1) This document is an IRS Form 990-EZ, which is a simplified tax return for small tax-exempt organizations with gross receipts under $1,000,000 and total assets under $2,500,000.

2) The form collects information about the organization's revenues, expenses, programs, and leadership to determine if it qualifies for tax-exempt status.

3) Key sections include reporting of revenue sources, grants paid, program accomplishments, compensation of officers, and political/lobbying activities.

Demystifying the Form 990: Tips, Tricks, and Traps of the Form 990GuideStar

Presenters: Virginia C. Gross, Shareholder, Polsinelli PC; Dave Moja,Partner and National Director of Not-for-Profit Tax Services, Capin Crouse, and Jenny Taylor, Community Manager, GuideStar USA (moderator)

Join us for our free webinar featuring Polsinelli PC shareholder Virginia C. Gross, and Capin Crouse National Director for Not-for-Profit Tax Services Dave Moja. These leaders will present new insights from the 2015 ACT report, go over common trip up points in the Form 990, and reveal what’s new in the 2014 Form 990.

Form 990, IRS Form 990, Nonprofit Accounting, Salinas Nonprofit CPA, Salinas Nonprofit Accounting Information on the revised Form 990 from Hayashi & Wayland CPAs,

5 powerful techniques for minimizing the problems that crop up when you've got people with varying levels of skill and trustworthiness working with your QuickBooks data.

Based on QuickBooks 2014 All-in-One For Dummies by Stephen L. Nelson and published by Wiley. For more info, visit: http://bit.ly/1tXG7um

Demystifying the Form 990: Tips, Tricks, and Traps of the Form 990GuideStar

Presenters: Virginia C. Gross, Shareholder, Polsinelli PC; Dave Moja,Partner and National Director of Not-for-Profit Tax Services, Capin Crouse, and Jenny Taylor, Community Manager, GuideStar USA (moderator)

Join us for our free webinar featuring Polsinelli PC shareholder Virginia C. Gross, and Capin Crouse National Director for Not-for-Profit Tax Services Dave Moja. These leaders will present new insights from the 2015 ACT report, go over common trip up points in the Form 990, and reveal what’s new in the 2014 Form 990.

Form 990, IRS Form 990, Nonprofit Accounting, Salinas Nonprofit CPA, Salinas Nonprofit Accounting Information on the revised Form 990 from Hayashi & Wayland CPAs,

5 powerful techniques for minimizing the problems that crop up when you've got people with varying levels of skill and trustworthiness working with your QuickBooks data.

Based on QuickBooks 2014 All-in-One For Dummies by Stephen L. Nelson and published by Wiley. For more info, visit: http://bit.ly/1tXG7um

Free QuickBooks Pro, Premier Training 2013, 2014, 2015, 2016, 2017 DownloadOgechi Ndukwe

Download Free QuickBooks Training Online - Pro, Premier 2013, 2014, 2015, 2016, 2017, 2018 Tutorials. Learn How to use QuickBooks Accounting Software Quickly for Small Business. Free Training on http://computeraccountingblog.blogspot.com/

Learn about recording expenses and income, hodge-podge and basic QuickBooks reporting. Additionally you will get an insight into eighteen common QuickBooks errrors.

Webinar - QuickBooks 2016 for New Nonprofit Users - 2016-02-25TechSoup

Are you brand new to using Intuit's QuickBooks or need a basic refresher to make sure you've got your nonprofit or church set up correctly? Watch this free, 90-minute webinar that focuses on a host of beginner topics including:

-- Setting up your "company"

-- Opening balance

-- Setting up accounts

-- Setting up programs

-- Basic budgeting

This free webinar is best suited to U.S.-based nonprofits and churches who are novices or new to using QuickBooks Premier installed on your desktop.

Webinar - QuickBooks for Newer Nonprofit Desktop Users - 2016-07-19TechSoup

Visit http://www.techsoup.org for donated technology for nonprofits and libraries.

