The document outlines the foundational building blocks of a financial report:

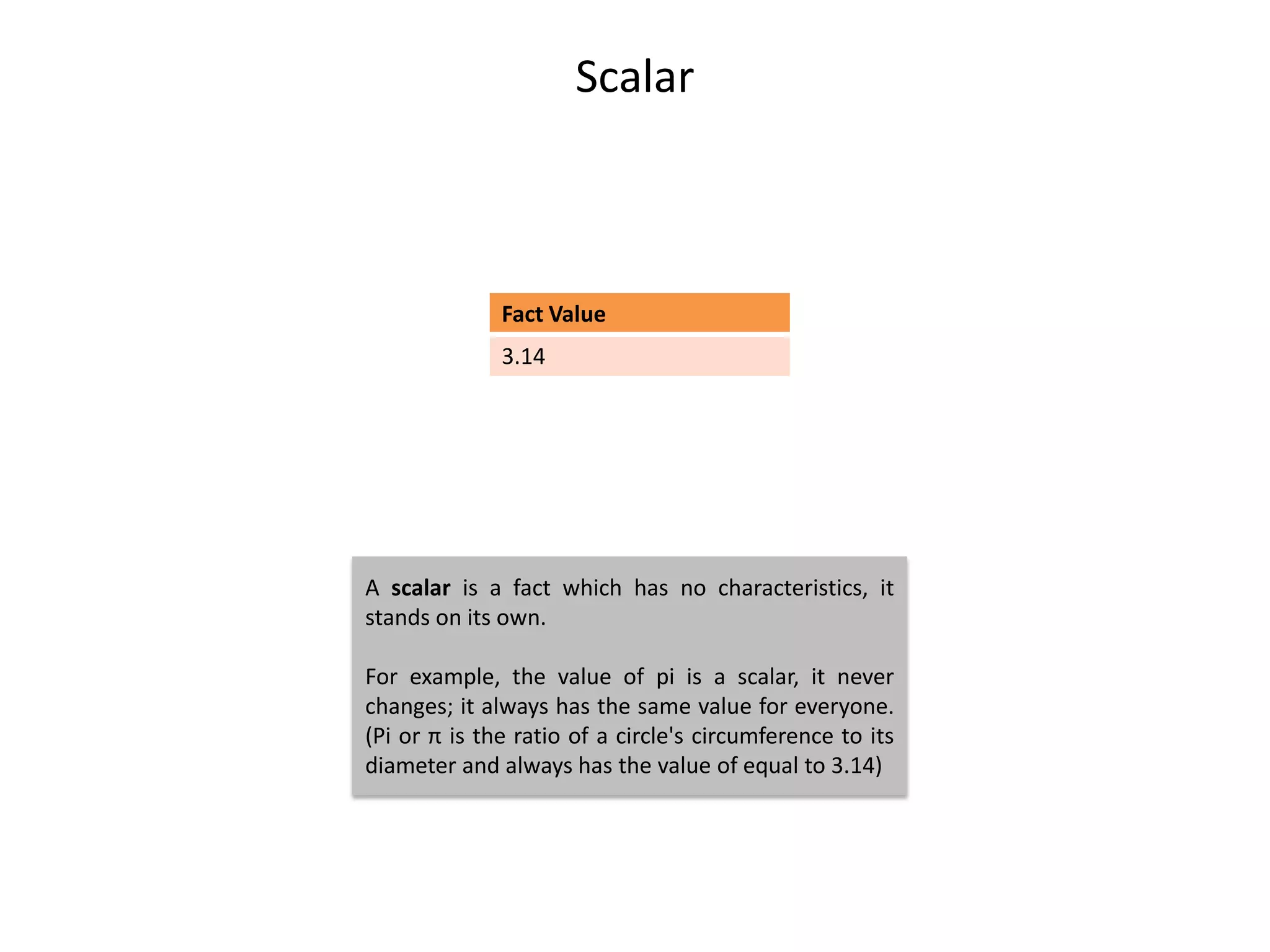

1) Scalars are standalone facts like the value of pi.

