1. RETAIL RESEARCH Page | 1

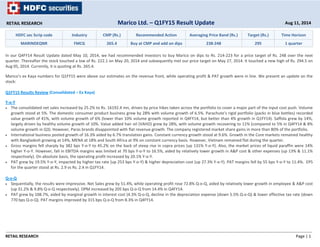

HDFC sec Scrip code Industry CMP (Rs.) Recommended Action Averaging Price Band (Rs.) Target (Rs.) Time Horizon

MARINDEQNR FMCG 265.4 Buy at CMP and add on dips 238‐248 295 1 quarter

In our Q4FY14 Result Update dated May 10, 2014, we had recommended investors to buy Marico on dips to Rs. 214‐223 for a price target of Rs. 248 over the next

quarter. Thereafter the stock touched a low of Rs. 222.1 on May 20, 2014 and subsequently met our price target on May 27, 2014. It touched a new high of Rs. 294.5 on

Aug 05, 2014. Currently, it is quoting at Rs. 265.4.

Marico’s ex Kaya numbers for Q1FY15 were above our estimates on the revenue front, while operating profit & PAT growth were in line. We present an update on the

stock:

Q1FY15 Results Review (Consolidated – Ex Kaya)

Y‐o‐Y

• The consolidated net sales increased by 25.2% to Rs. 16192.4 mn, driven by price hikes taken across the portfolio to cover a major part of the input cost push. Volume

growth stood at 5%. The domestic consumer product business grew by 28% with volume growth of 6.5%. Parachute’s rigid portfolio (packs in blue bottles) recorded

value growth of 41%, with volume growth of 6% (lower than 10% volume growth reported in Q4FY14, but better than 4% growth in Q1FY14). Saffola grew by 14%,

largely driven by healthy volume growth of 10%. Value added hair oil (VAHO) grew by 28%, with volume growth recovering to 11% (compared to 5% in Q4FY14 & 8%

volume growth in Q3). However, Paras brands disappointed with flat revenue growth. The company registered market share gains in more than 80% of the portfolio.

• International business posted growth of 16.3% aided by 6.7% translation gains. Constant currency growth stood at 9.6%. Growth in the Core markets remained healthy

with Bangladesh growing at 14%, MENA at 18% and South Africa at 9% on constant currency basis. However, Vietnam remained flat during the quarter.

• Gross margins fell sharply by 382 bps Y‐o‐Y to 45.2% on the back of steep rise in copra prices (up 131% Y‐o‐Y). Also, the market prices of liquid paraffin were 14%

higher Y‐o‐Y. However, fall in EBITDA margins was limited at 70 bps Y‐o‐Y to 16.5%, aided by relatively lower growth in A&P cost & other expenses (up 13% & 11.1%

respectively). On absolute basis, the operating profit increased by 20.1% Y‐o‐Y.

• PAT grew by 19.5% Y‐o‐Y, impacted by higher tax rate (up 253 bps Y‐o‐Y) & higher depreciation cost (up 27.3% Y‐o‐Y). PAT margins fell by 55 bps Y‐o‐Y to 11.4%. EPS

for the quarter stood at Rs. 2.9 vs Rs. 2.4 in Q1FY14.

Q‐o‐Q

• Sequentially, the results were impressive. Net Sales grew by 51.4%, while operating profit rose 72.8% Q‐o‐Q, aided by relatively lower growth in employee & A&P cost

(up 31.2% & 9.8% Q‐o‐Q respectively). OPM increased by 205 bps Q‐o‐Q from 14.4% in Q4FY14.

• PAT grew by 108.7%, aided by marginal growth in interest cost (4.3% Q‐o‐Q, decline in the depreciation expense (down 5.5% Q‐o‐Q) & lower effective tax rate (down

770 bps Q‐o‐Q). PAT margins improved by 315 bps Q‐o‐Q from 8.3% in Q4FY14.

