1) A rational economic agent in a two-period economy without capital markets must decide how to allocate their initial endowment income between current and future consumption. They do this by analyzing indifference curves and comparing their subjective rate of time preference to production opportunities.

2) With capital markets, the agent can borrow or lend at the market interest rate. This creates a capital market line that allows higher utility. The agent invests until the marginal rate of return equals the interest rate, then borrows along the capital market line until their time preference equals the interest rate.

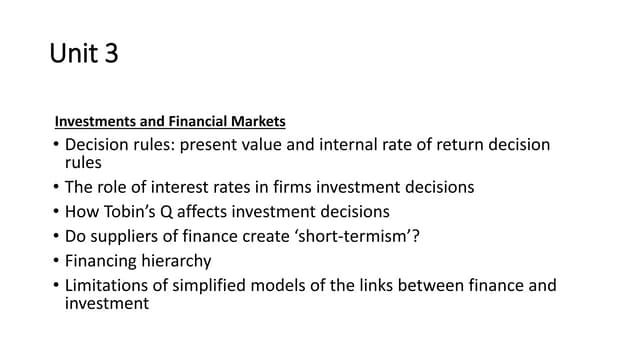

3) The maximum the businessman will pay for insurance is £114,941.55 if he has logarithmic utility. His expected wealth is £170,

![3. If an individual has logarithmic utility and (Markowitz and cost of gamble) risk

premiafor the following gambles: (1) No initial wealth and gamble .8 prob. to obtain 10

and .2 prob. to obtain 40; (2) Current wealth 20 and gamble .1 prob. to obtain additional

20 and .9 prob. to obtain additional 90; (3) Current wealth 20000 and gamble .8 prob . to

lose 4000 and .2 prob. to lose 10000. Compare the two risk premia for each example.

i).

Current wealth=0

80% chance to gain £10

20% chance to gain £40

E(W)= 0.8*10+0.2*40= 16

E[U(W)]=0.8*ln(10)+0.2*ln(40)= 1.84+0.74=2.58

Wc= exp(2.58)= 13.20

W=E(W) because the expected change in wealth is zero.

Markowitz risk premium= E(W)-Wc=16-13.2=£2.80

Cost of gamble= W-Wc= 16-13.2=£2.80

Therefore there is no difference between the risk premium and the cost of gamble. As both

outcomes of the gamble are positive, this individual would be willing to pay up to £2.80 in

order to take this gamble.

ii).

Current wealth= £20

10% chance to gain +£20

90% chance to gain +£90

E(W)=0.1*20+0.9*90= 2+81= 83

E[U(W)]=0.1*[ln(20+20)]+0.9*[ln(20+90)]=4.60

Markowitz risk premium= 83-99.48= -£16.48

This individual would need to be paid £16.48 for him to not take the gamble.

Cost of gamble= 20 – 99.48= -£79.48

iii).

Current wealth= £20,000

80% chance to lose £4,000

20% chance to lose £10,000

E(W)= 0.8*16000+0.2*10000=14800.

E[U(W)]= 0.8*(ln16000)+0.2*(ln10000)=7.74+1.84=9.58

Markowitz risk premium= 14,800-14,472.42= £327.58.](https://image.slidesharecdn.com/financialeconomicscoursework1-120711152838-phpapp02/85/Financial-economics-coursework-1-9-320.jpg)