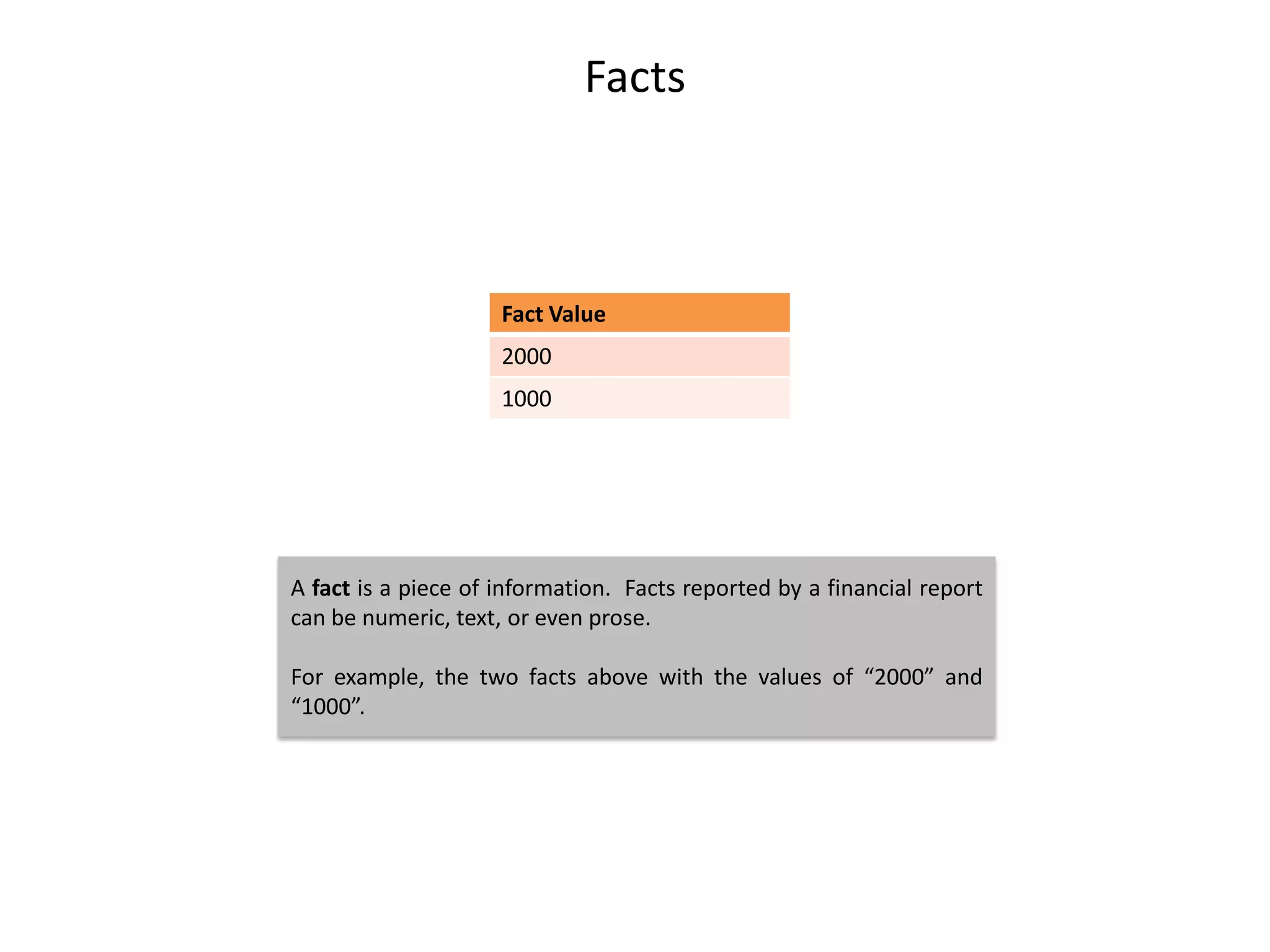

2) Facts are pieces of information reported, like revenues of 2000.

