Download as PDF, PPTX

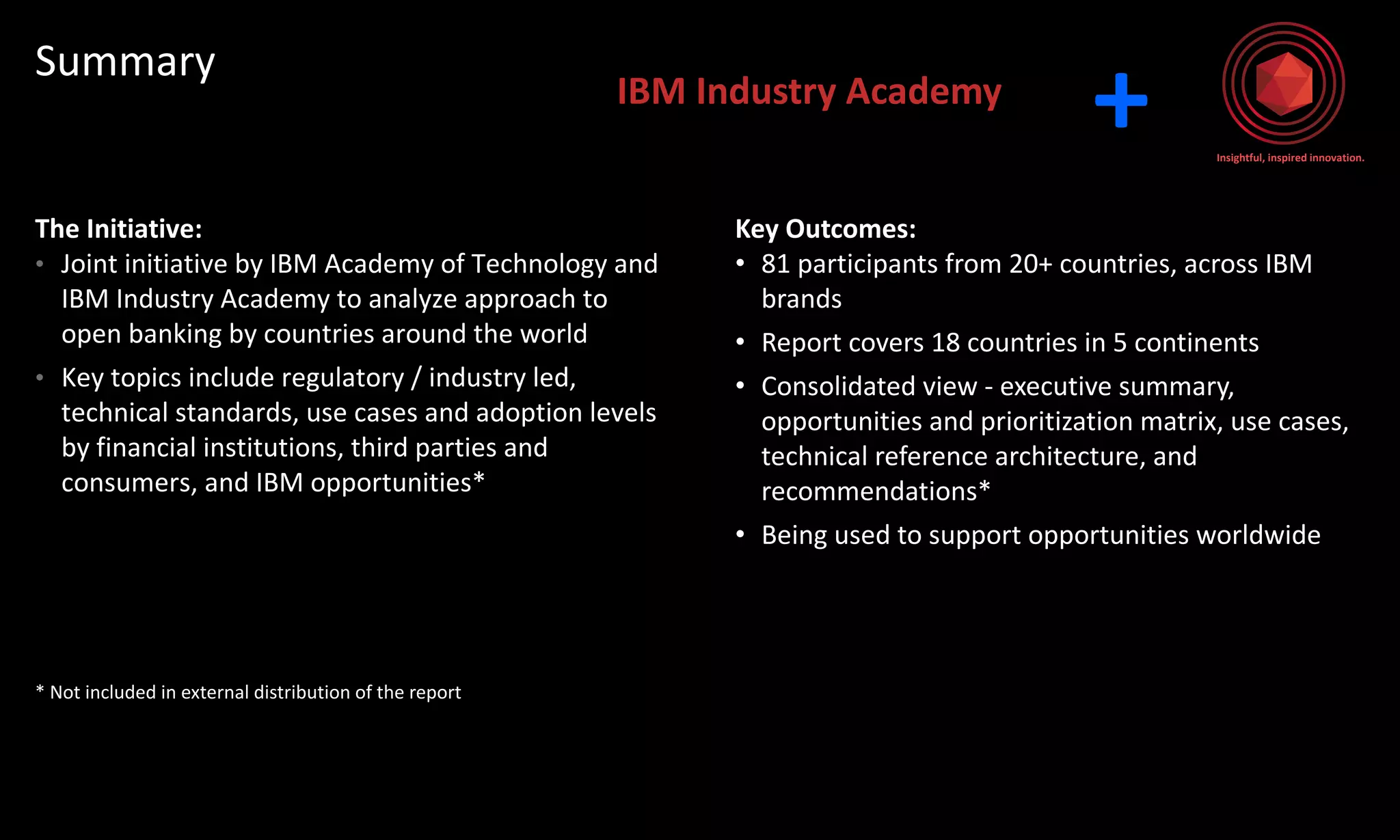

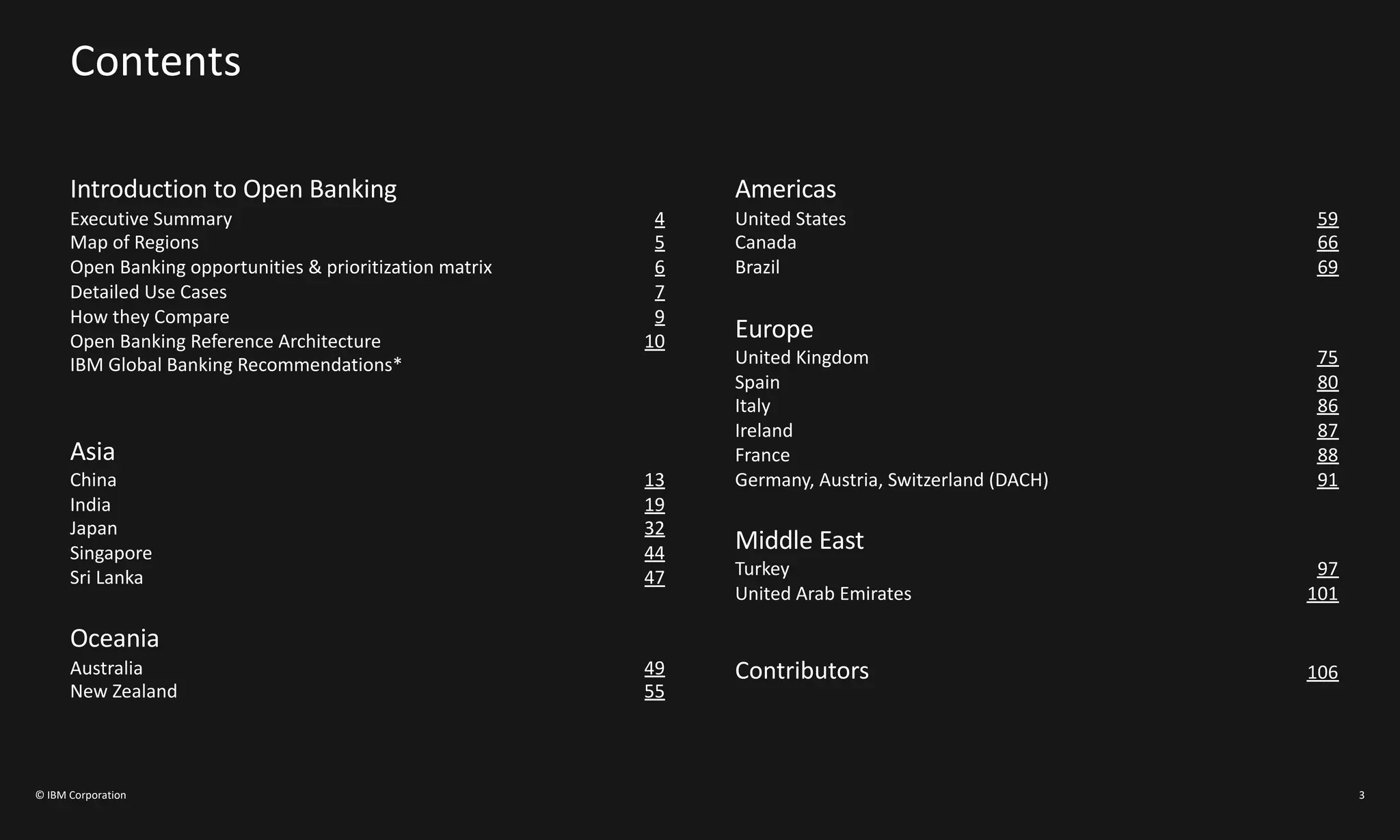

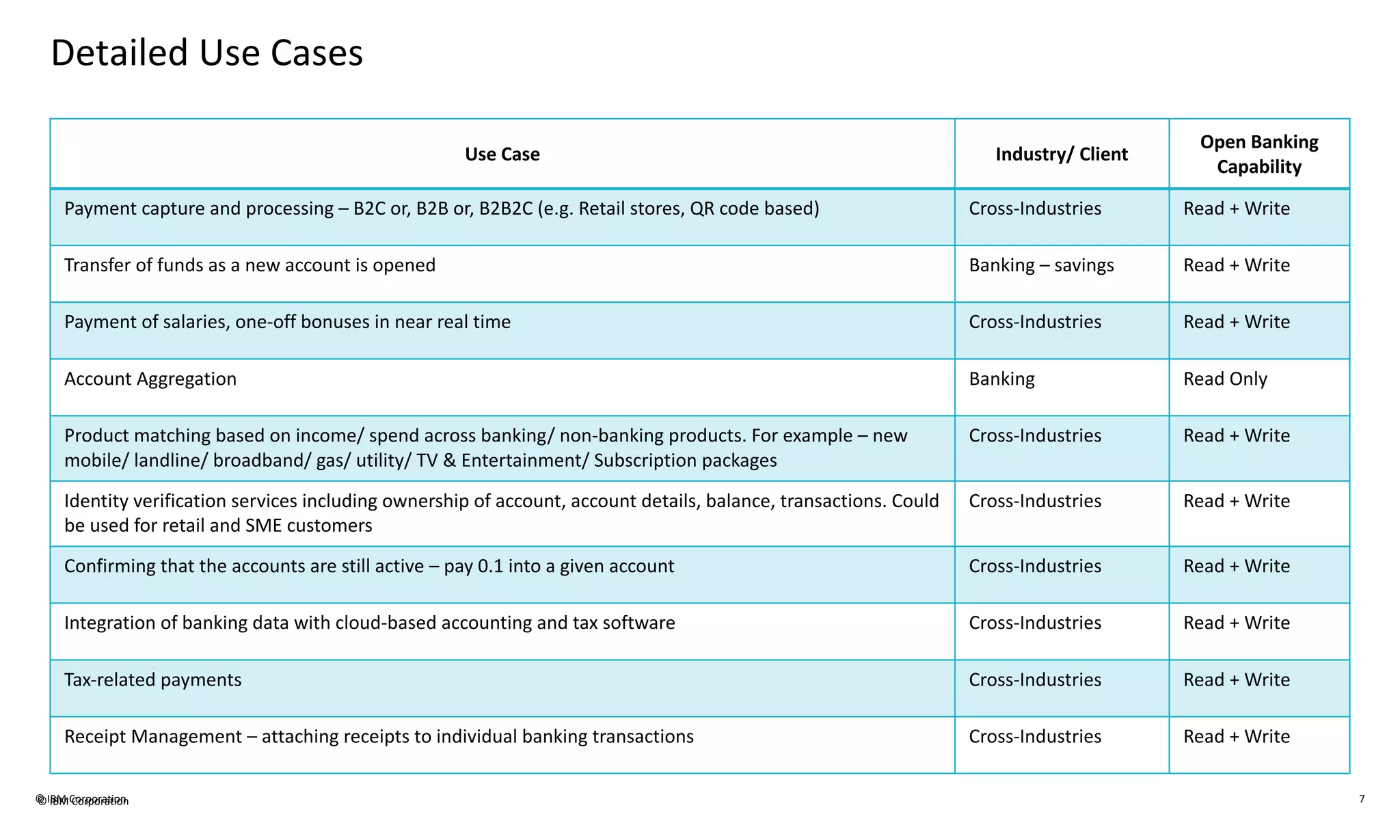

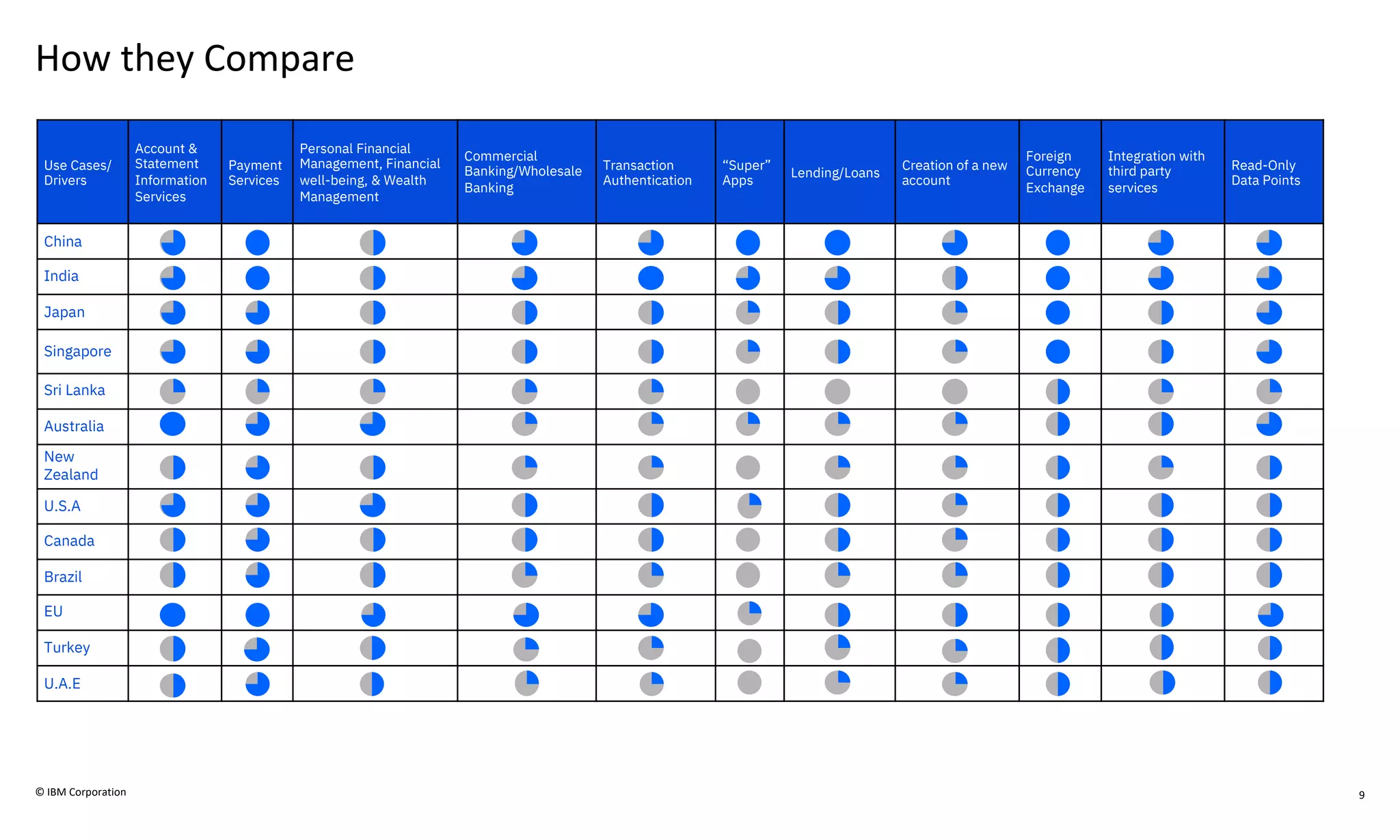

