VAT and Tax Govt. Treasury Deposit Code - Bangladesh

•

1 like•7,223 views

Govt. treasury code for VAT and Tax deposit

Recommended

More Related Content

What's hot

What's hot (20)

VAT and Tax Govt. Treasury Deposit Code - Bangladesh

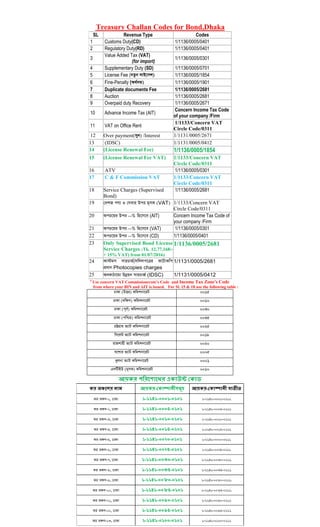

- 1. Treasury Challan Codes for Bond,Dhaka SL Revenue Type Codes 1 Customs Duty(CD) 1/1136/0005/0401 2 Regulatory Duty(RD) 1/1136/0005/0401 3 Value Added Tax (VAT) (for import) 1/1136/0005/0301 4 Supplementary Duty (SD) 1/1136/0005/0701 5 License Fee (bZzb jvB‡mÝ) 1/1136/0005/1854 6 Fine-Penalty (A_©`Û) 1/1136/0005/1901 7 Duplicate documents Fee 1/1136/0005/2681 8 Auction 1/1136/0005/2681 9 Overpaid duty Recovery 1/1136/0005/2671 10 Advance Income Tax (AIT) Concern Income Tax Code of your company /Firm 11 VAT on Office Rent 1/1133/Concern VAT Circle Code/0311 12 Over payment(my`) /Interest 1/1131/0005/2671 13 (IDSC) 1/1131/0005/0412 14 (License Renewal Fee) 1/1136/0005/1854 15 (License Renewal Fee VAT) 1/1133/Concern VAT Circle Code/0311 16 ATV 1/1136/0005/0301 17 C & F Commission VAT 1/1133/Concern VAT Circle Code/0311 18 Service Charges (Supervised Bond) 1/1136/0005/2681 19 †`kR cY¨ I †mevi Dci g~mK (VAT) 1/1133/Concern VAT Circle Code/0311 20 AcP‡qi Dci --% wn‡m‡e (AIT) Concern Income Tax Code of your company /Firm 21 AcP‡qi Dci --% wn‡m‡e (VAT) 1/1136/0005/0301 22 AcP‡qi Dci --% wn‡m‡e (CD) 1/1136/0005/0401 23 Only Supervised Bond License Service Charges (Tk. 12,77,168/- + 15% VAT) from 01/07/2016) 1/1136/0005/2681 24 Kv÷gm mviPvR©/`wjjc‡Îi d‡UvKwc cÖ`vb Photocopies charges 1/1131/0005/2681 25 AeKvVv‡gv Dbœqb mviPvR© (IDSC) 1/1131/0005/0412 # Use concern VAT Commissionerate's Code and Income Tax Zone's Code from where your BIN and AIT is issued. For Sl. 15 & 18 use the following table : XvKv (DËi) Kwgkbv‡iU 0015 XvKv (`w¶Y) Kwgkbv‡iU 0010 XvKv (c~e©) Kwgkbv‡iU 0030 XvKv (cwðg) Kwgkbv‡iU 0035 PÆMÖvg f¨vU Kwgkbv‡iU 0025 wm‡jU f¨vU Kwgkbv‡iU 0018 ivRkvnx f¨vU Kwgkbv‡iU 0020 h‡kvi f¨vU Kwgkbv‡iU 0005 Lyjbv f¨vU Kwgkbv‡iU 0001 GjwUBD (g~mK) Kwgkbv‡iU 0010 আয়কর পররশ োশের একোউন্ট ককোড কর অঞ্চশের নোম আয়কর-ককোম্পোনীসমূহ আয়কর-ককোম্পোনী ব্যতীত কর অঞ্চল-১, ঢাকা ১-১১৪১-০০০১-০১০১ ১-১১৪১-০০০১-০১১১ কর অঞ্চল-২, ঢাকা ১-১১৪১-০০০৫-০১০১ ১-১১৪১-০০০৫-০১১১ কর অঞ্চল-৩, ঢাকা ১-১১৪১-০০১০-০১০১ ১-১১৪১-০০১০-০১১১ কর অঞ্চল-৪, ঢাকা ১-১১৪১-০০১৫-০১০১ ১-১১৪১-০০১৫-০১১১ কর অঞ্চল-৫, ঢাকা ১-১১৪১-০০২০-০১০১ ১-১১৪১-০০২০-০১১১ কর অঞ্চল-৬, ঢাকা ১-১১৪১-০০২৫-০১০১ ১-১১৪১-০০২৫-০১১১ কর অঞ্চল-৭, ঢাকা ১-১১৪১-০০৩০-০১০১ ১-১১৪১-০০৩০-০১১১ কর অঞ্চল-৮, ঢাকা ১-১১৪১-০০৩৫-০১০১ ১-১১৪১-০০৩৫-০১১১ কর অঞ্চল-৯, ঢাকা ১-১১৪১-০০৮০-০১০১ ১-১১৪১-০০৮০-০১১১ কর অঞ্চল-১০, ঢাকা ১-১১৪১-০০৮৫-০১০১ ১-১১৪১-০০৮৫-০১১১ কর অঞ্চল-১১, ঢাকা ১-১১৪১-০০৯০-০১০১ ১-১১৪১-০০৯০-০১১১ কর অঞ্চল-১২, ঢাকা ১-১১৪১-০০৯৫-০১০১ ১-১১৪১-০০৯৫-০১১১ কর অঞ্চল-১৩, ঢাকা ১-১১৪১-০১০০-০১০১ ১-১১৪১-০১০০-০১১১

- 2. কর অঞ্চল-১৪, ঢাকা ১-১১৪১-০১০৫-০১০১ ১-১১৪১-০১০৫-০১১১ কর অঞ্চল-১৫, ঢাকা ১-১১৪১-০১১০-০১০১ ১-১১৪১-০১১০-০১১১ কর অঞ্চল-নারায়ণগজ্ঞ ১-১১৪১-০১১৫-০১০১ ১-১১৪১-০১১৫-০১১১ কর অঞ্চল-গাজীপুর ১-১১৪১-০১২০-০১০১ ১-১১৪১-০১২০-০১১১ কর অঞ্চল-ময়মনস িংহ ১-১১৪১-০১২৫-০১০১ ১-১১৪১-০১২৫-০১১১ কর আপীল অঞ্চল-১, ঢাকা কর আপীল অঞ্চল-২, ঢাকা কর আপীল অঞ্চল-৩, ঢাকা কর আপীল অঞ্চল-৪, ঢাকা কর আপীল অঞ্চল-রাজশাহী বৃহৎ করদাতা ইউসনট ১-১১৪৫-০০১০-০১০১ ১-১১৪৫-০০১০-০১১১ ককন্দ্রীয় জরীপ অঞ্চল ১-১১৪৫-০০০৫-০১০১ ১-১১৪৫-০০০৫-০১১১ ট্রাইবুনাল