Already using Intuit's QuickBooks installed on your desktop, but still pretty new to your organization's setup? Watch QuickBooks Made Easy CEO Gregg Bossen for a fast-paced, 90-minute lesson to improve.

http://www.quickbooksmadeeasy.com

Webinar - QuickBooks 2016 for Existing Nonprofit Users - 2016-03-03TechSoup

Visit http://www.techsoup.org to learn about donated technology for nonprofits, churches, and libraries!

If you are already using Intuit's QuickBooks to manage your nonprofit or church accounting, but want to know more, this webinar is for you! Watch QuickBooks Made Easy CEO Gregg Bossen in this free 90-minute webinar. This webinar covers topics including:

-- Best practices for list setup

-- Different methods for entering income

-- Using QuickBooks as a donor database

-- Auto-allocating expenses to programs

-- Reports for your board

-- Tracking restricted grants

-- Inputting in-kind gifts

This webinar is best suited for U.S.-based nonprofit or church users of QuickBooks Premier installed on their desktops who are already using the program to manage their accounting. Attendees should already be familiar with the basics.

Closing your accounting year is a necessary function even for QuickBooks users. Although not forced like many accounting programs, QuickBooks allows you to secure your accounting data and preserve your records. This methodology can be used more frequently, but is necessary at least once per year to retain reliable accounting data.

how to swap pi coins to foreign currency withdrawable.DOT TECH

As of my last update, Pi is still in the testing phase and is not tradable on any exchanges.

However, Pi Network has announced plans to launch its Testnet and Mainnet in the future, which may include listing Pi on exchanges.

The current method for selling pi coins involves exchanging them with a pi vendor who purchases pi coins for investment reasons.

If you want to sell your pi coins, reach out to a pi vendor and sell them to anyone looking to sell pi coins from any country around the globe.

Below is the contact information for my personal pi vendor.

Telegram: @Pi_vendor_247

how to sell pi coins effectively (from 50 - 100k pi)DOT TECH

Anywhere in the world, including Africa, America, and Europe, you can sell Pi Network Coins online and receive cash through online payment options.

Pi has not yet been launched on any exchange because we are currently using the confined Mainnet. The planned launch date for Pi is June 28, 2026.

Reselling to investors who want to hold until the mainnet launch in 2026 is currently the sole way to sell.

Consequently, right now. All you need to do is select the right pi network provider.

Who is a pi merchant?

An individual who buys coins from miners on the pi network and resells them to investors hoping to hang onto them until the mainnet is launched is known as a pi merchant.

debuts.

I'll provide you the Telegram username

@Pi_vendor_247

Currently pi network is not tradable on binance or any other exchange because we are still in the enclosed mainnet.

Right now the only way to sell pi coins is by trading with a verified merchant.

What is a pi merchant?

A pi merchant is someone verified by pi network team and allowed to barter pi coins for goods and services.

Since pi network is not doing any pre-sale The only way exchanges like binance/huobi or crypto whales can get pi is by buying from miners. And a merchant stands in between the exchanges and the miners.

I will leave the telegram contact of my personal pi merchant. I and my friends has traded more than 6000pi coins successfully

Tele-gram

@Pi_vendor_247

The secret way to sell pi coins effortlessly.DOT TECH

Well as we all know pi isn't launched yet. But you can still sell your pi coins effortlessly because some whales in China are interested in holding massive pi coins. And they are willing to pay good money for it. If you are interested in selling I will leave a contact for you. Just telegram this number below. I sold about 3000 pi coins to him and he paid me immediately.

Telegram: @Pi_vendor_247

Introduction to Indian Financial System ()Avanish Goel

The financial system of a country is an important tool for economic development of the country, as it helps in creation of wealth by linking savings with investments.

It facilitates the flow of funds form the households (savers) to business firms (investors) to aid in wealth creation and development of both the parties

Falcon stands out as a top-tier P2P Invoice Discounting platform in India, bridging esteemed blue-chip companies and eager investors. Our goal is to transform the investment landscape in India by establishing a comprehensive destination for borrowers and investors with diverse profiles and needs, all while minimizing risk. What sets Falcon apart is the elimination of intermediaries such as commercial banks and depository institutions, allowing investors to enjoy higher yields.

how to sell pi coins in South Korea profitably.DOT TECH

Yes. You can sell your pi network coins in South Korea or any other country, by finding a verified pi merchant

What is a verified pi merchant?