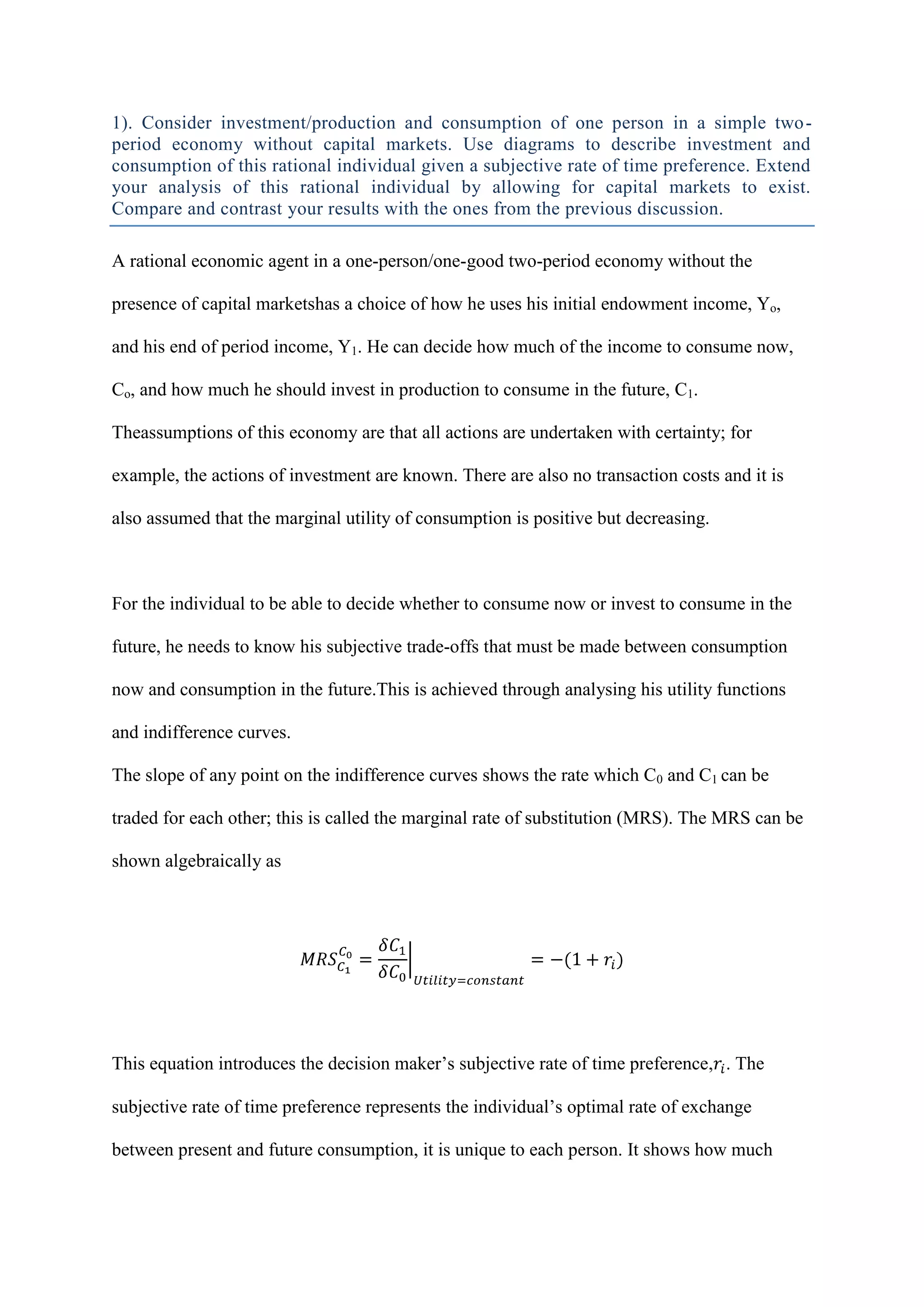

![6. A businessman faces a 10 % chance of having a fire that will reduce his net

wealth to £ 1, a 10 % chance that fire will reduce it to £ 100,000, and an 80 % chance

that nothing detrimental will happen, so that his business will retain its worth (£

200,000). What is the maximum amount he will pay for insurance if he has logarithmic

utility function U(W) = ln(W)? Explain your answer in detail.

Current wealth= £200,000

Gamble:

10% chance to be worth £1

10% chance to be worth £100,000

80% chance to be worth £200,000

E(W)= (0.1*1)+(0.1*100,000)+(0.8*200,000)= £170,000.10

E[U(W)]= (0.1*ln[1])+(0.1*ln[100,000])+(0.8*ln[200,000])=10.91615066

Wc = e10.91615066 = 55,058.45

The maximum risk premium that the business man is willing to pay is:

The Markowitz risk premium has been used to calculate the business man’s maximum risk premium

because by definition the Markowitz risk premium is the maximum amount of money that he would

pay to insure against the gamble. So this businessman is willing to pay an insurance premium up to

£114,941.55 to protect against fires.](https://image.slidesharecdn.com/financialeconomicscoursework1-120711152838-phpapp02/85/Financial-economics-coursework-1-16-320.jpg)