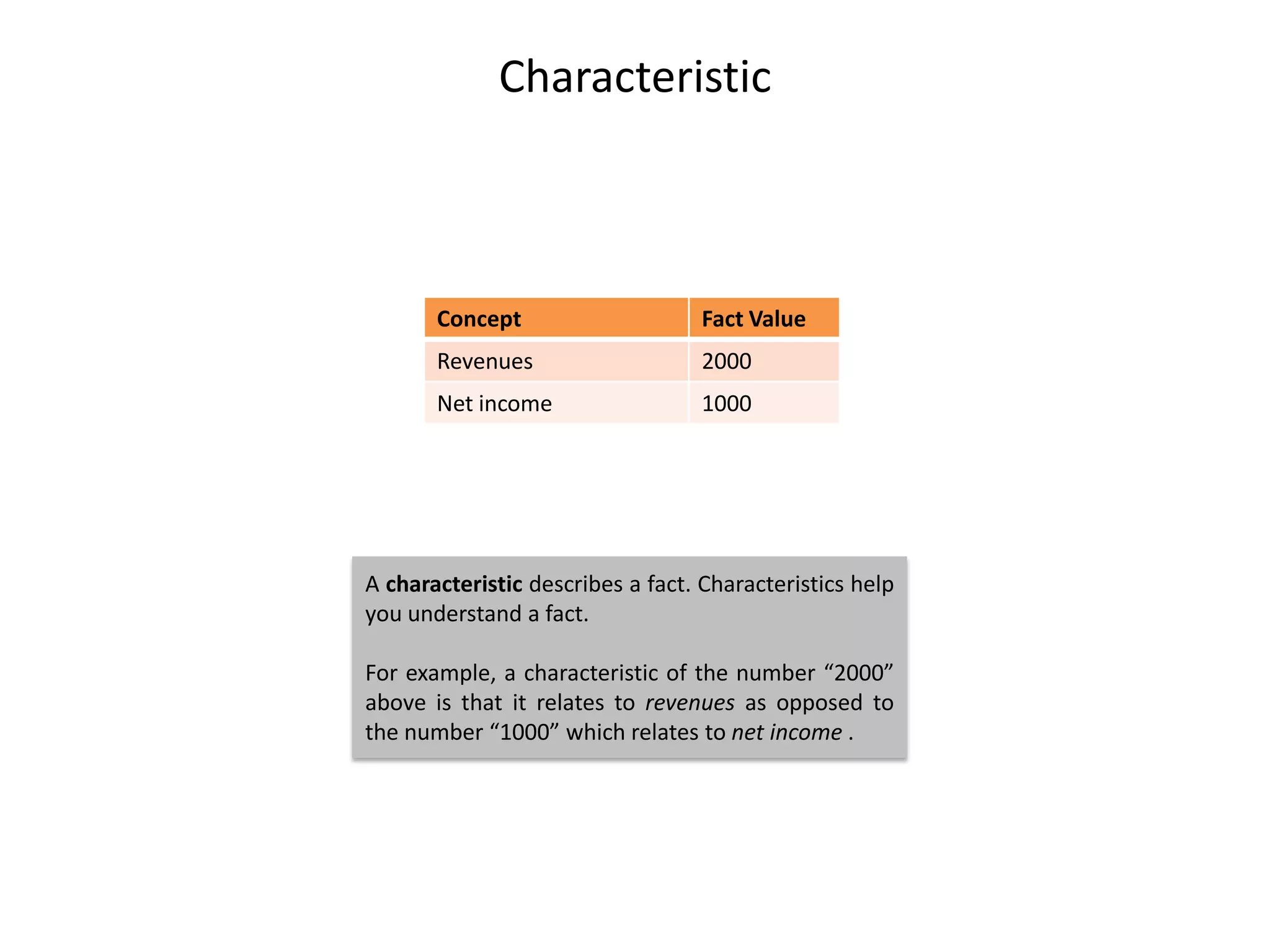

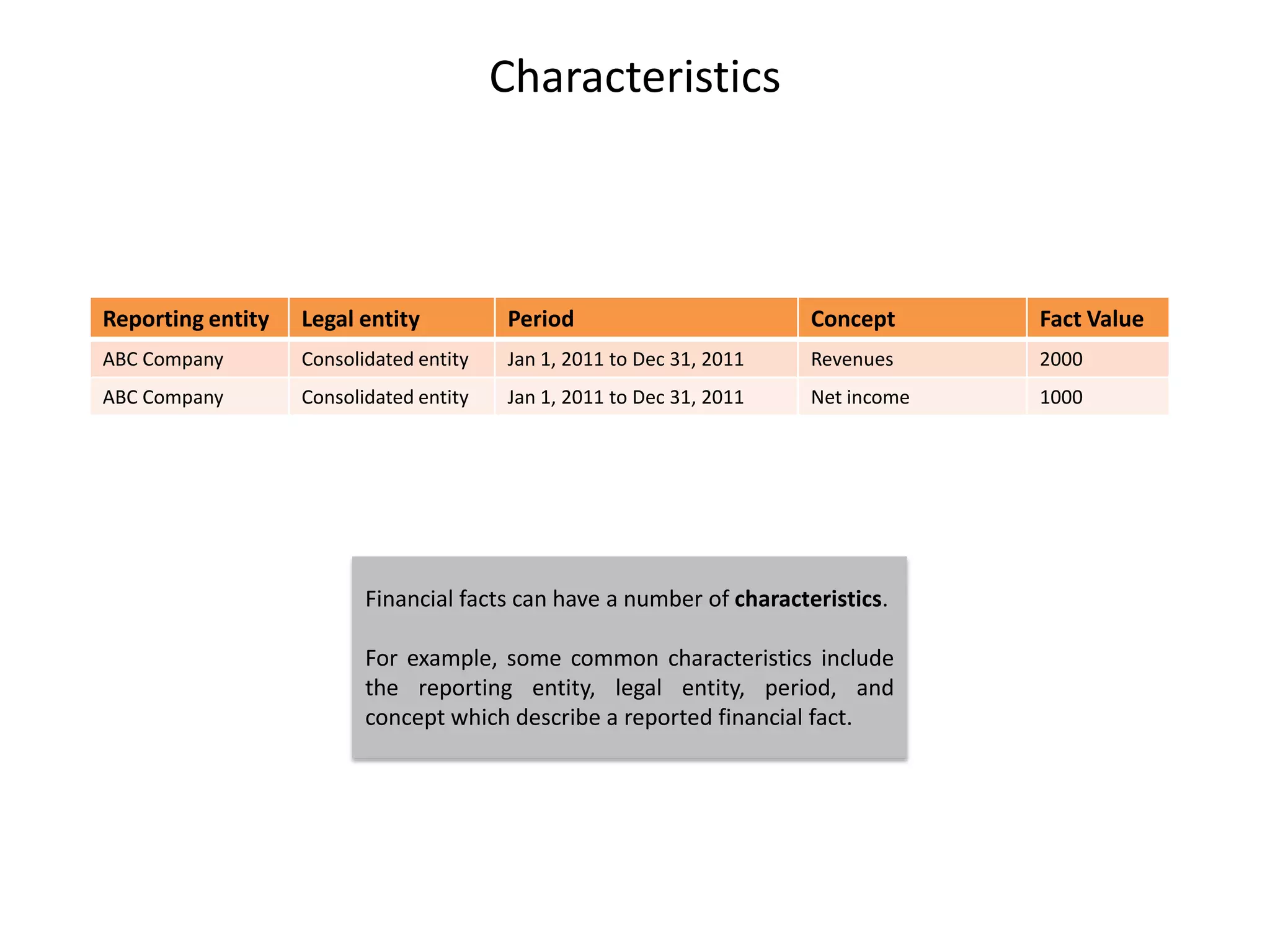

3) Characteristics describe facts, like the concept of revenues relating to the 2000 value.

