Download to read offline

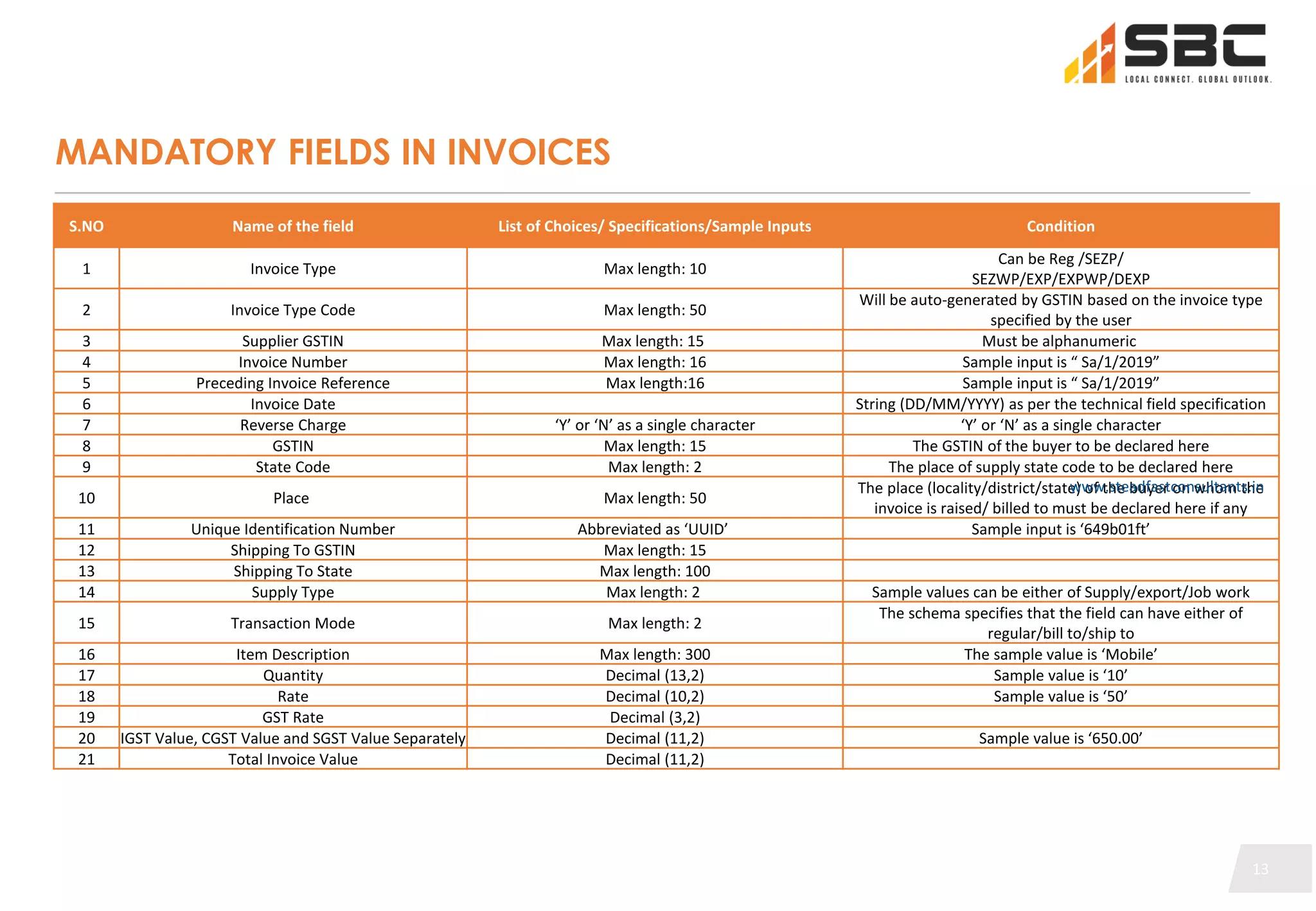

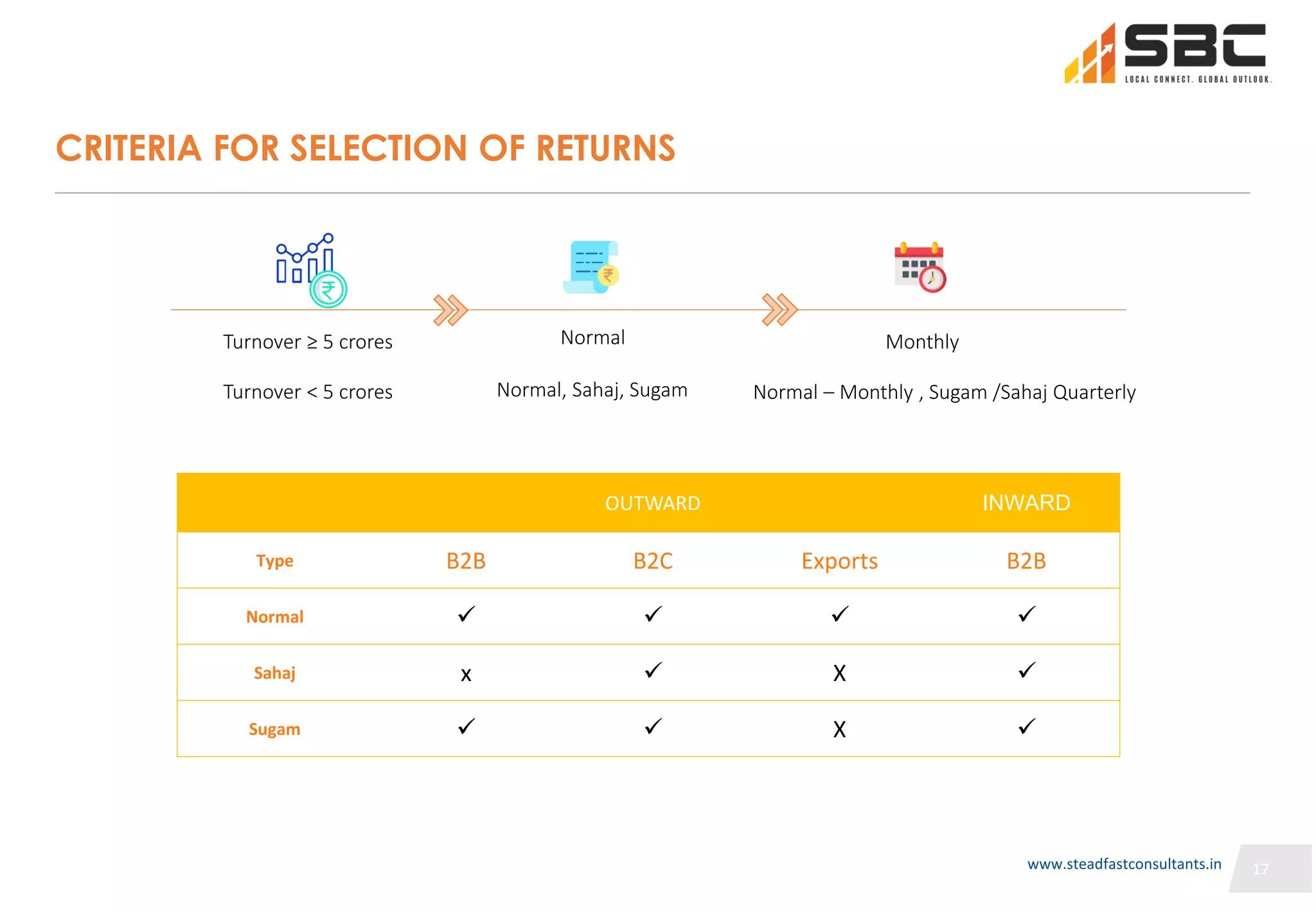

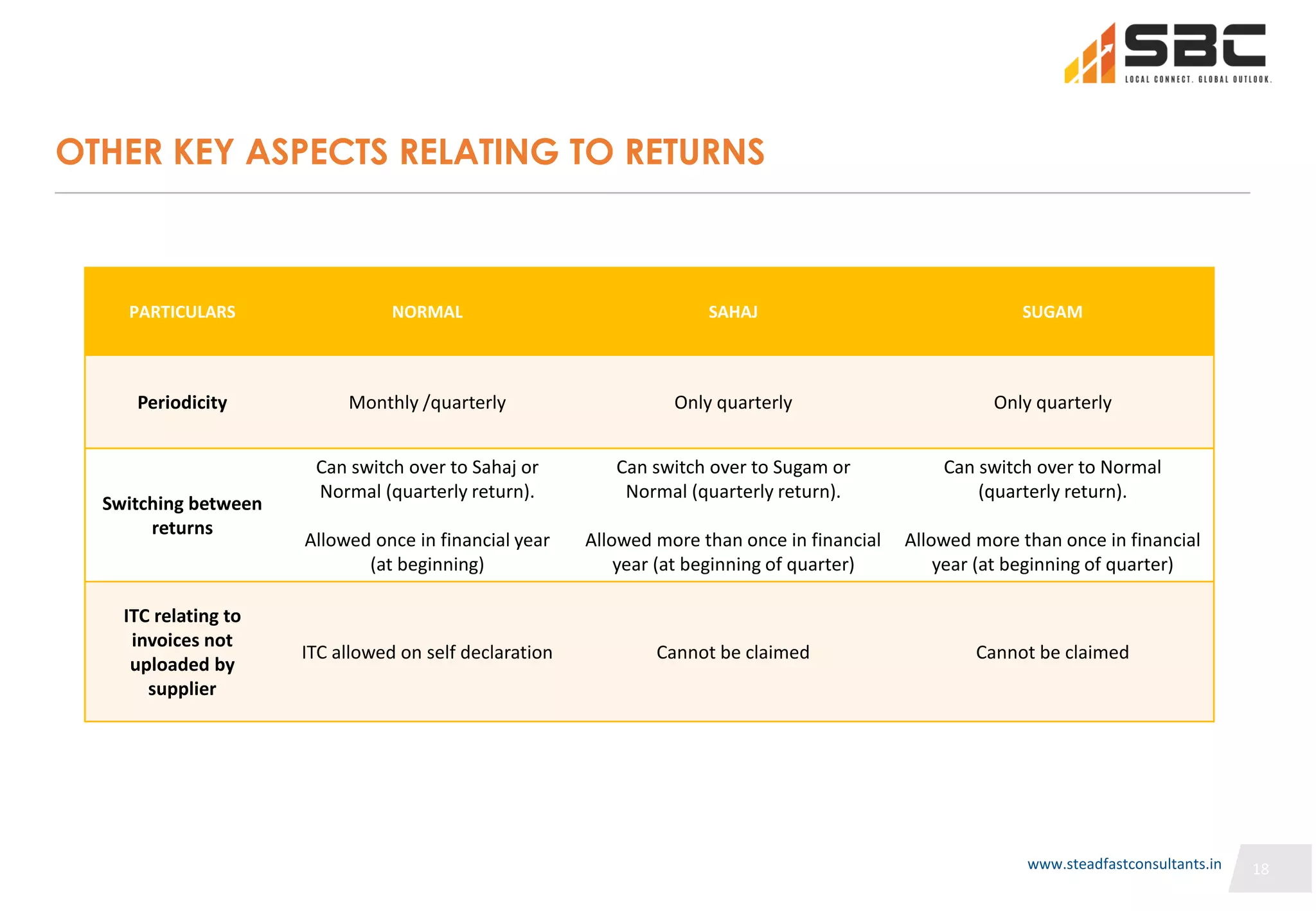