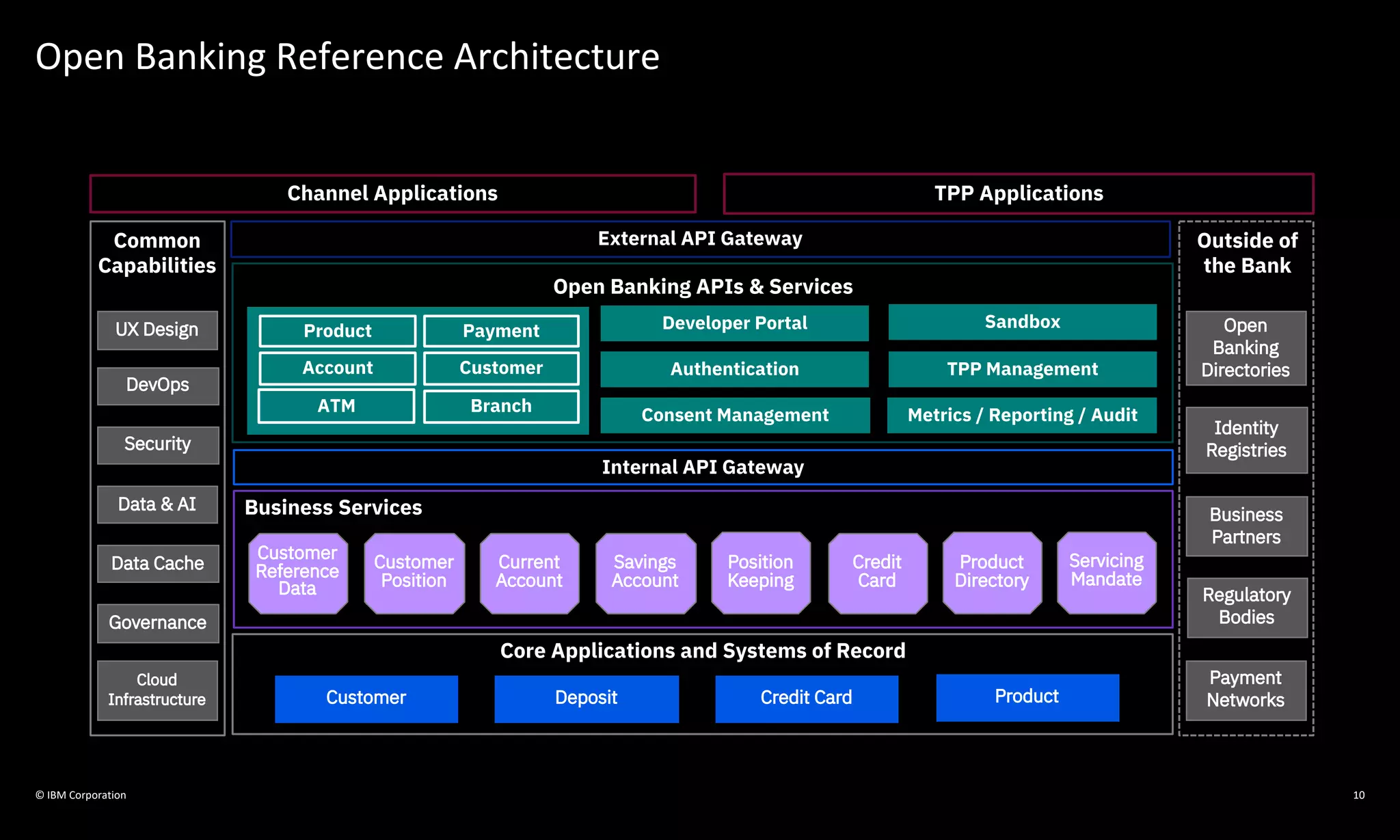

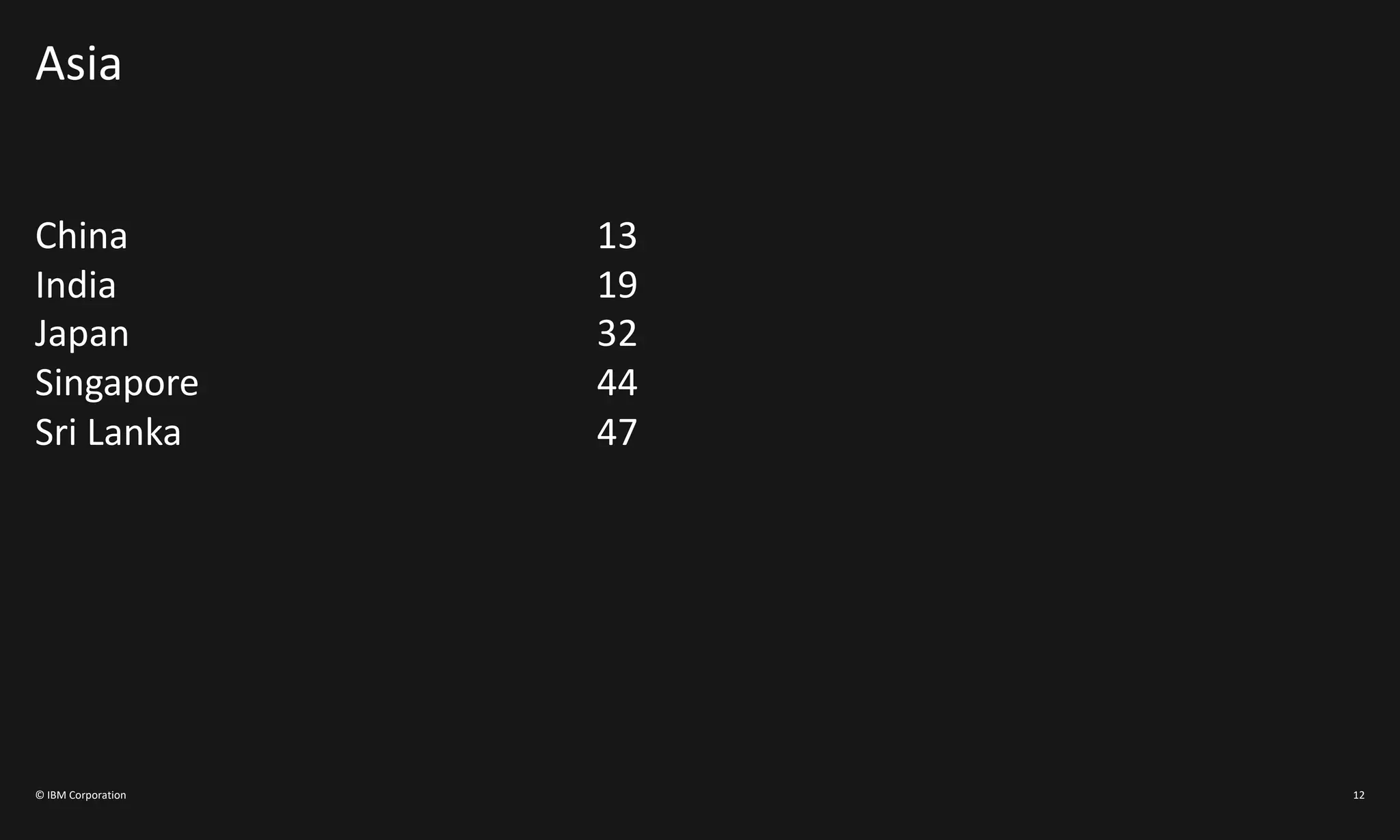

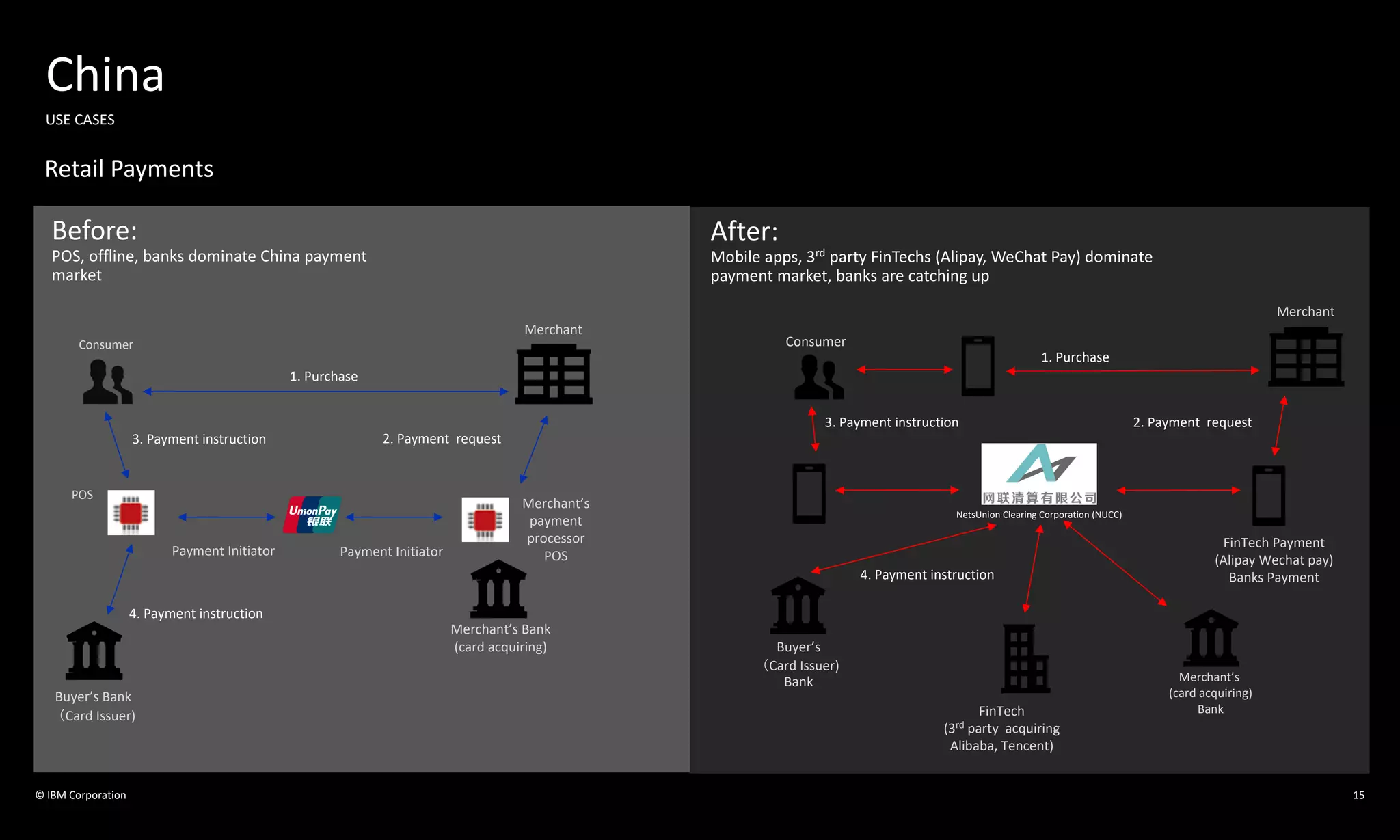

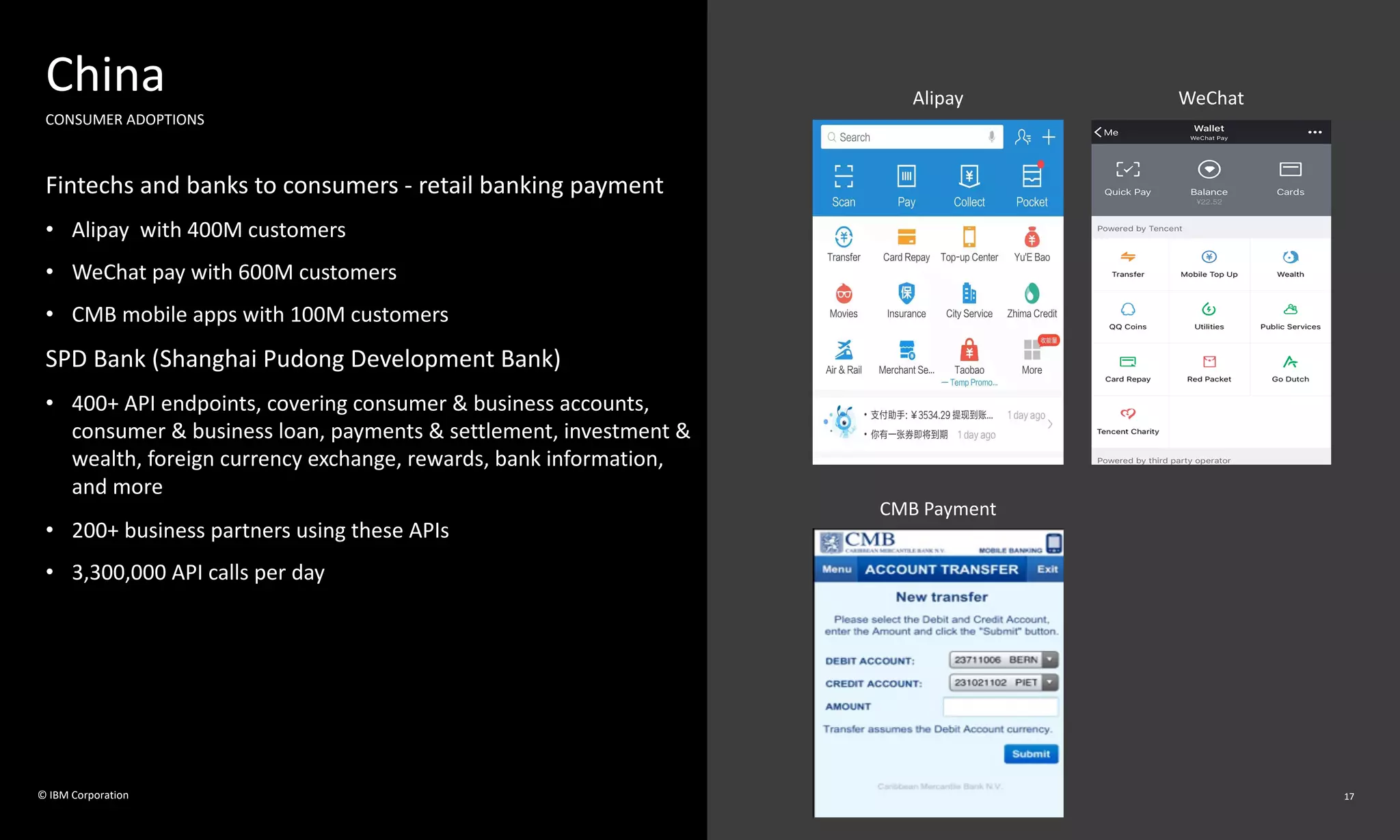

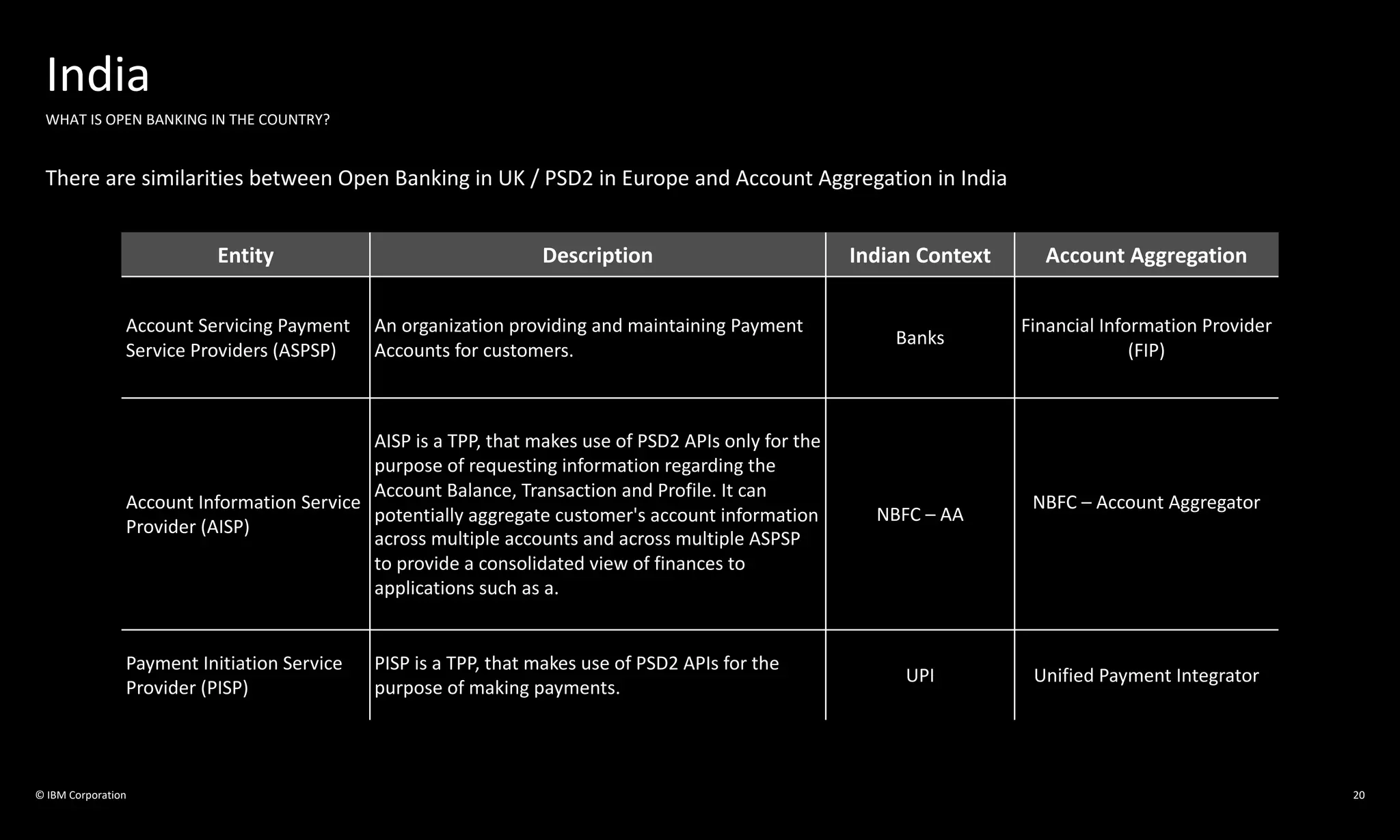