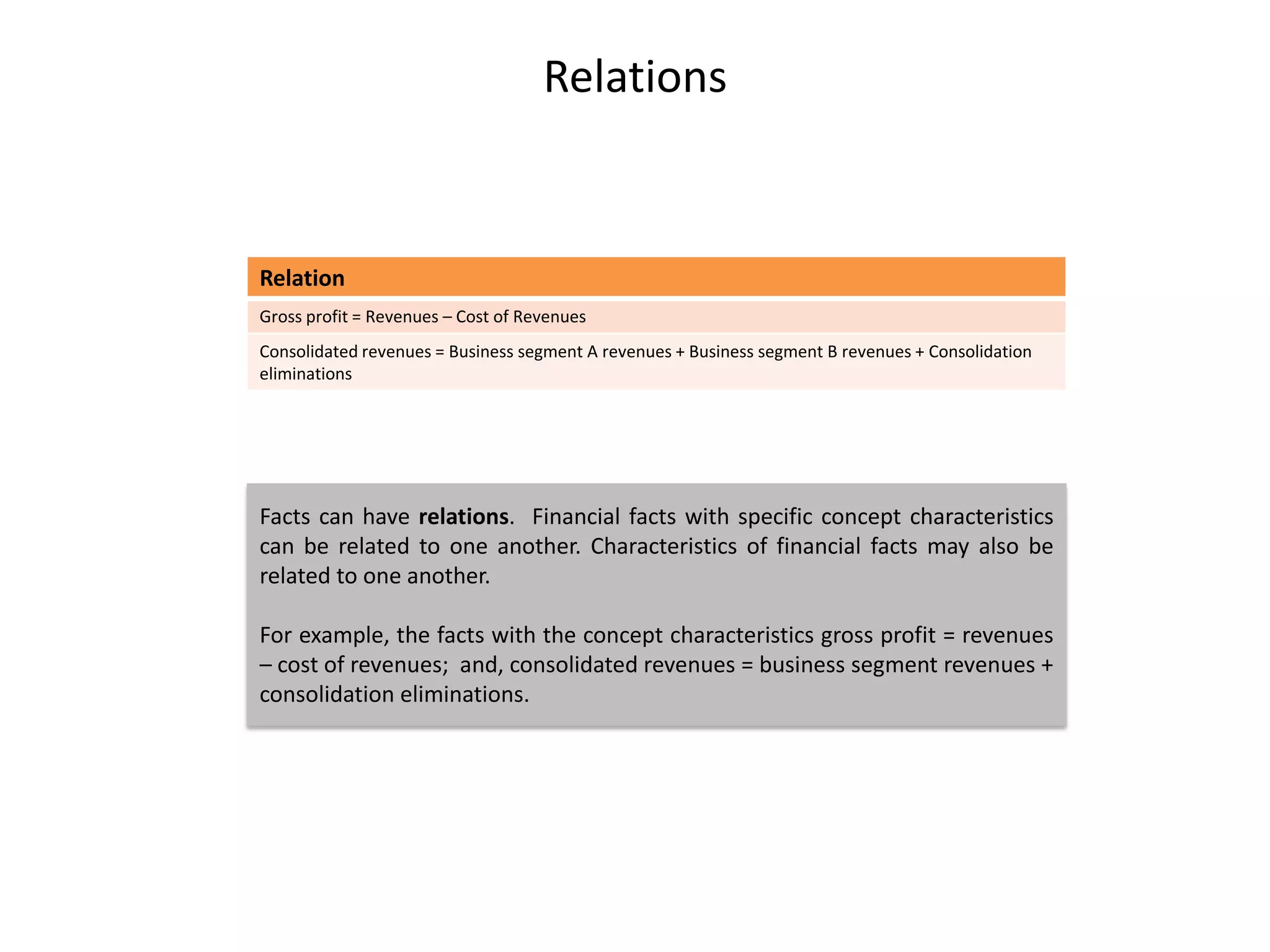

4) Relations show how facts are connected, like gross profit relating to revenues minus costs.

