GST- Refund process under GST brief

•Download as PPTX, PDF•

1 like•547 views

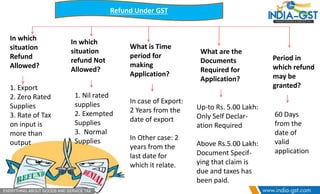

Refunds under GST are allowed for exports, zero-rated supplies, and when input tax is greater than output tax. Refunds are not allowed for nil-rated, exempted, or normal supplies. The time period for applying for a refund is 2 years from the date of export or the last date of the filing period the refund relates to. For refunds up to Rs. 5 lakh, only a self-declaration is required, while for larger refunds documents showing tax payment are needed. The refund will be granted within 60 days of filing a valid application.

Recommended

More Related Content

What's hot

What's hot (20)

Viewers also liked

Viewers also liked (9)

Recently uploaded

Recently uploaded (20)

GST- Refund process under GST brief

- 1. Refund Under GST In which situation Refund Allowed? In which situation refund Not Allowed? What is Time period for making Application? What are the Documents Required for Application? Period in which refund may be granted?1. Export 2. Zero Rated Supplies 3. Rate of Tax on input is more than output 1. Nil rated supplies 2. Exempted Supplies 3. Normal Supplies In case of Export: 2 Years from the date of export In Other case: 2 years from the last date for which it relate. Up-to Rs. 5.00 Lakh: Only Self Declar- ation Required Above Rs.5.00 Lakh: Document Specif- ying that claim is due and taxes has been paid. 60 Days from the date of valid application

- 2. CA Nikhil Malaiya Cell: 9545727818 E-mail: canikhilmalaiya@gmail.com CA Mayur Zanwar Cell: 9422855595 E-mail: cazanwar@gmail.com