Portuguese Personal Income Taxation of Non-Portuguese Investment Fund (IF) distributions under the Non-habitual tax resident (NHR) regime - 09.12.2021

•

0 likes•685 views

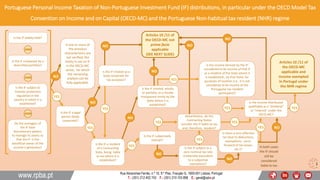

The Portuguese Personal Income Taxation of Non-Portuguese Investment Fund (IF) distributions, in particular under the OECD Model Tax Convention on Income and on Capital (OECD-MC) and the Portuguese Non-habitual tax resident (NHR) regime, is a complex topic, namely due to the diversity of legal and tax status among IFs. RPBA’s Infographic provides a step-by-step questionnaire for an accurate and full analysis of the matter.

Recommended

Recommended

More Related Content

What's hot

What's hot (20)

Similar to Portuguese Personal Income Taxation of Non-Portuguese Investment Fund (IF) distributions under the Non-habitual tax resident (NHR) regime - 09.12.2021

Similar to Portuguese Personal Income Taxation of Non-Portuguese Investment Fund (IF) distributions under the Non-habitual tax resident (NHR) regime - 09.12.2021 (20)

Recently uploaded

Recently uploaded (20)

Portuguese Personal Income Taxation of Non-Portuguese Investment Fund (IF) distributions under the Non-habitual tax resident (NHR) regime - 09.12.2021

- 1. Is the IF widely-held? Is the IF composed by a diversified portfolio? Is the IF subject to investor protection regulation in the country in which it is established? Do the managers of the IF have discretionary powers to manage its assets so that the IF is the beneficial owner of the income it generates? If one or more of the previous characteristics are not verified, the entity is not an IF in the OECD-MC sense, for which the remaining analysis can be fully applicable. NO YES NO YES YES NO Rua Abranches Ferrão, n.º 10, 9.º Piso, Fracção G, 1600-001 Lisboa, Portugal T.: (351) 212 402 743 F.: (351) 210 103 898 E.: geral@rpba.pt NO YES Is the IF a legal person (body corporate)? YES NO Is the IF treated as a body corporate for tax purposes? Is the IF treated, wholly or partially, as a fiscally transparent entity by the State where it is established? Is the IF subjectively exempt? Is the IF a resident of a Contracting State, being liable to tax where it is established? NO YES Nevertheless, do the Contracting States consider the IF liable to tax and, therefore, resident? Is there a zero-effective tax (due to deductions, exemptions, carry- forward of tax losses, etc.)? Is the income derived by the IF considered to be income of that IF as a resident of the State where it is established , by that State, for purposes of taxation (i.e., it is not considered to be income of the Portuguese tax resident participant)? NO Is the income distributed qualifiable as a “dividend” or “interest” under the OECD-MC? Is the IF subject to a zero nominal tax rate (materially equivalent to a subjective exemption)? YES NO NO YES In both cases the IF should still be considered liable to tax YES YES NO Articles 10 /11 of the OECD-MC applicable and income exempted in Portugal under the NHR regime YES Portuguese Personal Income Taxation of Non-Portuguese Investment Fund (IF) distributions, in particular under the OECD Model Tax Convention on Income and on Capital (OECD-MC) and the Portuguese Non-habitual tax resident (NHR) regime 1 AND AND Articles 10 /11 of the OECD-MC not prima facie applicable (SEE NEXT SLIDE) AND

- 2. Rua Abranches Ferrão, n.º 10, 9.º Piso, Fracção G, 1600-001 Lisboa, Portugal T.: (351) 212 402 743 F.: (351) 210 103 898 E.: geral@rpba.pt Articles 10 / 11 of the OECD-MC not prima facie applicable Given the structure through which the income is generated (e.g., a fixed place of business), can it still be considered as originating from the State where the IF is established (Source State)? Does the “Other income” provision of the real Double Taxation Convention (DTC) at stake follow article 21 of the OECD-MC? Does the “Other income” provision of the DTC allow the State where the IF is established (Source State) to tax this income, alongside the Residence State of the Portuguese tax resident participant? YES YES YES NO NO Income exempted in Portugal under the NHR regime Income taxable in Portugal at a 28% tax rate NO DISCLAIMER: This infographic is updated until December 9th, 2021. Although great care has been taken when drafting this infographic, Ricardo da Palma Borges & Associados (RPBA) - Sociedade de Advogados, S.P., R.L. does not accept any responsibility whatsoever for any consequences arising from the use of the information contained herein. Such information is provided solely for general purposes and cannot be regarded as legal or other advice. You are strongly recommended to take professional legal advice appropriate for your case before taking any decisions. 2 Portuguese Personal Income Taxation of Non-Portuguese Investment Fund (IF) distributions, in particular under the OECD Model Tax Convention on Income and on Capital (OECD-MC) and the Portuguese Non-habitual tax resident (NHR) regime