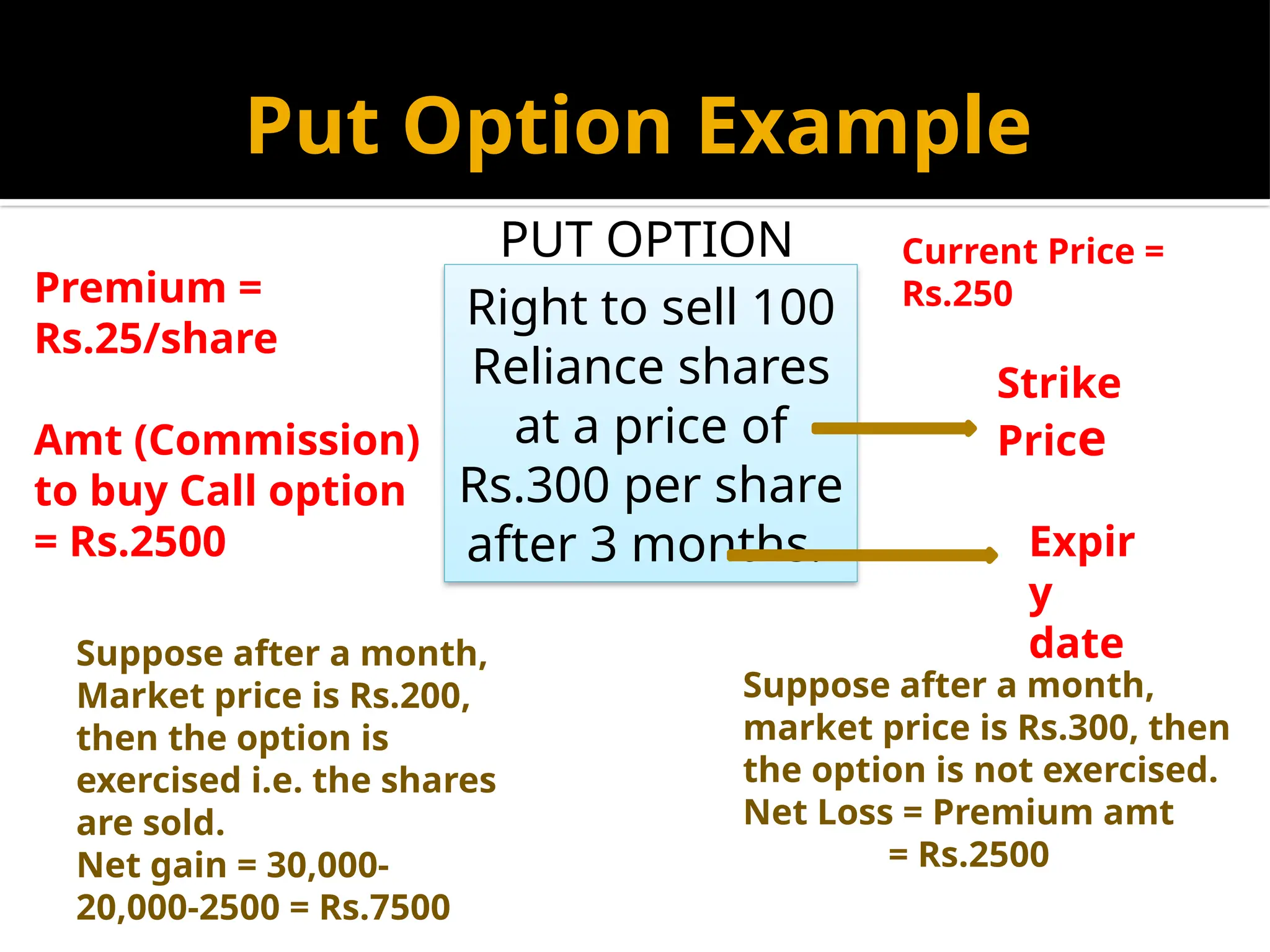

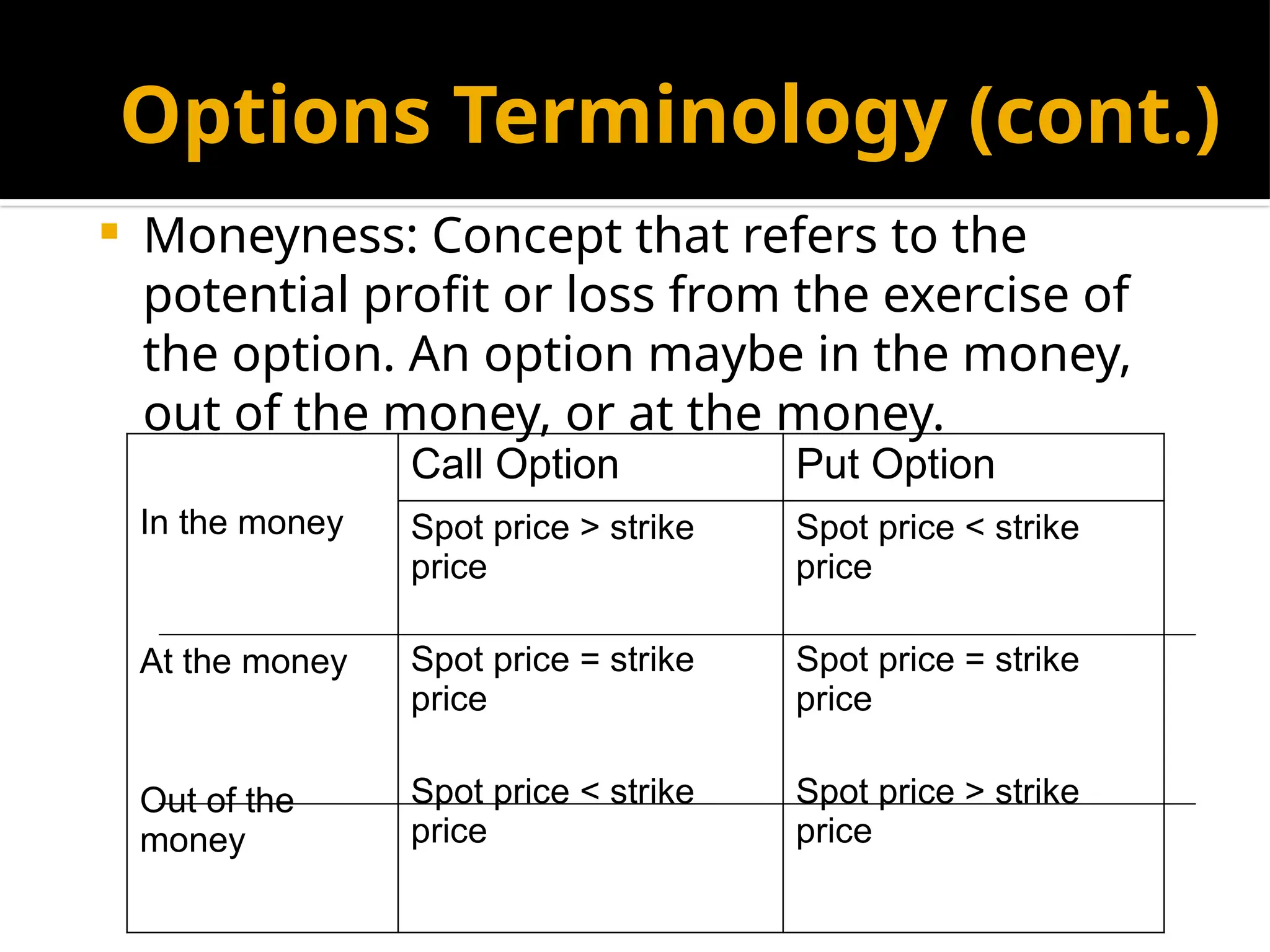

The document provides an overview of financial derivatives, defining them as contracts whose value is derived from underlying assets, and explaining various types such as futures, forwards, options, and swaps. It discusses the roles of different market participants including hedgers, speculators, and arbitragers, along with detailing the benefits and mechanisms of trading both over-the-counter and exchange-traded derivatives. Key concepts such as margin requirements, pricing dynamics, and the implications of market price fluctuations are also addressed.

![Scenario 1

If LIBOR rises by 0.75% per year, Company ABC's total

interest payments to its bond holders over the five-

year period are $225,000. Let's break down the

calculation. At year 1, the interest rate will be 1.7%;

Year 2 = 1.7% + 0.75% = 2.45%

Year 3 = 2.45% + 0.75% = 3.2%

Year 4 = 3.2% + 0.75% = 3.95%

Year 5 = 3.95% + 0.75% = 4.7%

$225,000 = $1,000,000 x [(5 x 0.013) + 0.017 + 0.0245

+ 0.032 + 0.0395 + 0.047]

In other words, $75,000 more than the $150,000 that