RETAIL RESEARCH Aug 11, 2014Marico Ltd. – Q1FY15 Result Update

2. RETAIL RESEARCH Page | 2

Quarterly Financials: Consolidated (ex‐ Kaya)

(Rs. in Million)

Particulars Q1FY15 Q1FY14 VAR [%] Q4FY14 VAR [%] Remarks

Net Sales 16192.4 12930 25.2 10698.2 51.4

• The overall growth was driven by price hikes taken across the portfolio to cover a major

part of the input cost push. Volume growth stood at 5%. The domestic consumer product

business grew by 28%, led by strong value growth in Parachute and VAHO (up 41% & 28%

Y‐o‐Y respectively.

• International business grew by 16.3% aided by 6.7% translation gains. Constant currency

growth stood at 9.6% with healthy growth (in CC) across key markets like Bangladesh (up

14%), MENA (at 18%) and South Africa (up 9%).

Other Operating Income 38.9 30 29.7 22.4 73.7

Total Operating Income 16231.3 12960 25.2 10720.6 51.4

Total Expenditure 13564.8 10740 26.3 9177.9 47.8

Raw Material Consumed 7863.9 5580 40.9 6005.3 30.9

The material cost to net sales rose 383 bps Y‐o‐Y & 271 bps Q‐o‐Q to 55%. Gross margins

fell sharply on the back of steep rise in copra prices (up 131% Y‐o‐Y). Also, prices of Liquid

Paraffin were up 14% Y‐o‐Y.

Stock Adjustment 730.9 740 ‐1.2 ‐697.1 ‐204.9

Purchase of Finished Goods 316.1 300 5.4 289 9.4

Employee Expenses 854.5 730 17.1 651.3 31.2

Advertisement & Sales Promotion 1921.8 1700 13.0 1219.1 57.6

ASP cost / Net Sales fell by 128 bps Y‐o‐Y, but rose 47 bps Q‐o‐Q to 11.4%. The Y‐o‐Y fall

was due to high inflation led topline growth. The Company expects to operate in a band of

11‐12% in the medium term.

Other Expenses 1877.6 1690 11.1 1710.3 9.8

Operating Profit 2666.4 2220 20.1 1542.7 72.8

Other Income 183.2 140 30.9 128.4 42.7

Interest 70.4 100 ‐29.6 67.5 4.3

PBDT 2779.3 2260 23.0 1603.6 73.3

Depreciation 203.7 160 27.3 215.5 ‐5.5

Y‐o‐Y rise in depreciation cost was due to adoption of the useful life of fixed assets as per

Schedule II of Companies Act 2013, effective April 1, 2014 (Rs.2.65 cr), fixed asset additions

made during the year and impairment of fixed assets in Egypt and Bangladesh.

PBT 2575.5 2100 22.6 1388.1 85.5

Tax (incl. DT & FBT) 678.5 500 35.7 472.6 43.6

The effective tax rate on PBT increased by 253 bps Y‐o‐Y, but fell by 770 bps Q‐o‐Q to

26.3%. The Y‐o‐Y rise in the ETR is primarily due to one of the factories in India going out of

tax exemption and another is moving into 30% exemption bracket from 100% exemption.

Also, from this year, there has been an increase in tax rate in Vietnam. The expected ETR

during FY15 and FY16 could be around 28‐29%.

PAT (before minority interest) 1897.0 1600 18.6 915.5 107.2

Minority Interest 44.2 50 ‐11.5 27.9 58.6

PAT (net of minority interest) 1852.8 1550 19.5 887.6 108.7

Y‐o‐Y PAT growth was lower than the sales growth, impacted by lower OPM, higher

depreciation cost & higher effective tax rates.