Since pi network is not launched yet on any exchange, the only way you can sell pi coins is by selling to a verified pi merchant, and this is because pi network is not launched yet on any exchange and no pre-sale or ico offerings Is done on pi.

Since there is no pre-sale, the only way exchanges can get pi is by buying from miners. So a pi merchant facilitates these transactions by acting as a bridge for both transactions.

How can i find a pi vendor/merchant?

Well for those who haven't traded with a pi merchant or who don't already have one. I will leave the telegram id of my personal pi merchant who i trade pi with.

Tele gram: @Pi_vendor_247

#pi #sell #nigeria #pinetwork #picoins #sellpi #Nigerian #tradepi #pinetworkcoins #sellmypi

what is the future of Pi Network currency.DOT TECH

The future of the Pi cryptocurrency is uncertain, and its success will depend on several factors. Pi is a relatively new cryptocurrency that aims to be user-friendly and accessible to a wide audience. Here are a few key considerations for its future:

Message: @Pi_vendor_247 on telegram if u want to sell PI COINS.

1. Mainnet Launch: As of my last knowledge update in January 2022, Pi was still in the testnet phase. Its success will depend on a successful transition to a mainnet, where actual transactions can take place.

2. User Adoption: Pi's success will be closely tied to user adoption. The more users who join the network and actively participate, the stronger the ecosystem can become.

3. Utility and Use Cases: For a cryptocurrency to thrive, it must offer utility and practical use cases. The Pi team has talked about various applications, including peer-to-peer transactions, smart contracts, and more. The development and implementation of these features will be essential.

4. Regulatory Environment: The regulatory environment for cryptocurrencies is evolving globally. How Pi navigates and complies with regulations in various jurisdictions will significantly impact its future.

5. Technology Development: The Pi network must continue to develop and improve its technology, security, and scalability to compete with established cryptocurrencies.

6. Community Engagement: The Pi community plays a critical role in its future. Engaged users can help build trust and grow the network.

7. Monetization and Sustainability: The Pi team's monetization strategy, such as fees, partnerships, or other revenue sources, will affect its long-term sustainability.

It's essential to approach Pi or any new cryptocurrency with caution and conduct due diligence. Cryptocurrency investments involve risks, and potential rewards can be uncertain. The success and future of Pi will depend on the collective efforts of its team, community, and the broader cryptocurrency market dynamics. It's advisable to stay updated on Pi's development and follow any updates from the official Pi Network website or announcements from the team.

What website can I sell pi coins securely.DOT TECH

Currently there are no website or exchange that allow buying or selling of pi coins..

But you can still easily sell pi coins, by reselling it to exchanges/crypto whales interested in holding thousands of pi coins before the mainnet launch.

Who is a pi merchant?

A pi merchant is someone who buys pi coins from miners and resell to these crypto whales and holders of pi..

This is because pi network is not doing any pre-sale. The only way exchanges can get pi is by buying from miners and pi merchants stands in between the miners and the exchanges.

How can I sell my pi coins?

Selling pi coins is really easy, but first you need to migrate to mainnet wallet before you can do that. I will leave the telegram contact of my personal pi merchant to trade with.

Tele-gram.

@Pi_vendor_247

how to sell pi coins on Bitmart crypto exchangeDOT TECH

Yes. Pi network coins can be exchanged but not on bitmart exchange. Because pi network is still in the enclosed mainnet. The only way pioneers are able to trade pi coins is by reselling the pi coins to pi verified merchants.

A verified merchant is someone who buys pi network coins and resell it to exchanges looking forward to hold till mainnet launch.

I will leave the telegram contact of my personal pi merchant to trade with.

@Pi_vendor_247

The Evolution of Non-Banking Financial Companies (NBFCs) in India: Challenges...beulahfernandes8

Role in Financial System

NBFCs are critical in bridging the financial inclusion gap.