ABC would have paid if LIBOR had remained flat:](https://image.slidesharecdn.com/financialderivativesppt-meaningantype1read-only-240812101317-b6bfd4d2/75/financialderivativesppt-Meaning_an_type-1-Read-Only-pptx-45-2048.jpg)

![Scenario 2

In the second scenario, LIBOR rises by 2% a year.

Therefore, Year 1 interest payments rate is 1.7%;

Year 2 = 1.7% + 2% = 3.7%

Year 3 = 3.7% + 2% = 5.7%

Year 4 = 5.7% + 2% = 7.7%

Year 5 = 7.7% + 2% = 9.7%

This brings ABC's total interest payments to bond holders

to $350,000

$350,000 = $1,000,000 x [(5 x 0.013) + 0.017 + 0.037 +

0.057 + 0.077 + 0.097]

XYZ pays this amount to ABC, and ABC pays XYZ $300,000

in return. ABC's net gain on the swap is $50,000.](https://image.slidesharecdn.com/financialderivativesppt-meaningantype1read-only-240812101317-b6bfd4d2/75/financialderivativesppt-Meaning_an_type-1-Read-Only-pptx-46-2048.jpg)

![Battery Testing Lab Panjab University[1][1].pptx](https://cdn.slidesharecdn.com/ss_thumbnails/batterytestinglabpanjabuniversity11-250326083454-8917358f-thumbnail.jpg?width=640&height=640&fit=bounds)