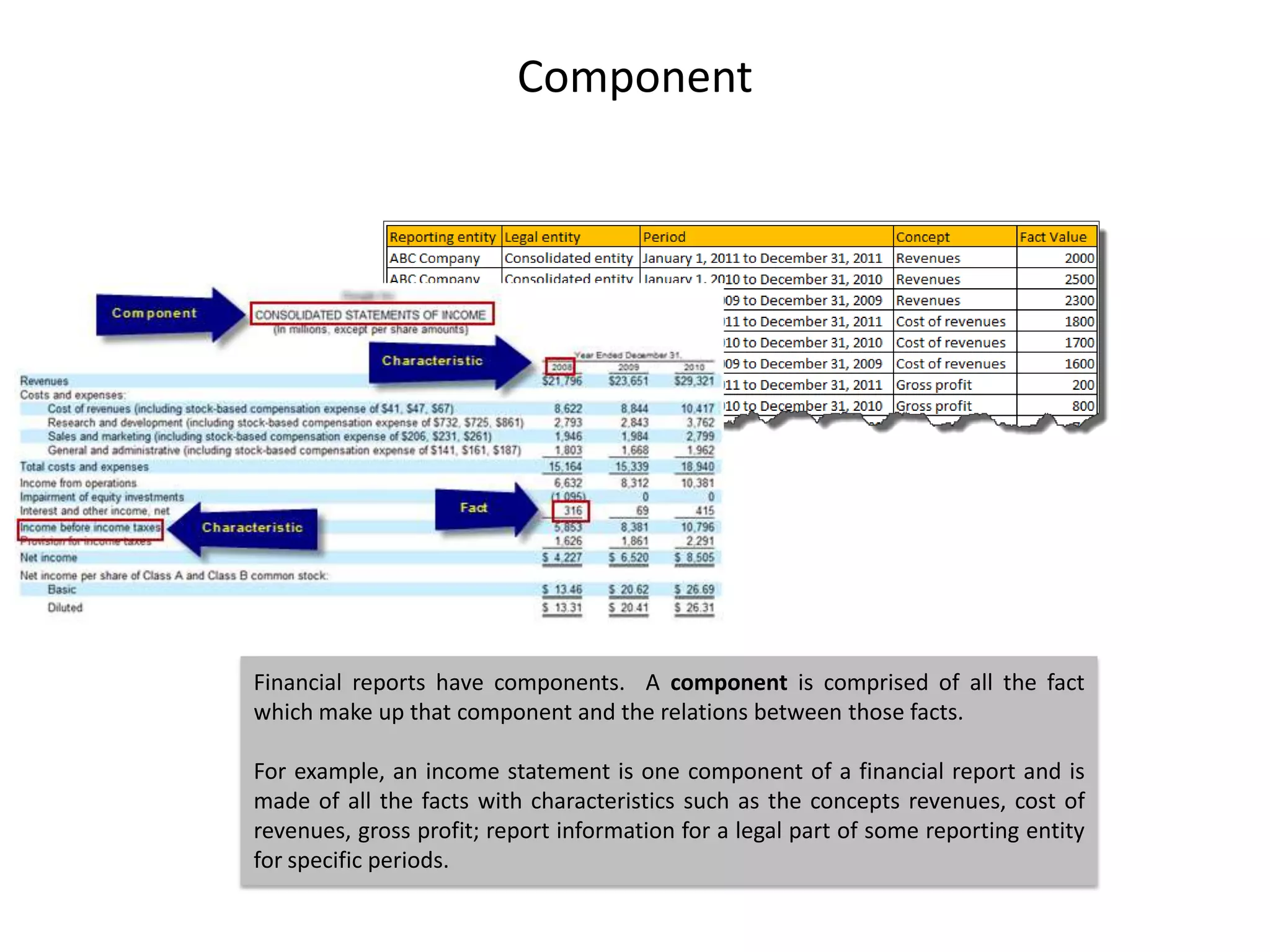

5) Components comprise related facts and make up parts of a report, like an income statement.