3. RETAIL RESEARCH Page | 3

EPS (Rs.) 2.9 2.4 19.5 1.4 108.7

Equity 644.9 644.8 0.0 644.9 0.0

FV 1.0 1.0 0.0 1.0 0.0

OPM (%) 16.5 17.2 ‐4.1 14.4 14.2

EBITDA margins contraction was limited at 70 bps Y‐o‐Y to 16.5%, helped by relatively

lower growth in A&P cost & other expenses. While the overall margins contracted, the

OPM of international business improved by 490 bps to 18.2% reflecting a structural shift in

international margins based on the cost management projects undertaken last year.

PATM (%) 11.4 12.0 ‐4.5 8.3 37.9

(Source: Company, HDFC sec)

Other Developments / Highlights

• The non‐focused part of the parachute portfolio (pouch packs) witnessed de‐growth as input prices faced inflationary pressures while the Company maintained

minimum threshold margins. It is generally observed that an inflationary environment swings the competitive position to the Company's advantage as it puts pressure

on the working capital requirements of marginal players. During the 12 months ended June 2014, Parachute along with Nihar increased its market share by 50bps to

56%. Parachute's share in the rural markets, in the range of 35‐40%, is lower than that in the urban markets, thus providing potential headroom for growth.

• Market share of Saffola declines 200bps Y‐o‐Y to 55%, thus indicating increased competitive intensity. However, Saffola Oats has emerged as a strong no.2 brand in the

oats category with a value market share of 17%. Two sweet flavours with fruits were introduced to compliment the bouquet of six savory flavors. Focus on value added

offerings in the oats segment has enabled the Company to capture 51% share in the flavored oats market. The Company launched a new campaign on Masala Oats this

quarter, the initial response to which has been very positive. The Company expects to reach a top line of ~Rs 70‐75 crore (USD 12‐13 mn) in this fiscal for the franchise

and is poised to cross Rs. 1 bn (USD 17 mn) landmark next year.

• In VAHO, the company continues to grow faster than the market and has emerged as a clear market leader with 28% share (for 12 months ended June 2014) as against

27% during the same period last year. Nihar Shanti Amla continues to gain market share and achieved a volume market share of about 30% for the 12 months ended

June 2014 in the Amla hair oils category (MAT Q1FY14: 27%).

• Sales in Modern Trade (9% of the domestic turnover) continued its good run and grew by 27%. Rural growth (33% Y‐o‐Y) continues to outperform urban (25% Y‐o‐Y) as

rural now contributes 30% to total domestic sales.

• As per the management, its key focus in the current scenario would be on improving volume growth over profitability. It has guided for 7‐8% volume growth and 14.5‐

15% EBITDA margin band for FY15 though it expects next two quarters to witness margin pressure on account of sustained copra inflation.

• Due to a spurt in copra prices from mid‐2013 onwards, the company has initiated a series of price increases. A weighted average price increase of 19% over Q4FY14

was taken during the quarter. This, coupled with price increases taken last year, has led to a weighted average price increase of 33%. The given price increases would

partially offset the rise in copra prices.

• The company plans to double its revenues over the next four years driven by a mix of organic and inorganic growth. It plans to become an emerging market MNC with

focus on Asia and Africa in key categories of hair care, skin nourishment and male grooming. It has identified give key areas of transformation—innovation, GTM,

Talent Value Proposition, IT & Analytics and Cost Management.

4. RETAIL RESEARCH Page | 4

Conclusion & Recommendation:

Marico’s ex Kaya numbers for Q1FY15 were above our estimates on the revenue front, while operating profit & PAT growth were in line. The growth was largely led by

price hikes taken across the portfolio to cover a major part of the input cost push. Volume growth stood at 5%. Strong growth in domestic consumer product business (up

28% Y‐o‐Y, aided by strong value growth in parachute and VAHO) and decent growth in international business revenues (led by double digit growth in Bangladesh &

MENA) despite challenging environment was encouraging. Further, the volume growth recovery in domestic business witnessed in Q4FY14 was sustained in Q1FY15

despite challenging environment (though in single digits). On the profit front, while the sharp contraction in gross margins (down 382 bps Y‐o‐Y), impacted by steep rise in

copra prices was discomforting, the overall OPM contraction was limited (at 70 bps Y‐o‐Y), aided by relatively lower growth in A&P cost & other expenses.