They provide specialized financial services that cater to segments often neglected by traditional banks.

Economic Impact

NBFCs contribute significantly to India's GDP.

They support sectors like micro, small, and medium enterprises (MSMEs), housing finance, and personal loans.

what is the best method to sell pi coins in 2024DOT TECH

The best way to sell your pi coins safely is trading with an exchange..but since pi is not launched in any exchange, and second option is through a VERIFIED pi merchant.

Who is a pi merchant?

A pi merchant is someone who buys pi coins from miners and pioneers and resell them to Investors looking forward to hold massive amounts before mainnet launch in 2026.

I will leave the telegram contact of my personal pi merchant to trade pi coins with.

@Pi_vendor_247

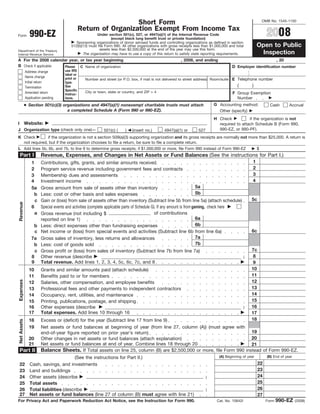

Form 990-EZ Short Form Return of Organization Exempt from Income Tax

1. Short Form OMB No. 1545-1150

Return of Organization Exempt From Income Tax

2008

990-EZ Under section 501(c), 527, or 4947(a)(1) of the Internal Revenue Code

Form

(except black lung benefit trust or private foundation)

Sponsoring organizations of donor advised funds and controlling organizations as defined in section

Open to Public

512(b)(13) must file Form 990. All other organizations with gross receipts less than $1,000,000 and total

assets less than $2,500,000 at the end of the year may use this form.

Department of the Treasury

Inspection

The organization may have to use a copy of this return to satisfy state reporting requirements.

Internal Revenue Service

A For the 2008 calendar year, or tax year beginning , 2008, and ending , 20

B Check if applicable: D Employer identification number

Please C Name of organization

use IRS

Address change

label or

Name change print or Number and street (or P.O. box, if mail is not delivered to street address) Room/suite E Telephone number

Initial return type.

( )

See

Termination

Specific City or town, state or country, and ZIP + 4

Amended return F Group Exemption

Instruc-

Application pending Number

tions.

● Section 501(c)(3) organizations and 4947(a)(1) nonexempt charitable trusts must attach G Accounting method: Cash Accrual

a completed Schedule A (Form 990 or 990-EZ). Other (specify)

H Check if the organization is not

Website:

I required to attach Schedule B (Form 990,

990-EZ, or 990-PF).

J Organization type (check only one)— 501(c) ( ) (insert no.) 4947(a)(1) or 527

K Check if the organization is not a section 509(a)(3) supporting organization and its gross receipts are normally not more than $25,000. A return is

not required, but if the organization chooses to file a return, be sure to file a complete return.

L Add lines 5b, 6b, and 7b, to line 9 to determine gross receipts; if $1,000,000 or more, file Form 990 instead of Form 990-EZ $

Part I Revenue, Expenses, and Changes in Net Assets or Fund Balances (See the instructions for Part I.)

1

1 Contributions, gifts, grants, and similar amounts received

2

2 Program service revenue including government fees and contracts

3

3 Membership dues and assessments

4

4 Investment income

5a

5a Gross amount from sale of assets other than inventory

5b

b Less: cost or other basis and sales expenses

5c

c Gain or (loss) from sale of assets other than inventory (Subtract line 5b from line 5a) (attach schedule)

Revenue

6 Special events and activities (complete applicable parts of Schedule G). If any amount is from gaming, check here

a of contributions

Gross revenue (not including $

6a

reported on line 1)

6b

b Less: direct expenses other than fundraising expenses

6c

c Net income or (loss) from special events and activities (Subtract line 6b from line 6a)

7a

7a Gross sales of inventory, less returns and allowances

7b

b Less: cost of goods sold

7c

c Gross profit or (loss) from sales of inventory (Subtract line 7b from line 7a)

