Download to read offline

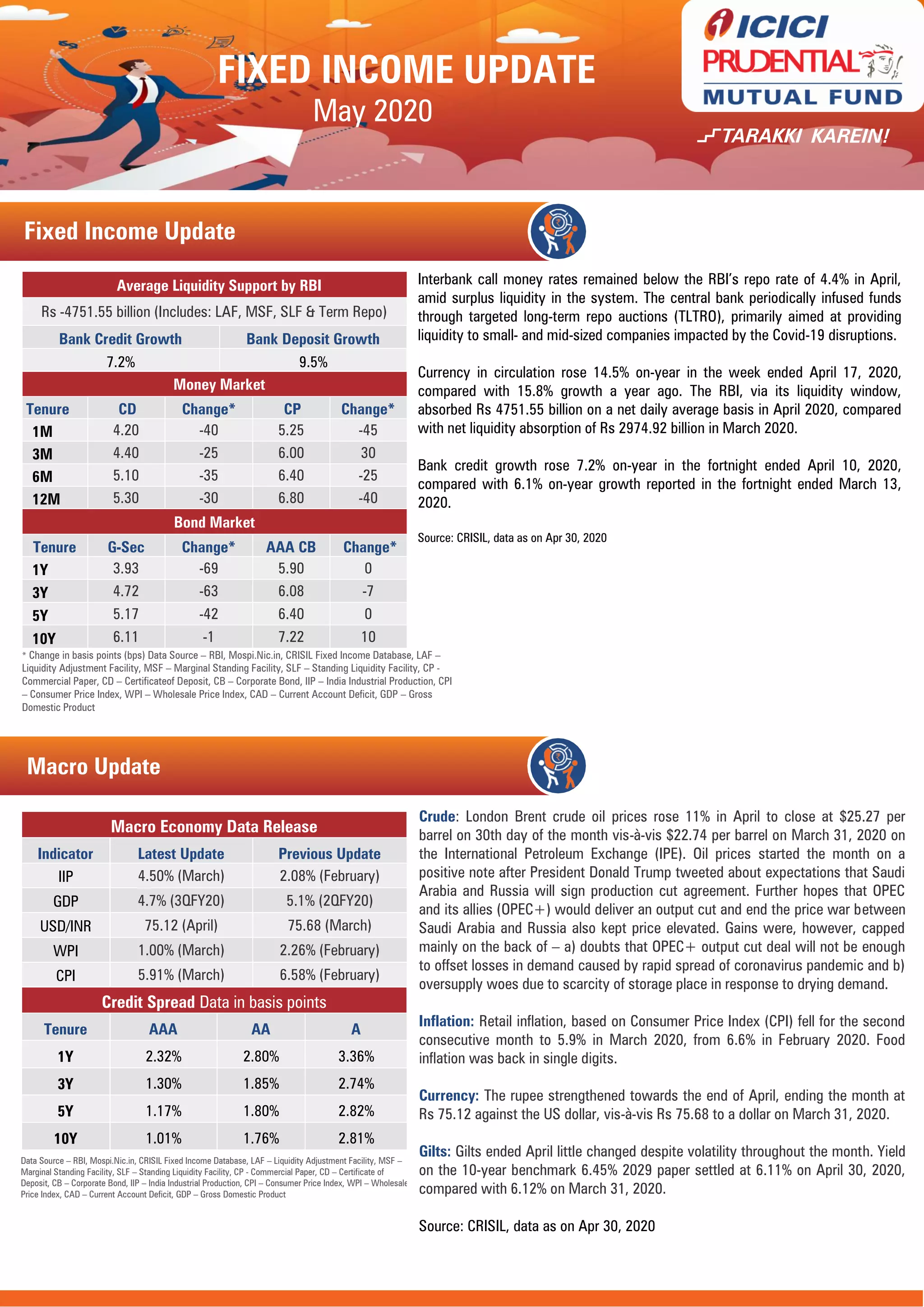

In May 2020, interbank call money rates remained below the RBI's repo rate due to excess liquidity influenced by TLTROs aimed at supporting companies affected by COVID-19, as bank credit growth rose to 7.2% year-on-year. The RBI absorbed significant liquidity through various facilities while retail inflation declined to 5.9%. Looking ahead, a combination of fiscal and monetary policies is expected to mitigate economic shocks and support bond markets.