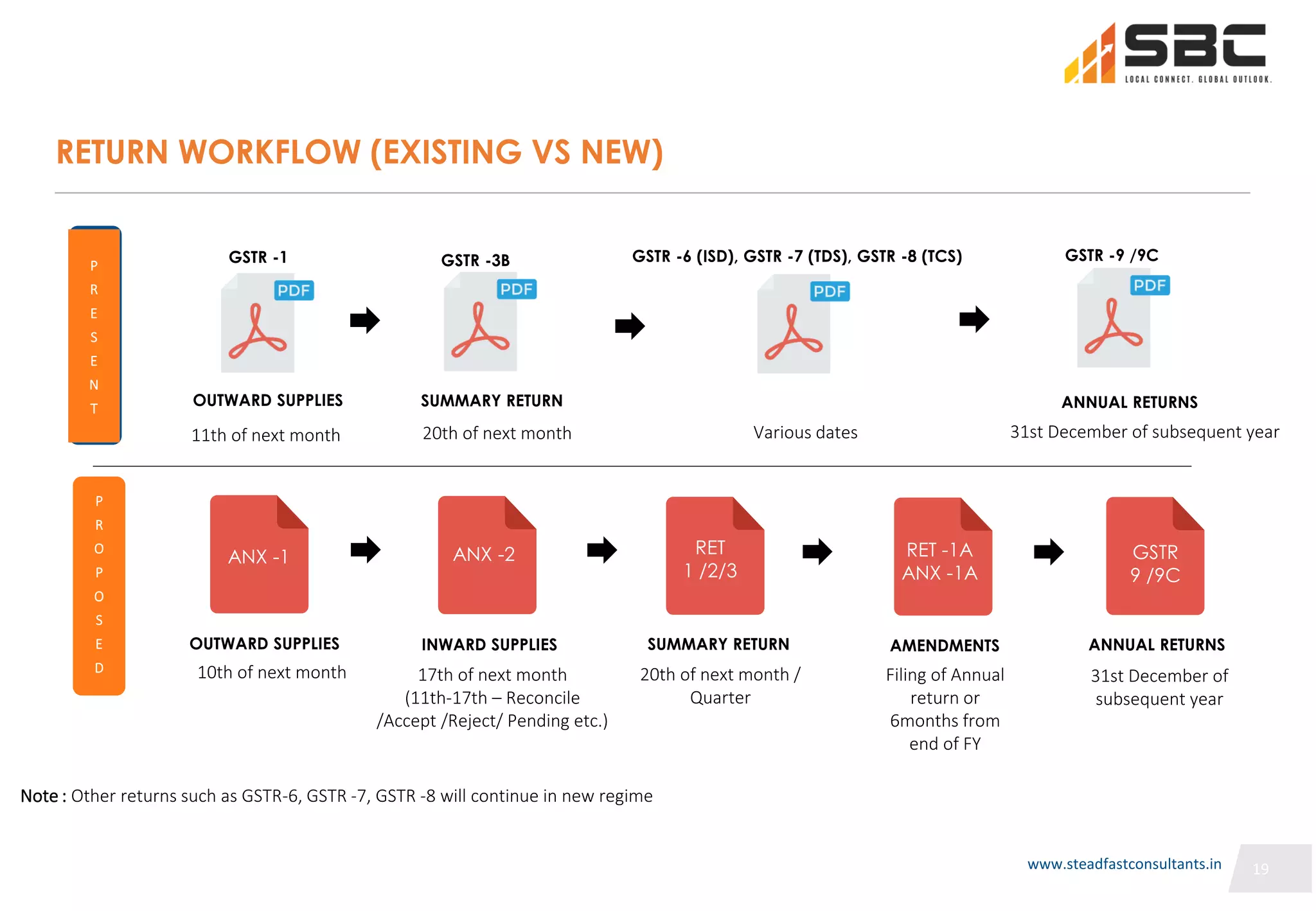

The document provides information on e-invoicing, new GST returns, and integrated GST solutions in India. It discusses the proposed e-invoicing infrastructure and process, highlighting key aspects like mandatory fields. New GST returns being introduced include Normal, Sahaj, and Sugam returns filed monthly or quarterly depending on taxpayer turnover. The document outlines differences between the existing and new return filing processes.