 107, 112.90 104.0 127.5 112.3 -0.5 Hold 2-3 days 112.90 -0.6 5-Aug-14 B Ranbaxy 569.00 555.0 620.0 563.0 -1.1 Hold 1-5 days 569.00 6.0 4 Aug 14 B U Flex 129.25 122.0 146.0 133.7 6-Aug-14 3.4 Premature Profit Booked 1-5 days 129.25 4.4 4-Aug-14 B Jindal Steel 271.90 264.0 284.0 276.4 5-Aug-14 1.7 Premature Profit Booked 2-3 days 271.90 4.5 4-Aug-14 B Bank of India 277.75 269.0 287.0 280.9 5-Aug-14 1.1 Premature Profit Booked 2-3 days 277.75 3.1 4 Aug 14 B Eros Media 225.50 218.0 245.0 220.0 5-Aug-14 -2.4 Exit Called 1-5 days 225.50 -5.5 4-Aug-14 B Time Techno 54.00 51.5 58.7 51.9 4-Aug-14 -4.0 Exit 2-3 days 54.00 -2.2 4 Aug 14 B Gitanjali Gems 71.15 - 69.5 67.9 78.0 69.8 -2.0 Hold 3-7 Days 71.15 -1.4 1-Aug-14 B Kolte Patil 149, 155.45 145.0 168.0 159.5 5-Aug-14 4.8 Premature Profit Booked 2-3 days 152.20 7.3 1-Aug-14 B Tata Sponge 894.50 867.0 975.0 915.0 5-Aug-14 2.3 Premature Profit Booked 2-3 days 894.50 20.5 31-Jul-14 B Anantraj 62.25 59.0 70.0 62.6 4-Aug-14 0.6 Premature Profit Booked 1-5 days 62.25 -0.4 31-Jul-14 B Graphite 111.90 106.0 120.0 108.8 1-Aug-14 -2.8 Exit Called 2-3 days 111.90 -3.2 30 Jul 14 S Short McDowell Aug Fut 2360.25 2420.0 2240.0 2396.0 4-Aug-14 -1.5 Exit Called 1-5 days 2360.25 -35.8 28-Jul-14 B Dredgecorp 440, 453.3 433.5 490.0 436.0 1-Aug-14 -2.4 Exit Called 1-5 days 446.65 -10.7 25 Jul 14 S YesBank Aug Fut. 541.50 560.0 510.0 532.3 1 Aug 14 1.7 Hold 3-7 Days 541.50 9.2 24-Jul-14 B Polaris 218.5 - 210 207.0 240.0 217.9 1 Aug 14 1.7 Premature Profit Booked 2-3 days 214.25 3.7 23-Jul-14 B Vakaragee 137, 144.5 134.0 160.0 136.5 -3.0 Hold 2-3 days 140.75 -4.3 10-Jul-14 B Jain Irrigation Fut 118.3 112 130 114.9 -2.7 Hold 7-Days 118.1 -3.2 8 Jul 14 B TV 18 Broadcast 32 30 36 31.2 -2.5 Hold 7-Days 32 -0.8 Update of Positional Calls: Date B/S Positional Call Entry at Sloss Targets Exit Price / CMP Exit Date % G/L Comments Time Horizon Avg. Entry Abs. Gain/Loss 6 Aug 14 B BHEL 234.00 222.0 260.0 229.3 -2.0 Hold 5-7 days 234.00 -4.8 1 Aug 14 S TATA Power Aug Fut. 97.25 88.0 105.0 96.4 0.9 Hold 3-10 Days 97.25 0.9 30-Jul-14 B Think Soft 455, 484 438.0 590.0 438.0 1-Aug-14 -6.7 Stop Loss Triggered 5-7 days 469.50 -31.5 25 Jul 14 S IRB Infra Aug Fut. 251.60 266.0 206.0 266.0 5-Aug-14 -5.4 Stop Loss Triggered 2 Weeks 251.60 -14.4 23-Jul-14 B Infy 3,307.00 3165.0 3800.0 3517.0 6.4 Hold 40-75 days 3,307.0 210.0 HDFC securities Limited, I Think Techno Campus, Building –B, ”Alpha”, Office Floor 8, Near Kanjurmarg Station, Opp. Crompton Greaves, Kanjurmarg (East), Mumbai 400 042 Fax: (022) 30753435 Disclaimer: This document has been prepared by HDFC securities Limited and is meant for sole use by the recipient and not for circulation. This document is not to be reported or copied or made available to others. It should not be considered to be taken as an offer to sell or a solicitation to buy any security. The information contained herein is from sources believed reliable. We do not represent that it is accurate or complete and it should not be relied upon as such. We may have from time to time positions or options on, and buy and sell securities referred to herein. We may from time to time solicit from, or perform investment banking, or other services for, any company mentioned in this document. This report is intended for Retail Clients only and not for any other category of clients, including, but not limited to, Institutional Clients