We expect volume growth of Parachute (rigid pack) to improve gradually from 6% (which was healthy in our view considering steep rise in copra prices) to 7‐8% in the

coming quarters, likely to be driven by conversion from loose coconut oil to branded coconut oil and rural market share gains. We feel that an inflationary environment

swings the competitive position to the company’s advantage as it puts pressure on the working capital requirements of marginal regional players. This leads to market

share gain and better volume growth. While volume growth recovery in VAHO (compared to Q3FY14 & Q4FY14) is encouraging, its sustainability is essential. With

company’s efforts to increase the distribution reach in rural market and shift in consumer preference towards living a healthy lifestyle, we expect Saffola’s volume growth

to remain healthy in double digits (expected to improve gradually from 10% currently).

Sharp rise in the Copra prices would continue to put pressure on Marico’s overall gross margins in near to medium term. However, price hikes initiated in parachute

(weighted average price increase of 33% Y‐o‐Y) and in VAHO (weightage average price hikes of 6% Y‐o‐Y across portfolio) would restrict a sharp deceleration in margins.

Further, cost rationalisation would limit the contraction in OPM in FY15. However, we expect gradual uptick in margins in FY16, since we expect stability in Copra prices.

We feel Marico could surpass our revenue estimates in FY15. Hence we are enhancing the same by 4.9%. However, it seems to be on track to meet our operating profit &

PAT growth. Hence we are keeping the same unchanged (since margins could be lower than our expectations). We have incorporated projections for FY16, wherein we

expect net sales, operating profit & PAT to grow by 16%, 19.7% & 20.8% respectively.

At the CMP, Marico trades at 25.7xFY16E EPS. Sustained improvement in the volume growth (which is a key driver for sustainable profit growth), market share gains &

profitability could result in gradual re‐rating in the stock price in the coming quarters. Valuing the stock at 28.5xFY16E EPS we arrive at a price target of Rs. 295. We feel

investors could buy the stock at current levels and average it on dips to Rs. 238‐248 (23‐24xFY16E EPS) band for our price target over the next quarter.

Financial Estimations: (Consolidated) ‐ excluding Kaya.

(Rs. in Million)

Particulars FY13 FY14 FY15 (OE)* FY15 (RE)* FY16 (E)

Net Sales 42480 46765 54169 56820 65059

Operating Profit 6010 7466 8559 8559 10247

Adjusted PAT 4053 4850 5525 5525 6669

EPS 6.3 7.5 8.6 8.6 10.3

OPM (%) 14.1 16.0 15.8 15.1 15.8

NPM (%) 9.5 10.4 10.2 9.7 10.3

PE 42.2 35.3 31.0 31.0 25.7

*OE = Original Estimates; RE = Revised Estimates (Source: Company, HDFC sec Estimates)

5. RETAIL RESEARCH Page | 5

Analyst: Mehernosh K. Panthaki – IT, FMCG & Midcaps; Email ID: mehernosh.panthaki@hdfcsec.com

RETAIL RESEARCH Tel: (022) 3075 3400 Fax: (022) 2496 5066 Corporate Office

HDFC securities Limited, I Think Techno Campus, Building - B, "Alpha", Office Floor 8, Near Kanjurmarg Station, Opp. Crompton Greaves, Kanjurmarg (East), Mumbai 400 042 Phone: (022) 3075 3400 Fax: (022)

2496 5066 Website: www.hdfcsec.com Email: hdfcsecretailresearch@hdfcsec.com

Disclaimer: This document has been prepared by HDFC Securities Limited and is meant for sole use by the recipient and not for circulation. This document is not to be reported or copied or made available to

others. It should not be considered to be taken as an offer to sell or a solicitation to buy any security. The information contained herein is from sources believed reliable. We do not represent that it is accurate or

complete and it should not be relied upon as such. We may have from time to time positions or options on, and buy and sell securities referred to herein. We may from time to time solicit from, or perform investment

banking, or other services for, any company mentioned in this document. This report is intended for non-Institutional Clients