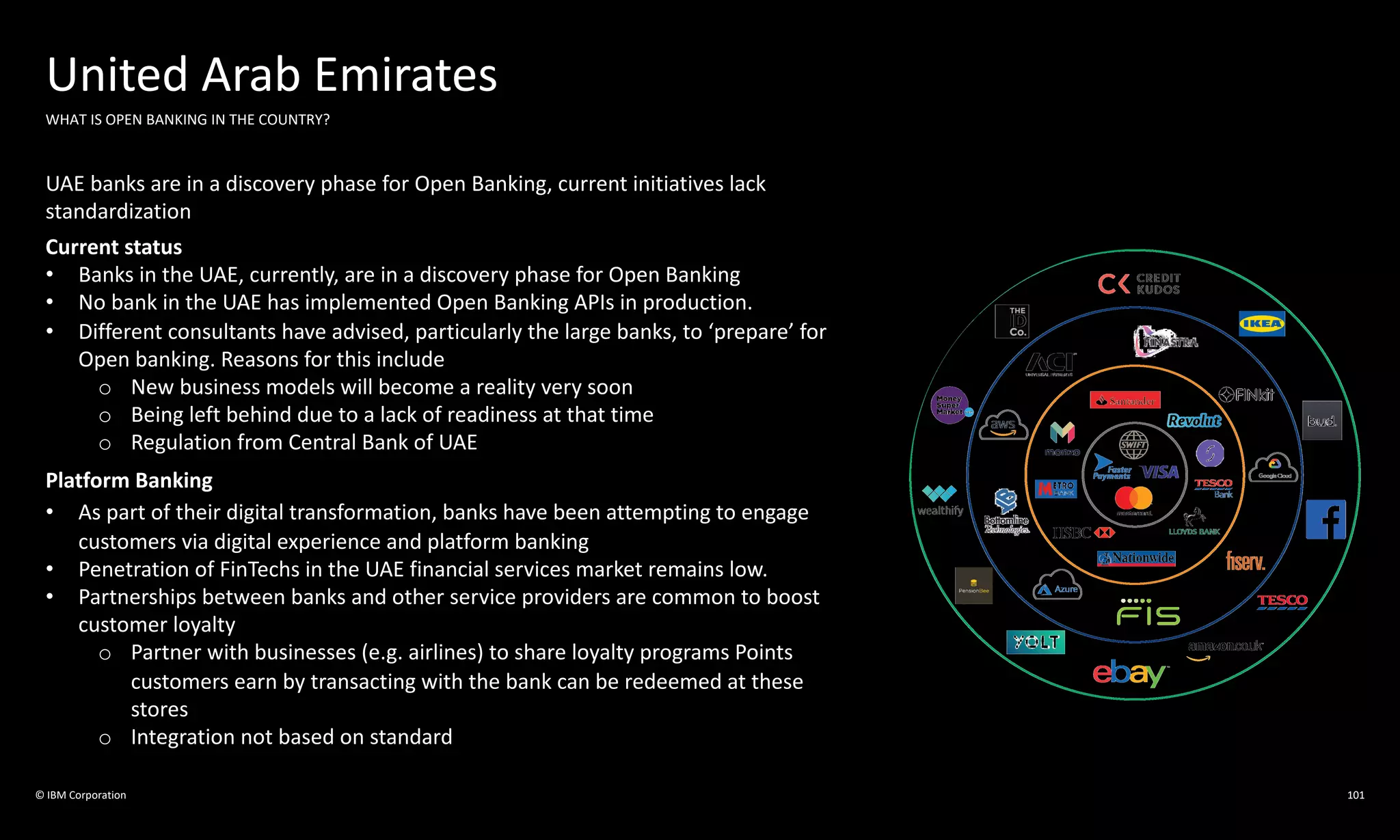

The document presents a comprehensive analysis of the global open banking landscape as of June 2020, detailing a joint initiative by IBM to evaluate the approaches of various countries towards open banking. It highlights the regulatory and market-driven initiatives, security challenges, and numerous use cases across multiple regions, alongside the technological frameworks that support open banking. Key outcomes include a consolidated view of opportunities for innovation, collaboration among banking entities, and a prioritization matrix relevant to financial services and fintech developments.

![Open banking [Evolution, Risks & Opportunities]](https://cdn.slidesharecdn.com/ss_thumbnails/openbanking-210606160258-thumbnail.jpg?width=640&height=640&fit=bounds)

![Coded Agents – with UiPath SDK + LangGraph [Virtual Hands-on Workshop]](https://cdn.slidesharecdn.com/ss_thumbnails/codedagentsdeck-251215155422-5497c599-thumbnail.jpg?width=640&height=640&fit=bounds)

![Vibe Coding vs. Spec-Driven Development [Free Meetup]](https://cdn.slidesharecdn.com/ss_thumbnails/vibecodingvsspecdrivendevelopment-251209105622-43f455e7-thumbnail.jpg?width=640&height=640&fit=bounds)