8

8 Other revenue (describe )

9 Total revenue. Add lines 1, 2, 3, 4, 5c, 6c, 7c, and 8 9

10

10 Grants and similar amounts paid (attach schedule)

11

11 Benefits paid to or for members

Expenses

12

Salaries, other compensation, and employee benefits

12

13

13 Professional fees and other payments to independent contractors

14

14 Occupancy, rent, utilities, and maintenance

15

15 Printing, publications, postage, and shipping

16

16 Other expenses (describe )

17 Total expenses. Add lines 10 through 16 17

18

18 Excess or (deficit) for the year (Subtract line 17 from line 9)

Net Assets

19 Net assets or fund balances at beginning of year (from line 27, column (A)) (must agree with

19

end-of-year figure reported on prior year’s return)

20

20 Other changes in net assets or fund balances (attach explanation)

21 Net assets or fund balances at end of year. Combine lines 18 through 20 21

Balance Sheets. If Total assets on line 25, column (B) are $2,500,000 or more, file Form 990 instead of Form 990-EZ.

Part II

(A) Beginning of year (B) End of year

(See the instructions for Part II.)

22

22 Cash, savings, and investments

23

23 Land and buildings

24

24 Other assets (describe )

25

25 Total assets

26

26 Total liabilities (describe )

27 Net assets or fund balances (line 27 of column (B) must agree with line 21) 27

990-EZ

For Privacy Act and Paperwork Reduction Act Notice, see the Instruction for Form 990. Cat. No. 10642I Form (2008)

2. 2

Form 990-EZ (2008) Page

Part III Statement of Program Service Accomplishments (See the instructions for Part III.) Expenses

(Required for 501(c)(3)

What is the organization’s primary exempt purpose? and (4) organizations

Describe what was achieved in carrying out the organization’s exempt purposes. In a clear and concise manner, and 4947(a)(1) trusts;

optional for others.)

describe the services provided, the number of persons benefited, or other relevant information for each program title.

28

28a

(Grants $ ) If this amount includes foreign grants, check here

29

29a

(Grants $ ) If this amount includes foreign grants, check here

30

30a

(Grants $ ) If this amount includes foreign grants, check here

31 Other program services (attach schedule)

(Grants $ ) If this amount includes foreign grants, check here 31a

32 Total program service expenses (add lines 28a through 31a) 32

Part IV List of Officers, Directors, Trustees, and Key Employees. List each one even if not compensated. (See the instructions for Part IV.)

(d) Contributions to

(b) Title and average (c) Compensation (e) Expense

(a) Name and address employee benefit plans &

hours per week (If not paid, account and

deferred compensation

devoted to position enter -0-.) other allowances

990-EZ

Form (2008)

3. 3

Form 990-EZ (2008) Page

Other Information (Note the statement requirements in the instructions for Part VI.)

Part V

Yes No

33 Did the organization engage in any activity not previously reported to the IRS? If “Yes,” attach a detailed

33

description of each activity

34 Were any changes made to the organizing or governing documents but not reported to the IRS? If “Yes,”

34

attach a conformed copy of the changes

35 If the organization had income from business activities, such as those reported on lines 2, 6a, and 7a (among others), but

not reported on Form 990-T, attach a statement explaining your reason for not reporting the income on Form 990-T.

a Did the organization have unrelated business gross income of $1,000 or more or section 6033(e) notice, reporting,

35a

and proxy tax requirements?

35b

b If “Yes,” has it filed a tax return on Form 990-T for this year?

36 Was there a liquidation, dissolution, termination, or substantial contraction during the year? If “Yes,”

36

complete applicable parts of Schedule N

37a

37a Enter amount of political expenditures, direct or indirect, as described in the instructions.

37b

b Did the organization file Form 1120-POL for this year?

38a Did the organization borrow from, or make any loans to, any officer, director, trustee, or key employee or were

38a

any such loans made in a prior year and still unpaid at the start of the period covered by this return?