![RETAIL RESEARCH Page | 2

Quarterly Financials: Consolidated (ex‐ Kaya)

(Rs. in Million)

Particulars Q1FY15 Q1FY14 VAR [%] Q4FY14 VAR [%] Remarks

Net Sales 16192.4 12930 25.2 10698.2 51.4

• The overall growth was driven by price hikes taken across the portfolio to cover a major

part of the input cost push. Volume growth stood at 5%. The domestic consumer product

business grew by 28%, led by strong value growth in Parachute and VAHO (up 41% & 28%

Y‐o‐Y respectively.

• International business grew by 16.3% aided by 6.7% translation gains. Constant currency

growth stood at 9.6% with healthy growth (in CC) across key markets like Bangladesh (up

14%), MENA (at 18%) and South Africa (up 9%).

Other Operating Income 38.9 30 29.7 22.4 73.7

Total Operating Income 16231.3 12960 25.2 10720.6 51.4

Total Expenditure 13564.8 10740 26.3 9177.9 47.8

Raw Material Consumed 7863.9 5580 40.9 6005.3 30.9

The material cost to net sales rose 383 bps Y‐o‐Y & 271 bps Q‐o‐Q to 55%. Gross margins

fell sharply on the back of steep rise in copra prices (up 131% Y‐o‐Y). Also, prices of Liquid

Paraffin were up 14% Y‐o‐Y.

Stock Adjustment 730.9 740 ‐1.2 ‐697.1 ‐204.9

Purchase of Finished Goods 316.1 300 5.4 289 9.4

Employee Expenses 854.5 730 17.1 651.3 31.2

Advertisement & Sales Promotion 1921.8 1700 13.0 1219.1 57.6

ASP cost / Net Sales fell by 128 bps Y‐o‐Y, but rose 47 bps Q‐o‐Q to 11.4%. The Y‐o‐Y fall

was due to high inflation led topline growth. The Company expects to operate in a band of

11‐12% in the medium term.

Other Expenses 1877.6 1690 11.1 1710.3 9.8

Operating Profit 2666.4 2220 20.1 1542.7 72.8

Other Income 183.2 140 30.9 128.4 42.7

Interest 70.4 100 ‐29.6 67.5 4.3

PBDT 2779.3 2260 23.0 1603.6 73.3

Depreciation 203.7 160 27.3 215.5 ‐5.5

Y‐o‐Y rise in depreciation cost was due to adoption of the useful life of fixed assets as per

Schedule II of Companies Act 2013, effective April 1, 2014 (Rs.2.65 cr), fixed asset additions

made during the year and impairment of fixed assets in Egypt and Bangladesh.

PBT 2575.5 2100 22.6 1388.1 85.5

Tax (incl. DT & FBT) 678.5 500 35.7 472.6 43.6

The effective tax rate on PBT increased by 253 bps Y‐o‐Y, but fell by 770 bps Q‐o‐Q to

26.3%. The Y‐o‐Y rise in the ETR is primarily due to one of the factories in India going out of

tax exemption and another is moving into 30% exemption bracket from 100% exemption.

Also, from this year, there has been an increase in tax rate in Vietnam. The expected ETR

during FY15 and FY16 could be around 28‐29%.

PAT (before minority interest) 1897.0 1600 18.6 915.5 107.2

Minority Interest 44.2 50 ‐11.5 27.9 58.6

PAT (net of minority interest) 1852.8 1550 19.5 887.6 108.7

Y‐o‐Y PAT growth was lower than the sales growth, impacted by lower OPM, higher

depreciation cost & higher effective tax rates.](data:image/gif;base64,R0lGODlhAQABAIAAAAAAAP///yH5BAEAAAAALAAAAAABAAEAAAIBRAA7)