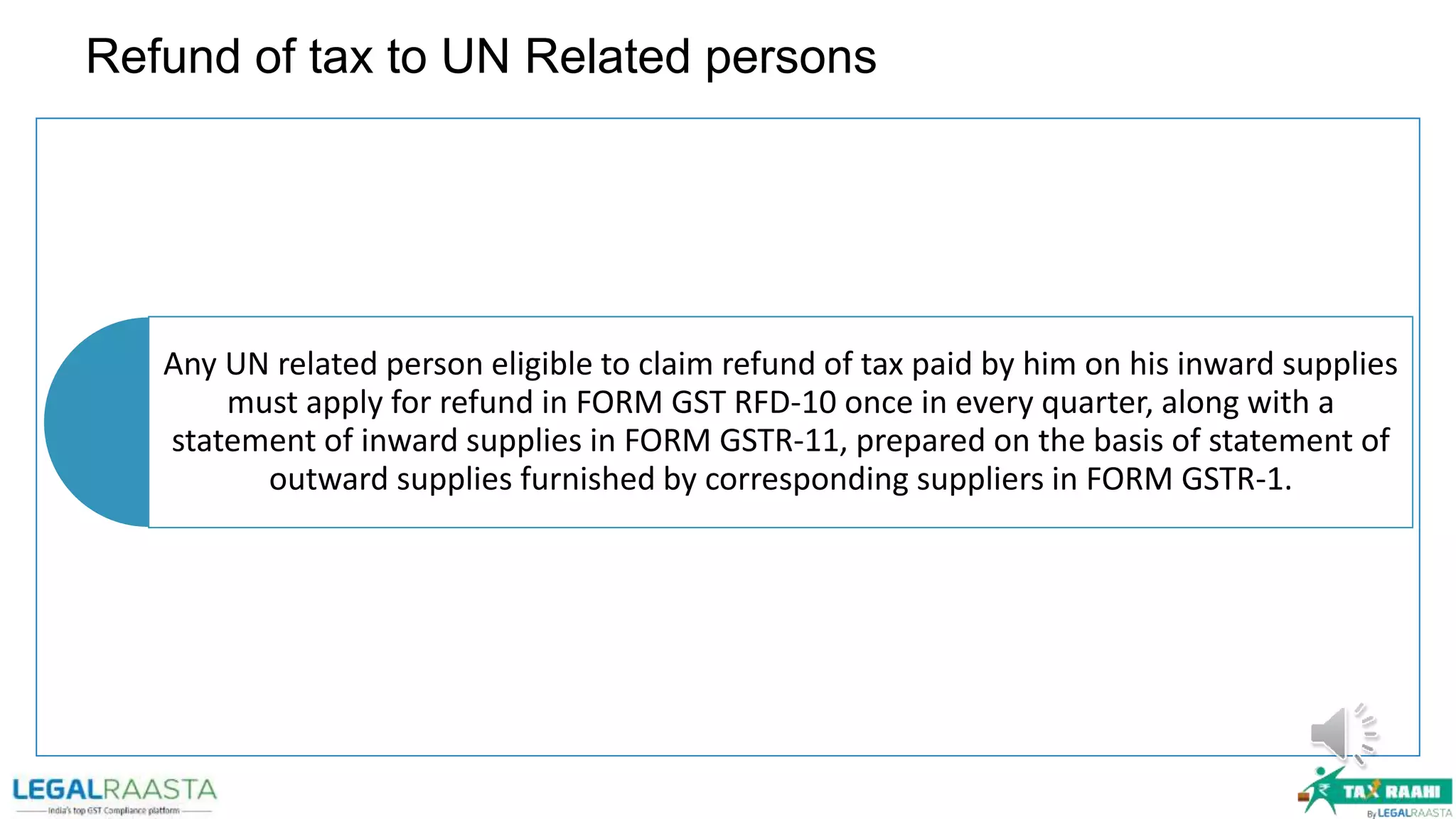

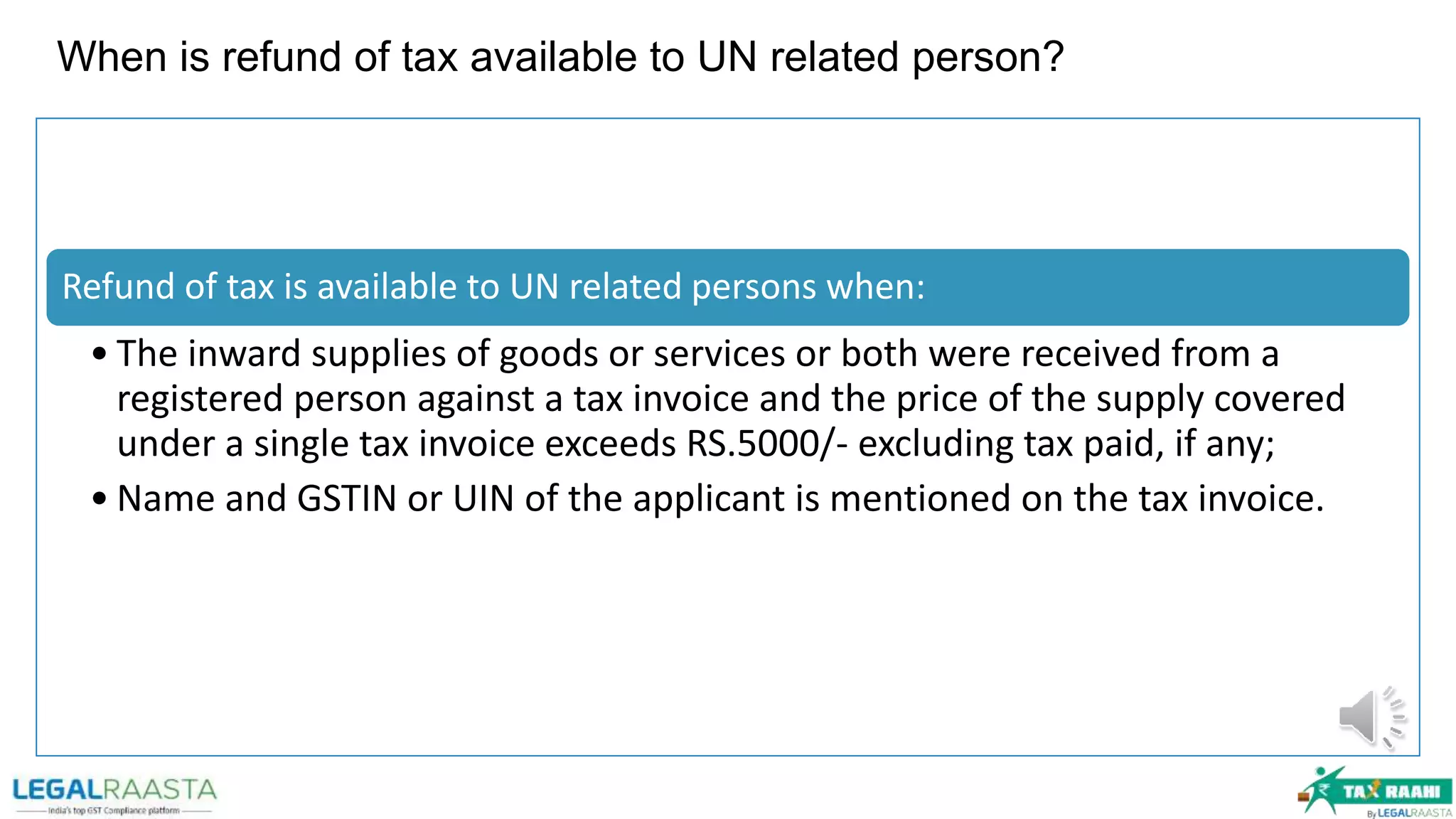

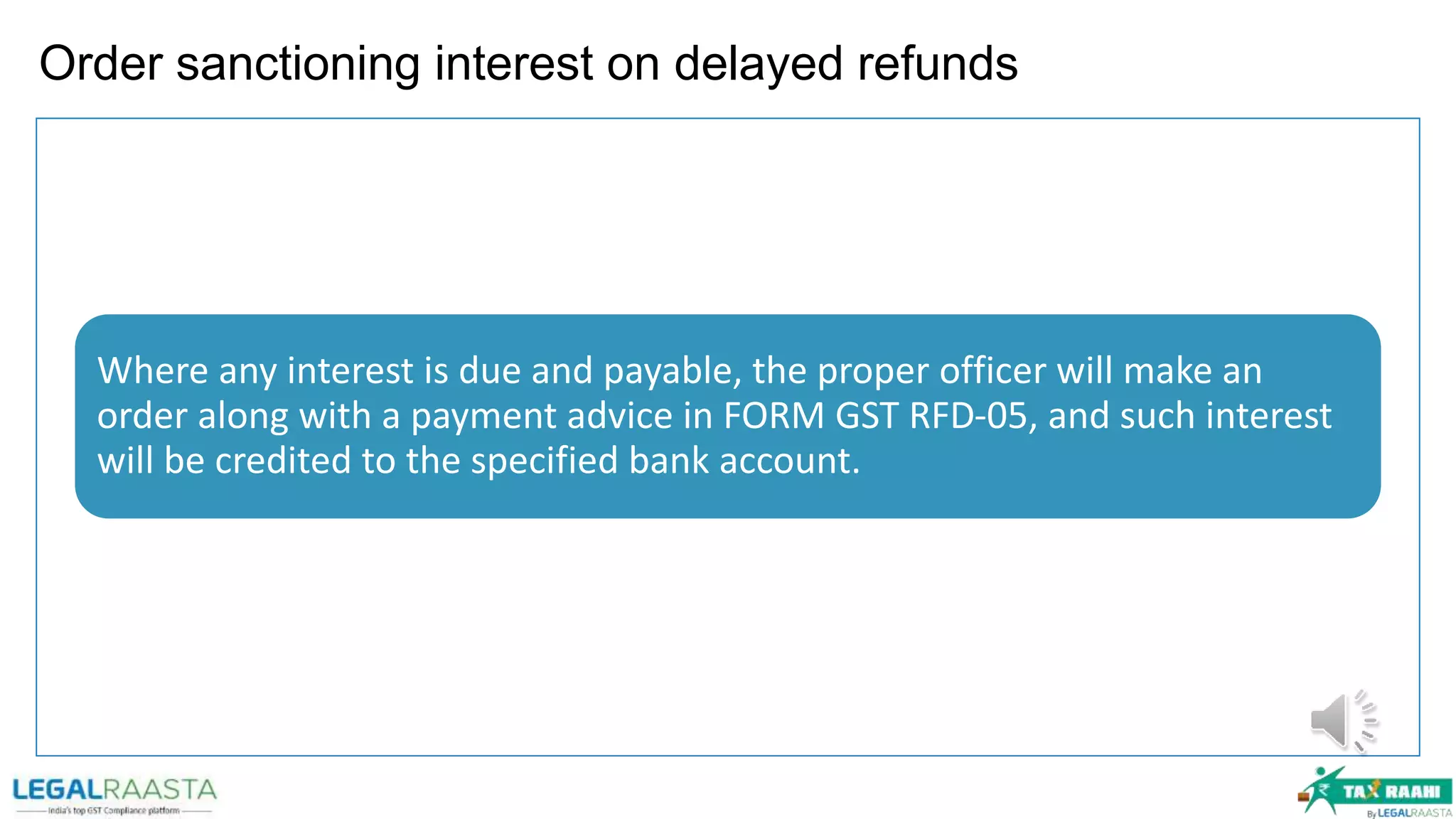

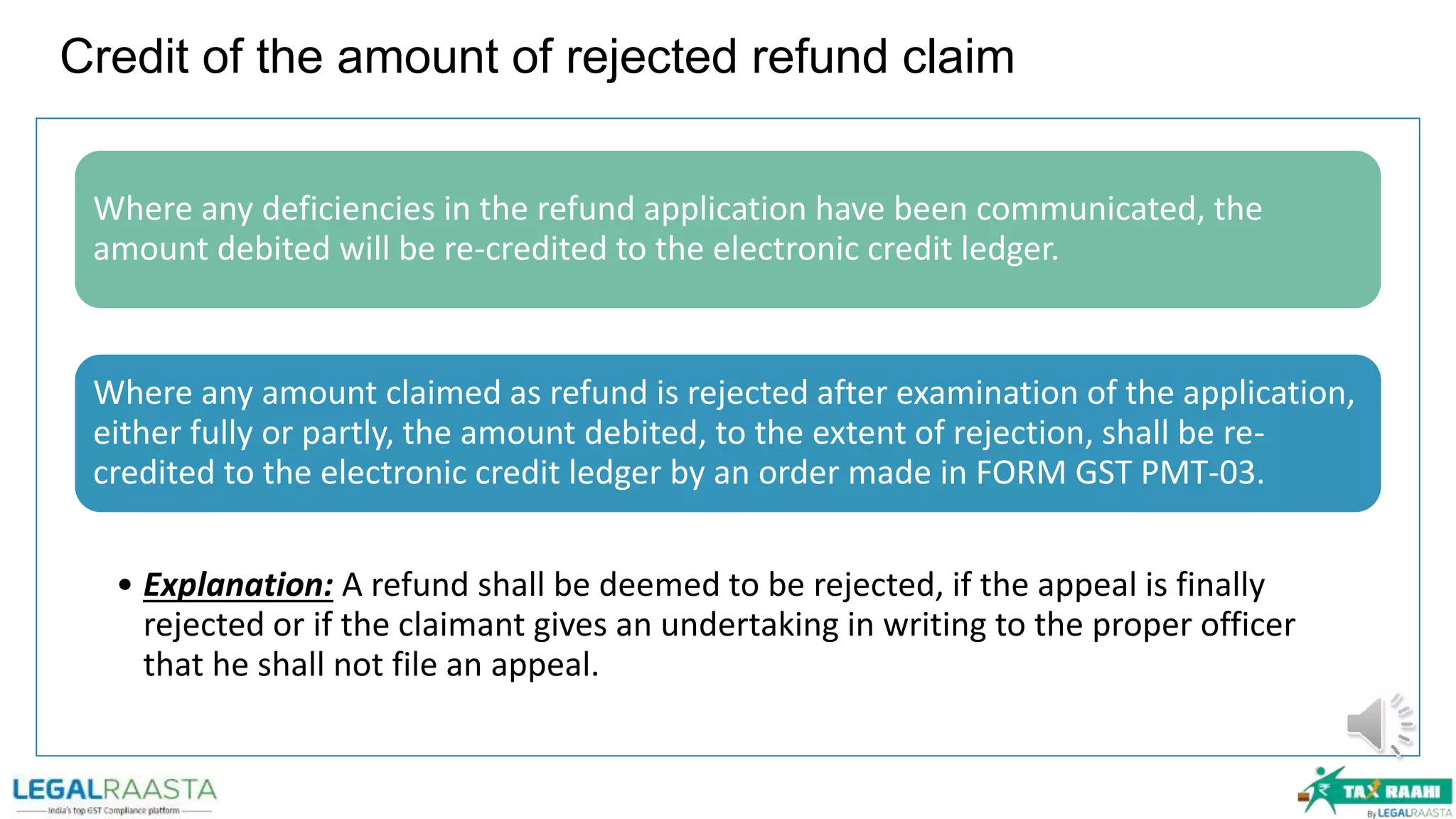

The document outlines the procedures and conditions for claiming refunds under India's Goods and Services Tax (GST) system, including the types of eligible refunds and documentation required. It specifies cases where refunds are permitted or denied and includes details on the process for unrelated persons seeking tax refunds. Additionally, it discusses the time frame for refund applications and interest on delayed refunds.