38b

b If “Yes,” complete Schedule L, Part II and enter the total amount involved

39 Section 501(c)(7) organizations. Enter:

39a

a Initiation fees and capital contributions included on line 9

39b

b Gross receipts, included on line 9, for public use of club facilities

40a Section 501(c)(3) organizations. Enter amount of tax imposed on the organization during the year under:

section 4911 ; section 4912 ; section 4955

Section 501(c)(3) and (4) organizations. Did the organization engage in any section 4958 excess benefit transaction

b

during the year or did it become aware of an excess benefit transaction from a prior year? If “Yes,” complete Schedule

40b

L, Part I

c Enter amount of tax imposed on organization managers or disqualified persons during

the year under sections 4912, 4955, and 4958

d Enter amount of tax on line 40c reimbursed by the organization

e All organizations. At any time during the tax year, was the organization a party to a prohibited tax shelter

40e

transaction? If “Yes,” complete Form 8886-T.

41 List the states with which a copy of this return is filed.

( )

Telephone no.

42a The books are in care of

Located at ZIP + 4

b At any time during the calendar year, did the organization have an interest in or a signature or other authority

Yes No

over a financial account in a foreign country (such as a bank account, securities account, or other financial

42b

account)?

If “Yes,” enter the name of the foreign country:

See the instructions for exceptions and filing requirements for Form TD F 90-22.1, Report of Foreign Bank

and Financial Accounts.

42c

c At any time during the calendar year, did the organization maintain an office outside of the U.S.?

If “Yes,” enter the name of the foreign country:

43 Section 4947(a)(1) nonexempt charitable trusts filing Form 990-EZ in lieu of Form 1041—Check here

43

and enter the amount of tax-exempt interest received or accrued during the tax year

Yes No

Did the organization maintain any donor advised funds? If “Yes,” Form 990 must be completed instead of

44

44

Form 990-EZ

Is any related organization a controlled entity of the organization within the meaning of section 512(b)(13)? If

45

“Yes,” Form 990 must be completed instead of Form 990-EZ 45

990-EZ

Form (2008)

4. Page 4

Form 990-EZ (2008)

Section 501(c)(3) organizations only. All section 501(c)(3) organizations must answer questions 46–49

Part VI

and complete the tables for lines 50 and 51.

Yes No

46 Did the organization engage in direct or indirect political campaign activities on behalf of or in opposition to

46

candidates for public office? If “Yes,” complete Schedule C, Part I

47

47 Did the organization engage in lobbying activities? If “Yes,” complete Schedule C, Part II

48

48 Is the organization operating a school as described in section 170(b)(1)(A)(ii)? If “Yes,” complete Schedule E

49a

49a Did the organization make any transfers to an exempt non-charitable related organization?

49b

b If “Yes,” was the related organization(s) a section 527 organization?

50 Complete this table for the five highest compensated employees (other than officers, directors, trustees and key employees) who

each received more than $100,000 of compensation from the organization. If there is none, enter “None.”

(d) Contributions to

(b) Title and average (c) Compensation (e) Expense

(a) Name and address of each employee paid more employee benefit plans &

hours per week account and

than $100,000 deferred compensation

devoted to position other allowances

Total number of other employees paid over $100,000

51 Complete this table for the five highest compensated independent contractors who each received more than $100,000 of

compensation from the organization. If there is none, enter “None.”

(a) Name and address of each independent contractor paid more than $100,000 (b) Type of service (c) Compensation

Total number of other independent contractors each receiving over $100,000

Under penalties of perjury, I declare that I have examined this return, including accompanying schedules and statements, and to the best of my knowledge

and belief, it is true, correct, and complete. Declaration of preparer (other than officer) is based on all information of which preparer has any knowledge.

Sign

Here Signature of officer Date

Type or print name and title.

Check if

Date Preparer’s Identifying Number (See instructions)

Preparer’s

Paid self-

signature employed

Preparer’s Firm’s name (or yours EIN

Use Only if self-employed),

( )

Phone no.

address, and ZIP + 4

May the IRS discuss this return with the preparer shown above? See instructions Yes No

990-EZ

Form (2008)